Leeham News and Analysis

There's more to real news than a news release.

Airbus/Boeing production rates forecast through 2020

Subscription Required.

Introduction

Feb. 3, 2015: Boeing out-delivered Airbus in 2014, for the second year in a row, as the 787 program improved in delivery rates and before the A350 made its first delivery in December.

Topping Airbus in deliveries allowed Boeing to claim it is the world’s leading ![]() commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

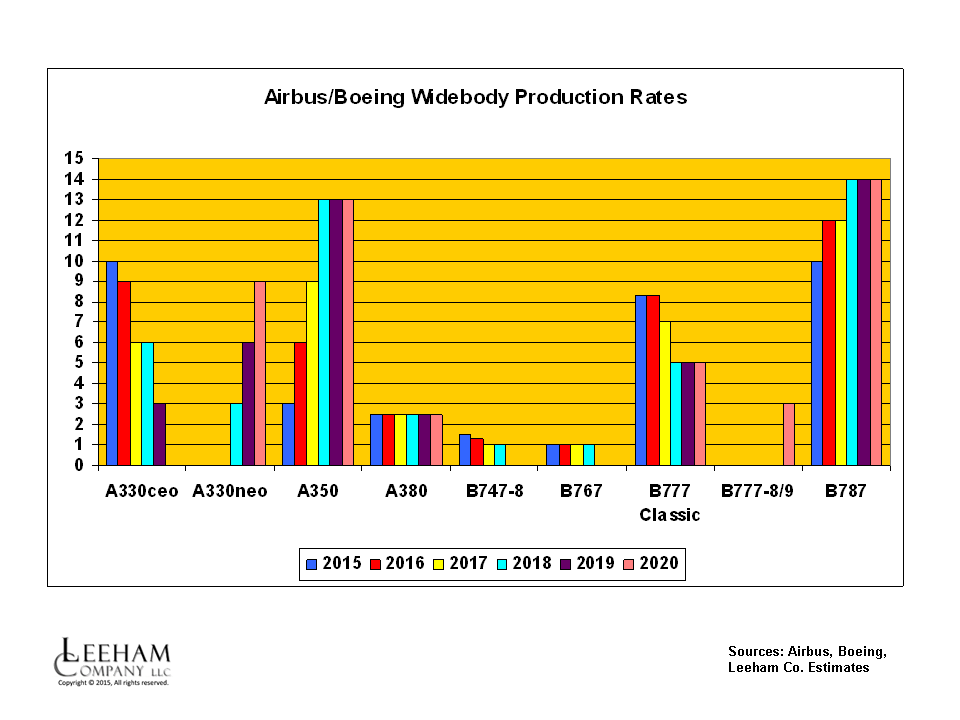

The A350 ramps up its production this year even as the A330ceo rate begins to come down at the end of the year and further next year. Boeing vows to maintain the current production rate of the 777 Classic at 100/yr. The 747-8 rate is declining. And both companies are ramping up rates of the single-aisle airplanes.

The production wars continue.

Summary

- Airbus is forecast to out-produce Boeing by 2018.

- Boeing’s ramp-up of the 737 line will drive the delivery stream.

- The 737 rate may hit 63/mo by 2020.

- Airbus will likely match.

Discussion

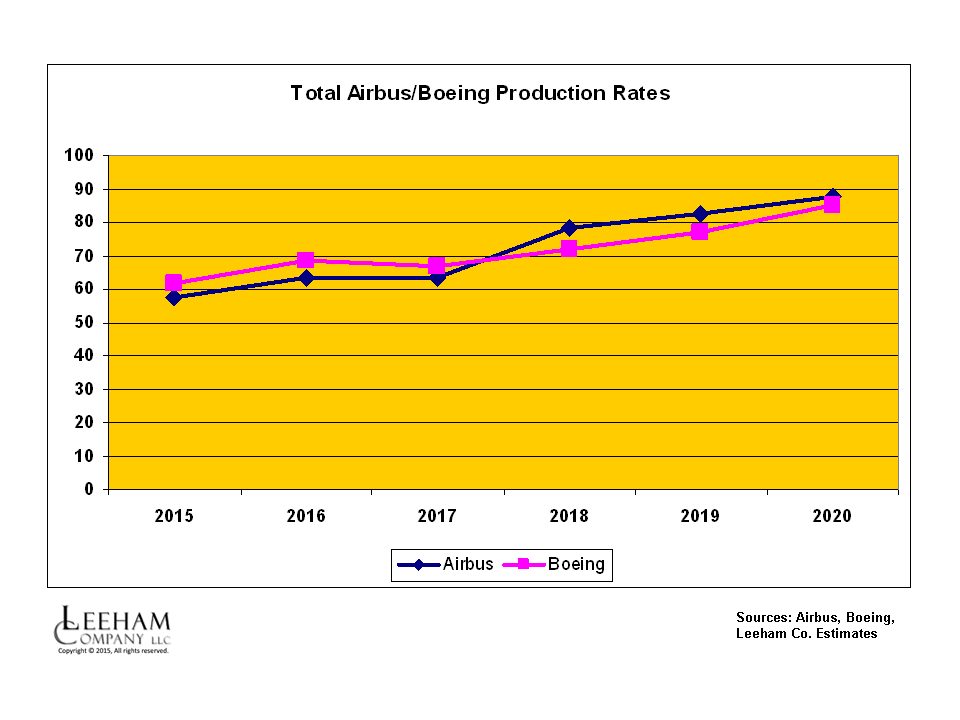

Figure 1. We expect Airbus to surpass Boeing in production rates in 2018, based in a number of assumptions. This chart is per-month, total production of all A-Series and 7-Series commercial airplanes, and excluding the A400M and KC-46A. Click on image to enlarge into a crisp view.

We expect Boeing to maintain the lead in production and deliveries through 2017, but relinquish this lead in 2018. (Figure 1.) There are several key assumptions, any one of which could upset the forecast:

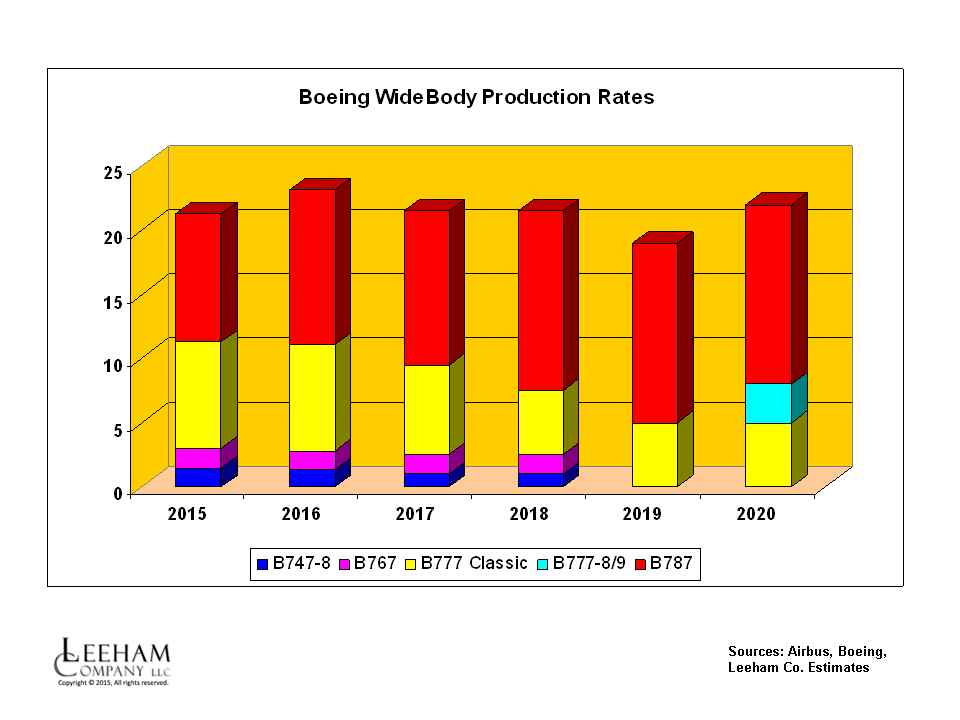

- We assume, as do most Wall Street aerospace analysts, that Boeing won’t be able to maintain the current production rate of the 777 Classic and this will come down beginning in 2017.

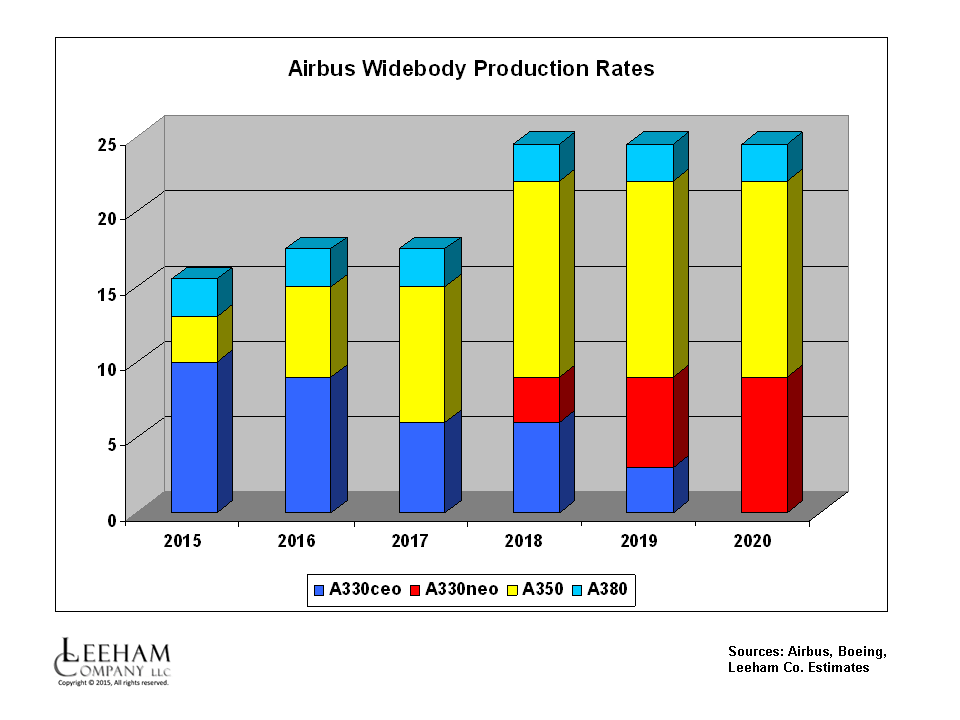

- We assume the A330ceo production rate will bottom out at 6/mo before

Figure 2. Click to enlarge into a crisp view.

the A330neo rate ramps up in 2018. We assume a two year overlap of the ceo and neo, following the transition plans for the A320ceo/neo, Boeing 737NG/MAX and 777 Classic/777X. (Figure 2.)

- We assume the 747-8 zeros out in 2019.

- We assume Airbus will find a way to maintain the A380 production rate at 2.5/mo until the A380neo is launched and enters service around 2021.

- We zero out the 767-300ERF in 2019 (only one is scheduled for delivery

Figure 3. Click to enlarge into a crisp view.

that year). Although the announced production rate for the 767 is 1.5/mo, scheduled deliveries of the commercial model through 2018 are well below this rate and we have adjusted our commercial forecast production accordingly. (figure 3.)

- We assume the A350 ramps up to 13/mo from 2018; the supply chain has been notified to plan for this, although a commitment has yet to be made.

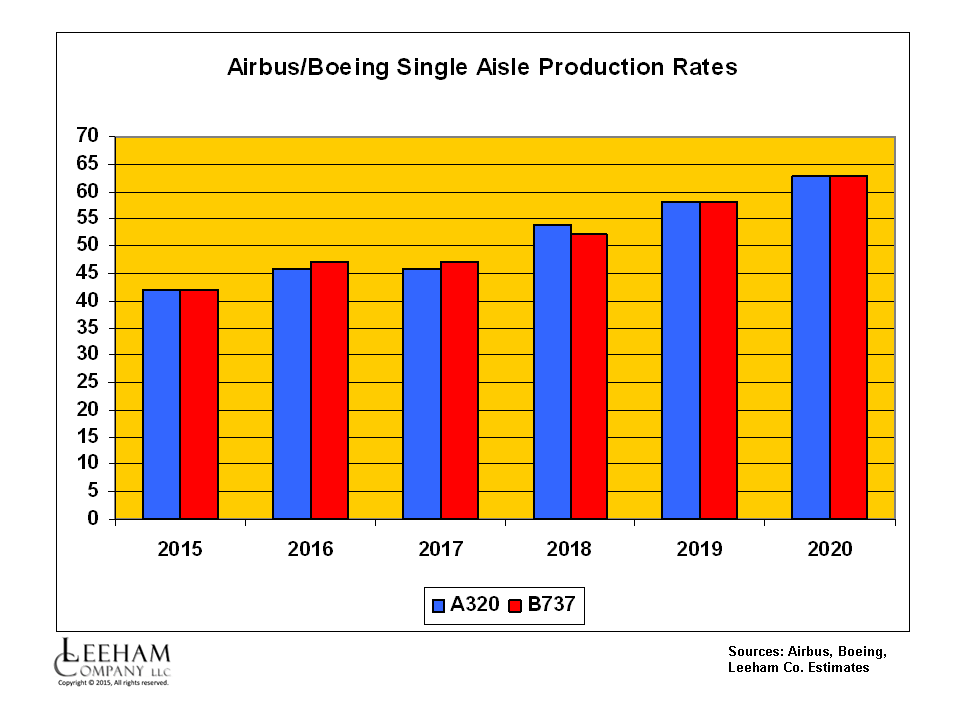

Figure 4. Click on image to enlarge into a crisp view.

- We assume the 737 rate to go to 58/mo in 2019 and 63/mo in 2020. The supply chain has been notified to plan for these rates, but no commitment has been made. (Figure 4.)

- Airbus has notified the chain to plan for 54/mo in 2018, though no commitment has been made. The supply chain has not yet been notified of higher rates, but we assume Airbus will match Boeing’s rates for the single-aisle sector. (Figure 4.)

- And finally, we assume no global geopolitical upset, no terrorist event that affects orders and production, and no global health epidemic.

These are a lot of assumptions, to be sure.

By 2020, Airbus and Boeing are forecast to be producing at about equal rates. (Figure 1.)

Figure 5. Click on image to enlarge into a crisp view.

The single-aisle sector has, by far, the most airplanes ordered and in backlog. The wide-body sector has high value, and Airbus and Boeing continue to argue each dominates this sector. In 2014, Boeing crushed Airbus in orders. There were, however, two unusual events: Airbus saw 70 A350s canceled by Emirate Airlines, which is going to re-run the competition this again in a bake-off against the Boeing 787-9/10 and the A350-900/1000; and Boeing firmed up 200+ orders for the 777X, most of which were announced at the Dubai Air Show in 2013. Even so, Airbus says that since the launch of the Boeing 787 in 2003, Airbus has captured 50% of the wide-body sales.

We expect this to be a normalized year, so orders for wide-bodies should be more competitive. Key to watch will be sales for the A330ceo and the 777 Classic. These will drive production rates. (Figure 5.)

Conclusion

Airbus and Boeing remain the proverbial elephants in the room. The new entrants into the single aisle sectors in which Airbus and Boeing compete–125-220 seats–are Bombardier with the CS300; COMAC with the C919; and Irkut with the MC-21. Bombardier is in a management disarray which, along with other factors, is slowing sales of the CS300. COMAC is already running at least two years late (to 2018) for the C919 and possibly as much as four years late. Irkut claims it is on track for a 2018 EIS of the MC-21. This remains to be seen and, in any event, the Russian geopolitical status casts a cloud over market viability of the MC-21 even if it is competitive to the A320/321neo and 737-8/9 MAX.

Bombardier’s ramp up for the combined CS100/300 is planned for 2/4/6/8/10 per month per year. Whether program sales support this ramp up is now unclear.

COMAC and Irkut each project rates of 5/mo, but we don’t see these until the 2020 decade now, if all goes well.

I believe Boeing out-delivered Airbus for the third consecutive year in 2014. It out-delivered A. the first time in 2012 => 601 to 588.

What does this mean for the Engine market share?

Will RR achieve 50% market share on wide-body engine deliveries in 2017 or 2018? On your numbers it feels like a major shift in the market place thinking that RR will get to 73% share by 2020, ie 62 out of 86 engines per month.