Leeham News and Analysis

There's more to real news than a news release.

Bjorn’s Corner: Aircraft engine maintenance, Part 6

By Bjorn Fehrm

April 7, 2017, ©. Leeham Co: Last week’s Corner developed the overhaul shop visits per year for wide-body engines. We will now look at how the market develops around these overhaul opportunities.

How does the shop structure develop over a popular engine’s life-cycle? How much choice has an operator and when?

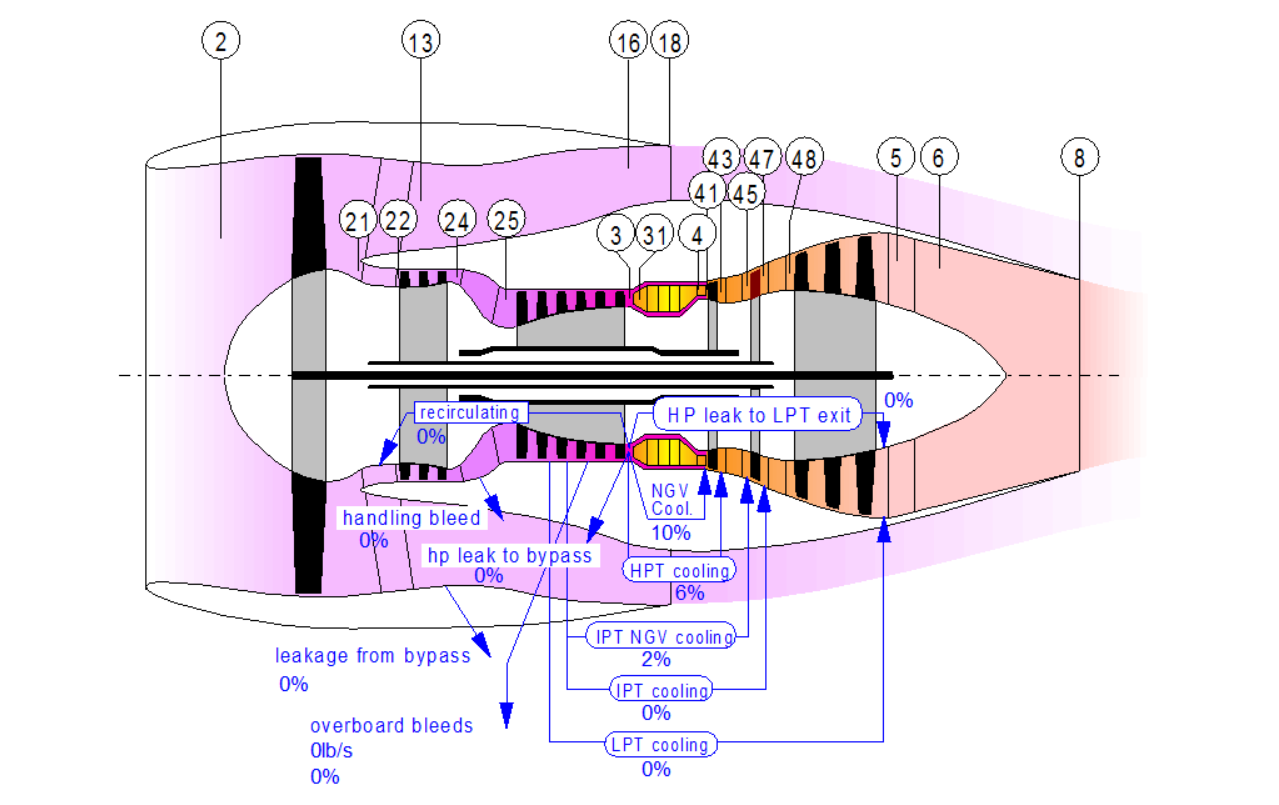

Figure 1. Principal picture of a three-shaft wide-body turbofan with station numbers. Source: GasTurb.

Wide-body engine overhaul market

Figure 2 shows the graph developed last week which shows the number of shop visits per year for different wide-body engines.

Figure 2. Number of shop visits per year for different wide-body engines. Click to see better. Source: Leeham Co and Rolls-Royce.

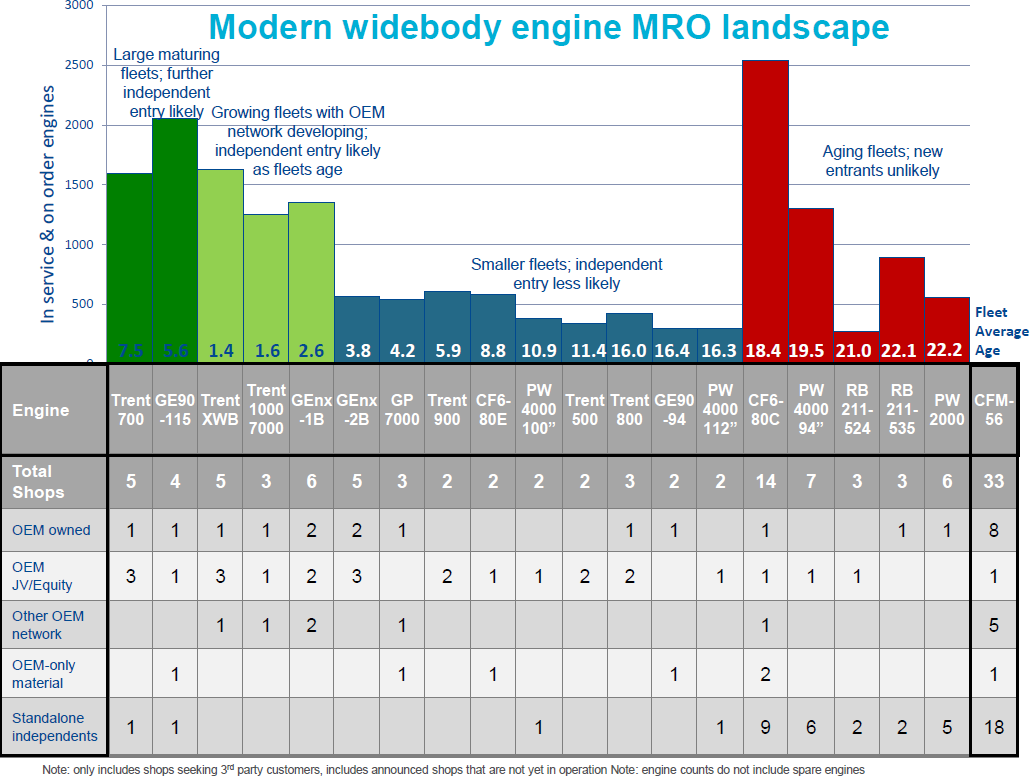

We will now discuss how the overhaul market develops dependent on where an engine is in its life cycle. Figure 3 shows the number of engines in the market for the different types (left scale), the population’s average age (number at bottom of bars) and their shop structure. It’s a Rolls-Royce chart that we have been given access to.

To the right in the table is the CFM56 single aisle engine shop structure as a comparison. There are close to 30,000 CFM56 engines in operation, which compares to the number of engines in service for the wide-bodies.

Figure 3. Wide-body engines in service, their average age and shop structure. Source; Rolls-Royce.

The wide-body engine with the most units in service right now is the GE CF6-80C. There are 2,500 engines operating on Boeing’s 747, 767, MD-11 and Airbus’ A300/ A310. This engine has 14 shops certified to do overhauls. The CF6-80C has a high number of independent shops, nine in all.

The shops called “OEM only material” are airline shops (Air France, KLM and Lufthansa Technik) which are contractually bound to use the OEM’s materials and procedures. When shops are labeled independent, they can source material on the open market from part out vendors or repair shops, in addition to the OEMs.

There is no chance of any new shops investing to overhaul CF-6-80C. The 14 shops compete for a market of 150 overhauls per year. It means many shops get less than 10 engine overhauls done per year. We said 50 were wanted and 10-20 are the minimum. All Red engines are in the Sunset phase and will not attract any new shops.

The Blue engines have relative small numbers in the market. The most common (CF6-80E, Trent 900, GP7200, about ~500 engines) have two to three OEM-affiliated shops. It’s less likely the blue engines will attract new entrants investing in qualification for these engines. The exception is the GEnx-2B (747-8), as this engine has a lot in common with the GEnx-1B for Boeing’s 787.

The GEnx-1B is part of the Light green engines.These engines are still young in the market and have a growing user base. Many engines are still maintained by the OEMs, on guarantee or power-by-the-hour agreements.

The market is growing and there will be more and more requests for independent quotes from the airlines, as these engines transit into their mature phase.

The Green engines are in the mature phase. Both the GE90 and the Trent 700 have around 300 shop visits per year and their numbers in the market are still increasing for many years. There is a clear interest for independent shops to qualify for the engines and to bid for the maintenance contracts.

There is one independent shop existing for both but there will be room for more. These independents would compete with the OEM-related shops for the jobs. Given the increasing shop visit opportunities coming into the market for these engines, and the operators want competition, it makes business sense for further shops to enter the market.

Bjorn,

Does this copetition between shops for more mature engines aid legacy engines and planes? There is still high demand for te 777 Classic and A330 CEO. As well as the lower cost of these planes relative to their upgraded counterparts, is it true that the competition beween shops and the supply of parts from these shops which readily source from the open market mean that these classic planes are in fact a more mature, more maintainable, cheaper and better choice in the eyes of Airlines. For example, Air China is still buying up 777 Classics and A330 CEOs. It seems like they get the best of both worlds – new planes, brand new engines with mature engine designs and the possibility that the savings they make on these older designs outweigh the Opex savings on fuel consumption from their newer updated couterparts, as wel as cheaper more readilty availbale maintenenace options, parts market etc.

“This engine has 14 shops certified to do overhauls. The CF6-80C has a high number of independent shops, nine in all.

The shops called “OEM only material” are airline shops (Air France, KLM and Lufthansa Technik) which are contractually bound to use the OEM’s materials and procedures. When shops are labeled independent, they can source material on the open market from part out vendors or repair shops, in addition to the OEMs.

There is no chance of any new shops investing to overhaul CF-6-80C. The 14 shops compete for a market of 150 overhauls per year. It means many shops get less than 10 engine overhauls done per year. “

The capability for independent shops to offer the most flexible workshop scope and parts to the operators is a clear plus for mature engines/airplanes. I wouldn’t go as far as saying the market is vacuumed for used 777-200ERs or A330-200 or -300 as a result. At every aicraft conference (we attend several each year, last in March and next in May) the problems of placing these aircraft in the market to reasonable prices are discussed. But the flexible engine overhaul for these aircraft is a pre-requisite for them finding a market. The engine maintenance costs dominate when aircraft get old.

This is also what the operators and leasing companies moan about for newer aircraft and engines coming of their first placement and going to next. They’d liked that the OEMs involvement would be less to stir up the competition for the jobs. As shown the market dynamics has to be there for independents to risk their investment in tools and peoples time to qualify for new engine types. The independent exits because they are savvy business people, they need to see a business case before investing.

What is typically the largest and most conplex part an independent shop offers on the maeket for the CF-6-80C?

The high costs are for the hard limit LLP sets. As said previously a complete set costs around $5-6m. Lets say its time to replace some important sets and these cost new $3-4m and the engine is only expected to be used for 60% of the lifetime of what these sets offer in flight cycles.

The independent shop would expected to search the market for used sets with that time left more vigorously than e.g. an OEM shop. It would also propose repairs for other parts where an OEM shop would sell new parts. This is one of the added values an independent shop can give, to more aggressively run the engine value down in the last stint.

The OEMs knows they need to be more flexible in this regard, they are getting more prepared to use parts from the used market as well.

Repair parts vs new is where it start gets getting complex for the OEM – the OEM typically will make 50% gross margins on the new parts, so a part that sells for $1m will cost the OEM $0.5m to make. However, as an example the independent repair shop might spend $0.6m repairing that part and be happy to sell it on for $0.8m – the question is how would the OEM compete? it can either maximise its profit short term and put in a discounted new part (making $0.3m profit vs $0.5m normally), but this potentially completely wrecks its entire aftermarket pricing. On the other hand, it is a tough decision to repair the part for $0.6m and sell it for $0.8m, reducing the OEM’s profit. This is probably what they should do in order to control the aftermarket stream, which they need to do having sold the engine at a loss and having spent all that money on R&D – they need to get a return.

The alternate would be for airlines to pay more for the engine in the first place…

Hi Charles,

you describe very pedagogically the dynamics of the Mature and Sunset engine maintenance market with a good example, thanks. The OEMs are adapting their strategies to this reality as their successful engine programs transit gradually from new engines to the Mature and finally Sunset phase. The key for their regaining of the lost money up front (due to the peculiar market behavior) it to keep the engines flying and collect hours/cycles. Only then can the engines generate revenue and margins for the OEMs in the overhaul shops.

The question on how much lock-in and control they shall have for the parts business is a delicate balance. To protective of own margins and the aircraft go for the desert or part out too early. Often better to take a thinner slice for longer and have the engines in the market ticking up hours.

With a long history of exceptional performance, Their products maintain an outstanding reputation in harsh environment military and aerospace applications.