Leeham News and Analysis

There's more to real news than a news release.

US Airways Media Day-Part 1

We’re at the US Airways Media Day and we’ll provide updates throughout the day.

First up is Doug Parker, CEO of US Airways and the new CEO of American Airlines when the merger is consummated.

Doug Parker:

- This media day is a little bitter-sweet. It’s the last one we will do here in Phoenix. (This is #13.)

- We’ve talked about consolidation over time, how US didn’t have to participate but would be better if it did. We talked about what the industry needed to do to be better. We talked about a lack of focus on labor, which was dysfunctional, a lack of discipline. The industry was improving on all fronts. Today the industry is much better with the exception of government policy.

- In 2010 I talked about the lack of profitability with oil a problem.

- In 2011 talking about how the recovery was real, in good and bad. Oil prices was as high as in 2008. US made over $100m, a $1bn turnaround from 2008.

- In 2012 we talked about how we were in a position to make a choice for a merger, not because we had to.

Odds and Ends: Boeing earnings call; US Airways Media; 787 update Day

There’s a lot of news happening today and tomorrow.

NTSB Hearing: The NTSB hearing on the Japan Air Lines Boeing 787 battery fire is today and tomorrow. This can be followed live (and later archived) here.

Boeing Earnings Call: This is Wednesday, April 24. This can be followed here. Expect a fair amount of discussion about the impact of the 787 battery issues on earnings. Ordinarily we’d have our usual live running coverage but instead we will be at the…

US Airways Media Day: This airline has an annual media day and it was scheduled for today a long time ago. We’ve been a regular at this, and due to the pending American Airlines merger, apparently there is going to be big press demand: they had to move the venue from headquarters to a hotel location in Scottsdale. We’ll have several updates throughout the day.

787 Update: LOT Polish Airlines expects to return its two 787s to service in June; Ethiopian this month; the Japanese airlines could return the airplane to service this month but ANA plans up to 200 test flights first, so this will slip to May and perhaps June. It’s unclear when Japan Air Lines plans a return-to-service (RTS). Qatar Airways wants to RTS this month. United Air Lines appears planning next month.

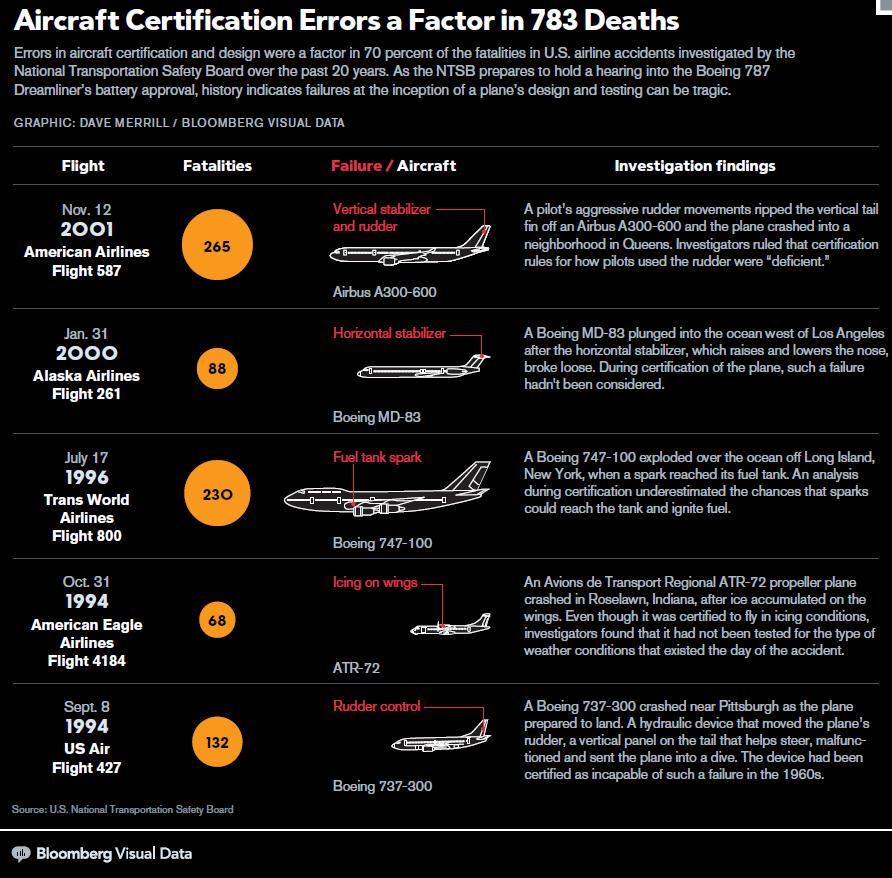

Flaws escape FAA certification

Bloomberg has a good story looking beyond the Boeing 787 issues at the FAA’s reliance on industry to certify airplanes. The story details a number of cases where flaws crept through the system, leading to deaths–a circumstance, of course, that did not happen with the 787.

We have written a couple of posts about the relationship between the FAA and industry in response to focus following the 787 battery issues. We pointed out this relationship is nothing new.

The Bloomberg piece is well worth reading.

US Airways’ 757 problem

Notation: Lan Chile has canceled Boeing 787 flights through June.

US Airways has a large fleet of aging Boeing 757s it needs to replace. The problem is, a carrier official says, neither the Airbus A321neo nor the Boeing 737-9 MAX can do what needs to be done: Phoenix-Hawaii non-stop in both directions with maximum payload under all conditions.

The distance is 2,910 miles, well within the advertised range of 4,200 miles for the A321neo and 4,137 for the 9 MAX. But Derek Kerr, executive vice president and chief financial officer says fleet planners have yet to be convinced either plane can replace the 757W, which is uniquely able to handle the hot, summer conditions at Phoenix, where temperatures often soar to 110F degrees or more.

US Airways is one of only two legacy airlines in the US that has yet to order the MAX or the NEO (Delta Air Lines is the other). A year ago, US Airways CEO Doug Parker told us that the value proposition of ordering the neo still was unconvincing given the price premium sought by Airbus. Kerr told us last week that the large, outstanding order for the current generation A320 family as replacements for the oldest jets–and the lack of a true replacement for the 757–meant the airline wasn’t in a hurry to place an order for re-engined aircraft.

Washington State air facilities that could close with sequestration

The FAA has released a list of air traffic control facilities that could close with Sequestration, which is due to take effect March 1.

The following facilities in Washington State are on the list:

ALW Walla Walla Regional Walla Walla WA

MWH Grant County International Moses Lake WA

OLM Olympia Regional Olympia WA

PAE Snohomish County Airport (Paine Field) Everett WA

RNT Renton Municipal Renton WA

SFF Felts Field Spokane WA

TIW Tacoma Narrows Tacoma WA

YKM Yakima Air Terminal/McAllister Field Yakima WA

Additionally, the over night shifts in the following control towers are at risk:

BFI Boeing Tower Seattle WA

GEG Spokane Tower Spokane WA

The FAA warns that passengers at TSA lines could be up to three hours and tarmac delays at major hub airports could be up to 90 minutes.

Odds and Ends: 787-10/777X; 737NG engine issues; American-US Airways

787-10/777X: Aspire Aviation has this long analysis of the current status of these developmental programs.

737NG Engine Issues: Aviation Week on February 8 had a report of thrust irregularities on the Boeing 737NG. The Seattle Times reported it on line last night and in print today. And then the Seattle media went mad. We’re perplexed. The issue goes back five years, it happened 32 times and not since December when a fix appears to have–fixed it. What’s the big deal?

American-US Airways: The long-awaited merger was announced today and to our great relief, the US Airways management will run the place. American CEO Tom Horton is booted upstairs to non-executive chairman, much as was Glenn Tilton in the United-Continental combination. Unfortunately the AA-US merger keeps the awful tail livery rolled out by Horton a few weeks ago.

Odds and Ends: Airbus’ frustration over A350 fallout–blame yourself; DC-10 grounding retrospective

Airbus’ frustration: Airbus says it has a Plan B for its lithium ion battery design and the CEO says he’s frustrated over the attention the A350 is getting as a result of the Boeing 787 issues.

Airbus has only itself to blame for any frustration: it’s stonewalling all questions about the design and fire protections of its lithium-ion batteries. The absence of answers from Airbus leads to the conclusions that it doesn’t have fire suppression as it’s commonly thought of.

Boeing remarked after the JAL fire that thermal runaway can’t be suppressed with in-flight fire fighting techniques. The presentation we detailed from Airbus makes it clear Airbus has the same conclusion. Although Halon can be used to suppress small fires, a thermal runaway can only be suppressed by water, and plenty of it. It took firefighters more than an hour to put out the blaze on the JAL airplane, according to the NTSB timeline.

The Airbus slides suggest there is Halon designed into the A350 and we are told the design has venting that the Boeing design does not. But Airbus won’t say what its design is. Does it take the containment approach The Seattle Times wrote about in connection with Cessna? Airbus won’t say. But we know from a well-placed source that venting overboard is part of the Airbus design.

See KING 5’s report below-Boeing is working on its own Plan B.

“We have a robust design,” Reuters quotes Airbus CEO Fabrice Bregier. “I’m not going to give any lessons to Boeing. At the same time, I don’t have to take any either, when I think we have done well and have a plan which allows me to have aircraft flying with batteries that don’t catch fire,” he said, according to Reuters.

We find this second statement to be a load of crap. Where safety begins, rivalry should end. For the good of the industry, Airbus ought to share its thoughts with Boeing. The rivalry perpetrated between the two companies is often childish (both sides are guilty of this) and unworthy of two world-class companies. We find the statement above to be appalling.

Airbus has told us its battery-from a different supplier than that of Boeing’s-meets FAA standards, something that weren’t in place when Boeing selected the lithium-ion batteries in 2007. The FAA issued Special Conditions for Boeing’s use of the new technology batteries.

Aviation writer Christine Negroni has a post that expresses a great deal of frustration with Boeing’s corporate attitude toward the lithium ion issue. Frustration seems to be catching. But Airbus has the opportunity here to take the high road for safety and share its approach with Boeing–and to assure the aviation world publicly that its airplane will be safe.

Bregier says his design is safe and there’s a Plan B if regulators say more is needed. Tell us what is safe about the design and tell us what Plan B is.

Meanwhile, KING 5 (NBC-Seattle) has further information on Boeing’s Plan B, which is to build a containment box around the battery (similar to the Cessna approach).

DC-10 Grounding: The last time the FAA grounded a commercial airliner was in 1979, when American Airlines lost a McDonnell Douglas DC-10-10 at Chicago O’Hare International Airport. Aviation Week linked its report at the time and we link this article here.

Space Shuttle: The Seattle Times has a story about the space shuttle Columbia, which broke apart 10 years ago. It’s interesting reading.

American to firm up 787 order, add two 777s and firm up MAX

American Airlines will firm up 42 orders for the Boeing 787, its 737 MAX order and add two 777 orders upon bankruptcy court approval, according to an SEC filing today.

American’s plans to acquire 75 787s had always been contingent on a new pilot contract–which has come through the bankruptcy process. The MAX orders, placed in July 2011, also were never firmed up due to the bankruptcy filing the next month.

Two new 777 orders were unconnected to the 787 and MAX orders.

From the SEC filing:

Odds and Ends: PNAA Aviation Conference; AA-US merger review; UAVs in USA; SPEEA-Boeing; 2013, Part 2

PNAA Conference: The Pacific Northwest Aerospace Alliance holds its annual conference Feb. 12-14 in Lynnwood (WA), north of Seattle. This event is now the largest of its kind in the Pacific Northwest and the first or second largest of its kind on the West Coast. The top airframe manufacturers present, along with key aerospace analysts (including the ever-entertaining Richard Aboulafia) and key suppliers. There is a Suppliers Fair and this year for the first time a focus day on the airline industry. Follow PNAA @pnaalliance on Twitter.

American-US Airways merger review: This should be concluded within weeks, says AMR CEO Tom Horton.

UAVs in USA: Rules on the use of UAVs within the US are emerging and vary widely throughout the world.

SPEEA and Boeing: A reminder that SPEEA contract negotiations resume with Boeing next week on January 9. Based on conversations with SPEEA, we don’t expect things to go well. SPEEA told us–and pretty much anyone else–that it believes the gap between it and Boeing is so wide that it expects talks to break off quickly. A strike vote will follow and a target date for a strike is February 1. SPEEA filed another Unfair Labor Practice complaint this week over Boeing taking pictures of SPEEA marchers at the Everett plant.

The year ahead, Part 2: Earlier we posted our Leeham.net look at 2013. Here’s what we did for CNN.com, in a somewhat broader look.

APA speaks about potential American-US Airways merger

From the Allied Pilots Association leadership to its membership:

Fellow pilots,

The APA Board of Directors reconvened today at 9 a.m. at union headquarters as part of the ongoing four-party negotiations between American Airlines and US Airways management, APA and the US Airline Pilots Association (USAPA) on behalf of US Airways’ pilots.

These negotiations are aimed at reaching a Memorandum of Understanding (MOU), or interim agreement, to address each pilot group’s respective concerns if the two carriers proceed to merge. The MOU would serve as the transition agreement and would also include improvements to our newly ratified collective bargaining agreement.

Some have suggested that the only way APA should “agree” to a merger is to first negotiate an integrated seniority list with USAPA. Major corporate mergers involving represented employee groups don’t work that way. No legal mechanism exists that would allow union-represented employees to interfere with a major transaction such as a merger. With McCaskill-Bond the law of the land, unless management predicates a merger on an integrated seniority list—much as we saw at Southwest in their acquisition of Air Tran–we are left to pick up the pieces after the merger has occurred.

While APA’s institutional position has consistently been one of support for a merger between the two carriers within bankruptcy, support for a merger at this juncture is not unanimous within the union. Likewise, AMR management has not embraced the concept of expediting a merger before restructuring concludes and clearly wants to retain control of the corporation and consider a merger on their terms following exit from bankruptcy. Keep in mind that AMR management has executed four different mergers—beginning with Trans Caribbean and ending with TWA—while completely disregarding the impact on our pilots’ seniority. I doubt that pilot seniority is anywhere near the top of their concerns right now. Likewise, I doubt that pilot seniority would be a key consideration if they were to execute a merger with US Airways, JetBlue or any other carrier following an independent exit from bankruptcy.

Instead, what we’re seeing is likely a deliberate attempt to sew fear amongst our pilots in an effort to derail consensual merger talks. A small group of pilots, with assistance from AMR management and a former CEO [here and here], has been advancing the notion that an integrated list should be a precondition to any further consideration of a merger. Their motives are crystal clear: hold on to the reins of power and control any merger on their terms. To be clear, fundamental capital transactions such as a merger involve a large number of parties. By virtue of the 13.5 percent equity stake we now hold as part of our ratified agreement, APA can exert influence over various aspects of a merger as a major stakeholder in AMR. However, we don’t have the ability to stop the clock and make everyone else wait while we sort through all of the issues associated with an integrated seniority list. To suggest otherwise is disingenuous, and simply ignorant of the law and the facts.

Our advisers have indicated that if we do not finalize an MOU in the very near future, in all likelihood there will be no merger before American Airlines exits restructuring. An MOU specifying wages and working conditions for the pilots, along with interim seniority protection in the form of fences, would enable creditors to identify synergies that would result from a merger of the two carriers. Absent an MOU, the financial benefits of a merger would remain unclear.

We all understand that seniority is extremely important to our careers. Of course, your seniority number is irrevocably tied to the airline you work for, so it’s likewise critical for your employer to be able to compete and thrive. The analysts who study our industry and make judgments about which airlines are best positioned in the marketplace have been virtually unanimous in the view that a merger with US Airways represents the best way to address our airline’s current deficiencies. Make no mistake—a merger of some sort is inevitable. The questions before us: Who do you want at the helm and do you want the ability to have some control over the process? In a post-bankruptcy merger, we would have little ability to influence any potential leadership changes at American Airlines and would represent nothing more than a speed bump.

It’s worth revisiting some of the reasons why the APA leadership decided several months ago that despite the inherent difficulties, a merger with US Airways represents the best path to a reinvigorated American Airlines and, by extension, a brighter future for us all. With the mergers of Delta-Northwest and United-Continental, American Airlines now stands at a distant third (and, by some measures, fourth in the U.S. industry) in terms of our revenue base and route network. A merger with US Airways is essential for both carriers and represents the quickest way to recapture the critical mass essential to competing effectively with those two carriers.

We have seen a model for a successfully arbitrated seniority integration at Delta-Northwest using fences and a ratio methodology based on a percentile seniority list ranking. Also, if an American Airlines-US Airways seniority integration were to be arbitrated, our attorneys have indicated that the ongoing seniority dispute between “West” and “East” at US Airways would be settled as part of the process and should not have any negative impact on an arbitrator’s decision under the McCaskill-Bond statute.

Many analysts believe that American Airlines finds itself in its present predicament because of an excessively cautious approach to consolidation during the past several years. Instead of vigorously pursuing Northwest Airlines as a remedy to American Airlines’ deficiencies in the Asian network, they sat on the sidelines as the rest of the industry flew by. How much longer should we wait before deciding that something needs to happen to fix American Airlines’ revenue and network disparities? Merging within bankruptcy also affords APA opportunities to “re-attack” sooner rather than later to capture additional contractual value in the form of a transition agreement/MOU for our members. On the other hand, a “wait and see” approach would ensure that American Airlines exits Chapter 11 restructuring as an independent carrier with our newly ratified contract. At that point we would have no mechanism for making any near-term contractual improvements, and little ability to influence the management structure or strategic direction of the corporation.

If the four parties agree to an MOU/transition agreement, we would proceed to the next phase of the process, which would involve the creditors assessing the financial benefits of a merger. If a merger meets with their approval, a series of additional steps would have to occur before a merger is approved and the new company exits restructuring, including consideration by the two companies’ boards of directors; antitrust review by the federal government; and approval of a plan of reorganization by the Unsecured Creditors’ Committee and the bankruptcy court.

Upon exit from restructuring, an application for single-employer status with the National Mediation Board must be made, which would take approximately six months. Once single-employer status is declared, we would go through a process to determine the bargaining agent for the pilots. After that we would begin negotiating a joint collective bargaining agreement (JCBA), which would focus primarily on reconciling and integrating the US Airways pilots into the American Airlines operation. This JCBA must be completed within 24 months of a plan of reorganization being approved. If not, it would be submitted to binding arbitration for any remaining open items. Seniority integration negotiations would then commence. In the interim, we would operate in accordance with the protections stipulated by the MOU, including fences and provisions to ensure that pilots on the American Airlines seniority list would operate any aircraft delivered as part of the previously announced aircraft orders.

Fellow pilots, we understand your keen interest in the ongoing MOU negotiations, and we will continue to provide updates as developments warrant.

Thank you for remaining engaged in determining our collective futures.

In unity,

Keith Wilson

First Officer Dennis Tajer

Allied Pilots Association (APA)

APA Industry Analysis Committee – Chairman

APA Communications Committee