Leeham News and Analysis

There's more to real news than a news release.

At long last, Boeing appears near certification and EIS for 777X

Subscription Required

By Scott Hamilton

July 14, 2025, © Leeham News: Boeing is still months away from receiving certification of its newest, largest jet—the 777-9—and the company didn’t bring one of the test airplanes to the Paris Air Show last month. However, officials showcased the passenger and freighter models in an experience center during the major international event.

Justin Hale has the imposing title of Customer Leader & Senior Product Marketing Director for 777X and Production Freighter aircraft

The 777X comes in three models: the 465-seat 777-9; the 777-8F cargo airplane; and the 777-8 passenger model, which is an ultra-long-range (ULR) aircraft. The program was launched in 2013 at the Dubai Air Show (even though the first order, from Lufthansa Airlines, was placed earlier). Entry into service (EIS) was planned for the first quarter of 2020 with an unofficial goal of December 2019.

Flight testing revealed some technical issues with the 115,000 lb thrust GE9X engines. These required engine removal and return to GE Aerospace for redesign, delaying the program by nine months. Further flight testing revealed some uncommanded nose-down flight anomalies, requiring software redesign.

Then two fatal crashes of the Boeing 737 MAX in October 2018 and March 2019 revealed design and certification problems with the MAX. Scrutiny by the Federal Aviation Administration (FAA) of the MAX program expanded to include a comprehensive review of the work done up to that point on the 777X. The COVID pandemic further stalled flight testing and certification work. The engine-mounted thrust links developed cracks during further flight testing, adding to the delays.

Now, Boeing sees the program is finally on track for certification this year and EIS next year.

Related Story

Air India Flight 171 Preliminary Crash Report Is Unclear Regarding Pilot Actions

By Bjorn Fehrm

July 11, 2025, © Leeham News: India’s Aircraft Accident Investigation Bureau has issued the preliminary report of the crash of Flight 171.

The report indicates that the aircraft and flight crew were fit for flight and that the pilots were experienced, with the Captain having a total of 15,638 flight hours, including 8,596 on type, and the First Officer having 3,403 flight hours, with 1,128 on type.

The report documents the technical registration of the engine’s Fuel Cutoff switches, which transition from RUN to CUTOFF, remain at CUTOFF for 10 seconds, and then return to RUN. By then, the engine cores have slowed down below flight idle, with the engines delivering almost no thrust.

GE testing of giant GE9X engine aims for maturity at entry into service

Subscription Required

By Scott Hamilton

June 30, 2025, © Leeham News: GE Aerospace developed a huge engine for the Boeing 777X, the most powerful engine ever created. The GE9X tops out at 115,000 lbs of thrust.

The giant GE9X engine for the Boeing 777X generates 115,000 lbs of thrust. The human scale of the engine is illustrated here at a display at the Paris Air Show. Credit: Leeham News.

It’s had its development challenges. The 777-9, the first of the X family, was supposed to enter service in early 2020. Technical issues with the GE9X required removal of the engines from the test airplanes and a return to GE for fixes. This delayed flight testing by nine months. By then, certification of the 777X got caught up in the Boeing 737 MAX crisis; the 777X still is awaiting certification, which parties hope will come this year. Deliveries are now expected to begin next year.

Tim Clark, the president of Emirates Airline, has 205 Xs on order, more than any other customer, out of 521 in total. He’s publicly complained about the initial test results of the GE9X and demanded engine maturity before he’ll accept delivery.

GE has used the six year delay in the program to attempt to satisfy this demand.

Engine makers tout “Plan A” but have “Plan B” backups in R&D

Subscription Required

By Scott Hamilton

June 23, 2025, © Leeham News, Paris: CFM International touts its Open Fan RISE engine as the wave of the future. (CFM is a 50-50 joint venture between GE Aerospace and Safran.)

Rival Pratt & Whitney says evolution of its Geared Turbo Fan is the best engine choice going forward.

CFM’s Open Fan engine design called RISE. Credit: CFM.

Neither company will admit that it is also researching and developing a Plan B engine. For CFM, this is a conventional turbofan. For PW, this is a new Open Fan. But during the Paris Air Show, LNA confirmed that both have a Plan B engine in development.

PW has gone out of its way to dismiss the very idea of an Open Fan engine. Rick Deurloo, the president of Pratt & Whitney Commercial, won’t even talk about the “competitor.” Deurloo makes it clear—publicly, at least—that an evolution of PW’s Geared Turbo Fan (GTF) is the best solution for the next generation engine for the single aisle market, in its view.

Mike Winter, RTX’s Chief Engineer, dismissed the Open Fan as “sub-optimal” on a successor to the Airbus A320neo and Boeing 737 MAX families. It involves too many installation compromises on this size aircraft, he says. RTX is the parent of PW.

But, says one person with direct knowledge, PW fully understands that if CFM is successful in solving all the challenges of an Open Fan and meets the publicly stated goal of improving fuel consumption by 20% compared with today’s GTF and CFM LEAP engines, PW’s gain of an evolutionary GTF won’t be competitive.

So, says the person with direct knowledge of PW’s activities, the development of an Open Fan alternative engine is being worked on as PW’s Plan B.

Furthermore, PW’s sister company, Pratt & Whitney Canada, publicly disclosed its development of an Open Fan engine in a briefing on Tuesday this week. This engine is for a new 70-100-seat aircraft designed by the start-up company MAEVE. PW is following PWC’s development.

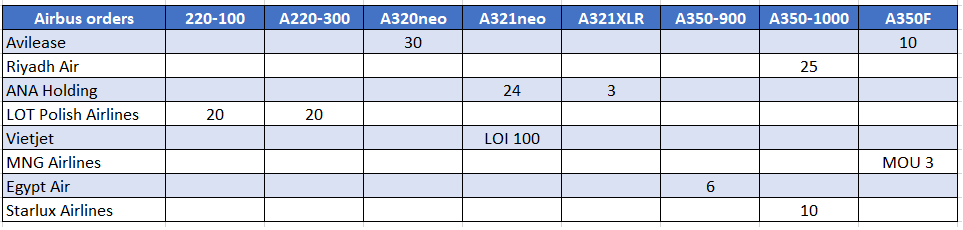

Airbus books 142 firm orders as Boeing retracts from the Paris Air Show

By Bjorn Fehrm

June 19, 2025, © Leeham News at Paris Air Show: Boeing chose to scale down its participation at this week’s Paris Air Show out of respect for the victims of the Air India crash last week. This left Airbus and Embraer to announce new orders, with a total of 142 firm orders for Airbus and 60 for Embraer.

Outside the order activity for the three large airliner OEMs, it was a relatively quiet show, with few noteworthy announcements of advancements in areas such as Sustainable Aviation.

Figure 1. Airbus orders and commitments at the Paris Air Show. Source: Airbus.

Five for Five: Air India crash points to systemic problems at Boeing that CEO Ortberg must fix

By Scott Hamilton

June 15, 2025, © Leeham News, Le Bourget, France: The Paris Air Show was supposed to be another step, however small, in Boeing’s way back from six years from crisis after crisis, safety and quality concerns, criminal investigations, Congressional hearings and existential threats following two fatal crashes of the 737 MAX and the COVID-19 pandemic.

Boeing wasn’t bringing any MAXes, 777X or 787s to the air show. There would be no awe-inspiring flight displays. The cost wasn’t worth it given Boeing’s billions of dollars in losses in recent years.

Nevertheless, Boeing planned low-key executive appearances and media events.

Air India flight 171 on its descent to a crash on July 12. Credit: Amateur video.

And then, four days before the show was to officially begin tomorrow, Air India flight 171 crashed, killing 241 of 242 people on board and at least three dozen on the ground where the 14-year-old 787-8 pancaked in to a densely packed residential and educational area only two kilometers from the airport.

Videos of the event showed the 787 using up almost all of the 11,500 ft runway to take off in a cloud of dust (presumably the overrun area), barely climbing a few hundred feet, dipping and climbing slightly again before smoothly descending into an explosive ball of smoke and flame on impact out of view of the cameras.

The pilot radioed a Mayday with the terse message reporting power problems with the GEnx engines on the plane.

Very quickly pundits, pilots, armchair experts and even former crash investigators began hypothesizing on what went wrong. Theories ranged from pilot error, misconfigured flaps, dual engine failure, electrical failures and more. The only thing missing was an alien ray from outer space.

Boeing bullish on 20-year forecast, despite short-term headwinds

By Karl Sinclair

June 14, 2025, © Leeham News: The Boeing Company (BA) remains upbeat on its annual 20-year commercial aircraft projections, as the aviation industry comes to terms with the economic uncertainty of the current political climate.

Credit: All images – Boeing

Credit: All images – Boeing

Boeing projects a need for 43,600 aircraft over the next 20 years, with 75% of those being single-aisle jets.

This is a drop of 375 aircraft over the previous years outlook, in which the company foresaw a need of 43,975 over the same period. Most of the drop off has happened the wide-body segment, which will now need 7,815 planes, versus 8,065 in 2024, a decrease of ~3%.

Related story

Little known, most unknown in Air India 171 crash

By Scott Hamilton

June 13, 2025, © Leeham News: One day after the crash of Air India flight 171, very little is known about what happened. Almost everything remains unknown.

What we know

- This is the first fatal crash of a Boeing 787. The accident airplane was delivered in 2014 and is a 787-8,

A screen show of a video of Air India flight 171. The camera is from a distance and the quality is grainy, but to many this seems to show that that flaps were not extended for take off. However, some flaps positions are set at 5 degrees, and may not be readily visible in this shot.

the first sub-type of the family of airplanes.

- There were 242 passengers and crew on board. One passenger survived; there were fatalities on the ground, but the number is fluid. One news report cited a total of 290 killed in the plane and the ground.

- Two videos of the accident surfaced yesterday. One shows the plane’s final seconds as the flight appeared in a relatively flat-attitude climb followed by a slow descent into the ground and explosion of fuel. The other showed the 787 on its take off roll, ascent, descent and crash. Both show that landing gear remained down throughout the short flight. The grainy videos appear to show the flaps were not extended for take off. The second video shows what appears to be a lot of dust thrown up as the plane lifted off the runway. Some speculate that was from the runway overrun area, but the angle and distance from the CCTV doesn’t include this detail.

- A Mayday call was sent from the flight. Most reports end with this one word. A few said the words “no power” were included in the Mayday.

- The weather was clear, but it was humid and more than 100 degrees in temperature. These hot conditions extend take off rolls.

- The plane was headed to London, some 10 hours away. A heavy fuel load would be on the plane.

The speculation

- The videos appearing to show the flaps were up led to the possibility that for some reason the plane was not properly configured for take-off. A flapless take off often leads to crashes, and the presence of a cloud of dust as the airplane lifted off could lend credence to a flapless roll. Flaps up after lift off could lead to a stall.

- However, past accidents with misconfigured flaps and slats included a wobbly take off and immediate crash within the airport perimeter. The video shows a smooth climb, such as it was, and smooth descent, suggesting the pilots retained some control over the airplane.

- “No power” in theory points to a problem on the take off roll, as well as a climb out. “No power” can mean any number of things: complete failure after lift-off, or reduced power at a critical point of the take-off and short flight.

- Fuel contamination could be a factor, but investigation will look into this possibility.

- The landing gear remains down throughout the flight. Normally, the gear would be raised right away. This leads to speculation of a hydraulic issue or perhaps the pilots mistakenly raised the flaps instead of the gear.

Boeing’s 737 North Line and the Everett factory: in transition now

Open to all Readers

By Scott Hamilton

Boeing 737-10 MAX. Credit: Boeing.

June 9, 2025, © Leeham News: Boeing announced the addition of a fourth 737 production line in 2023 as the last 747 rolled out of the Everett (WA) widebody factory where the Queen of the Skies was born.

To meet burgeoning demand, Boeing said it would assemble the 737 in Everett. Plans were put on hold a year later when the Alaska Airlines flight 1262 experienced a full cabin depressurization on a new 737-9 MAX minutes after take off from Portland (OR). A failure by Boeing during the assembly to resecure a door plug led to a 60-lb piece blowing out of the fuselage.

The Federal Aviation Administration (FAA) froze Boeing’s plans for the Everett 737 production on what’s called the North Line.

Boeing’s CEO Kelly Ortberg reaffirmed plans to establish the North Line. Doing so requires FAA approval. The North Line will be exclusively for the 737-10 MAX, which has yet to be certified by the FAA.

Boeing has quietly been laying the groundwork for the new line in the intervening year. Tooling, floor plans and other elements necessary to establish the line continued at a low pace. The company recently leased about 250,000 of space in a nearby industrial park to serve as a staging area for 737 kits.

The North Line will supplement the main 737 factor in Renton (WA), which is slowly returning to higher rates from a complete production suspension in 2019 following the grounding of the 737 after two fatal accidents of the MAX five months apart. The root cause of both accidents was a design flaw in the flight control system.

Boeing quietly returned to a 737 production rate of 38 a month on May 30, keeping a low profile in deference to the FAA, reported The Air Current on June 2.

Boeing CEO: Lessons learned are key to certification of 737-7/10 and 777X

By Karl Sinclair

Analysis

June 2, 2025, © Leeham News: Boeing CEO Kelly Ortberg believes that lessons learned from the 737 MAX crisis and subsequent in-depth oversight by the Federal Aviation Administration (FAA) are key to certifying the 737-10 MAX and the 777X.

June 2, 2025, © Leeham News: Boeing CEO Kelly Ortberg believes that lessons learned from the 737 MAX crisis and subsequent in-depth oversight by the Federal Aviation Administration (FAA) are key to certifying the 737-10 MAX and the 777X.

He explained why during an appearance last week at an investors conference organized by Bernstein Research.

“We’re watching real closely to make sure that we aren’t over committing in terms of how many different seat configurations we can get certified in a certain period of time and the complexity,” Ortberg said. “It’s something that we’ve got to watch, particularly the Dash 10s that have types of complex seat configurations.”

Ortberg added that the 777-9 also features complex configurations for international airlines, offering luxurious passenger accommodations.

Kelly Ortberg, CEO of The Boeing Co. Credit: Getty Images.

“It’s going to be with us also on the 777-9 as we bring that into service, making sure we incorporate lessons learned here so that we don’t have seating delays on those aircraft,” he said. “Those aircraft will have the most complex configurations in the front of the airplane.”

Certification of the 777X stalled because of the MAX certification review. There have also been some technical issues that have been and must be resolved. But at long last, flight testing with all four test aircraft has resumed.

“I’m hopeful that we’ll get through the certification flight tests by the end of the year,” Ortberg told the Bernstein conference. “We may still be doing some ETOPS testing going into next year, but there is no real change to our forecast of getting that certification done so that we can start deliveries next year.

“It’s an airplane that has had the most flight testing done of any other aircraft we’ve ever done in terms of hours. We feel pretty good about the stability and our entry into service for the airplane that we’ve done enough flight testing on that it’s going to be a great airplane.”