Leeham News and Analysis

There's more to real news than a news release.

Assessing the 100-149 Seat Sector

Introduction

Oct. 12, 2014, (c) Leeham Co.: The 100-149 seat market sector has long been criticized as irrelevant because of a string of poor-selling aircraft. Boeing officials even labeled this a Bermuda Triangle. The critics fail to recognize, however, that except for the Bombardier CSeries and the Embraer E-195 stretch based on a clean sheet design, there hasn’t been an airplane specifically designed for this sector since 1983. That was the British Aerospace BAe-146, which despite being powered initially by poor engines and having a cramped cabin, sold moderately well.

The early derivatives, the Boeing 737 Classic, and the McDonnell Douglas MD-80, did well. (The MD-80, while capable of seating up to 172 in shoe-horn configuration, was principally operated within the 130-150 seat layout.) But as fuel prices increased, derivatives began to lose their appeal because they weren’t optimized for the market. Engines then in use couldn’t keep up with the rising cost of fuel and airframes designed in the 1960s/70s/80s were no longer aerodynamically efficient as required for the changing fuel environment.

Summary

• Until the Bombardier CSeries and Embraer E-Jet, there hadn’t been an airplane specifically designed for the sector since 1983.

• Engine technology and airframe aerodynamics didn’t keep up with the demands of rising fuel prices for derivative designs.

• Airbus and Boeing are ceding the sector.

• Bombardier and Embraer will “own” the sector.

• There is a valid market for the 100-149 seat sector.

Discussion

Market Demand

The market demand for the 100-149 seat sector is a matter of debate—but only for those who don’t look closely at the numbers.

Airbus dropped segmenting the 100-149 seat sector from the all-encompassing 100-210 sector from its 2014 20 year Global Market Forecast. Airbus did separate the lower end in its 2013 GMF. Boeing doesn’t segment the sector from its Current Market Outlook forecasts, but has said the 100-149 seat sector will likely represent 10%-15% of the total single aisle forecast. Bombardier and Japan Aircraft Development Corp. provide specific forecasts, while Embraer only forecasts the 90-130 seat sector. Thus, the market demand for the next 20 years looks like this:

Sources: Airbus, Boeing, Bombardier, Embraer and Japan Aircraft Development Corp. 20 year forecasts.

For comparison, Airbus and Boeing forecast a demand for more than 4,000 small twin-aisle aircraft (787-8, A330)—a figure that draws no skeptics. Accordingly, we don’t understand why the 100-149 seat sector is considered a no man’s land—for the right airplane.

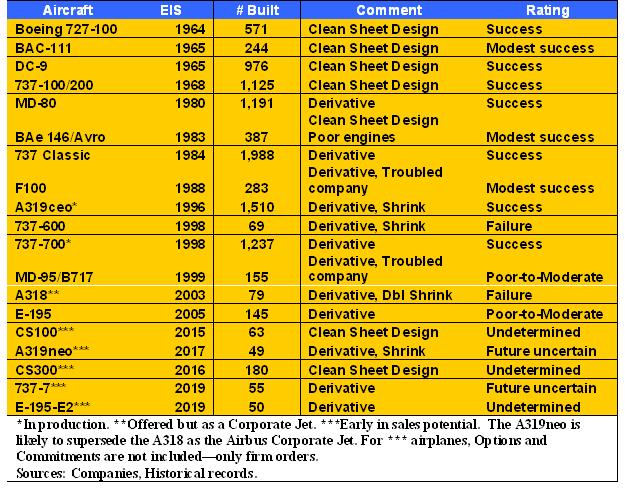

A look back at airplanes

Looking at the string of aircraft for this sector, the original designs and derivatives worked well—until fuel pricing began to increase sharply from 2000. Financially distressed companies didn’t help despite decent designs.

Our Rating is not based on profit or loss for the OEM, but on sales figures. For mature or terminated programs, we have taken into account the era as well as the quantity. What was Modestly Successful in 1965 and 1983 would not be successful today.

Our Rating is not based on profit or loss for the OEM, but on sales figures. For mature or terminated programs, we have taken into account the era as well as the quantity. What was Modestly Successful in 1965 and 1983 would not be successful today.

The 737-600 and A318 were developed principally to kill the last gasp of McDonnell Douglas Corp., the MD-95, itself a derivative, and never were intended to be particularly competitive. Insofar as MDC merged with Boeing in 1997, which then shut down all commercial MDC programs when orders were filled, it’s not surprising that these three airplanes were Poor or Failures.

We rate the BAC-111 as a Modest Success for its era despite a low number of sales. It was certainly eclipsed by the Douglas DC-9 and Boeing 737 but saw widespread use in Europe. The Fokker 100 was selling reasonably well but Fokker’s financial condition cut short the potential for the airplane. Had it not ceased operations, sales undoubtedly would have been better.

The British Aerospace 146/Avro derivatives sold in greater numbers than the poor reputation of the airplane would suggest. With four engines of an initially troublesome design and a cramped fuselage that made its designed 3×3 seating nearly untenable, the airplane sold much better than most European designs of the era.

The chart clearly indicates that until the advent of the Bombardier CSeries, every airplane was a derivative. The Embraer E-195, itself a multiple stretch, barely falls within the 100-149 seat sector, and hasn’t sold especially well but which is certainly a contributor to the overall program profitability. The new E195-E2, which doesn’t enter service until 2019, has been stretched again to seat 133 passengers. We expect this re-winged, re-engined airplane to be a better seller than the legacy E-195 and to be the principal competitor to the CSeries.

The A319neo, 737-7, CSeries and E195-E2 are too early in their sales programs to definitively rate based only on firm orders. We believe the CSeries program, with 543 orders and commitments, will be a success as commitments are converted to firm orders and new orders obtained. The CS100 will be a niche airplane for difficult airports.

Airbus now has 49 orders for this model. Qatar Airways upgraded its A319neo orders to the A320neo, but Avianca upped its order to 19 and there are 12 from Unidentified(s). Absent delivery schedule for the Unidentifieds, the first delivery is in 2017 to Avianca. Frontier Airlines follows in 2019. We believe Frontier is likely to upgrade to the A320neo now that its business plan evolved to that of an Ultra Low Cost Carrier for which maximum seating is desired. It would not surprise us to see Avianca also upgauge. In any event, we believe the A319neo’s future rests with the Airbus Corporate Jet and not the commercial airline market.

The 737-7 doesn’t enter service until 2019. Only Southwest Airlines and WestJet have ordered the airplane. By the time it comes to cutting metal c.2017-18, we would not be surprised to see these airlines upgauge to the 737-8. We have our doubts whether the 737-7 will ever be built.

Others

Sukhoi and Mitsubishi currently play in the 60-99 seat space. Both indicate they may develop a derivative of their current offerings that would trade in the lower end of the 100-149 seat sector. At this stage, however, they are non-factors.

Conclusion

Bombardier and Embraer will “own” the 100-149 seat sector. Embraer will do better within the 100-125 seat subsector and BBD will do better in the 126-149 seat sector. Airbus may have a very small contribution. We have our doubts whether Boeing will be a participant in this sector.

The BAe-146 is a strange aircraft. Its engine offered the best performance in its class for years. It became obsolete when the CF34 appeared (first on CRJs in numbers, climbed from 9klbf to 20klbf). Compare the Fokker 100 with its “leaky turbojet” (bypass of 3) or the smaller MD-variants with the JT8D with a bypass of 1.5ish. Also, the high bypass offered much better noise values.

The engine has severe issues with air contamination and reliability (for a commercial fan), but performance was apparently quite good.

good performance _and_ rather low noise footprint aka “Whisper Jet” ( alt: Jumbolino 😉

Human being, just like any other animal, prefer symmetry. I think that has been the core problem here. Seating 130 pax in a 2+2 body makes a very long body, 3+3 a rather short and tubby one. Both versions are not ideal for weight and arodynamics. The relation between diameter and length is very critical for the performance of the design.

Sukhoi and Bombardier Engineer have got it right with the 2+3 seating, and I think this is the key element for this segment.

Maybe the situation about Russia and Ukraine will stabilise in a good way, then we might also have an interesting competition with the Superjet. It sure is a good looking bird.

Ukraine is SOL denuded of anything valuable.

Mostly due to their oligarchs under western guidance having unfettered access.

Wait for the next winter and the exodus of western friends.

The Eastern Ukraine could fare slightly better with association

into the Russian Federation.

What’s the matter with you Uwe? Are you watching too much Russian TV? Please just leave all propaganda out of this forum and we will get along fine.

Matter of fact is that with current situation no western airline will buy a Russian plane, no matter how good it is or how you judge the political situation. That is really sad, because guys at Sukhoi have certainly earned some success with the Superjet.

(In my company I have three guys from the former USSR, one of them from the Ukraine, so I think I am quite well informed of what is going on there, but again, this is not the place to discuss it.)

With the Superjet out of the race, if Bombardier does not make any serious mistake, they look like a future big winner. I don’t see any other players entering this game for many years to come.

This comment violates our Reader Comment rules WRT Nationalistic attacks.

The C-Series’ fuselage diameter is just slightly smaller compared to a 737 fuselage. I would expect Ryanair to fly with 3+3 on C-Series.

The E-195E2 with 132 seats at 31 in pitch has about the same capacity as the C-300 and is only about 3 meters (7 %) longer than the 38.7 m long C-300.

http://www.airlinereporter.com/2012/02/tour-of-the-bombardier-cseries-mock-up/

They have done the math – the seats would only be 15.8″ wide. That would not even work for Asia. So no 3+3 for Ryanair.

In other news; 747-8F orders almost +1

https://www.youtube.com/watch?v=bnBr3enzW1I

(just in case anybody missed this)

Boneheaded stunt, pilot should be fired.

The issue that is always overlooked in the 130 to 150 seat class is that in the short to mid term there are sufficient aircraft operating in that segment to cover most requirements. 10 years from now we don’t know what that market will look like but we can guesstimate from current trends: LCCs and ULCCs will continue their market share growth with +150 seat aircraft. There will be continued industry consolidation, thus continuing the up-gauging requirement. Furthermore, within 10 years time we’ll be much further along on the fuel demand destruction curve and oil prices will stay static or even decrease as per Pilarski’s prediction.

And with fuel prices falling quite fast?

An item of note, Ak Ailrines says their 737-900ER operates for the same fuel use as the 737-400.

http://www.adn.com/article/20141007/alaska-airlines-orders-10-new-boeing-737s

One way to put things in perspective, 181 carried for same fuel vs 144

And if fuel stays low what does that do to the whole range of order books? Good deals picked up on current offerings and delay the NEO offerings?

It should be interesing

15% less is always going to be 15% less, what’s not to like? and I doubt whether we’re going to see a spectacular fall in fuel prices.- particularly if the IS sphere of influence spreads.

But 15% is not always 15% and is not always going to be worth it. 🙂

By the 15% is 15% recoding the old days of fuel hog aircraft makes no difference.

At some point it cams over and becomes a much lower part of your operating costs.

My recollection was its used to be 30% and now its 60% or better.

Lower it is, less impact and the more other things affect.

So yes it does matter, Delta with its older fleet is more competitive and the rational for needing more fuel efficient aircraft can become muted, decent is good enough (like CEO types)

And ISIS has not affected oil, you can bet its boots on the ground if they do so that is not a factor.

US is now exporting oil, there is at least a short and mid term paradigm shift going on.

We live in interesting times

Low oil prices is more linked to political measures than anything supply demand driven:

http://www.reuters.com/article/2014/10/13/us-oil-saudi-policy-idUSKCN0I201Y20141013

Low oil prices will hit IS, Iran, Russia ( US interest ) _and_ will inhibit investment in extraction infrastructure ( Saudi interest ).

Expect an elevated “normal” market in a couple of years.

Low oil price fundamentals are here to stay, save for the occasional short spikes. Demand destruction is just picking up steam and fracking costs will be coming down. Countries dependent upon crude revenues are fracked. 😉

I´m going to buck the trend here and say the 100-150 at business will be more important than people guess. Main growth market China is building HS rail like crazy, EU already has a lot of HS rail but what people haven´t noticed is that the ticket price, traditionally high on EU trains, is coming down. India has always been a big rail country. I see 100-150 as a safer bet in some ways as destinations using these aircraft generally aren´t worth the high cost of HS rail lines.

As an airline a new developed 150-seater allows to reduce capacity and remain profitable. Today larger aircraft and/or more seats are ordered to reduce cost per seat. However, market doesn’t grow as quickly and hence overcapacity ruins prices. A single class domestic CS130 seats roughly 135-140 people, same as an A319 in the old days. It can be assumed to be 6t lighter in empty weight and up to 10t lighter in take-off weight for a mission.

That would be the conventional wisdom but it isn’t working out that way. Look at Delta Airlines. Airlines will hold onto their NBs as long as possible because of lower capx/lease (or already capitalized) plus route planning flexibility. With sinking oil prices it makes it all the more easy to hold onto older metal.

You say the BAe146 “sold in greater numbers etc” but it did not “sell”, most of them where leased at favorable/subsidized terms thus inflating the “success” of the aircraft. Once production ceased and the real numbers came out, BAe had to do a “Billion pound” write off and still had 100s of 146s/RJs on its balance sheet, the real story is that the 146 was a disaster for BAe…they should have stuck to the decision Hawker Siddeley made when they cancelled the program earlier, instead of “re-launching” it.

Could you please glue together “leasing” and “writeoff” with some facts?

Off the cuff the write-off looks more like it is linked to the creation of “Avro RJ Regional Jets” for developing the RJX derivative that did not go beyond 3 prototypes.

150 seats is single aisle territory. 200 seats and it’s time for a double aisle.

Indigo orders 250 A320 NEOs.

http://www.bloomberg.com/news/2014-10-15/airbus-wins-accord-from-india-s-indigo-for-250-a320neo-airliners.html

250?!