Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Airbus easily leads narrow-body backlog, Boeing ahead in wide-bodies

By Scott Hamilton

Feb. 5, 2018, © Leeham Co.: Two thousand seventeen is over and the numbers are in.

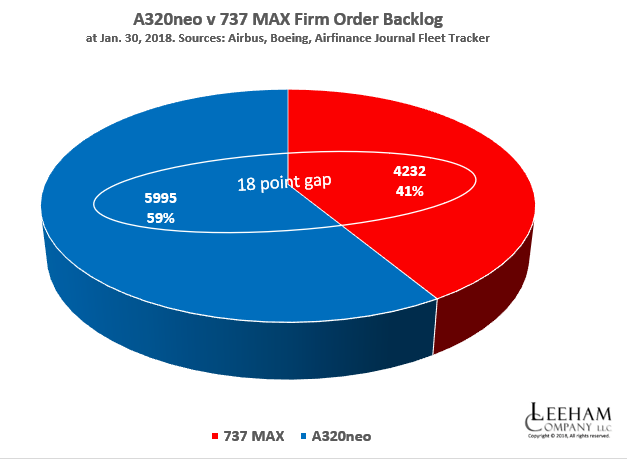

Airbus continues to have a commanding lead over Boeing for single-aisle, neo v MAX backlog.

Although Airbus got pounded by Boeing in wide-body orders last year, the backlog tilts only slightly in Boeing’s favor.

Narrow-bodies

Looking only at the A320neo family vs the 737 MAX, Airbus had a 59% market share of the backlog at Dec. 31. Adding the ceo and the NG makes no difference; there was only one airplane difference between them.

The addition of the 737-10 to the MAX family, coming at mid-year, only marginally helped Boeing: there were about 150 incremental orders after swaps from the 737-8 and 737-9, launching the program at the Paris Air Show.

The shortcomings of the MAX 7, in our view, have been discussed many times, so I won’t repeat them here. Its future is that of a niche airplane for airlines, a BBJ and as a military transport, in our view.

The MAX 9 was getting killed by the Airbus A321neo sales, so Boeing launched the MAX 10. LNC has written that the MAX 10 gave Boeing a product that’s on an economic par with the A321neo (Boeing and Airbus each claim the advantage; our independent analysis shows there is “economic indifference” between the two.) It was creation of the MAX 10 that put Boeing in the race for the Delta Air Lines order, which ultimately went to Airbus, but which was a highly competitive race.

But the MAX 10 has field performance issues that can’t match the A321neo, giving the latter airplane its historic advantage over the MAX 9.

While Boeing sharply trails Airbus today in market share, this is, perhaps, a bit misleading. A far larger percentage of A320 family operators ordered the neo compared with a smaller number of 737NG operators. Based on this alone, Boeing has more upside to regain market share than Airbus has to maintain its lead.

Airbus needs to grow the market for the neo, which it can do at the lower end of the Middle of the Market sector with the A321neo—something Boeing can’t do with the MAX 10.

Emerging competitors

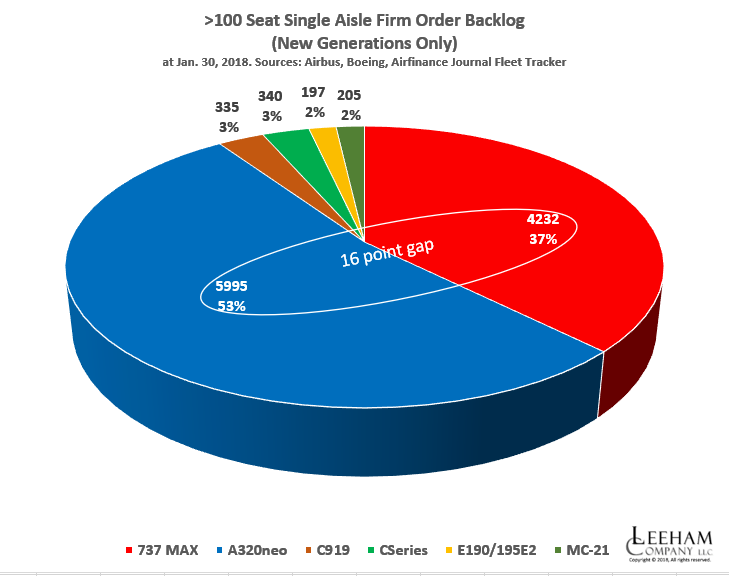

Boeing’s market share looks worse, however, when the emerging competitors in the single-aisle sector are factored in.

Airbus’ commanding lead over Boeing shrinks slightly when these competitors are factored in.

Bombardier and Embraer cover the low end of this sector, 100-150 seats, that Airbus and Boeing essentially have exited. The A319neo and 737-7 are largely rejected by the market.

The COMAC C919 and Irkut MC-21 don’t have much market penetration and as yet are restricted by market forces to their home countries.

None of these four OEMs command more than 3% of the backlog of new generation aircraft. Collectively, they capture 10% of the market. This reduces Airbus’ share to 53% of the single-aisle backlog and Boeing to just 37%.

(If Bombardier’s C Series is lumped in with Airbus, pending the acquisition of 50.01% of the program, Airbus’ share climbs to 56% of the six OEMs.)

It’s a surprisingly low showing for the venerable 737.

Boeing needs to new airplane to replace the 737. However, with a MAX backlog of more than 4,000 aircraft, Boeing isn’t hurting. In fact, the financial results from the 737 program, along with the increasing cash flow from the 787 program, are staples of Boeing’s financial performance.

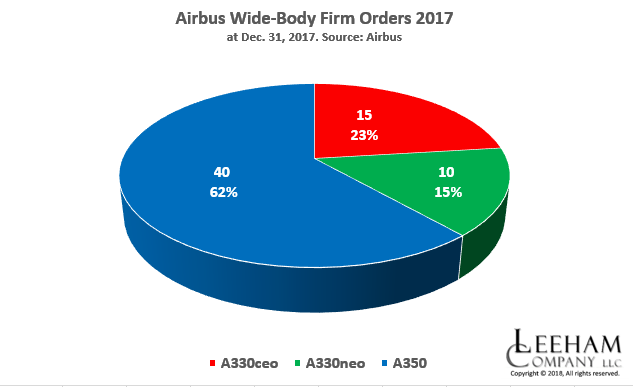

Wide-bodies

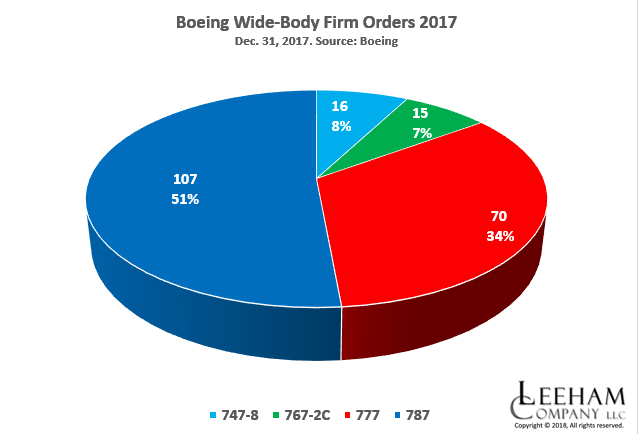

Last year was Boeing’s year for wide-bodies. Boeing captured 77% of the firm orders and announced commitments for many more. The Emirates Airline order for 40 787s, announced at the Dubai Air Show in November, wasn’t booked into last year’s tally.

Boeing ended the year under a 1:1 book:bill for the 787—it hasn’t won more orders than deliveries since 2013. Had the EK order been firmed up, the 1:1 would have been reached. But the deal gives Boeing a good jump-start on this year’s contracts, when it’s firmed up.

The 777 did well, logging 70 orders—43 for the -300ER, 20 for the 777X and eight freighters.

In all, there were 208 orders for all types.

Airbus trailed badly, with just 63 orders, adjusted for the cancellation of two A380s. The A350 won 40 orders. The A330ceo won 15 and the A330neo won 10.

The A330neo continues to struggle in a low-price fuel environment.

However, as badly as Airbus was thumped last year, the backlogs are close: Airbus has 1,123 wide-bodies in backlog at December 31; Boeing has 1,158.

Emirates order for 40 of the 787’s and UPS order for 15 747 waiting to be finalized, Boeing has jump started 2018.

I am still waiting for Lufthansa to order maybe 10+5 777F, – as the MD-11F’s are approaching 20 years, and I had expected them to order last year. However Lufthansa CEO Carsten Spohr has said in public that they maybe did order to many 777X and to few A350’s. And a solution could be to swap some orders from 777X to 777F. Just guessing.

KR/Airboe

Imo LH has to replace a lot, the MD11 might not be top prio.

As one of the few carries out there, they didnt go for B787, but have a need for their A330 replacement. The oldest are 2004/05, so 15 years soon.

Austrian needs to replace it B767 – and their B777 are pretty old to.

There might be another battle between A330(neo) B787 and A359.

LH also has a need on the lower end, where all of their airlines are operating a wild mix of regional airplanes, Dash, E-Jets, CRJs, Superjets, Fokkers and CS.

Getting this uniformed could be a great way to save costs.

A340 is leaving all Airlines, A350 coming.

B779x is the replacement for B744.

But i found different numbers – 20 till 34.

LH is so busy with EW…

Who operates Fokker? And who SSJ?

The UPS order is finalized and the total for 747-8F is 28.

I believe it was 14 options, but those have been firmed up.

Add in 4x767F for UPS.

Nice bonus will be the deliveries of the KC46.

The FOKKER’s just left Austrian (late Nov. 2017) and CityJet is operating SSJ’s on behalf of Brussels

Flight global seems to think UPS has 32 747-8F ordered?

https://www.flightglobal.com/news/articles/ups-expands-nonstop-to-dubai-using-747-8f-445554/

I think FG added the 767s they ordered.

UPS does fly a lot of MD11 and 767 through Anchorage.

MD-11s are not top prio. Cargo frames can and do fly forever due to low utilization and “passengers” that don’t complain!

A330s can be simply shuffled to Eurowings when LH mainline deems them too outdated. A350 seems to be the anointed replacement.

And you’re right on OS’ long-haul fleet – that will need a replacement sooner rather than later. I also see the 359 for commonality’s sake with LH similar to their future A320neo fleet.

And yes, the real fireworks is the regional fleets, but I can already see the BBD CS winning out. LX seems more than thrilled with their’s.

Oh on the subject of fireworks, but of the boardroom variety: LH seems to have peeved off an entire country with the SN/EW consummation, interesting to see how that turns out.

…and their new livery seems to be going going like a lead balloon?

Cargo planes can fly almost forever – remember cardboard does not complain about paxex! I can see LH’s MD-11s go for another 10 years minimum. And when they are ready to retire those they can convert their passenger 744s to cargo and keep those flying – that ought to be more economical than retiring them and inducting another type or purchasing more 777Fs.

Perhaps you mean the 19 8Is?

And with Emirates’ 360 A380s and Turkish’s A350 order, Airbus seems to be off to a good start as well…

36 A380s obviously.

Scott, do you have any update on adding comment edit functionality?

Has anyone noticed this interesting sales trend common across Airbus and Boeing widebody types today?

Boeing:

“The 777…logging 70 orders—43 for the -300ER, 20 for the 777X…”

Airbus:

“The A330ceo won 15 and the A330neo won 10.”

Older version out-sold the newer version for both veteran widebody families.

I recall decades ago /b4 the mid-90s, newer version typically sold @ least as well as the older version fm the same family during any given yr e.g. A300-600 vs A300B4, 744 vs 742/3, M11 vs D10…

A few possible explanations:

1. Manufacturers are more aggressive in pricing(not the official list price) older versions than decades ago to fill the production gap(and therefore cashflow gap) fm old to new?

2. Buyers(airlines or lessors) today are more interested to lower CapEx fm older versions than to gain whatever improvements fm newer versions?

3. Diff between new vs old these days is mostly in fuel burn. Most buyers are projecting a generally low oil price level will remain throughout asset’s econ life time which diminishes the value of new vs old?

4. In cases of fleet expansion, buyers are more interested in commonality than superiority – more of the older version is better than inducting newer version?

5. In cases of replacing older version, buyers lean more towards alternative clean sheet design than the newer version of the existing?

Interest points

Specific to the A330neo I see it as a tough sell. From Airbus they are offering it somewhere between a A330ceo and A350, so the airline has to have a very specific niche within which the neo comes out as the best option. If you want cheap go ceo, if you want capability and future proofing go A350.

And of course it stands opposite the B789 which is probably the most sought after wide body in the Boeing stable by some margin. I reckon it takes quite a lot of pencil sharpening to make a unique case for the neo.

Re the B777 I think Boeing has done a solid job of bridging the transition but it must have bit at wafer thin margins on the W, and who said this was a bad plane? They have sold north of 800 of them.

The amount asked for the X could easily be $50-100m more (educated guesses before you hold me to them) for what is in some respects essentially the same thing.

I was surprised the the first time I saw the small price differential between the 339 and 359, was wondering if AB actually wants to sell 333’s as long as possible while sorting out the NEO’s.

The 330NEO could proof to be a better than expected aircraft but airlines may be concerned if the T7000’s will run into the same problems as the T1000 engine?

I believe that a LGW A339 with MTOW around 230-235T, 5500-6000Nm range, 68Klb engines and a lucrative price could sell well end of the day.

AB maybe also had in the back of their mind that current 332/3 operators that want to keep things simple and not introduce a new type in their fleets will buy 330NEO’s, this still could happen.

I don’t have the order break down, but commonality being maintained would probably be the CEO sales reason.

Like the 767, its still a very good aircraft and a market for it.

The A330neo seems more conflicted as neither fur nor feathers.

Not enough gain and changes when you need a significant numbers of hem to justify orders. Delta yes, rest ?

At one stage (and still) I sounded like a stuck gramaphone on an 330-200X with the NEO’s aerodynamic and wing tweaks and cabin/cockpit updates.

Sure GE and/or P&W will be happy to see if they could squeeze some small (1-2%?) improvements from their CEO engines without breaking the bank.

Trouble is A330 has heavy long range (A340) bones, and they won’t get any lighter unless it’s is replaced completely. Wonderful design, it should never have been a sucess in in the first place, but its origin is catching up with it on medium range routes.

All wide bodies are heavy at the moment (excluding the 767’s).

An 787-9 is ~7 tons (OEW) heavier than an 330-300 (339?). That’s Boeing wants to change with NMA/MoM.

We will know how the A330-800 will sell only when the Trent 7000 has shown it reliability and performance and when the -200 production is terminated – and when and if Boeing comes up with small twin-aisle. If all goes well with the Trent 7000 and no NMA is launched (and at what price???) we may very well see some rather strong sales of the -800 to replace aging 767s and all kinds of A300/330/340s in the next decade.

On the other hand, if Boeing comes up with a really good concept for a NMA and the Trent 7000 is troubled, well then the -800 is probably as good as dead.

Something just crossed my mind, maybe someone said it somewhere?

But what is the probability that the 797 is basically an 767X along the lines of the 777X with Li-Al fuselage, CRP wing, Ultrafan engines? BA could draw from the manufacturing experiences gained from the 777X.

This fuselage will pave the way for future freighters, tankers whereas CFRP fuselages have limitations in this regard.

Could be a bloody nice aircraft (as long as they don’t go 17.2″ with 8 abreast seating).

Good points you made Ted. Think lots depends on the T7000’s.

AB seems to have a winner in the XWB84, XWB97 long way to go.

BA seems to want get rid of the 788, the NMA looks like not more than 5500Nm range. The 338 could be shy of the 789 on seat mile cost but could equal its range (251T-at least) and have better sector costs.

The 338 and 359 could be a potent pigeon pair for airlines operating long range. In my view the B787-10 is what AB needs to address.

Gundolf:

An A330-800 is going to be a very heavy aircraft.

Better off to keep running your 767Ws.

@ TransWorld: Weight is NOT the primary issue when it comes to airplanes, otherwise todays planes would have stubby wings and tiny engines. The longer wings and more efficient (larger) engines are what made the A330 the more efficient plane than the 767 and finished it off for good.

By increasing the size of the fan and improving the bypass ration the Trent 7000 obviously also became more heavy than the 700, but of course it’s more efficient again.

The A330-800 has similar or even lower trip costs than the 767 but is much more capable in pax number, cargo and range.

(Besides we should also not forget about the supercritical profile of the A330 and FBW, which the 767 is missing too.)

@Anton:

“…wondering if AB actually wants to sell 333’s as long as possible while sorting out the NEO’s”

Pls elaborate what do U mean by “sorting out”.

“330NEO could proof to be a better than expected aircraft ”

New types often turn out to be better than expected regardless of whether it’s an Airbus or a Boeing. Fm as early as 2004 upon launch, most folks(myself included) already expected 789 would be capable of ranges even @ the extreme end of the 77W range envelope. However, almost no one(again including myself) expected a 789 to be econ sustainable to fly SFO->SIN nonstop on a yr-round basis clearly beyond 77W capability…let alone the even tougher stuff like LAX->SIN and PER->LHR by nex mth all to be done by 789.

The point is doing a job type “better than expected” is not really relevant to sales improvement when such job type(i.e. size+range combo) is needed by so few customers(i.e. small potential mkt) relative to another job type(i.e. large potential mkt).

“..airlines may be concerned if the T7000’s will run into the same problems as the T1000 engine?”

I think @ least for those serious airline buyers who would look into really really basic details can easily recognize that:

1. There’re really two generations of T1000 flying:

T1000 and T1000TEN

2. The “problems” are exclusive to T1000 but not T1000TEN.

3. T7000 has nothing to do with T1000 but has everything to do with T1000TEN (U think it’s just pure coincidence that the 78J and 339 are certified with T1000TEN and T7000 respectively only within 6mths of each other?)

4. Even if U want to order any 787 today and must hv a Trent, RR may not even want to sell the T1000 for your 787 and tell U to order the T1000TEN instead.

So as long as an airline buyer is not ignorant for millions $ of investment, T1000 issue on 787 is @ least technically irrelevant to whether a 330Neo commitment is too much risk.

“LGW A339”

Pls explain how to arrive @ such theoretical machine? Take out all the seats and let pax seat on the cabin floor and hope all flyings will be under the FAA/EASA reg radar? Or Airbus somehow purposely put more gross weight than necessary on its current 339 just for amusement and therefore leaving room for U to suggest a brilliant “LGW A339” on a forum?

“MTOW around 230-235T, 5500-6000Nm range, 68Klb engines”

U honestly believe a de-rated 339 can’t achieve all of the above?

“and a lucrative price”

And as usual, U assumed Airbus has not already been offering that re 330Neo for the past 4yrs.

“…could sell well end of the day.”

If that’s the case, firm order total for Max7/319Neo should be well beyond 200 units each a long time ago.

“…current 332/3 operators that want to keep things simple and not introduce a new type in their fleets will buy 330NEO’s,”

That’s the well-known theory behind the 330Neo launch decision not just for Airbus but for everyone who knows what is a 330Neo already knew about, again, a long time ago.

“this still could happen.”

Anything “could happen”….including hundreds of Max7/319Neo being ordered in the future….no matter how unlikely.

But the real billion $ question is:

Why it has not happened to 330Neo and does not appear will happen soon?

I mean:

a) 330Neo has been on sale for nearly 4yrs(even before official launch). That’s not a short time to try to sell a new & improved type.

b) Only a tiny % of 330Ceo operators hv ordered 330Neo. In fact, among the top 15 airline customers(everyone else has fleet size below 15) for 333, only AirAsiaX and GA hv ordered 339.

Time will tell, if the 339’s seat mile cost is closer to the 789 than predicted (especially by Boeing) and the T7000 proves reliable interest in the 330 NEO’s may increase. Availability of delivery slots and potentially lower pricing could change a few things.

(p.s. Wonder how the seat mile cost of an 8 abreast 789, as it was intended to be, and an 339 will compare?)

@Sowerbob:

“Re the B777 I think Boeing has done a solid job of bridging the transition”

Ditto Airbus re 330Ceo->330Neo.

“but it must have bit at wafer thin margins on the W…have sold north of 800 of them.”

Purely my guess:

The last batch of 77W, say the final 100 frames, probably was/will be sold @ near breakeven.

The 1st batch of 77W, say the 1st 100 frames, probably were sold @ below breakeven circa 2000 upon program launch thx to typical launch discount.

Still my guess but a very high probability:

The middle batch of 77W, say about 600 frames, were most likely sold @ eye-watering profit margin…especially when 346 sales was practically dead and 35K was still about 7~10yrs fm cert(in hindsight).

“..the B789 which is probably the most sought after wide body in the Boeing stable by some margin”

My theory re why:

It has the most sought-after combo of size+payload/range in the global mkt.

How so? Just look @ the key characteristics of the top 2 sellers(specific variant of a family) in the global widebody mkt b4 the 787/350 EIS:

#2 best seller=333

About 300 seats in Airbus nominal 2-class config(or about 290 if in Boeing nominal config). 786 frames sold as of Dec2017 and we know most buyers bought it clearly not because it offers the longest range capability among all types in service.

#1 best seller=77W

About 7,400nm range in Boeing nominal config (or about 7,600nm if in Airbus nominal config). 839 frames sold as of Dec2017 and we know most buyers bought it clearly not because it offers the largest seat count(even in 10abreast Y) among all types in service.

In essence, Boeing fused the seat count of a 333 with the range of a 77W to create the 789 and naturally, it caters to buyers which must hv 333 size but do not mind more range and to buyers which must hv 77W range but do not mind fewer seats(Paraphrasing legendary AA ex-CEO Robert Crandall – Airlines NEVER go broke due to not having enough seats to sell). As a result, 789 sales already reached 700+ today on par with the previous champions. To a slightly lesser extent, the 359 also found as much mkt acceptance as the 789 with sales being far superior to any other Airbus widebody type on offer(In fact, #2 only behind the 789) because its design aims @ a very similar size+range combo as the 789.

No 330Neo variant falls within that ultra popular size+range combo.

Saw a speculated date of 2028 for the EIS of a 330 replacement, interesting that this will be only a year or 3 after the “797”? By then the Utra-fan should have sorted out its growth pains.

Interesting is that A330 production from 2007 to 2017 was about 940 units, this will make the 330NEW available for a large number of 330 replacements.

Also, Boeing delivered 300 B788’s between 2012-2015, those operators will then have an option of a very new aircraft as replacement.

@Anton:

“Saw a speculated date of 2028 for the EIS of a 330 replacement”

Where and by whom? Some Airbus enthusiasts/lovers on an aviation forum? Perhaps only U would equate ‘speculation’ with ‘dreaming’.

To the best of my knowledge, Airbus has never officially talked about any 330 family replacement(Note: 330Neo is 330 family) except the 350 ten years ago.

” interesting that this will be only a year or 3 after the “797”

Nope, not interesting and totally expected fm such speculation. Such date is speculated PRECISELY because the 797 MAY come 1-3yrs before that date i.e. ‘dreaming’ something fm Airbus to kill the 797 head on when even the 797 itself is still a bit of a dream today…….classic kindergarten playground toy dynamics @ work….

“By then the Utra-fan should have sorted out its growth pains.”

Pls kindly explain how a future RR product based on UltraFan tech is available only for a 330 replacement but not for 797(or anything else for that matter).

“Boeing delivered 300 B788’s between 2012-2015, those operators will then have an option of a very new aircraft as replacement.”

I’m speechless re your far-fetched dreams.

1. A 2015 vintage 788 will be only 15yrs old by 2030…well before typical retirement age….but I guess that doesn’t matter to U because “330NEW” will be so good that 788 operators will completely ditch their CapEx financing /retirement cycle model in order to access the divine “330NEW” as replacement.

2. If U can speculate as far as a 330 replacement, why not a 787 replacement as well….or even a 797 replacement? We can play this game all day long…

So you expect Airbus to do nothing over the next 10 years and Boeing everything?

@FLX

I agree with almost all you say, I focused on the W bridge as it is still a WIP whereas the ceo bridge was largely completed a couple of years ago. Further there is a desire to keep the ceo in production I understand whereas the W will bow out to the X in due course.

I see the W in the past 10 years and the B789 today as the ‘ultra winners’, those frames that can command a premium price on every sale

The question is the same on single aisle. Is the MAX strategy a stroke of genius that ensures quite unseemly amounts of cash to be generated and shovelled into the mouths of shareholders in the form of dividends and buybacks?

Or is the MAX the beginning of the end for Boeing as it cedes any suggestion of ownership or domination of this market to AirBomb? By my reckoning they have 12-18 months at least to sort out some sort of NSA/NMA strategy given backlogs and what seems to be a lot of ‘natural’ B737 replacement orders in the pipeline.

Boeing will be fine. “The Dude abides, as does the stock!” LOL

Are you saying ‘the MAX really hangs the company together’?

The Max and 787 are GUSHING cash flow! And what’s the point of more than 3 1/2 years’ worth of backlog—UNLESS you’re expecting massive cancellations and/or Air Berlin type collapses?

When was the last time of major cancellations in the aerospace sector? Was it around 2002 when many airlines World wide saw a turn down and cut their orders? I think after Sept. 11, 2001…

As we have just seen at the stock exchange, linear movements can all over sudden experience a most unexpected crash.

The 737 backlog might very well fold IF the A320 production gets expanded, the GTF becomes not only perfectly reliable but receives a PIP of several %, the CS300 is produced in significant numbers and the economy takes a bit of a dive. Impossible? I don’t think so.

The stock exchanges really took a knock this morning. Had me nearly reach for a Scotch before 12H00.

Never say never, things can go pear-shape very quickly.

@Gundolf

Without wishing to tempt fate the MAX is in the weaker position, but if you want any SA delivery in the near to medium term it is really the only thing on offer alongside the neo. Do you really think the supply side will move any time soon?

@sowerbob

from what I gather Airbus is expanding A320 production in Tianjin and in Mobile. If you factor in at what time Airlines really need their new planes and again taken into account a possible economic downturn then yes, short term delivery will all over sudden not be an issue any more and decisions which plane to buy will mostly depend on performance and price. That could very well cut the life of the venerable 737 short.

I think both, The 737 is so profitable for Boeing that they want to hang into it forever until they are way too late for a replacement. Airbus can do the A322 now with new composite wings and upgraded A321neo engines and price it high making Boeing feel safe, then at a suitable time pull all stops and make 40 a month of the rewinged A321/A322 for a new price with todays A320/A321neo’s making up the rest.

Assuming Boeing is going for UF-engines the price of those could mess up the BAC NMA cost.

AB could potentially use beefed up PW1100G’s that has cut its teeth and offer an 322 at a good price with an engine whose teething problems had been solved.

Shades of Henry Ford and the model T.

When the market went out from under it, it went down like a rock.

AB could burn its fingers with the 322 if they not careful? My view is keep it relatively simple, and fight within your weight group.

With a new wing (38-40m) and landing gear increase the range of the 321LR (4500Nm-180/190 pax) and have an 322 stretch with 20-25 more pax than the 321 with a comfortable 3500 NM range (length 47m = 752).

With ~35Klb engines and MTOW of 100-102T this is realistic and should not break the bank.

Airbus must be careful not spending too much on the A322, a contianers width stretch for and aft the new winbox might be enough, a 35k verion of the neo Engines plus a new carbon wing that can allow 2-4″ wider Engines. Still this little excercise will burn almost $7-10bn and take at least 4-5years.

That’s serious. Rather build an NSA or 330 replacement. Can’t see a huge market for the 322 (500?).

Maybe update the current wing with 350-like new winglets. Will take it over 36m but not cost and arm and a leg, fuel capacity a big question. Stay with the current 81″ inch fan engines?

Claes you seem to be closer to the numbers what things cost. What will the approximate cost be to do a ~3.5m stretch of the 350-900.

Certification with the current wing, bogies, and possibly XWB-EP’s?

@Anton, Re: A350-900 stretch. It depends a bit on Udvar Hazy and what he wants and can calculate a good return and profit for the operators buying it. I think he would like to see the TXWB-97 derated installed so the A350-1000 operators getting Close to 0C EGT margin can change dataplug and dataplate and get 15C extra EGT onto this A350-900+ swapping around Engines from new A350-900+ to the A350-1000. The difference in length between the-900 and -1000 is approx 7 meters. Going for half that stretch looks like just a extension fwd of the wingbox and space for 4ea extra LD3’s.

The modified wing and winglets for the A350’s make the -900 wing sufficient for this design with 4 Wheel boogies. It gets shorter range and a bit more pax/payload. I would guess a 4 year program and $8bn. Airbus will do the A350-900ULR Qantas double sunset Aircraft first. Putting the A350-1000 fuselage onto a -900 wing/gear/engines might be quicker/cheaper for a $3-4bn program.

Still the Trent XWB-97 is only 600lb heavier per Engine and Airbus claimed the wing had margin. We do not know yet how much better the TXWB-97 is. I suspect it will be much cheaper to maintain due to different core Engine design so RR should push it giving operators more EGT margin for similar Total care payments hence RR will see this engine less often in shop and customers just pay and run it watching EGT margin slowly disappear over the years as expected from a great RR engine.

Thanks Claes, much appreciated.

My thoughts more towards what AB can offer airlines as alternative to the 787-10. Both current 350’s seems to be (very) long range orientated.

That’s why I see an 350-“950” (70m) with 20-30 more pax, 7000/500Nm range and 359 “goodies” a hypothetical aircraft that could tick a lot off boxes for many airlines.

Seems rich to me, the A350 program was $12B. Maybe I talk in circles, a “simple”stretch of the 359 (3.5m), basically all the rest the same. (Personally I think AB should not lose the plot with QF, they seem to be caught in the Boeing web).

More pax, less range. Could even go the original 359 MTOW of 268T.

A simple stretch sometimes is not so simple, but you are correct that is should be easier on a fly by wire Aircraft. The advantage Airbus has is that the “original A350-1000” was already designed and analyzed when they decided that it could not replace all the 777-300ER missions and then the A350-1000 was restarted. So in a parallell to the A330neo much of the work has been done saving time and Money. Many development programs to strech an airframe also incoporates lots of improvements blurring the costs. The 787-10 has the same MTOW as the 787-9 of 560,000 lb and OEW of approx 300 000lb. The A350-900 comes with MTOW of 617,295 lb and a similar operator OEW of +300 000lbs. A “half stretch” of the A350-900 gives approx 20 more seats to 345 and a “full stretch” 40 more.

The other option is the stretch the A330-900 with 4 rows in front of the wingbox giving 32 additional pax taking it to approx 320pax similar to the A350-900 and 787-10 but a much cheaper Aircraft to produce but heavy at OEW 342,000 lb for the present A330neo-900. Just stretch it you get into the A340-600 problems, too Heavy.

If you do a 4 row stretch (+4 LD3’s), massive weight reduction and reduce fuel load and derate the Trent7000’s you get into a new A330neoRe design that might be popular as a MoM competitor and a new Beluga, but it looses the flexibility to do longer routes. Still it should do the Atlantic and all trans continental flying cheaper than the 787-10 until it gets killed by the much lighter 797.

So it looks like the 787-10 is pretty efficient for its routes with its smaller diameter fuselage, composites and most modern Engines available.

The A350 is a bigger Aircraft more expensive to make and is a good 777-200LR/-300ER replacement but will have a hard time to be made as cheaply as the 787-10, Airbus real chance to beat the 787-10 is with a new A330Re that had major surgery that can compete on price until Boeing gives up the 787-10 and switch to the 797 that will almost hit 300pax that Boeing hopes finally should kill the A330.

“The A350 is a bigger Aircraft more expensive to make and is a good 777-200LR/-300ER replacement but will have a hard time to be made as cheaply as the 787-10,..”

do you have anything tangible to give this statement some substance?

The perception is created that the 350’s are heavy aircraft (by Boeing?), to put things in perspective.

B789/290 seats/OEW 129T), 445Kg/seat,

A35K/366 seats/OEW 155T, 424 Kg/seat.

And that is the 35K in relatively low density seating, large wing and 6 wheel bogies (and you have wider seats!!!).

The 359’s OEW range between 135T and 145T, the heaviest option (145T) gives 446Kg per seat OEW, which is for all purposes the same as the 789.

… and by the way, the OEW per seat of the 339 is approximately 430Kg’s, 15kg per seat less than the 789, and, you get a comfortable 2-4-2 layout with 18″ seats. Do Boeing tell airlines that?!!!

Rest my case.

A350-900 bigger in size than 66.8×64.75m the 787-9 62.81 x 60.12m and a smaller diamter fuselage. The A350 has no Engine option with a heavier Engines.

The A350 is quite effective with good range but still more expensive to build.

It is quite natural as Boeing was forced to improve alot for the -9 and many big sections comes from suppliers with goverment backing guaranteeing Boeings margins on the -9/-10. Boeing is paying of the 787 development pretty quickly now. Airbus most likely follow the same type of cost reduction curve but are not a Boeings levels yet. Just looking at list prices there is a $36M difference indicating an approx $20M difference in manufacturing cost.

The 2018 list price of the 787-10 is ~$8M higher than that of the 359.

Just another point, the Airbus aircraft prize includes outfitted cabin, the Boeing’s not.

“Boeing is paying of the 787 development pretty quickly now. ”

Boeing is reducing deferred _production cost_ ( @ $2B/a for about a 12+ years target to zero.

List prices are not really linked to manufacturing cost but more to what the manufacturer thinks is the relative value if this airframe. Only once was this broken for a time in the initial 787 offering: list well below the comparable A330 ( because it was to cheap to manufacture. rebates at the time were moderate. couple years and Boeing adjusted list to reflect positioning while rebates went through the roof.:-)

manufacturing cost for the 787 initially went completely beyond any reasonable upper bounds trashing estimates. ( only one entity could ever have been surprised here. if that.)

Even with a high rate initial learning curve cost must still be significantly elevated over day 1 planning.

I would not be surprised if Airbus A350 learning curve sits quite a bit lower than the 787. A snapshot view today is misled by being on different progress points on that curve.

The obvious view is that 737 is / has been profitable for Boeing, but in reality it’s been 25 years of lost opportunities. Consider the relative positions of Boeing vs Airbus back in 1992 regarding 737 vs A320. 737 existed, and should have been poised to keep dominating that sector. However up pops Airbus with what we all know is an excellent product.

Every single A320 sold since introduction is a 737 that Boeing didn’t sell. That’s a whole lot of lost opportunities.

Ideally Boeing would have responded to the A320 with a new design, and made it very difficult for airlines to choose the A320. They didn’t, and Airbus have had a very easy ride for 25 years.

Matthew,

if Boeing would have reacted to A320, you don’t think that would have been a rat race?

Same technology, same physics and same construction & manufacturing processes usually leads to quite similar solutions.

There still would have been a few good arguments fpr Boeing, having etablished support & customer base.

But overall, they had a very good product that sold on the same level as it’s newer competitor.

You need a little bit more then some competition to burn a well selling product, put 10 bn. $ in R&D and built a product that’s just slightly better.

This is not how business and the world works.

The whole point is that had Boeing done a new design to counter the A320 back in the 1990s, there would have been a good chance that Airbus would never have got going in the first place. The market has exploded since 2002, and Airbus took the larger share of that.

Prior to 2002 Boeing had a big market advantage, selling about 1000 more aircraft (737 vs A320) than Airbus between 1988 and 2001. Since about 2002 Airbus have sold approx 450 more A320s than Boeing have 737. In percentage terms Boeing had 24% more market share up to 2002, and from then on Airbus has had 4% more market share than Boeing.

That’s a big swing towards Airbus, at the time the new kids on the block, and it shows no sign of abating.

Had Boeing retained that 24% lead over Airbus since 2002, that equates to nearly 3000 additional aircraft sold. That’s a large number of aircraft for Boeing to have not sold; a new design would have paid off handsomely.

The next few years could be interesting, who’s going to pull the trigger first on an NSA?

AB could get caught in the same situation as BA with the 737, the A320’s selling well, why change? Next thing you see you are to late.

I think Boeing will first because they effectively have little choice, and then Airbus will take stock, see what the Boeing looks likely and then do something a tiny bit better.

Develop, or die. If there is any imaginable improvement, then either one builds it oneself or let the competition build it instead. Going first is risky only if one has an underdeveloped sense of imagination (which in this business equates to the money men trying to force a development to be done on the cheap and also using a hire’n’fire approach to labour cost control, whilst they continue to take profit out of the company. Sounds familiar?).

“Ideally Boeing would have responded to the A320 with a new design,..”

Do you think Boeing would have been able to do a “Super A320” to the same certification base Airbus worked to?

Uwe, yes they could. At least, they had / have the right engineers to be able to do that. Let off the leash they’d at least have been able to equal the A320; just copying it would have been better than keeping the 737.

I think the majority of their difficulties are brought about by company strategy and management.

equal maybe. super ? not.

imu what Boeing managed is to leverage the gift that continued to give after 1945.

I know my remarks may seem marginal, but it seems to me that future partnerships between Bombardier / Airbus and Boeing \ Embraer will boost the 70-150 seat segment. I wrote 70-150 well. So, in the long run, will the expected picture of the single-aisle market change? By analyzing these mergers, we can see that the market for aircraft with 100 seats or less makes the Bombardier / Airbus duo more vulnerable. Is Airbus management ready to live with a smaller portfolio than the Embraer / Boieng couple? Will Airbus leave this segment to Bombardier? If not, how much would a smaller model of the CSeries cost? One or two billion dollars? Will Airbus / Bombardier be tempted to occupy a dominant position in the upcoming renewal of regional aircraft in the United States? Imagine for a moment the addition of a CS75 and a CS90. Will the chart presented by Scott change over the next 10-20 years? What would be the nature of the attractive force of a portfolio including a CS75-CS90-CS100-CS300-CS500 + A320-A321-A322NEO? Rather strong, no? Even before a possible project of an NSA? And again, in this specific context, where will the E2 be housed? Many unknowns, certainly, but such a portrait of the future is alive, dynamic and the recent merger projects between these manufacturers will certainly blur all these predictive maps …

AB is only in on the CS, the only aircraft that is not covered is the E-175E2.

An LGW CS100 with W1519G’s could be offered for airlines that does not need more than ~2500Nm range, this should rival the 175-E2 on seat mile cost?

BBD could re-engine and jazz-up the CRJ700/900’s which should be competitive in their own right.

On the other hand doubt if the 195-E2 could be stretched, an CS500 more than plausible.

I don’t think Boeing really wants to play in that regional space.

Having missed out on buying the program they would want…

And do Turbo props still have a place?

Transworld I love prop aircraft, maybe place for something around 40 seats (Q200-size) still has a place?

See GE has developed a nice new 1900 SHP engine, maybe for something of around 30-40 seats?

…or a niche aircraft such as the Dash 7 with 4 x 1900 SHP engines.

Anton:

I grew up with props, I like them.

Many air pax (US anyway) equate props to dangerous and unreliable.

For that area I am talking about the Q400/ATR area that vies with the small jets.

Alaska Airlines is moving off some routes to the Embraers.

Q400 was flying Anchorage- Fairbanks routes and now they are moving to Embraers I believe (and before it was 737s)

Something about matching the competition, so maybe Delta flies on up to Fairbanks and returns and makes them look bad.

That is a 400 mile route, Ak wanted to save money. Lot of unhappy people used to 737s.

Think the use of the larger props (Q400/ATR72’s) will fade away with time (ATR42 size might remain). Aircraft such as the E175’s will take over most if their rolls. AirBaltic for example is talking about replacing Q400’s with Cs100’s.

STOL and/or dirt strip applications will remain. In many parts of the world there could still be niche applications for 30-45 minute flights which crosses inhospitable terrain.

Off topic but interesting about bringing back the US C47 squadron for D-day celebrations, will be amazing to see.

http://www.aviationpros.com/press_release/12395725/launch-of-d-day-squadron-to-bring-american-c-47s-back-over-beaches-of-normandy-in-epic-flyover-event

https://en.wikipedia.org/wiki/Light_of_Other_Days

We went from 8 track players to cassette players to CD’s. From cars with mostly V8’s to mostly 4 and 6 cylinders. All these and other moves were made because a better product came along that were more efficient, had more public acceptance, and increased operational capabilities.

Props have had their day as did the Lockheed Electra, Convair 440’s,580’s, Dash-8’s, Saab 340’s, etc.

I used to take the PHL-ROA flights quite a bit, most times with the Dash-8. When the CRJ-200 has been put on the route, a night and day difference, faster, quieter, no vibrations, in short, a more comfortable ride.

Piedmont will retire the last Dash-8-300’s on July 4 2018, and it can’t come soon enough for me. Most of the cancellations I experienced in PHL and CLT were the Dash’s.

The next gen RJ’s are selling very well and can fly above bad weather and with their increased speed, can probably add another leg to a days worth of flying. No turning back, electron tube TV’s are gone, as are VCR’s and rotary dial phones.

The prop Engines has a maintenance and cost disadvantage with a gas turbine engine+ Power gearbox+prop electrical controller and pitch mechanism+prop. Only when fuel gets very expensive and there is a merge between the prop and UDF will it return. The day will come and the engines will look like the Safran UDF’s of different sizes reducing fuel burn another 20% with reduction gear and pitch mechanism buried into the Engine and a small cheap nacelle with no thrust reversers. You have the common Engine controller in the TP400M and GE’s “enhanced PT-6”, you have the high Power gearbox in the PW1000G series, the Composite fan blades from the LEAP. The missing link is a cheap and durable pitch mechnism for these powerful engines, don’t know if Safran&co solved it on their demo UDF?

And the LP record?!

Interesting how BBD’s dilemma with the CRJ mirrors Boing’s with the 737. Try continue to update an old design or develop something new.

You right, BBD spend all heir efforts on the CS and let the CRJ’s slip. Maybe they have one chance with putting GTF;s on it but that’s it for current CRJ’s?

I think the GE Passport engines are more likely. They are available now for rear mount and BBD has them on the 7000

Thanks, was not aware of that option. The CRJ’s are real workhorses and deserves another leash of life.

Just had a look see the GE-passport and PW800 fairly similar specs.

They seem however come short on by-pass ratio due to fan diameter limitations on rear mounted engines.

The MRJ’s look good on paper for between 70-100 seats but things seem to be going pear shape there?!

It’s “lease on life”.

The CRJ is a terrible plane to be a passenger on. I hope it is allowed to die. low ceilings, tiny bins, narrow seats. yes, I prefer it to the old EMB/SAAB turboprops, but _every_ other RJ is superior in terms of passenger experience.

Can’t argue about that. About same seat width as 789 and densified 777’s (16.8′-17.2″), at least flights are not >10 hours.

Ridden it many times, between MSO and DEN. There’s a reason the 200’s nicknamed “The Devil’s Chariot”! LOL

At one stage was doing a once a week day trip on CRJ200/700’s. Red eye flight in the morning smooth as can be, evening return feels like driving an 4×4 over rocky terrain with no shocks. Seems those wing not handling turbulence well?

Barbie Jets!

… you mean the CRJ1000?

The CRJ1000 is not in my liking, for that size I will rather go for an LGW CS100. The 190-E2 could turn out to be a very competent and comfortable aircraft.

A re-engined CRJ900 could be good competition for the 175E2?

It occurs to me that when you add up the C sere is deliveries and the back log of A320/21 due to engine issues, Airbus is going to be close to equal with Boeing on deliveries this year.

Good observation! In addition, there is something else that is emerging in terms of delivered units. If Bombardier puts $ 300 million for a new line in Alabama + $ 300 million production line in Mirabel, Quebec, it is $ 600 million worth of investment that must be made profitable by sales. Which sales? Sell what? CS300s to manufacture and sell in the US to counter Boeing’s psychotic reactions. But what else? That’s the question: what will the Alabama workshop manufacture and deliver? Surely not only CS100 and CS300 … Anyone know how many regional aircraft will have to be renewed in the next years in the United States? Can anyone tell us whether or not a wealthy American entrepreneur can start a new regional airline, with CS100, without affiliation with major airlines, to find out whether or not he will have to deal with the “Scope Clauses”?

Delta might be pretty disruptive to the airline market with all those CSeries 100s they’ll be getting.

@sam: exactly, Delta’s CSeries will disrupt many routes – currently served by less comfortable & higher CASM aircrafts.

That pressure should bring in new US CSeries (or E195E2) sales from competing airlines.

Delta has about 166 MD-88/90 in its fleet and another 91 717’s. So lots of room for more orders just there.

The CS100 will most likely end up being a niche aircraft where field performance is important, lower airport taxes on high frequency routes, etc.

The seat mile cost of the CS300 looks significantly less than the CS100 (?) and could see DAL doing conversions sooner than later to the CS300 once the waters has settled?

No one is getting around the scope clauses. Period. This is a “fight to the death” item for U.S. airline unions. As I’ve noted before, as per Comrade Stalin’s Order No. 227: “Not one step back!” is apropos!

The scope clauses benefit the majors too, in that those regionals dont build their own brand and fly in competition with larger aircraft.

Am confused, what would 2 lines in Canada and one in the States provide in terms of capacity for the Cseries? And could that sort of expansion be replicated back through the supply chain in such a short time frame?

Airbus Bombardier should look at placing a new FAL next to Airbus in China as well. Quite alot of structures on the C-series is made in China anyway. Hence Airbus can make the new FAL’s in Mobile and Tianjin flexible to do the A320-series or the C-series depending on demand.

The A320 (actually all Airbus) FALs use quite a lot of (sophisticated) stationary tooling. More like auto manufacture than what I’ve seen around Boeing. Airbus does do “flexible” but IMU a combined FAL line would be beyond.

Probably true, but no sane production manager wants to get there by finishing outfitting 30 or so leftover “gliders” from last year! LOL

Can Airbus catch up with Boeing in widebody deliveries in 5 years? The 787 and A350 could be equal, same with the 747 and A380. But the 767 gives Boeing a dozen more a year. Then there is the A330 and the 777. The 777 has the advantage of having a bigger difference in size from the 787, whereas the A330 is pretty close to the A350, so I think the 777 will see more production.

Ah no .The A330 and A350 are quite different in size, being 8 across and 9 across respectively in economy. The A359 is 10 ft longer and the 35K is 22ft longer, which could mean 40 extra seats for a similar layout in 333/339 comparison, and of course the newer plane is more optimised for very long range.

Most likely not. Having just one FAL in Toulouse limits output. I assume they never tought Boeing would build more than 12/month of the 787 and Airbus would eventually reach similar output with one FAL. Boeing dug themselves into a deeper debt hole than assumed and now when they make Money on each -9/-10 delivery they want to go full throttle on both FAL’s as the market is there for long range direct flights often from a minor hub to a major one.

Airbus will win the Qantus order with the more fuel efficient A350-1000ULR condeming the 777-8X into history before it’s even off the paper.

How can it be dead before it off the paper if it already has 53 orders?

Firm orders for Boeing 777X -8

Etihad Airways 8

Emirates 35

Qatar Airways 10

Totals 53

How big will the Qantas order be?

A bit of history is in order over Qantas long range aircraft.

The ‘short fuselage’ 707-138 to enable some of the longer sectors in its island hopping trans pacific route. No one else bought this version. The 747-SP wasnt built for Qantas routes ( Pan Am and Iran Air) but Qantas bought that too. Wasnt really a success with only 45 built.

The 747-400ER was another Qantas only special long range, but only 6 bought.

Cant see Boeing or Airbus busting their gut on another Qantas special on existing aircraft that will sell a hand full and be exceeded by a new generation anyway.

See Mr. Joyce of Qantas says they need 3 for the Sydney-LHR route, not sure about Brisbane/Melbourne-LHR route. So why all the fuss about ~10 aircraft?

Hope AB opens their eyes, Qantas wants the long ranger by 2022, that coincides with the 778 being available. Think the decision has already been made, AB should rather focus on the 787-10, etc.

Sure AB can do the mega-range it with and A350-950 (3.5m stretch) with the 35K wing, bogies, engines, etc. The same fuselage (~70m) with 359 goodies could compete with the 787-10, then things could make sense?!

Airbus can mix the A350 major parts, like using the A350-1000 wing for the A350-900ULR and also use the Trent XWB-97 with some optional derate. I don’t think RR will have the Advance with ALPS fan certified and ready for delivery by 2022.

That would require final drawing release by X:mas 2018, first metal cut 2019 and an instrumentetd prototype ready for test by X:mas 2019, FETT 2020, compliance Engines testing 2021 and certification 2022. It sounds they are appox 3 years behind this schedule.

Thanks, is this the XWB-EP or is it something else?

Still believe that an 350-“950” (70m, +3.5m) fuselage could give AB a magnitude of options which they can apply components depending on airlines demand of the time.

From a 6000Nm range aircraft with 79Klb engines to a 9000+Nm aircraft with 97Klb engines.

It’s for prestige and technological superiority, if nothing else.

Think Bugatti Veyron or Chiron: these cost untold millions to develop, will never turn one Euro in profit despite their stratospheric MSRPs, but are hugely important to VW Group and are considered kings amongst hypercars.

Understand that, but seems AB is vulnerable in picking up this type of bait.

If there are technology spin-offs its good. But if I read things correctly Qantas will most likely go for the 777-9 as 747 (A380’s) replacement, 777-8 for mega-range. They effectively replacing 330’s with 789’s.

Maybe AB wants to stay in the Qantas light to sell 321’s? Doubt if they will be interested in an A380NEO.

Judging from QF’s outstanding 789 firm orders + options, you might be right on the A330 replacement tack – I always pictured QF using their 789s both as a “backfill” to their 4-holers (ie. add frequencies to routes already served by their 388 and 744 that cannot economically support another 400+ seats, like SYD-LAX/SFO) and to open up routes that don’t make sense for said 4-holers (ie. SYD-YVR is served seasonally with a 744 – I would personally LOVE to see that route go year-round with a 789 during the off-peak months, and would be profitable doing so.) I can definitely see QF retire their oldest A330-family international-configured frames and keep a subfleet for their domestic trunk routes (SYD/MEL/BNE/PER.)

QF’s 388s are average 8 years old, so still very young and will not require replacement for many years. They still have 8 outstanding orders they have no interest in taking up – it’s very possible this order is converted to A350-family frames if AB meets their ultra-long-haul challenge.

It’s possible QF orders A321neo/LRs for new long-and-thin routes, but given their geographical restrictions (their major urban centres are in the southeast of Australia!) those routes are likely better covered by their widebodies.

Still, the 777X family is a tough sell for QF. It gets ordered iff BA meets the ultra-long-haul challenge and/or QF decides the 789 isn’t large enough AND the 388 is too big. Tough niche for them.

Personally I think the 350-1000 could serve QF well. They are generally sophisticated travelers and flights long. A relatively large premium economy (2-4-2) section could be accommodated.

Range of an 35K with a high comfort level layout (300-320 pax?) and ~310-315T MTOW could have a very interesting range.

I agree that the HGW A350-1000 in ULR configuration could be the better choice than the 777-8. It was perhaps the secret surprise weapon Airbus had. It’s already at 8100 nm range with more passengers. With reduced a passenger load to to get to the range required by Qantas, it may turn out to be the lightest, more economical choice. However, Qantas invested in the 787 so may stick with Boeing.

Some interesting detail in the TA figures.

7double7 Classics — wonder what price they got for them?

Everything points to BA selling build slots on the old line at knockdown prices.

AB could have played the same game with the A330CEOs.

Although it might be that these are the only AB TA’s that can be had without RR engines.

Or the NEO programme is running late and they now have extra slots to sell.

One thing that must change is the HD / LR vibe that seems to come with all modern TA aircraft.

SA OEW is in the region of 40T – 50T plus at the moment.

TA OEW starts at 125T and quickly heads north.

The B767 is the only outlier in production although there is a large history of MD / MR TA from AB.

Consequently gap in the market.

However it is a gap that the market does not want to fill.

The range gap is around 2,500 NM.

Consequently hard to miss.

UA got their 77Ws cheap enough to completely upend their fleet plans (early retirement of their 744s + downgauge their 35K orders to 359s.) Plus a good number of earlier 777-family frames are nearing early-retirement age for the Asian/ME carriers that prefer to keep their fleets fresh. This can’t help resale values.

As for the MOM, I can’t help but get the feeling the only reason BA has taken this long to commit is the cost of development vs being able to sell enough frames to make that development cost back. It must be a very borderline business case.

(Off note: I keep reading BA = British Airways and AB = Air Berlin whenever I read the comments here!)

True about the Ab/BA thing.

Think Boeing’s decision on the MoM is if it is going to be a large NSA or small twin aisle. Basically 757 vs 767, and what Airbus response will be.

phoenix: You might note that Boeing has never been able to get enough feed stock of the older 777 to get a pax to F program going.

FedEx was hilly involved but Singapore elected to keep their 777s (200s) for Scoot and that went away.

At some point they get too used to be worth converting.

Ergo, Boeing has done nicely with the 777F.

Transworld you seem interested in freighters, my knowledge of these are Zip. As far as I can make out the 777F is based on the 777-200LR.

At what point is ex pax 773ER’s going to be converted to Freighters, or won’t it happen?…or even build “primary” freighters based on the 773?

As usual, Boeing isnt making the existing 777F on an -300ER airframe so it wont cut into the bigger 747F market.

The fuel prices mean even the early -300ERs at 15 yrs old are still doing well carrying passengers.

Only because airlines are now flying the 773ER at 10 abreast. Its economics at 9 abreast is marginal?

@Anton:

“..airlines are now flying the 773ER at 10 abreast. Its economics at 9 abreast is marginal?”

Relative to what? Surely can’t be against a 346 @ 8abreast which is fm the same tech era and with a similar usable cabin floor area+payload/range.

In any case, it’s hard to argue against this:

77W @ 9abreast has more than fulfilled its original mission in its specific mkt segment for Boeing during its prime(i.e. peak of the product life cycle). New built 77W @ 10abreast config continues to sell today is just gravy/dessert for Boeing……which is a particularly interesting contrast against the lack of sales for the 35K. 3 likely possibilities:

1. Current 77W pricing is much more friendly than 35K(I suspect may be even cheaper than a 359/78J)?

I don’t doubt this for 1 second and UA is likely an excellent example(I vividly recall about 10yrs ago, UA declared 77W as obsolete tech relative to the 350 they were ordering back then).

2. 77W has much much better/faster availability than 35K?

If U firm an order today, U can likely take delivery of a 77W nex yr but can only take delivery of a 35K earliest in 2022….if U hv good friends @ Airbus.

3. Op econ of a 77W @ 10abreast may not be too far worse than a 35K @ 9abreast?

This is akin to for upto medium range mission requirements, 333 continues to sell despite the 789.

Some good points there, but if you buy a new 77W now you stuck with if for 15-20 years happily sipping fuel. Also seems the 2nd hand value not the greatest.

If the fuel prices goes up 25% in the next 5 years those operating 77W’s will have a distinct disadvantage compared to those operating more efficient aircraft.

Maybe there is not much on paper difference between a densified 777 and 350, but flying in them are very very different.

The fate off the 330NEO’s could to a large extent depend on the T7000’s performance and reliability. If it proves better than the RR TEN and GEnx it could become a fair seller, some of these facts should start to surface during 2018.

If above average positive may even tempt AB to consider an A330-1000 to compete with the 78J.

We can hope they both are better than the Trent 1000!

The engine alliances for me is interesting on the widebodies. GE-Boeing, RR-Airbus.

P&W is wedging its way into the single aisles, especially the smaller RJ’s.

What aircraft size is the RR UF really targeting and what engines/suppliers to power the NMA and future NSA. Surely work must be in advance stages as engines are very long lead time animals?

I don’t know RR has targeted an engine. Notionally it was A380, but that looks like nebulous at best. What Emirates chooses for the last batch of them will tell us something for sure.

I think they went up to 100k thrust or a bit more so they had one as large as you would need and scale it down. Not sure how well that works how far down the thrust ladder.

Right now the only new engine is the NMA if that comes to be. 50k or so.

Can RR afford to even go for that. They have all those new engines and the modified ones and no ROI.

Thats what I am trying to get to, RR seems to focus on larger fanned engines as is GE if the CFM is not included. P&W got their hands full sorting out the smaller fanned GTF’s which could have spin-offs down the line with an NSA.

Their is a definite need for new engines between 40 and 60KLb which probably reflects the MoM gap and the demise of “classic” 4 engine aircraft.

Interesting reading on the realities re: CS sales during the AB/CS deal transition from BBD management.

http://c.newsnow.co.uk/A/922995724?-303:3665

“CS sales pause until Airbus transition…” (even after the USITC decision)

That illustrates very well the additional boost the CSeries will get, once Airbus gets on-board.

Airbus now talking about going to over 60 A320s pero month:

https://www.bloomberg.com/amp/news/articles/2018-02-05/vistara-8-5-billion-jet-order-said-to-pit-airbus-against-boeing

Per month, for the English teachers amongst us. I write in 3 languages on this phone and the spelling checker goes crazy.

which is obvious. 8 FAL lines with a capacity of 8 each max. := 64

Better switch of your spell checker. Better to make your own errors than getting russian roulette sniped by your spell checker.

My written Spanish isn’t so good, it needs all the help it can get.

I read in the Seattle’s Business Journal that the B737-Max7 which just was rolled out, has a 18% fuel savings over the B737-700. If that’s the case, shouldn’t this model of the B737 Max have a decent run? Or are they playing loose with the numbers? Or is the CSeries 300 that much more efficient than even this? TIA The Max 7 had a list price of 96m!

Well if its fuel savings per passenger with an extra 12 seats, it will be a good plane. But airlines need to think to residual values as well, and it will be a bit of an orphan in 20 years

According to Boeing (and they should know)the max7 has no chance now that the ITC has ruled against it. Its even worse than that,the future of the company itself is threatened.

which is self afflicted, isn’t it?

Mirages do have limited lifetime.

There is also a bit of pricing negotiation in having this plane so close in size to the A320. Its then offered at a pricing point to be competitive with Airbus offering and then when they say the Max 8 suits us better , this can be priced ‘higher’ than the A320 -as its a more competitive plane in many respects.

Theres lots a marketing reasons why customers buy the mid priced offering , even when its a sophisticated purchase like an airliner

Haters gonna hate.

“Haters gonna hate” for Grubby and Uwe.

Straight from the horses mouth.The story does change a bit though,just before the judgement (which I think everyone expected them to win)it was about 2000.Today Randy has said that he expects about 10% of MAX sales to be MAX/7.

SSJ shrink,is this not a woefully bad idea?

I assume Russian gov. will force airlines to take it in preferance to E-jets or CRJs. Might be some short field Russian conditions involved as well? I doubt if they are aiming this at the export market.

Bit of NIH ?

More the Russians are more than iffy with sold equipment.

Full support and backup is critical. Its not been taken to heart as they are still struggling to transitions.

When theft hint at a new engine that means it did not go well with the combo one they came out with.

If you sell aircraft all over the world you need good solid customer oriented service.

When its a government owned/controlled entity that is not going to happen.

Super Jet is going to get stomped by the C series everywhere but Russia.

They will tilt the deck to favor it and even that has not worked for the bigger jets.

Report somewhere recently that Interjet have 4? SSJs grounded due to shortage of spares.

What is estimated ranges of the 311 and 316 t0nne A350-1000’s ?

That would require a subscription and a search of recent 350-1000 articles.

Think only AB really knows at this stage?

Published fuel capacity of the 359ULR (280T) is 165KL, that of the 35K (316T) 159KL.

To get to the magic QF 10KNm range with full pax you could go 359 + 35K wing and bogies, 4 x LD3 Aux tanks (16Kl) MTW of 300T with derated to 90Klb XWB97’s.

Not sure if this will have enough pax and cargo capacity for QF?

For an 35K to get to the desired range you will probably need to increase the fuel capacity with 25T (MTOW 340T). The wing and bogies could potentially handle it but thrust requirement will be around 105T?

AB have been studying an 35K stretch, they will have data to know what is required in terms of wing, landing gear, engines to increase MTOW to a postulated 330-340T.

Just find the best means to store sufficient fuel without compromising to much cargo capacity.

Although AB is well ahead of Boeing with the larger single aisles maybe it should be a priority to update/improve the 321’s wing, such as with A380+ type winglets, etc. Introducing this with the 2nd generation GTF’s will make the 321/(LR) even more competitive.

The 322 (+20-25 pax) is becoming more uncertain in my mind. Or it must have a totally new wing for 4500-5000Nm range (not sure about sales volumes and high cost). Rather look at ways getting the 321LR’s range to ~4200Nm with more pax and MTOW to 100T (35Klb engines)?

…or the 322 must use the relatively low cost 321 wing updates and be optmized for shorter haul (~2500/800Nm) high density “domestic” routes. MTOW to stay around the current 321LR’s 97T but with 35Klb engine for additional wetted area/drag, OEW, and also 2 exit doors in front of wing.

First images of A330-800, looks good. Will write to Santa, I want one.

http://c.newsnow.co.uk/A/923147306?-303:3665

Another few interesting comments by BBD at Singapore. One is they wont re-engine CRJ’s, must tell something?

http://c.newsnow.co.uk/A/923150434?-303:3665:3

Looks like GE not going GTF for NMA.

https://www.flightglobal.com/news/articles/singapore-cfm-to-stick-with-direct-drive-architect-445532/

To Readers looking for an Edit option for your comments, IT tells me a Plugin has been installed. Someone want to test it out? It functions for about five minutes after you post, apparently.

Thanks Scott, this will be very helpful, especially well after dawn, and English being my 3rd language.

This is a test. This is a teste. Boeing is a good company. Boeing is a goode company. All they need is a new single aisle airplane. All they need is a new singlee aisle airplane. Scott, looks to me before the post to spellcheck good and single – hope this helps on the basic spellcheck function.

Yes, what came up was my comment in a box with a timer on allowing me to clean-up my paragraph (which I did not use for testing sake).

Huge gripe on the industry — BA for building them and the airlines for kitting them out.

B7double7 NG @ 10 abreast = 17.2” wide seats.

Interesting that the classic model @ 10 x 16.8” seats was seen as too narrow.

B787 @ 9 x 17.? = waste of a great aeroplane.

Why is the industry just so low rent?

All for the sake of 15 to 20 seats on a 3/4 class layout.

I always worn an Boeing cap but the 787 at 3-3-3 changed my mind.

Its all about squeezing in more pax so that the can claim a few percent better seat mile cost in their marketing.

The guys making the decisions are not flying at the back, they just want to tell the shareholders about how their “game changing” sardine cans will make money for them. Bur it can backfire.

You make a wider plane, airlines will stuff in more seats and have a tighter seat pitch, OEM’s make the planes and airlines use medieval seating configurations. They don’t CARE about the passenger, plain and simple.

When customers feel fu*ed which ever way they go

they go for the cheapest.

All for the sake of staying solvent

RR and their all singing, all dancing UF tech.

Some of their comments point to a very specific intro date.

For a newbie like me I am intrigued to understand what the airframe project could be.

Then there is RR and their half finished product catalogue.

And then there is the huge whitespace that is MoM and its lack of an up to date engine.

Current SA with growth = 2 x 40K lbs thrust for 110/120T MTOW.

Enough real estate for 240 LH economy seats out to 4,500 NM

New “Fat Bloke” SA with 156” cabin width = 2 x 50K lbs for 150T .

Enough real estate for 300 plus LH economy seats out to 5,000 plus NM.

New MD TA / B767 NG = 2 x 60K lbs for 180T.

Range would probably extend out to 6,000 NM.

Not sure how RR would cover this gap.

Base engine at 50K lbs thrust and flex 20% in both directions?

However their place in the value chain would be paramount — single engine going on more than one airframe.

They have the advantage of focus.

GE and PW have existing product families to protect.

RR can go all in with nothing to lose.

Points to 35K – 45K lbs thrust initial offering.

B797 MoM turns up in 2027 for the second UF family.

UF on a A32X architecture would probably mean a new saddle / wingbox and an A330 sized undercarriage. Length not strength.

Sichuan orders 10 A359’s.

http://c.newsnow.co.uk/A/923557974?-303:3665

Did Airbus delay some orders to give Boeing its year of fame?

🙂

…or airlines bosses eyes are starting to open? Passengers negative responses to the 787 is starting to build up.

Or Arline’s are choosing aircraft based on what they think fits?

787 has been out there for a while with all the complaints well heard.

Regarding QF they have left the 1st of their 15 options for 789 lapse. Coincidentally AB will be touring Australia with a roadshow of the 35K shortly.

Project Sunrise if the OEM can meet the requirements will be very niche. The unknown here is what affect will operational changes have on the overall passenger experience on board these ultra long flights.

Even SQ when previously flying to Newark had a premium config with J class, a Y class pitch closer to PE and the Coffin closet.

Recent reports indicate QF PER-LHR nonstop is not selling at a premium, will Y class passengers really prefer a 789 3-3-3 against an A380 to save 3 hours on PER-LHR?

My only experience on 789 was on a 5 hr flight which was bearable. The large windows certainly are a nice touch, but one thing that struck me is how loud the engine noise is in the cabin for a latest design aircraft.

Im glad QF are trying something new, but the armchair Airline CEO in me can’t see what the earnings accretive advantages are for this route other than bragging rights “We woz the first to do it!”

I don’t read it as dropping all 15, one that was coming up.

http://australianaviation.com.au/2018/02/qantas-to-let-first-787-option-lapse/

It seems pretty murky reasoning as they do have experience with the 787-8s as well as a plethora of other airlines operating experience.

Qantas has been an enigma for some time in their decisions processes (or lack of). Ben Sandilands was pretty scathing of them.

Giving Emirates the routes they did was deeply puzzling.

It never looked like they had a real fleet replacement update plan, more knee jerk.

The NMA if it happens will surely change a few things. More and more voices are indicating the planing and de-planing time importance for such an aircraft. AB obviously looking at the 322 and this aspect could be its short coming vs a twin aisle, especially with the Boeing marketing machine.

An A332-NMA with new center section, wingbox, new wing (CAT-D) and 55-60Klb engines with 5000-5500Nm range might just find a market between the 797 and 787. Applying these to the 333 will give it a range of 4000-4500Nm and could be what airlines need for high density short-medium haul routes. But the perception of an old design will remain.

First price will be a new aircraft with 250 seats, 5500Nm range, 55Klb engines?

Also way to costly and too heavy.

What is the latest betting on the MoM / B797?

Vanguard style double bubble?

Warmed over B767 NG with snazzy marketing?

New wider SA fuselage with B757 sizing?

How much floor area?

What range / payload?

What level of OEW?

And their is the powertrain?

Chances of existing 4x25K lbs vs brand new 2x50K lbs?

For the record my thoughts are BA will go with a warmed over B767 and snazzy marketing.

Very shareholder friendly.

The latest PWG engine snag not going to help 320/1 deliveries.

http://c.newsnow.co.uk/A/923682817?-303:3665

That is getting to be a serious safety issue.

It looks like in the rush to implement a fix, they shot themselves in the saf4etyt foot and created a safety issue vs an annoying maint issue.

Oblivious its not tolerable to have a known issue shutting engines down.

Safest would be to remove all engines with that fix. Remove the fix if possible and only then resume ops.

P&W has gone from a black eye to serious questions

Some serious decisions need to to be made, like even stopping PWG deliveries for 3 or 6 months?

Times when seat mile cost doesn’t matter, A380 lands at Stewart airport due to to JFK closure.

http://c.newsnow.co.uk/A/923763004?-303:3665:3