Leeham News and Analysis

There's more to real news than a news release.

COMAC struggled in 2025; 2026 won’t be much better

Subscription Required

By Scott Hamilton

Jan. 15, 2026, © Leeham News: COMAC had a rough year in 2025. It’s unlikely that this year will be much better.

Jan. 15, 2026, © Leeham News: COMAC had a rough year in 2025. It’s unlikely that this year will be much better.

COMAC is China’s state-owned commercial aerospace company. It builds the C909 regional jet (formerly known as the AVIC ARJ21; AVIC is now part of COMAC). The C909 is a Douglas DC-9-10 look-alike with GE CF-34 engines, the same powerplant that’s on the Mitsubishi CRJ and Embraer E1 E-Jets.

The C909 is not a particularly commercially competitive airplane to the CRJ or E1, but that wasn’t the point of the aircraft. The C909 is China’s truly first effort to establish a commercial jet airliner industry after a false start decades ago with the Y-10, a Boeing 707 clone. China developed turboprop airliners with limited success.

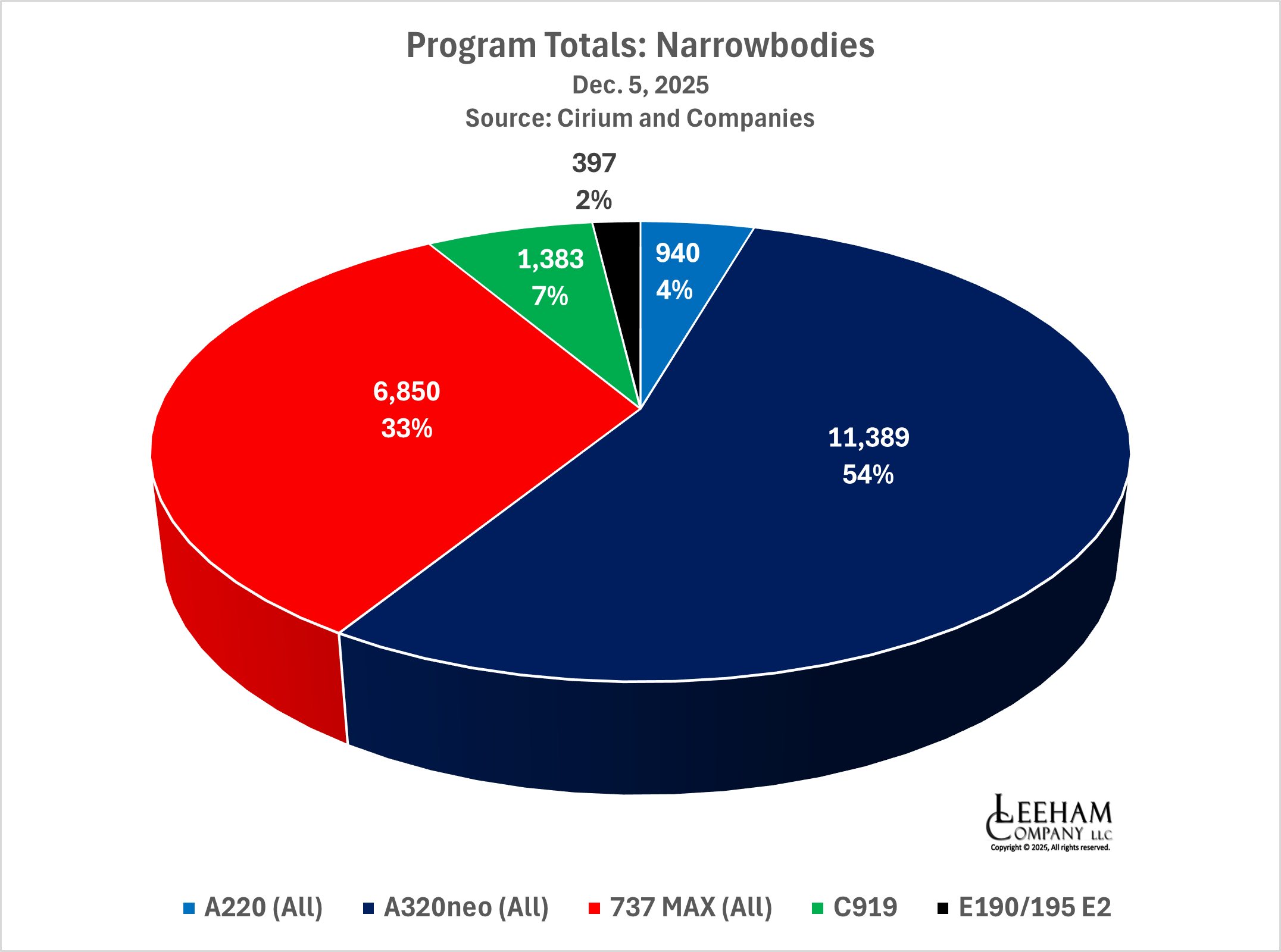

COMAC also builds the C919 mainline jet. The C919 is a competitor with the Airbus A320neo and Boeing 737-8. This jet is China’s next step in developing a commercial airliner industry. More than 1,000 orders have been placed. All but a handful are orders dictated by the central government to China’s airlines and lessors.

Nevertheless, an analysis of the backlog of the 125-240 seat single aisle sector gives the C919 about a 7% share. With China evolving eventually into the single largest global market, this captive market share is evolving into a force to be reckoned with.

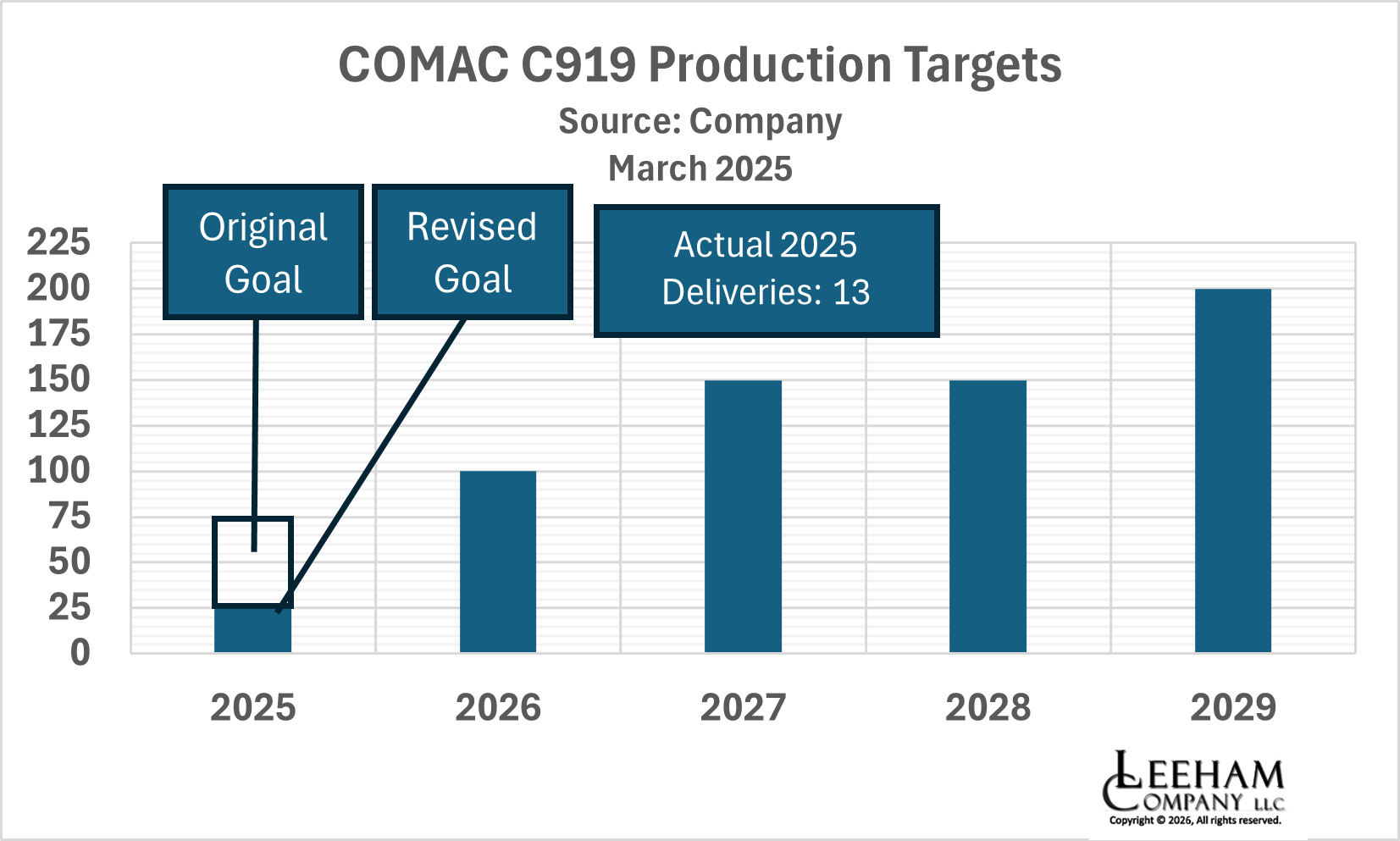

COMAC hoped to deliver 75 C919s last year. Hurt by Western sanctions for China’s support of Russia in the Ukraine War and by trade sanctions imposed by the Trump and Biden administrations, COMAC reduced the delivery forecast to 25. In reality, C919 deliveries last year fell to about 13, the same as in 2024. COMAC outlined its production goals in March; they are unrealistic.

Spirit Aero problems affected A350 deliveries

By the Leeham News Team

Christian Scherer, the former CEO of Airbus Commercial Aircraft. Credit: Leeham News.

Jan. 13, 2026, © Leeham News: Deliveries for the Airbus A350 fell last year compared with 2024, reflecting supply chain challenges.

Christian Scherer, the former CEO of Airbus Commercial Aircraft, said, “The ‘stagnation’ of A350 deliveries is not a lack of demand. There is a center section of the A350 fuselage that is being built by a company formerly known as Spirit Aerosystems. They ran into trouble. They were the pacing item.”

Airbus acquired Spirit’s Airbus business when the company merged with Boeing in December. “Now that we have regained, let’s say, control of that particular center fuselage piece on section 15 of the A350, you will see the A350 continue its ramp up,” Scherer said during the annual Airbus media briefing of its annual orders and deliveries results.

Dissecting the results reveals:

Airbus meets revised delivery target in 2025, touts sales performance for A350

By Scott Hamilton

Jan. 12, 2026, © Leeham News: Airbus confirmed today that it delivered 793 jetliners last year. This was on a target revised downward from 820 guided at the beginning of the year.

A late 2025 quality issue involving fuselage panels on the A320 resulted in a reduced target.

Christian Scherer, who relinquished his position as CEO of Airbus Commercial Aircraft, responds to a question during his final press conference today wearing that hat. Credit: Leeham News.

Officials also said that the number of engineless A320 “gliders” was reduced from a peak of 60 last year to a “manageable” small number. Despite continued supply-chain difficulties for interiors, Christian Scherer said that there aren’t any widebody airplanes parked awaiting components.

Scherer officially relinquished his title as CEO of Airbus Commercial Aircraft on Dec. 31. This was his last press conference in that role. He remains with Airbus for the next six months in a transition role with his successor, Lars Wagner.

Scherer and Benoit de Saint-Exupéry, EVP Sales Commercial Aircraft, said sales of the flagship, top-of-the-line aircraft, the A350, are gaining momentum. Orders were signed for 193 A350s last year. A Memorandum of Understanding from Air Europa, which will be finalized this year, is intended to replace aging Boeing 787s.

“I want to particularly highlight the Air Europa order for 20 A350-900s,” said Saint-Exupéry. “With this move, Air Europa recognizes the A350 platform as the right tool for the next chapter of growth, including the superior economics and performance of our technology to replace their existing 787 fleet.

“As we are reaching the first wave of replacements of the early 787 fleets, we are confident that other airlines will reach the same conclusion as Air Europa with the A350-900, but also that of many other airlines which have already decided to replace their 777 fleet with the A350-1000,” he said.

However, Boeing had a banner year for 787 sales, too.

Airbus adds emphasis for A220 to regional airlines; adding high-density version

Subscription Required

By Scott Hamilton

Jan. 6, 2026, © Leeham News: Airbus is tweaking the marketing messaging for the A220 to boost sales for regional airline operations.

Marketing for the A220 began as the C Series when Bombardier launched the program in 2008. Bombardier positioned the 100-seat CS100 as a replacement for the Airbus A318 and Boeing 737-500/600. The 130-seat CS300 was designed to replace the Airbus A319 and Boeing 737-700. The Airbus and Boeing airplanes are considered mainline aircraft as opposed to regional airliners.

The A220-100 is a “necessary” part of the family, Airbus says. Credit: Airbus.

Bombardier also design a larger CS500, but didn’t launch the program. The CS500 would be a direct competitor to the A320 and 737-800/8.

Airbus continued this marketing approach when it agreed to purchase control of the C Series program in 2017, renaming it the A220-100 and A220-300. Airbus says it’s a matter of when, not if, it will proceed with the A220-500.

However, at an event hosted by the European Regional Airlines Association, Airbus told regional carriers the A220 is a choice airplane for them if they have ambitions to spread their wings, so to speak.

Benjamin Peiron, VP Single Aisle Marketing for Airbus, told LNA in an interview last month that this message didn’t represent a shift in marketing strategy. “It’s more focused, I would say. If we look at the operator base of A220, it’s about half composed of legacy carriers, [like] Air France, Delta, Air Canada. About one third is from so-called regional airlines, whatever the exact definition is. The rest is hybrid low-cost or equivalent.”

Airbus gets new CEO for Commercial Aircraft; faces supply chain issues, decisions on A220 Stretch, Open Fan engine

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Jan. 5, 2026, © Leeham News: The big news at Airbus at the start of this year is the new president and chief executive officer for Airbus Commercial Aircraft: Lars Wagner.

Wagner succeeds an Airbus lifer, Christian Scherer, who retired from his position on Dec. 31. He remains with Airbus for another six months in a transition capacity. Wagner joined Airbus in November to begin a transition period. He previously was the CEO of MTU Aero Engines AG. He joined MTU from Airbus in 2015, holding various positions until he was recruited by Airbus to succeed Scherer.

Lars Wagner took over as CEO of Airbus Commercial Aircraft on Jan. 1. Credit: Airbus.

Immediate challenges facing Wagner include stubborn supply chain issues as Airbus seeks to ramp up production of the A320 family to 75/mo by 2027; the A220 family to 12/mo this year, the A350 to 12/mo by 2028, and 5/mo A330 by 2029.

Airbus’ supply chain—as with Boeing, Embraer, the engine makers, and the suppliers within their own chain—remains stressed for a variety of reasons.

In fact, quality control issues on A320 fuselage panels that became public on Dec. 1 illustrate just one of the many challenges the 50-year-old Wagner faces. Those problems, and others, prevented Airbus from meeting its delivery target of 823 aircraft for 2025.

Two other major issues facing Wagner, but in the coming near-term years, are whether to stretch the A220-300 into an aircraft the size of the A320neo; and whether to select the GE/Safran CFM International RISE Open Fan engine for the A320 replacement in the coming decade.

Group CEO Guillaume Faury said during the Paris Air Show last year an engine decision will be made by 2027 or 2028, and a program launch will be in 2030. A RISE demonstrator engine is to be mounted on an A380 next year to begin flight testing.

Scherer was the leading proponent of both projects, arguing that a market leader should not wait for the competition to move but rather jump them to stay the leader.

Boeing captures 33% of single-aisle sector, maintains big lead for wide-bodies

Subscription Required

By Scott Hamilton

Jan. 2, 2026, © Leeham News: Boeing’s 2011 decision to launch another derivative of the 737, a slow response to the Airbus A321neo, and the series of crises involving the 737 MAX beginning on March 10, 2019, caused a dramatic drop in market share that places Boeing at a distant No. 2 to Airbus.

The total program orders give Airbus a 54% share of the market for the A320neo family to Boeing’s 33% for the MAX. Adding the A220 into Airbus’ share, the European company has captured 58% of the single aisle market, an analysis of data from the companies as of Dec. 5 reveals.

China’s COMAC C919 captures 7% of the single-aisle market, according to data analyzed from Cirium and other sources. Embraer, with its two-class 100-seat E190-E2 and 120-seat E195-E2, captures a mere 2% of the 100-240 seat sector.

Russia’s Sukhoi MC-21 is not included in this analysis because the market is closed to Airbus, Boeing, and Embraer due to international sanctions on Russia due to the Ukraine war.

“Rise and Fall of Boeing and the Way Back” picked by Royal Aeronautical Society as a top book for Christmas

By Scott Hamilton

My book, “The Rise and Fall of Boeing and the Way Back”, has been named as one of its top picks of aviation books by the Royal Aeronautical Society for Christmas 2025.

My book, “The Rise and Fall of Boeing and the Way Back”, has been named as one of its top picks of aviation books by the Royal Aeronautical Society for Christmas 2025.

“Following on from his previous Air Wars, which looked at Airbus vs Boeing rivalry, aviation journalist and analyst Scott Hamilton brings commercial aerospace up to date with a look at the rollercoaster ride that has been Boeing’s fortunes over recent years. How did a brand that personified American engineering excellence become so distrusted by customers, politicians, and even the general public? And more important – what are the ways back from this?” The RAS wrote.

This is the second time one of my books has been so named. (I’ve only written two books.) The first, “Air Wars, the Global Combat Between Airbus and Boeing”, was chosen when it was published in 2021.

“Rise and Fall” continues the story begun with “Air Wars.”

“Rise and Fall” may be purchased here.

“Air Wars” may be purchased here.

Mitigating mounting pressures in the global supply chain

Subscription Required

By Charlotte Bailey

Michael Haidinger, president of Boeing Germany. Credit: Leeham News, Charlotte Bailey.

Dec. 22, 2025, © Leeham News, Hamburg: “In today’s aerospace environment, which is marked by workforce challenges, evolving technologies, geopolitical risk, financial pressures, and industry consolidation, our supply chain deserves not just attention but requires true partnership,” says Dr. Michael Haidinger, president of Boeing Germany, Central and Eastern Europe.

“Over the last few years, [the global supply chain] has carried a tremendous load.”

Speaking at December 2025’s Aviation Forum in Hamburg, Haidinger acknowledged that the pressures present throughout a complex ecosystem continue to evolve. Recognizing that “integrating stability across the aerospace value chain is essentially the foundation of our long-term success,” the industry is nevertheless having to place renewed focus on inflationary pressures and geopolitical uncertainty as it looks to bolster its ongoing resilience.

For Boeing, this includes “working more transparently than ever with [its] suppliers” through a monthly supplier brief, sharing details of production plans, key performance indicators, and any changes that could impact planned production. “Transparency builds trust, and trust brings alignment,” he urged.

Supply chain continues to bedevil Airbus, Boeing

Subscription Required

By Scott Hamilton

Dec. 8, 2025, © Leeham News: Supply chain difficulties continue to bedevil Airbus and Boeing deliveries this year.

Embraer also has had some impact from supply chain disruptions, but at a much lower rate.

November deliveries by Airbus and Boeing are lower than in September and October. Boeing delivered 53 and 55 aircraft, respectively—but only 42 in November.

Airbus and Boeing are struggling to meet production goals because the supply chain still can’t delivery parts and engines on time. In some cases, quality also is a factor. Photo Credit: Airbus.

Airbus delivered 78 aircraft in October and 73 in September. Defective panels delivered by a supplier, which Airbus did not identify, for the A320 family were discovered, impacting total November deliveries (72) and anticipated December deliveries. Airbus now expects to deliver 790 aircraft this year compared with its original guidance of 823. Airbus delivered 84 aircraft in November last year. Airbus needs to deliver 133 aircraft this month to meet its revised, lower goal.

In addition, delays in receiving interiors, mainly from Collins and Safran but also from others, caused Airbus and Boeing to delay widebody deliveries. Continuing shortages of engines from Pratt & Whitney and CFM (GE and Safran) for the GTF and LEAP impacted Airbus, Boeing and Embraer. PW continues to divert new production GTFs to AOG (Aircraft on Ground) A220s, A320s and E-Jets. A strike at GE interrupted CFM LEAP deliveries.

Airbus and Boeing want to increase production rates next year and in following years. The supply chain is the driving factor.

Aerospace analyst Ken Herbert from RBC Capital Markets raises some caution from the supply chain in his survey for the second half of 2025. In a report issued on Dec. 4, Herbert wrote, “Just when confidence in the aerospace OE outlook appears to have inflected, we get a reminder from Airbus (ELAC software, metal fuselage panel quality escape) that the industry is still dependent on a relatively fragile supply chain, and we believe the supply chain will remain part of the A&D narrative for the foreseeable future.”

Airbus rolls out prototype A350F in march toward 2026 certification

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Dec. 1, 2025, © Leeham News: Airbus rolled its first A350F out of the factory last week. It now moves to another building for the installation of systems and engines. The first flight is planned for the third quarter next year, as a second freighter is completed to begin regimented flight testing.

Airbus hopes to deliver the first freighter in the second half of 2027.

Figure 1. The first Airbus A350F rolled out of the factory this month. Source: Airbus.

Boeing’s new freighter, the 777-8F, is still a “paper” airplane. With 59 orders from six customers, entry into service (EIS) is now estimated for 2029 (some say 2030). Airbus has more than 80 orders from 13 customers. Airbus claims a 58% market share of new freighter orders.

A350F sales fall short of the 120 sales for new-build A300-600Fs, Airbus’ best-selling freighter, most of which went to package operators FedEx and UPS. However, neither has chosen between the A350F or the 777-8F for their next airplanes to replace the decades-old Boeing (McDonnell Douglas) MD-11Fs. The future of these aircraft is uncertain following the Nov. 4 crash of a UPS jet in Louisville (KY).

Within days of the accident, which killed three pilots and 11 people on the ground, Boeing recommended grounding the nearly 60 MD-11 freighters on the US registry for inspections. The Federal Aviation Administration (FAA) made the grounding mandatory shortly after.

Related Stories

- UPS crash presents potential opportunities for Airbus’ A350F

- Airbus sticks to 2027 EIS for A350F (Briefing pre-Dubai Air Show)