Leeham News and Analysis

There's more to real news than a news release.

Rolls-Royce plans for new single-aisle, twin-aisle airplane engines

Rolls-Royce may not be at a cross road but it’s certainly at a fork in the road.

RR sought to be a dual-source supplier for the Boeing 777X, competing with GE Aviation for the privilege; it was generally a given that GE would be a provider. The question was whether it would be the sole supplier or share the platform with another. Pratt & Whitney withdrew, concluding the business case wasn’t there for its proposed big Geared Turbo Fan. RR stayed in the competition, assured by Boeing that it wasn’t a stalking horse to GE.

But GE won the position as exclusive supplier, much to RR’s consternation.

Next, the future of the Airbus A350-800, powered exclusively by RR, is in serious doubt. The backlog is now down to a mere 46 as customer after customer, encouraged by Airbus, up-gauged to the A350-900 and -1000 sub-types. While RR is also the exclusive supplier on each of these models, and the engines are largely common, there has been substantial investment by Rolls on the -800’s application. If the -800 is canceled (as many industry observers believe it will be), RR’s investment is largely down the drain. How does Airbus “make good” to RR for this?

There is the prospect of choosing RR to be the sole supplier on the prospective A330neo. While a re-engined A330 is envisioned with an entry-into-service of 2018 and therefore only the GEnx and the Trent 1000 TEN are the feasible options, selecting the Trent would compensate RR for a canceled A350-800.

Exclusively selecting RR to power an A380neo, with an EIS of around 2020 or somewhat later, could also accomplish this. The engine OEMs believe the potential market for an A380neo is 300-400. This means 1,200-1,600 engines plus spares, parts and Maintenance, Repair and Overhaul contracts. Today’s A380 shares the power between the RR Trent 900 and the Engine Alliance GP7200; Airbus forecast 650 sales of today’s A380, according to a lawsuit between RR and PW a few years ago. Engine Alliance, a joint venture of PW and GE, dominates the market share thanks to Emirates Airlines selecting the GP7200 to power 90 A380s. But Emirates’ recent order for 50 more left the engine selection open, and its president wants future engines to provide a 10% reduction in fuel burn. The timing of many of the deliveries means the current generation of engines will power at least some of the 50. But some of them could be powered by a new generation.

This brings us to the fork in the road facing RR. Last month, Rolls announced its development plans for a new big engine and another that will compete for the next generation New Small Airplane.

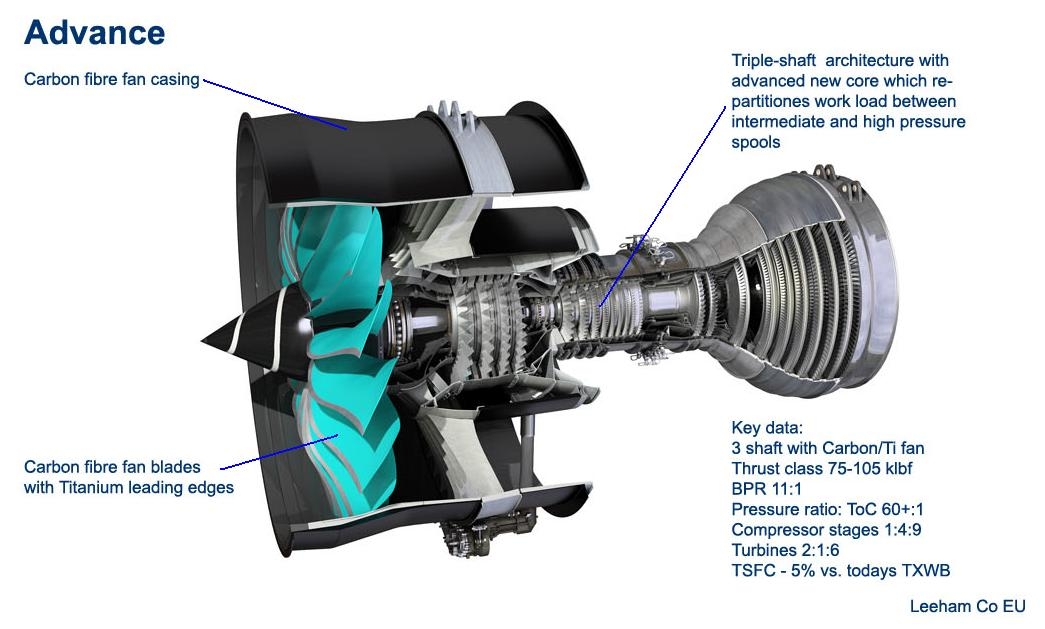

Advance for 2020

The next opportunity is six years away and requires an evolutionary solution. With the A380neo and A350-1100 being the only near-term realistic projects, an engine that can match/supersede GE’s GE9X with a low risk is what is required. Here the architecture diagram for this new triple-shaft as given by Rolls-Royce, with our conclusions:

Diagram 1: Advance architecture and key data based on Rolls-Royce material.

The Advance uses the results from Rolls-Royce’s EU-sponsored technology programs. The CFRP fan concept comes from its developments with GKN and the new compressor/turbine designs are from the different EU ACARE programs. The result is a modest risk program which will fly its CFRP fan demonstrator next year based on a TXWB core.

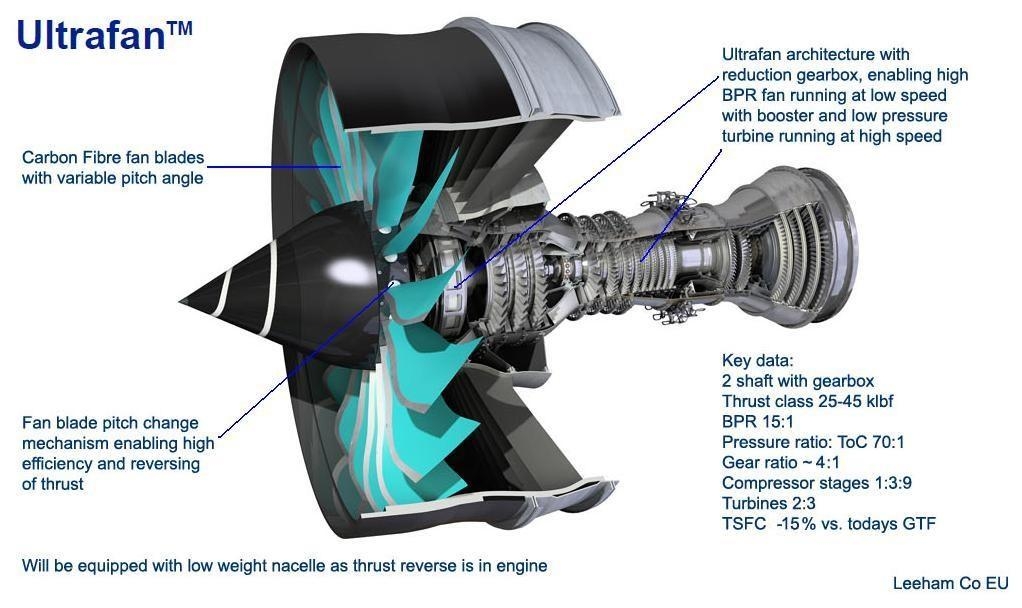

Ultrafan

The Ultrafan is a logical further development of the variable pitch geared turbofan Rolls-Royce worked on 45 years ago. It was a variant of the RR-Snecma M45H (WFV-Fokker 614). Here is the Ultrafan’s architecture diagram:

Diagram 2: Ultrafan architecture and key data based on Rolls-Royce materials.

The variable pitch fan improves the efficiency but also does away with the need for a variable fan nozzle area nacelle and thrust reverser. Rolls-Royce thereby plans to compete with PW’s future offering with a lighter engine matching or exceeding the efficiency of the then contemporary PW GTF.

Having been cut out of the 777X program, having withdrawn from the International Aero Engines V2500 A320ceo partnership and facing an uncertain future of the A350-800, RR is embarking on a new path to expand its wide-body power plants and to return to the single-aisle market.

Neither PW nor GE/CFM will give RR a free path to these market sectors. These will be subjects of future analysis.

The preceding was jointly prepared by Leeham Co (USA) and Leeham Co EU.

“While a re-engined A330 is envisioned with an entry-into-service of 2018 and therefore only the GEnx and the Trent 1000 TEN are the feasible options, selecting the Trent would compensate RR for a canceled A350-800.”

How about delaying the A330neo two years and put the RR Advance engine on it? It would cut A330 fuel burn significant. If the China order for 200 planes comes through, it might not be that hard to bridge the production gap until 2020.

It depends on how much life Airbus thinks a reengined A330 has in it. The initial suggestion was a plane that could be built at 10 per month until the 2020’s, at which point 787’s will be available at competitive prices. In this case, time is of the essence so there is a minimal dip while the A330 is transitioned to the NEO.

Possibly they could hold out for a more efficient plane with the latest engine. The Advance might fit in. In that case Airbus thinks the A330 NEO can compete with the 787 on an equal basis for the forseeable future.

But supposing the A330 will die after a brief NEO period, Airbus will need a new plane. And a new engine. That engine could be the Ultra.

Boeing has to produce 12.5 aircraft per month until 2020 to get rid of all current open orders (900). Here some old news, January 2011:

“As for the overall production ramp up, McNerney says that the margin for achieving the record widebody production rate has shrunk and the bulk of the increase from today’s rate of two 787’s per month to 10 per month will push into 2012, rather than 2011 as previously planned.” (http://www.flightglobal.com/news/articles/boeing-holds-firm-to-787-production-ramp-up-352385/)

There are 65 deliveries for 2013 and for the first two months of 2014 8 aircraft were delivered and now cracks somewhere in new wings.

Airbus is also quite full with A350 orders right after 2020. So there is only one choice for an aircraft available before 2020: the A330. So why put a new engine on this aircraft before 2020?

I wonder how large the dedicated Trent A350 -800 XWB investment is at this stage. Maybe not worrying / keeping anyone awake at night..

Looking at the Ultrafan, that seems an exiting, risky engine.. No doubt aimed a the larger single aisle, small twin aisles of the twenties. I wonder what position key player MTU will take.

I think RR and airbus seem to have a good overlap over the next 10 years.

Airbus is safe on,single aisle for this period with their neo, great cabin width etc. It’s a great ‘passenger’ craft.

The a330… As an airframe is well proven, liked, and reliable, so using this in in the 250-300 market is a more ideal solution, especially on medium/long routes where the a350 is ‘too much plane’. The neo/tweaks will make this even better, and ‘paper’ regional versions can also be offered. The engine architecture is pretty much known, being additive optimizations as,opposed to ‘new-new’ tech.

From a RR 330neo engine, we optimize further for the,a380neo.

The a350-1000 will become a very well understood airframe/engine by the,time a 1100 starts to be drawn, based on weight,reductions/understanding gained on the,900/1000.

Once the 1100 is in the,air, perhaps the 330neo may be superseded by an 800, developed with yet more knowledge from the 900/1000/1100.

All the while RR can slowly optimize their core engine tech to ‘fit’ the trust req’s.

It all seems quite progressive as opposed to revolutionary, meaning investment can be controlled progressively also.

The 787-10 it what makes Airbus nervous, if it delivers on its promises it surely will replace the A330. The question is will RR/GE pay up for the certification of a A330neo and deliver a certified engine/nacelle to Airbus. In a dollar race GE can pay but RR has the most to lose but do not want to pay $2bn to Airbus in cash that GE would pay if it was a Boeing aircraft. If Airbus throws in A380neo as well then RR will get uncomforatbly big for GE and tehy will pay Airbus $3-4bn in cash. RR then needs UK goverment support to overbid GE and be close to GE’s size on big engines

Looking at the current PW1100G compressor configuration (1:3:8) and a pressure ratio of something like 45 I wonder how RR will achieve a 70 OPR with just one more (and then tiny) compressor stage. The fan has to have a low pressure ratio to be efficient, so the low and high pressure compressors have to have high pressure ratios. I have some doubts about the feasibility of the concept especially for a narrowbody:

http://aeroturbopower.blogspot.de/2014/02/rolls-royce-looking-ahead.html

70:1 is high, very high. But the PW1133G was designed a little conservatively. PW got more than a little burned on the PW6000 methinks… so decided not to overdo it again.

The TXWB us above 50:1, or am I mistaken (sure, wb engine, but still).

Re 70:1, RR have given the 8 stage HPC as 22:1 which it will reach already at the Advance time of 2020. A geared booster running at optimal speed should be able to give 0.9 per stage for 2.7 which leaves 1.2 for the fans inner stream, realistic with a low pressure fan. It should be doable come 2025 IMO.

Agree, but 22 from 8 high speed stages is still quite agressive. I think the booster/IPC will run at approx. same speed as today (IP shaft), the difference being the lack of a dedicated LP shaft since the fan runs off a gearbox from the “IP” shaft. 0.9 per stage is also high I think.

Having said that, 60:1 in 2020 almost seems more sporty…

Come 2025, perhaps, but compressor technology is as most other stuff reaching a plateau, the gains from CFD, contoured endwalls, 3D stacked blades/vanes have already been cashed imho. Just pushing conventional tech, you will reach a limit at some point, not sure how far away it is…

But from the pics the boosters almost seem to have rising mean lines so could be that. Gives more aggressive duct, but that tech can be pushed a little more I believe (see FP7 AIDA).

So, could be doable, but will need some work.

If you assume constant pressure gain per stage ( too simplistic, I know )

you need a 1:1.375 pressure differential per stage. ( i.e. 1.375^^12 ~= 45.5 )

Adding just one more stage brings you to 63 ;-). I bit of pimping here and there

reducing losses should bring you past 70 easily.

( And obviously the last stage can have a per stage gains smaller aperture )

While working on the Garrett TFE 731 program one of my colleagues who came from Ham-Std sketched his ideal engine. The fan had variable pitch blade that almost “feathered” at cruise. I had earlier been a flight engineer on the Boeing Stratocruiser – 28 cylinder – geared prop reduction. I was one of the few FE that used 1,400 eng. rpm for cruise. Very quiet at the same horsepower cruise.

Jim Helms

TATSCO

About the A350-800….

Does it make sense to delay it and produce a more optimized derivative a few years after the -1000, instead of a direct shrink of the 900 as it is designed today? Or is the -800 a “lost cause”?

If that could happen, the -800 investment is not lost either…

How much did RR invest in the A350-800 engine? I thought it was just a simple reduction in thrust so suit the A358, unlike the engine for the -1000 where I know there were actually some few changes made to get it up to 97k thrust.

Afaik, the same engine for -800 and -900, software derate submodels (both -800 and -900). -1000 engine (TXWB-97) has quite a few changes.

I agree that only software (data entry plug) difference exist between -800 and -900. Generally, engine price is link to engine thrust, which means that RR has benefit from cancelling -800 and transfer to -900 with bigger thrust engine.

There is no need for Airbus to compensate about -800 at all.

Besides, GE has benefit for A330neo by GEnx-2B. Trent1000 and GEnx-1B do not have customer bleed while GEnx-2B has it. In case RR offer engine for A330neo, RR needs to spend bigger development cost that GE.

Sorry to interrupt, but I need to intervene in honor of the last all-German (yeah, some Dutch was in it) airframe. Quoting:

” It was a variant of the RR-Snecma M45H (WFV-Fokker 614)”

It is VFW … Vereinigte Flugtechnische Werke. Located in Bremen, it is the predecessor of (besides other) Focke-Wulf. Today – after half a dozen mergers – it is the center for high lift systems for Airbus, and assembles the A400M fuselage.

I guess Airbus will let RR have an exclusive on the A350-1100 as compensation.. Esp if it is done as a straight stretch. I think Airbus will have to do the 1100 anyway as after 5-10 years of PIPs and weight saving the 787-10 will eventually eat into the A350-900 market from below in the same way the A333 ate into the B772 market, then Airbus will need to eat into the shorter range part of the B779 market to keep the sales coming. Leaves the B779 in the same situation as the B772 was, which is why I think it is a mistake. I guess the lack of new orders/confimed MOUs probably means Airbus are offering the 1100 now on the quiet.

Assuming that they get their 200 orders from China I suspect that Airbus will put all their efforts into getting EIS the A350-1100 about 2019.

I guess after that would be an A380 NEO in 2020. Clark wants it, and nobody else is as important in the airline industry today. As he wants new engines in 2020 its obvious he doesn´t want warmed over 2007 tech ie GEn1/2 or Trent 1000-TEN.

IF Airbus gets 200 orders from China I guess deliveries would be over 5 years? That´s sort of how they work. Pick up a few extra orders and Airbus could keep the A330 CEO line going at 6 per month until end 2020, allowing them to take RR-Advance or P&W GTF with EIS in 2021 and 2022. That would mean probably the same level of discounts as Boeing give on the B787. A lot more profitable for Airbus than rushing in with an existing tech aircraft in 2018, which would still need a lot more discounting than the B787. The idea is to make money after all, not just make sales

the RR motor for the 350-1000 is already big compromise, basically running the -900 engine past redline at higher pressures/temps because they didn’t want to design a new core and didn’t have room for a significantly bigger fan. any engine for an -1100 is going to need to either be a new core & fan _or_ the -1100 will have to have severely compromised range/payload. the cost of developing a unique engine for the -1000 was already an issue, doing it again for the -1100 doesn’t sound very attractive, meanwhile GE is sitting there with the GE9x motor (pip-3 by then) just waiting to bolt it on.

agreed, I think a straight stretch is all they can do with the existing engine. Still good for a lot of the 777X business though. If Airbus don´t go with Rolls TRENT XWB and want to wait for 2020 for GE9/RR Advance/PW?? then A330 NEO with Trent/GEn2 in 2018 becomes more likely as rushing through everything 2020-2022 is too much. I guess after 2022 everybody will need to look at NBs as YAK-242 and C500 will be mature and well into production. No confidence in C919 as a product but Chinese will be forced to buy it anyway.

RR was willing to split the 777X market with GE with the “Advance” offering. I don’t see why they cannot spend on developing it to put it on a rival frame to split the market. And I don’t understand this “Pip-3” you’re talking of. Conceptually, isn’t the GE9x at about the same stage as the RR Advance at this time?

no, RR was hoping to win the exclusive engine deal for the 777x. Boeing had no intention to offer more than one engine and made that clear to the bidders as the manufacturing costs of supporting 2 different engines is hard to justify.

Scott, you mentioned the engine OEMs forecast 300 to 400 A380NEO market. Do they all feel the same way or is it just one or two?

Also, would that be an A380-800NEO market or also include A380-900 variant?

You have a source for that?

It’s quite laughable for anyone to suggest that RR was hoping they’ll get the monopoly on McNerney and Co’s GE…sorry, Boeing 777X. When Boeing sent out the RFPs for engine proposals, they never indicated to the engine makers or its potential customers whether they’ll sole source or dual-source it. They were undecided right up close to when the final decision was made.

http://www.flightglobal.com/news/articles/boeing-to-decide-777x-engine-strategy-in-early-2013-378657/

“Boeing will decide by the end of this year whether to continue a single-source engine policy or offer customers more choice, says Rich Oldfield, director of technology at GKN Aerospace. “…”Oldfield says that if Boeing decides to offer the 777X with engines from two manufacturers, it is “95% certain” that the R-R powerplant would be one of the options. ”

http://www.flightglobal.com/news/articles/in-focus-engine-makers-prepare-to-do-battle-on-777x-376865/

RR’s vp for strategic marketing “declines to say whether R-R would seek a sole-source deal to power the 777X”

The above statement clearly indicates that, for RR, monopoly was a long shot and something too much to ask from Boeing, and they’d be content with splitting the 777X market with GE.

Whoops, wrong post! Sorry!

Comment was in reply to “bilbo” above.

Has there ever been a turbofan with a thrust reversing fan? I can imagine the mechanism being vey delicate because of a combination of strenght, weight and maintenance requirements. Maybe the fan blades can be smaller/ lighter because they can be adjusted for different speeds / thrust ranges. Will there be doors behind the fan to let the air in during thrust reverse? There might be some FOD challenges.

It feels like they’re embarking on a project as potentially revolutionary as their Hyfil bladed RB211. Very bold move but brilliant if it works.