Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Boeing 777 production rates

By Scott Hamilton

Feb. 27, 2017, © Leeham Co.: When Boeing announced it will reduce 777 production to 5/mo, with actual deliveries of the 777 Classic to 3.5/mo beginning in 2018, the aerospace analyst at Goldman Sachs immediately concluded Boeing will have to reduce the rate to 2-2.5/mo.

Since then, and other analysts (whether publicly or privately) reached a similar conclusion.

On the 4Q/YE2016 earnings call in January and again last week at a Barclays conference, company executives said 90% of the positions in 2018 and 2019 are sold.

Shortly after the Barclays conference ended, one analyst called me to challenge the assertion by Greg Smith, Boeing’s CFO, about 2019. By his assessment, the analyst could only get to 60% in 2019. Did I see anything differently?

59% or 74%, but not 90%

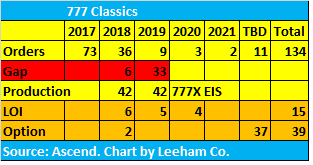

At that point, I hadn’t looked. When I did later, I got to 59% based on firm orders. I could get to 74%, giving Boeing every benefit. But I couldn’t get to 90%.

Here’s what I did, using the Ascend data base and Boeing’s information on its website.

According to the Boeing website, there were 103 777-300ERs and 32 777Fs Unfilled at Jan. 31, 2017, or 135 total.

According to Ascend at Jan. 15 (last time I pulled the numbers), there were 133 firm orders—pretty close—15 LOIs (Iran Air) and 39 Options (mostly EK and Etihad, with the balance SQ). EK previously said it doesn’t want to take any more -300ERs, though certainly this might change.

Ascend shows the delivery distribution at follows:

I get that Ascend isn’t 100% accurate. But bear with me.

Ninety percent of the slots filled at a delivery rate of 3.5/mo (42/yr) is 38. So, 2018 is fine.

According to Ascend, 5 -300ERs TBD are Pakistan. I understand these are going to United. Let’s assume these are in 2019. This takes 2019 to 14.

Six 777-200Fs that are listed as TBD are for Hong Kong Airlines. I’m not sure HK will take these freighters, but let’s assume they do and let’s say these are all in 2019 (unlikely they’d take this much F capacity in one year, but let’s say they do.) That brings this to 20 deliveries in 2019. Iran Air, if consummated (and President Trump doesn’t trump the deal), that’s 25. That’s 60%.

Even if the 2020/21 airplanes from Ascend are allocated to 2019, this becomes 74%. (The skyline can move around. These are 777Fs.)

I just can’t get to 90%, even being most generous to Boeing.

Rate 2/mo

On the other hand, if 60% is the more realistic figure, this comes to 25 aircraft (60% of 42/yr)—or 2/mo.

There is still time to sell more Classics for delivery in 2019, but not a lot of time if these are -300ERs. Buyer Furnished Equipment (i.e., interiors) orders typically need an 18-month lead time for passenger models.

But as the entry-into-service gets closer for the 777-9 (right now, early 2020), the less likely 777-300ERs will be orders, or options/LOIs converted into firm orders.

Orders for 777Fs can be closer in.

What Boeing says

I reached out to Boeing’s Corporate Communications in Chicago (the HQ) for comment. The reply was that there was nothing to add to what had previously been said.

Here is what CEO Dennis Muilenburg said on the earnings call and what Smith said at Barclays (emphasis added):

Muilenburg on earnings call, Jan. 25

Within the updated rate plan, delivery slots for the 777 are now nearly sold out for 2017. For 2018 and 2019 when we begin phasing in 777X production, we are now approximately 90% sold out for both years where, as a reminder, we will be delivering at a rate of approximately 3.5 per month. This rate plan includes the recent agreement from Iran Air for 15 777-300ERs, and we continue to work a number of 777 sales campaigns to fill out the remaining production slots. Based on the current sales environment, we believe the rate plan we’ve put in place establishes a production floor for the 777 program. And we have a strong foundation of 320 777 exporters and commitments that support our production plan for ramping up 777X deliveries.

Smith at Barclays, Feb. 23

Well, if you kind of just start with the market to the production rates, the commercial market. I think, the answer is yes there, as we see it today. But, what do we focused on, filling the bridge on 777, and we made great progress there and at the same time modify that rate down. But, we got work to do and we’ll continue to keep everybody up to date on that, but that risk is definitely not at a different – it’s had a different risk profile than it once was because of those elements. We’re about 90% sold out in 2018 and 2019. And so, we’re focused on filling at the same time, focused on keeping those folks in the skyline through that period. So getting through that, because if you go pass this, there is a big replacement cycle in wide bodies coming. So, we need to get through this transition in this, these areas of softness on the wide body. And then of course 87, we have making the final decisions on going to 14 a month. And so as that fits today, that looks good, but we’re monitoring.

A350 trouble ahead?

There appears to be some trouble brewing for the Airbus A350.

United Airlines publicly said on several occasions that with the addition of 777-300ERs to the fleet, the order for 35 A350-1000s is being reviewed. UAL took the -300ERs on the cheap as Boeing struggled to fill the bridge between the Classic and the X. UAL officially ordered 14. Market intelligence says it’s also taking the five previously ordered by Pakistan International Airlines, which is swapping these to 787s. There’s been no announcement on this, however.

With the addition of perhaps 19 -300ERs, UAL doesn’t need 35 A350-1000s. Would it want a small fleet of 16? Presumably not.

What to do?

United floated the idea of taking A330s instead. This could start to solve the problem of what to do with its aging fleet of 767s.

Over at American Airlines, market intelligence indicates that the New American Airlines finds the A350-900s surplus. These (22 of them) were ordered by US Airways, while the old American chose the 787 for its next generation of long-haul airplanes. The new American rescheduled the A350s once already.

Officials are trying to simplify the very diverse fleet of the combined US Airways and American, not add complexity. This raises the question about the future of the A350 order.

Like United, American could opt for the A330 to begin replacing the 767 on 4,500nm routes. AA already has the A330-200 in its fleet (from US Airways). But the A330-800 is different than the -200 and its range is well over 7,000nm.

It will be interesting to see how Airbus manages these new and unhappy challenges.

On a personal note

The National Geographic recently published this 13-minute video of an abandoned Russian city in Svalbard, north of Norway well inside the Arctic Circle. On a vacation a few years ago to Svalbard, one of the stops was this Russian city. Only about six Russians live there. Despite the long-term global politics, the Norwegian locals and American tour guides get along fine with the Russians. On a people-to-people basis, life is about getting along and helping each other. It’s too damn bad the governments can’t behave like the ordinary citizen.

My Svalbard trip reports are here, here and here.

Any solution via adding in more “blank” slots that count as full use of the FAL process?

Boeing once talked about not needing to reduce 777 production rate but would fire “blanks” through the process.

If they now reduce the rate that will still include the blanks !?

( bit of a mind f*ck, for sure. But that is about what one can expect from past experience.)

As Boeing officials are fond of saying, it’s deliveries that matter. Shooting blanks doesn’t help the cash flow or the profits.

Grin, touché.

The A350 programme seems to have suffered more than its fair share of problems with its order base. I have no doubt that it will be a very successful programme overall but it does seem too easy for airlines to drop down to the A330 or even up gauge to A380 presumably at considerably lower relative prices.

These include Emirates loss, American (double) deferral, potential United loss and the Qatar order being delivered at a snails pace. Let’s not even talk about the Sri Lankan debacle

It may a “drop down” for airlines to switch from the bigger and long range A350 to the A330 but it might be an upgrade for Airbus’ profits.

Sri Lankan Airlines order is about 4 aircraft and 3 or 4 more leased aircraft. A350 is being delivered at snail pace to all airlines due to problems already discussed on this site. As already mentioned I wouldn’t look at United switching to A330 as a financial loss for Airbus. American deferred the orders to 2018. The Emirates cancellation was huge but the A350 still has an impressive backlog.

Yup maybe it works for Airbus in the swings and roundabouts. Regarding the snails pace of Qatar however it is of a different order to other aircraft.by my count they have 6 aircraft in final assembly that are ‘out of order’ and would have been delivered to any other airline. Also all but one are not painted. They were theoretically receiving 13 in 2016 and actually took 5. Perhaps there is a world shortage of that particular shade of purple or alternatively something more fundamental is at work

In a parallel move Qatar is wet leasing A350 from LATAM.

Looks a bit convoluted.

Boeing seems to have a hand for turning around existing orders to their advantage. ( example: 777 for A340 swap)

Wonder how much that costs them.

El cheapo will later be declared technologically superior 🙂

Wonder how much el cheapo A380 orders cost Airbus?

If they had gone that way BA would have acquired further new A380. They haven’t yet. lets see what happens there.

I wonder how much Airbus’ yearly December el cheapo orders cost them!

I don’t see the A380 as being a sensible up gauge for the A350. The number of routes the A350 can do profitably are much greater that what the A380 can be placed on.

2017 could be a good year for top off orders on the 777-300ER if the price is right. I could see both AA and UA cancelling the A350 as it brings not much benefit but adds another fleet type and its associated costs.

Just my 2 cents worth.

I was referring to the Emirates A350/A380 order shift, sensible or not it happened 🙂

Airbus is strong is the single aisle space but has a weak track record in the widebody sector. It is good though for Airbus to aspire to be successful in the widebody sector. Boeing could use a solid competitor. I suspect though the Chinese with their huge home market will beat the French to the punch.

Not sure that Airbus will be taken over by the Chinese any time soon. They may not match Boeing in this segment but with 3 active WB programmes and thousands of sales and orders I think arguing that they have a weak track record and that they ‘aspire’ to be successful are way wide of the line. The A330 has been one of the key success stories of the past 15 years and continues to be competitive, the A350 promises to take much of the old B772/3 market in the next 15 years. The Chinese won’t have a viable competitor for at least 10 years. What you say is not borne out by fact

There was simply too much ‘call’ for totally new aircraft designs in the last decade. it takes so long to develop them that by the time they’re ready… the cycle has changed.

The loss of a350 orders can likely be dealt with with slower ramp-ups [maybe thankfully], but as I’ve commented before, (the lull in current generation aircraft sales/production + the slow ramp of the new generation + the cost of development of the latter) has gotta totally screw up both manufacturers and will affect any MOM decision – where’s the money gonna come from… especally if the MOM affects the sales of yet another ceo model [737] and launches another (lull+research+slow-ramp] cycle of reduced cash – $$$$ payments are made at delivery – not at order, and early orders for new models are discounted.

Airbus has managed that lull much more than Boeing… indeed it the 330ceo has benefited greatly from the 767>787 s changed over, and again the 330ceo still sells pretty well even with the neo on it’s way [any new on the trent 7000???].

I’d hate to be an accountant at Boeing trying to make the graphs’n’numbers work.

The beauty of the MOM (if it works and the market is there) is that its an all NEW area and screws up nothing for anyone.

At worst it picks off some A321 sales that are a force fit for lack of anything that really fits a route.

It is a heck of a field, but it always has been and that’s why they make the big bucks and there are only two competitors left.

MD had a poor line up before the demise and Lockheed only dabbled in it with the L1011.

Oh don’t get me wrong… MOM @ Boeing will happen as it has to. I just think it would have happened already if not for the upset new program’s cause to existing ones… The effect of sales and sale prices… ‘that tapering off lull’ from current lines, and that unpredictable cycle when product is ready (post investment).

It just a very tricky move with so much Dev money already spent on 787/47/77X.

I don’t see any beauty in the MOM/NMA decision to Boeing. They can expect a marginal win if they hit the correct market, develop to timeline and cost and the economy holds good. Alternatively they could be left with a disastrous loss. They are forced to act by circumstance but the lack of enthusiasm is palpable. The upside on this one is marginal at best

Any sign of political pressure in these decisions?

I am shocked, I say shocked that politics would have anything to do with a capitalistic market decisions.

The next thing you know, Boeing will build a factory in Charleston to stick it the union!

Last year Airbus sold 124 widebodies (83 A330 and 41 A350) in what everybody is calling a bad year. Not bad for a bad year. The A330 isn’t having the sames issues as the 777. The A350 is slot restricted, which is hampering sales.

United and American may indeed do what the rumours are suggesting but it won’t concern Airbus a great deal. History shows slots have been quickly taken up. Having said that, I think United and American will think long and hard before letting the A350 go

Loosing a customer for a type always concerns a mfg be it Airbus or Boeing.

United and American are not going to dump Airbus. If these release slots it is temporary at best!

United has turned into another Qatar, what it wants when it signs the order is not what it wants when the time comes to play ball.

There was the schemozzle over the Boeing 737-700 vs Bombardier Cseries which supposed to be a filler from the small Boeing runout but ended up as just a ‘political designed move against the Canadians’ as United doesnt need that sort of plane after all!

Now United is playing some sort of political game against Airbus, when its likely any orders for 777W that arent going as 747 replacements end up as a switch to the 777X models. United still has a lot of worn out 777-200’s that it needs a replacement for.

I see Boeings hand in all these maneuverings, which hide the reasonable rational fleet orders that eventually happen

I see Putin’s hand…

UAL and AA might have US Government dangling contracts if they do not pick up Airbus widebodies. Similar to the FedEx buying 767’s. Soon the Ex-Im bank will be fully functioning and Boeing can quickly offer a trade in all remaining 747-400 pax Airlines for 777-300ER’s getting production numbers up.

“The A350 is slot restricted, which is hampering sales. ”

The problems run deeper than “slot restrictions. Compare it to the 787 sales, 2013 was the last year the 350 outsold the 787 230 to 182, Since then the 787 has outsold it 172 to 9. Until last year the 787 had a bigger backlog.

If you look back far enough, 2010 to 2012, the 787 had the same problem as the A350. During 2010 to 2012 period the airlines were in the middle of a buying spree, but nobody bought the 787

Time will tell, but my guess is that once the A350 backlog reduces sales will pick up

The A330 is not having the same issues as the 777!

Scott:

I am confused on the A330-NEO choice for either group.

Is it that even the -800 has too much range (or has far ore range) than the 767 it would replace? (as well as too muich passenger cpaicity)

And does that not make 767s very attractive or really the only alternative for replacing itself for that segment below the A330 but not a 787 market?

Back to doing the miner tweaks and Scimitar Winglets, best latest engine upgrades without an NEO and viable for the future?

@TW: The 767s are aging and the A330neo is the only (cheap) choice to replace it. The A330-200/800 has way too much range (as does 787-8). But in international configuration, it comes closest to the capacity AA, DL and UA want. Boeing is essentially dropping the 787-8 (though it denies this), focusing on the 787-9/10 (which it freely acknowledges). The A330-200/800 is far cheaper to buy (or lease) than the 787-8 and Boeing is fiddling while Rome burns on the Middle of the Market aircraft (NMA). Launching the NMA is necessary but won’t happen this year, when it should.

Boeing is likely to launch their NMA in the not to distant future? They would have gone for upgraded landing gear, wing mods, LEAP 1A engines etc. on the MAX10 if the NMA was far from being “activated”.

The NMA could be a single aisle (180-230 seats) with wider seats and wider aisle (better ergonomic, access etc.). By then the PW1100 problems should have been resolved? A 767MAX (New-300ER) could be part of a Boeing “NMA package”, this will bridge the gap between a new “wide” single aisle and the 787-9. The 737MAX8 could cover the “lower-end” of the single-aisle market for still a very long time.

Boeing is good at “distracting” Airbus, with the 777X Airbus is drawn into the study of a stretched 350-1000, then airlines start ordering B787-10’s (won’t be surprised if Air Malaysia and others also go the SIA route?). With the 330-NEO Airbus is trying to do catch-up on the 787-8/9. Next thing you see there is Boeing’s NMA offering/s, then they scramble after that.

Airbus should wake up before they loose the single-aisle market in a few years as well?!

I though Airbus quite helpfully were retaining the CEO just for this eventuality. On the 767 pairs the CEO is likely to be a more cost effective solution. Much as I have enjoyed the 767 as my stock choice of transport over the past 20 years it’s time has gone.

The 737,777,A320,A330 have all been upgraded and are selling well. Why not a 767MAX, good range 5000+ miles, 200+ seats and the line is still open. The lowest cost option available and the quickest to market.

The 2-3-2 seating is the most passenger friendly arrangement, more window and aisle seats and quicker deplaning. The sweet spot for many routes.

Scott: I get the 767 ageing.

But for its size, range and what should be pretty low costs, can buying a new one with the enhancements there (engine updates in place ) and adding the Scimitars Winglets keep it competitive? (appealing?)

It has a production base with the KC46 and FedEx buys to work off of.

It should be cheaper to make than an A330, let alone the A330-NEO.

Steve/Sowerbob:

Still try9ng to find out why the 767 is not as cheap as the A330.

Its been in production longer, it has a solid base.

That said, I don’t drive a tractor trailer around town, I do a station wagon.

A good part of the time even that is too much. I could drive one of those wrap around tiny cars and be fine (other than cramped – my wife would kill me if I tried to sell the wagon)

The point is, if you don’t need a Semi (A330 of any type) then why is the 767 not an option?

You have a 3 engine shootout for options, you have the latest PIP those engine offer,

In other words , its seems like a good option for the right market.

The A330 is nothing more than a longer A300 and that tech is even more dated than a 767.

@TW

I think you are fishing here. The A330 has a number of fundamental benefits that sadly missed the B767 by a few years or by priority or by design.

The A330 benefitted from FBW which has enabled it to be refined and updated substantially over the. It also benefits from a superb wing, it took the science/art forward a notch and has been fettled over time. Further the A330 has been continuously evolved with an intensity the B767 did not, all to do with the relative importance of each model and overstretch at Boeing.

The upshot is a relatively minor upgrade allows the A330 to compete at near parity with the B787 on some missions, quite astonishing given the age of the base product and the evolutionary change during that period. The B767 remains somewhere near the A300 killer it was, a pity as I like the cabin format and it always feels like hewn from solid metal.

Was the B767 worth a fundamental makeover? Well given the B788 matches the basic plan of the aforesaid I believe Boeing wrote off any further B767 development around 2004 if not earlier.

The 757 was discontinued due to lack of demand _boosted_ by an overcome production process.

767 and 757 are (late joined) siblings from the same design generation. Boeing’s aerodynamics made a real step only later with the 777 where Airbus had already moved forward with the A310 wing.

I suspect you are right about missing things

Just what I am missing is what I am after

All good ideas on that.

How much of the missing “goodies” were put into the 767-2C and how much is left to do for the 767MAX?

@claes

The 767-2C offers nothing new except a bullet proof cockpit section with flat-screens. No better engines.

The wing is an ordinary -300 wing pimped with -400 flaps.

The 2C is based on -200 fuselage in length.

(You may search for “Frankentanker” as picture.)

That short fuselage might be later on a source of enduring profit for Boeing or which company ever makes the engine nacelle or engine suspension. Perpendicular to the cargo door the engines are just a few feet away. Steering backwards slightly to the right is fatal. Angle from cargo door to engine is about 45° for -300F are; 2C maybe 10° or less. Right behind the pilot seats a station for refueling operators is located. Then a section with permanent seating is following.

You may ask why such a short fuselage? The rotation angle of -300 was to small to get -300 based tanker up in the air with required fuel load on board for a certain air field length. Still the A330MRTT is able to take off with the required fuel load from twice as much airports (~800 vs. 400). “It’s the wing …”

Trans World,

I think what you are missing is the ability to read the writing on the wall vis-a-vis the 767.

The fact is that not that many customers are interested in it any longer, especially when it is compared to the A330.

It’s not like Boeing wants to drop the line. They have been doing everything they can to keep it in production, all except for making a MAX out of it.

It would seem they know that making a MAX out if is also not going to help sales or maybe they have other plans for that market segment.

Nudge, nudge, wink, wink.

Hi Scott,

I am from the Mining Sector and new to the Blog. The only things I know from the Aviation Industry is the internet and being a passenger for 100’s K km (My father was a fighter pilot and served in the Korean War).

My Question is technically how easy/difficult will it be to install the current A330 engines (Tent772, GE) on the A330-Neo (Engine management systems, etc)? These will give a ~3 Ton weight and US$28M cost savings on the engines alone compared to the NEO, the penalty being Opex. I believe that a 232/8T MTOW A330-“800” with the NEO wing/cabin/etc but with the current engines, a shorter maximum range (~6 000Nm), better Engine-Ground Clearance (Dessert Strips) and higher seating density with lower Capex will be competitive and potentially sell well, especially with the new trend for Low Cost Carriers to enter the Medium-(“Long”) haul market (Want to call this the A330-8). Replacement of aging 767’s and early generation 330-200’s are also on the cards, the target market mostly the smaller Carriers.

Personally I foresee that the B787-10 is going to be a late bloomer hurting the A350. Also think what a re-winged/-engined B787-10 with a range of ~8000Nm will do to the A350? (p.s. Sitting at the back of a 787 is NOT fun)

On the 777-300F/ER I can’t comment except that if there are indications of production delays or big orders for the 777-X there could be an increase of current 777 orders, especially Lease Companies, to breach the supply gap of the X.

Thanks, Anton

Dear Anton,

the mayor difference between the A330ceo and the neo except of the engine type are the wing tips. I guess all the other enhancements are also available for A330ceo. An ceo with neo’s wing tips might require a complete certification process to calibrate the flight computers for the new wing tips. That could lead to a similar problem the A380neo encountered. The money for fuel saved is not as much as the higher price required to pay of the engineering effort.

Thanks MHalbaub,

Suspected life is not that easy. Hope the 330-Ceo/Neo have a good future. Flying at the back in a 787 in 3-3-3 configuration makes flying longhaul an unpleasant experience if you have a larger frame.

The A330ceo engine are getting old by now. Airbus could ask GE if they want to upgrade the CF6-80E1 with all the GE9X goodies for a 75k CF6-80E2, like composite containment, revised HPC, new ceramic burner liners; NGV; T2 vanes and shrouds in addition some Ti-Al LPT stages. Airbus can promise a lighter Al-Li wing with some A330neo aero. GE can promise 10 000 cycles on wing if max thrust is 58k.

Sorry,

I don’t understand the argument.

Because Boeing has a gap in B777 it sells it’s B77w so cheap, United & American drop the A350 – the most modern long haul plane?

Why?

There are 22 B744 still active with 374 seats – you can bet A350-1000 is a pretty good replacement.

The 10 B77w are more a addition to a B772 fleet.

And with beeing down to 4 major carriers, there might be room for growth.

Why should United add A330 when it’s already in B787? The argument is too much complexity in fleet – but it’s used agains A350. So why bring A330 in then?

American has a nice fleet of B787 – 8 and -9 . A359 would add nice to it, giving a lot of chances to adept routes to demand.

It seems a bit constructed for me.

And idk about Boeing, but reducing the rate while changing from classic to x doesn’t seem like a big issue.

On top, there have been rumors Boeing is early with B777x.

So what about just manufacturing B777x in 2019 already?

Sell a few more B777f and maybe some B77w, be a little early with B777x and the gap is not existant.

Why buy the B77W over A35J or the A333/9 over B788/9? In both cases the answer is “fuel is now (relatively) cheap.” So it makes sense to save on the up-front capital costs and pay in the form of higher fuel burn. And in the case of 330neo vs 787, the fuel burn advantage is very slight, especially for the intermediate stage lengths that UA is probably looking at.

Cheap now, but new plane is calculated for lifetime cost of idk 15 or 20 years, so you work with a projection of fuel prices.

Idk if a decision to buy 10 B77w for a super cheap price to add to a fleet of 70+B777-200and its’ versions is a argument against a order of 35 A350-1000.

Imo not when you have 22 B744, 21 B757-300, 51 B767 and 74 B772.

With just 44 B787 as replacement & addition.

All of them above are pretty old planes, and it’s possible United is pushing out old B772 and replace them with B77w while A350-1000 will be added to the fleet 2018/19 on.

United may be interested in A330neo and A321neo, to replace it’s B757/767 fleet. But I don’t see evidence to let down A350 order from.

The 773 is now cheaper than the A350.

The guys with the golden parachutes don’t care about tomorrow. They just thing about their bonuses.

15 or 20 years? Not their business.

Not a clue of airline business.

A fleet decision like this follows a long term plan, a process.

It’s not a managers decision.

It’s a process with many different factors, complicated models about future demand and cost.

It’s not like a bunch of managers have a sit in and fall in love with a plane.

UAL is taking a bet that oil prices are going to stay relatively low. And honestly I don’t think it’s a bad bet…shale oil is cheaper to extract than we thought it would be 5-10 years ago. I say this as both a UAL shareholder and a passenger who utterly detests the (10-abreast) 77W from a comfort standpoint.

Boeing may choose to sell 777-300ER’s and 777F’s at a lower price using incremental overheads. Basically, they have a manufacturing and supply chain overheads spread over the production rate. If the production rates go down, there is less people/material to absorb the overheads and they will go up. With incremental overheads, they can justify a lower sell price to bridge to the 777-8/9. The use of incremental overheads is justified as long as you are not investing in more tooling or manpower.

It’s interesting that the A330-300 is selling better than the 777-300ER. I suppose the larger size is more of a liability. But, the same rationale works for both. With fuel at more or less stable prices for the future, top up orders at end of line pricing will be a smart buy.

Thats because based on list prices a 777-300ER is 50% more expensive than the A330-300

United is really using 777-300ER for replacing its 747-400s- long after everyone else- but should have gone for the 747-800.

That way they can have the A350 as well and use both to juggle demand on long haul fleet. Say trans pacific flights to Australia in summer have the 747 in summer and the A350 in winter and the same for north pacific with some routes having 747s all the time such as Tokyo and Shanghai.

Boeings machinations have probably prevented that.

No 747-800, there is a 747-8I

Yes, the 747-8 for United would have been the way to go. Painted in the old Continental black meatball livery.

What is more profitble for Airbus, replacing all UA´s 767s with A330s or selling the A350s? My guess is the A330 business will be better for them, paid for and slots are sooner. A350s will find a home somewhere, EK maybe? Though I think that will depend on when slots at a Dubai airport become availabe. Remember too that these stories usually don´t happen in a vacum, Airbus and United are already talking and each is busy calculating how what and how much to make the changes.

It may be a wash as the A330 claim to fame now is the low prices.

Same as a deal for a new Aircraft to get market share.

I would think the more A350s the better for Airbus as they have all the costs to pay for.

Äirbus does not do program accounting.

A350XWB outlay is directly paid from profits fron the A320 and A330 sales.

(Much) later profits from A350 ( maybe A380 🙂 deliveries will nurture another new project.

What Airbus will look at is how efficient investment in the A350 ( and any other established frame ) was/is.

EK will take no more 777-300ERs, their base is maxed out and a lot of 777s will come off lease/are getting old and I dont see them taking a lot of smaller aircraft. Could A350-1000s be back in the plan as part of an A350 order? You can be sure EK have a plan and it doesnt include shrinking, but they are having trouble now competing with long haul LCCs and I dont see a long range aircraft only solution on shorter sections as working, but what? I remember reading that Airbus are working on a 16.8 x 10 seating setup for the A350 by slanting the seats a bit. A shorter range B777-X equivalent? So having A350 slots for EK and A330s for UA might be a profitable deal, as both will take a lot more than 35 aircraft in the long run.

Just wondering with the current Geo-Political environment in the USA if an Airline like UA with an apparent “aggressively” pro-American CEO will buy European aircraft with British engines?

That’s why I was thinking about a “hybrid” A330-900 with all the NEO features (including wing) with the current GE-engines (tweaked where possible -> 75K Lb thrust?). A new certification will be required but should not cost an-arm-and-a-leg and take ages. With possible landing gear upgrades and increased MTOW range could be increased to a ~6 800 Nm variant?

Did Airbus went the right way with Trent 7000, news on the new engine is very thin and time is ticking, are there more delays on the way for Airbus? A breeding ground for 787-9/10 orders!