Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Does an A220-500 need a new wing and engines? Part 4. July 3, 2025

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

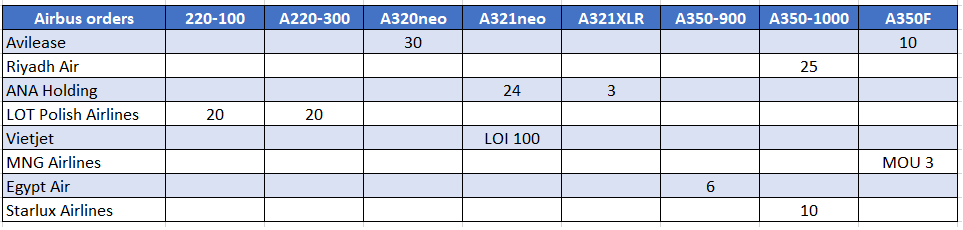

Airbus books 142 firm orders as Boeing retracts from the Paris Air Show

By Bjorn Fehrm

June 19, 2025, © Leeham News at Paris Air Show: Boeing chose to scale down its participation at this week’s Paris Air Show out of respect for the victims of the Air India crash last week. This left Airbus and Embraer to announce new orders, with a total of 142 firm orders for Airbus and 60 for Embraer.

Outside the order activity for the three large airliner OEMs, it was a relatively quiet show, with few noteworthy announcements of advancements in areas such as Sustainable Aviation.

Figure 1. Airbus orders and commitments at the Paris Air Show. Source: Airbus.

Airbus sees Boeing as medium-term competitor, with Comac next

By Scott Hamilton

![]() June 14, 2025, © Leeham News: Airbus and Boeing forecast a significant production gap during the next 20 years of more than 2,000 aircraft per year in their current outlooks released in conjunction with the Paris Air Show. The event begins Monday.

June 14, 2025, © Leeham News: Airbus and Boeing forecast a significant production gap during the next 20 years of more than 2,000 aircraft per year in their current outlooks released in conjunction with the Paris Air Show. The event begins Monday.

Neither company can fill this gap given their current production rates and the goals they have for the rest of this decade.

This means other manufacturers must step up. The question is who?

China’s Comac is current producing a competitor to the Airbus A320neo and Boeing 737 MAX, the C919. But the production rate is excruciatingly low.

Comac also has plans for a widebody airplane to compete with the Airbus A330-900 and Boeing 787. If past is prologue, development of this aircraft will be much longer than the target entry into service of 2029.

Embraer currently is the world’s third largest airliner manufacturer. However, its jets seat between 76- and 144 seat. The company is studying whether to enter the mainline jet sector, but the decision seems a year or more away.

Start-up JetZero wants to develop a Blended Wing Body aircraft for the 250-300 seat sector. But it has little money, no engine and, LNA believes, little hope of meeting the ambitious timeline of having a demonstrator aircraft by 2027.

In a media briefing on June 13, Airbus named Boeing as its medium-term competitor; China is most like to become one; Embraer is a question mark; and JetZero appears to be making little progress, in its view.

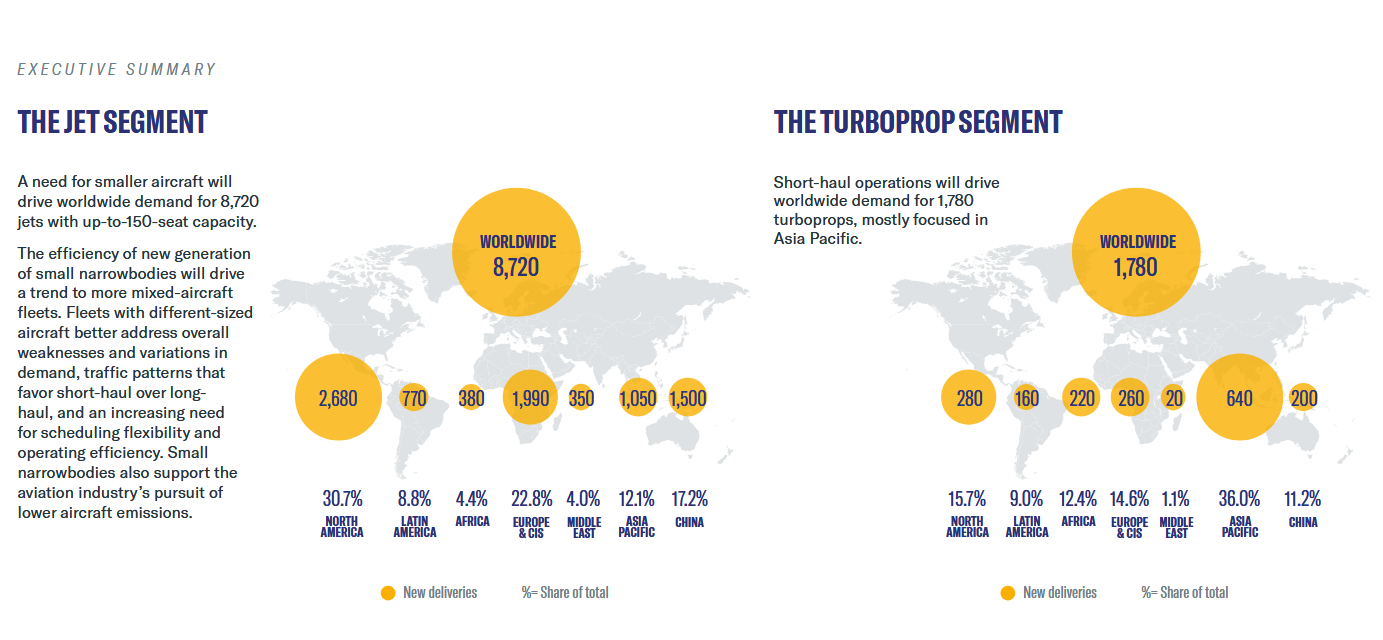

Embraer’s 20-year market forecast under 150 seats: fewer turboprops, jets about the same

By Scott Hamilton

June 14, 2025, © Leeham News: Embraer’s 20-year market forecast for airliners with 150 seats or less shows a decline in anticipated turboprops and a jet outlook (100-150 jets) about the same as last year’s study.

The study was released days before the Paris Air Show, which begins Monday.

Credit: Embraer.

Embraer now sees a demand for 1,780 turboprops and 8,720 jets. Embraer and ATR, now the only new producer of turboprops outside China and Russia, previously forecast a demand for around 2,100 turboprops. A few years ago, Embraer appeared on a path to develop a new turboprop. It shelved the program, stating there wasn’t a new engine available.

Embraer’s current airliner family consists of the 76-seat E-175 E1, the 100-seat E-190-E2 and the 144-seat E-195-E2. Officials publicly acknowledged that Embraer is studying whether to enter the mainline jet segment of 180- to 230 seats.

Services are driving revenues and profits in difficult times, Part I

Subscription Required

By Karl Sinclair

May 15, 2025, © Leeham News: The aerospace industry is a maintenance-intensive operation, where strict regulatory rules drive many requirements.

Assets must be constantly maintained, governed by the time or usage an airline derives from them.

This goes for airframes, engines, and human resources.

Services account for a large part of aerospace corporate profits. Boeing’s Global Services division is the most profitable part of the company. Photo credit: Boeing Global Services.

Some equipment manufacturers derive little or no profits from product sales, but they make lucrative and long-term revenues from attached maintenance contracts.

Political factors are also coming into play in the services segment.

As airlines are forced into a difficult and expensive decision regarding the payment of tariffs on new aircraft they acquire, many could opt for a different strategy.

Older aircraft that were due for replacement with newer, more fuel-efficient jets will be sent into MRO facilities for an additional heavy-maintenance check.

With falling fuel prices playing less of a factor in the acquisition decision, airlines will be tempted to defer deliveries (thus avoiding the payment of tariffs) using their current assets in their installed fleets.

Extending an aircraft’s useful life by another six to seven years will allow carriers to simply wait out the tariff threat when things return to normal.

LNA looks into the growing services revenue segment among various companies in the aviation industry.

Embraer downplays tariff impact on 2025 results

May 6, 2025, © Leeham News: Embraer CEO Francisco Gomes Neto sought to reassure investors on Tuesday, emphasizing the limited effect of new U.S. tariffs on the company’s operations as its Q1 2025 results were published.

![]()

“Our initial analysis points towards limited impact and we remain confident in and reiterate our 2025 guidance,” Gomes Neto said. He added that the company is “working on initiatives to limit impact of U.S. tariffs on our business.”

Gomes Neto credited the resilience in part to its high U.S. content, with Embraer aircraft incorporating substantial American-sourced components and systems—a factor that helps blunt the impact of cross-border tariffs.

But he added: “We join other companies in calling for a return to zero tariffs… for a highly globalised industry.” Read more

Embraer reports record revenue in 2024, eyes growth in 2025

By Leeham News Team

Feb 27, 2025, © Leeham News: Embraer closed 2024 on a high note, posting record-breaking revenue and strong aircraft deliveries across its commercial, executive, and defense sectors.

![]() The Brazilian aerospace manufacturer reported total revenues of $6.4 billion for 2024, a 21% increase year on year (YoY), reaching the high end of its guidance range. The company’s Defense & Security division saw 40% revenue growth.

The Brazilian aerospace manufacturer reported total revenues of $6.4 billion for 2024, a 21% increase year on year (YoY), reaching the high end of its guidance range. The company’s Defense & Security division saw 40% revenue growth.

The fourth quarter of 2024 was particularly strong, with revenues totaling $2.31 billion. Embraer delivered 75 aircraft during the period, including 31 commercial jets (20 E2s and 11 E1s) and 44 executive jets (22 light and 22 medium).

For the full year, the company delivered 206 aircraft, comprising 73 commercial jets, 130 executive jets, and three C-390 Millennium military transport aircraft. This marked a 14% increase in total deliveries YoY, aligning with its guidance. Read more

Earnings: Pay closer attention to the supply chain than to the OEMs

Subscription Required

By Scott Hamilton

![]() Jan. 23, 2025, © Leeham News: Earnings season begins today. Among the companies followed by LNA, GE Aerospace and Hexcel report today. RTX and Boeing report next week. ATI and Spirit AeroSystems follow the week after. Other suppliers follow then.

Jan. 23, 2025, © Leeham News: Earnings season begins today. Among the companies followed by LNA, GE Aerospace and Hexcel report today. RTX and Boeing report next week. ATI and Spirit AeroSystems follow the week after. Other suppliers follow then.

Airbus doesn’t report until Feb. 20. Rolls-Royce reports on Feb. 27.

The manufacturers draw the headlines, but LNA found long ago that the supply chain often provides better information to draw conclusions about the future than listening to the OEMs. All it takes is one supplier to fall down on the job to muck up the works for the OEMs.

That’s not to say listening to the OEMs is not important. Clearly, it is. But there’s just no getting around it: the credibility of many of the OEMs is damaged. Airbus hasn’t hit its production ramp up targets in years. Quality control suffers. And deliveries are consistently late.

Steven Udvar-Hazy, executive chairman of the board for Air Lease Corp, says that every single Airbus aircraft, 250 of them, has been late since 2017. That’s long before the pandemic began in March 2020, which caused such disruption continuing to this day. Airbus was still delivering A320ceos during 2017 and 2018, which didn’t have engine issues.

Boeing’s credibility speaks for itself. It doesn’t matter that it has a new CEO. Until Boeing starts performing, anything it currently says is hope, not performance. Post-strike delivery recovery will be an important indicator of Boeing’s performance in the essentially truncated fourth quarter and January.

Suppliers often discuss information on their earnings calls that provides a better understanding of production rates at the OEMs and where downstream issues are or are emerging.

2025 remains another year for recovery in commercial aerospace

Subscription Required

By Scott Hamilton

Jan. 6, 2025, © Leeham News: Don’t look for any dramatic new product launches in 2025.

Nor should you expect any dramatic news, absent global upheaval of some kind.

Nor should you expect any dramatic news, absent global upheaval of some kind.

This year is going to be yet another year dominated by recovery. Recovery from the COVID-19 pandemic, which officially ended in 2022. Recovery by the supply chain. Recovery for Pratt & Whitney’s nearly decade-long problems with its Pure Power GTF engines supplying the Airbus A220, A320 family and Embraer E2 jets. Recovery by Airbus from its production and delivery delays. Recovery by Boeing from its series of self-inflicted crises, now beginning the sixth year.

There is just no getting around the fact that the commercial aerospace industry isn’t a smooth-running industry. It’s a long way from 2018, when all sectors were running smoothly. There is still a long way to go to recovery.

Here’s LNA’s take on what’s to come this year.

How Trump tariffs affected, and could affect, Airbus, Boeing and Embraer

By Scott Hamilton

Dec. 6, 2024, © Leeham News: President-elect Donald Trump vowed to immediately impose a 25% tariff on “ALL” imports into the US from Canada and Mexico, and 10% from China.

![]() Last week, he threatened to impose a 100% tariff on imports from the BRIC-aligned nations if they move away from the US dollar in international economics.

Last week, he threatened to impose a 100% tariff on imports from the BRIC-aligned nations if they move away from the US dollar in international economics.

The BRIC nations begin with Brazil, Russia, India, and China (the “BRIC” part of the group). Egypt, Ethiopia, Iran, South Africa, Iran, and the United Arab Emirates round out the group.

There is widespread criticism of the potential damage the Trump tariffs could impose on the US economy. The targeted countries would be certain to impose tariffs on US goods.

The impact could be significant for commercial aviation—and Boeing in particular. Before its repeated self-inflicted wounds began with the 2018/19 737 MAX crisis, which continues today, Boeing was by far the largest US exporter. Deliveries of its 7-Series airplanes outside the US helped balance the trade deficit the US usually has.

Before Trump’s first term, China was the largest customer for Boeing airplanes. Deliveries accounted for 25% or more of Boeing’s annual deliveries. After![]() Trump took office in 2017 and imposed tariffs on China, Beijing stopped ordering Boeing airplanes. China was the first country to ground the MAX after the two fatal accidents. It was the last to recertify the airplane. And there still remains a sizeable inventory of undelivered 737s awaiting Beijing’s approval for delivery, one by one.

Trump took office in 2017 and imposed tariffs on China, Beijing stopped ordering Boeing airplanes. China was the first country to ground the MAX after the two fatal accidents. It was the last to recertify the airplane. And there still remains a sizeable inventory of undelivered 737s awaiting Beijing’s approval for delivery, one by one.

Trump also imposed tariffs on Airbus imports into the US as part of the two-decade-long World Trade Organization (WTO) trade dispute between Airbus and Boeing.

However, imposing tariffs is a complicated process. LNA extensively reported on the WTO battle (see related articles). We explain this further below.

Related Articles

Leeham News articles:

- Boeing files trade complaint vs Bombardier with Trump Administration 4-27-17

- Boeing C Series trade complaint is no surprise 5-1-17

- Boeing-Bombardier trade complaint revisited 7-31-17

- Decision was expected, tariff is a shocker in Boeing-Bombardier case 9-26-17

- Assessing the impact of the Bombardier tariff decision 9-27-17

- No harm to Boeing, what happened and what’s next 1-26-18

- Insignificant impact from steel tariff 3-2-18

- China tariffs on Boeing airplanes unlikely 3-14-18

- Boeing yields on C Series tariff case; what’s next for Bombardier? 3-26-24

- Trump proposes tariffs on Airbus; EU likely to retaliate 4-9-19

- EU ready to instantly retaliate if US imposes tariffs in WTO case 9/29/19

- US imposed $22m in Airbus tariffs in 2019 3/3/20

- EU tariffs on Boeing airplanes in effect 11/16/20

- US to tax fuselage, wings, tail imported for Airbus’ Mobile plant 12/31/20

Engineering, Innovation is our DNA: Embraer

Subscription Required

By Scott Hamilton

Nov. 25, 2024, © Leeham News: Embraer’s revenues may be small compared to Airbus and Boeing.

Luis Carlos Affonso. Credit: Embraer.

But “under the hood,” the company is, in many respects, more innovative and aggressive in developing new airplanes.

Compared with Boeing, which in 2017 wanted to take over Embraer’s commercial airplane unit, Embraer is far more efficient and more dedicated to making safety and engineering the top of its culture.

Airbus hasn’t developed an all-new commercial airliner since the A350, launched in 2013. Boeing hasn’t launched an all-new airliner since the 787, launched in December 2003. Each has developed derivatives of existing products since then. Airbus launched the A330neo in 2014 and the long-range and extra-long-range versions of the A321neo. It added the Ultra-Long-Range model to the A350.

Boeing launched the 737 MAX derivative in 2011, the 747-8 in 2005, and the 777X and 787-10 in 2013.

Since 2000, Embraer developed and certified more than 20 aircraft types across its commercial, military, and executive product lines.

During the same period, Airbus launched the A320neo family in addition to those listed above. Boeing launched the KC-46A (a derivative of the 767-200ER) aerial tanker in 2011 and a few new military programs.

Credit: Embraer.

“One thing that is incredible at Embraer is the amount of new designs, new platforms that we have developed in the last 25 years. I don’t know any other company that has developed so many airplanes in this time frame,” Luis Carlos Affonso, Senior Vice President of Engineering and Technological Development, said during the Embraer investors’ day on Nov. 18 in New York.