Leeham News and Analysis

There's more to real news than a news release.

Boeing’s next airplane will eventually come; what will it be?

Subscription Required

By Scott Hamilton

Part 1

April 9, 2026, © Leeham News: CEO Kelly Ortberg has been clear: there won’t be any new airplane program launched until the airlines are ready, the technology is ready, and Boeing is ready.

Ortberg became CEO of The Boeing Co. on Aug. 8, 2024. One of his first decisions was to kill the research and development of a concept called the X-66A, the moniker for a Transonic Truss Brace Wing (TTBW) single-aisle airliner that could replace the 737 MAX in the coming decade.

However, he said that Boeing, coupled with NASA, would continue to research and develop an advanced wing for a new, highly efficient airplane. NASA, the National Aeronautics and Space Administration, has a long history of partnering with Boeing to evaluate new aerospace development.

Ortberg’s decision to kill the X-66A demonstrator project reversed a decision by the man he replaced, David Calhoun, who was the TTBW’s leading proponent within Boeing. Calhoun became CEO in January 2020 when his predecessor, Dennis Muilenburg, was fired during the prolonged 737 MAX crisis.

Figure 1. The Boeing-NASA concept X-66A TTBW airplane. Source: NASA.

One of Calhoun’s first decisions was to kill the R&D project of a New Midmarket Airplane (NMA), a twin-aisle design roughly the same dimensions as the Boeing 767-200ER and -300ER. The NMA had been under study since at least 2012. Muilenburg was on the path to seek board approval to launch this program in 2019, when the MAX was grounded by global regulators. Calhoun, the lead director, didn’t support the plane. With Boeing’s cash-cow 737 grounded, Calhoun used the crisis to kill the NMA. Given the billions of dollars in losses Boeing was and would incur, the decision was an obvious one.

Related Article

Boeing’s 30-year march to its next new airplane

Subscription Required

Open to All Readers

By Scott Hamilton

Background

April 6, 2026, © Leeham News: Depending on what starting point you want to choose, it will be up to 30 years between brand new, clean sheet airplane designs at The Boeing Co.

Boeing announced its 787 program in December 2003, with a formal launch the following spring. The entry-into-service goal for the 787 was May 2008. Boeing planned to design a replacement for the aging 737 platform after the 787 entered service. A new design for replacing the 777 was supposed to come after that.

The 787’s EIS date came and went as design and production problems added up to 3 ½ years of delay.

With cost overruns, deferred production, and deferred tooling costs totaling more than $50bn, plus several billion more dollars written off for research and development and abnormal production costs, the 787 still has more than $14bn in deferred costs to recover.

Delays and cost overruns hurt the 747-8 program. The 2019 21-month grounding of the 737 MAX resulted in billions more in charges. The January 2024 door plug blowout on a new Alaska Airlines 737-9 hurt recovery. Scrutiny by the Federal Aviation Administration (FAA) continues to this day. Production rates for the 737 and 787 are well below those that predate the MAX grounding. Certification of the 737-7, 737-10, and 777X remains a hope, not a reality, so far.

A plethora of losses, charges, and delays in defense and space programs added to the losses. Boeing’s long-term debt in 2018, its last normal year, was over $10bn. Today, it’s over $54bn, with big repayments coming soon.

Boeing’s next new airplane program remains years away.

What will Boeing’s next new airplane be? We have a pretty good idea. A new series beginning Thursday explores this question. Credit: Leeham News.

Reader Comments Open Forum, week of April 6

LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

Maintain civility and follow Reader Comment rules.

A new Open Forum will be posted weekly.

Bjorn’s Corner: Blended Wing Body Airliners. Part 4

By Bjorn Fehrm

April 3, 2026, ©. Leeham News: We have started a series of articles on the Blended Wing Body (BWB) as a potentially more efficient design for passenger-carrying airliners than the classical Tube And Wing (TAW) configuration.

In the third article last week, we saw that the large wing surface area of a Blended Wing Body does not come from cruise-phase requirements; it comes from the lift needed in the landing phase, where BWBs lack flaps to increase wing lift. It needs a large wing area to compensate.

Now we will see that the wingspan is not sized by cruise requirements but by takeoff requirements.

Figure 1. The JetZero Z4 BWB. Source: JetZero.

Boeing, once the king of freighters, falls behind Airbus going forward

Subscription Required

By Scott Hamilton and Bjorn Fehrm

April 2, 2026, © Leeham News: Boeing is no longer “freighter king.”

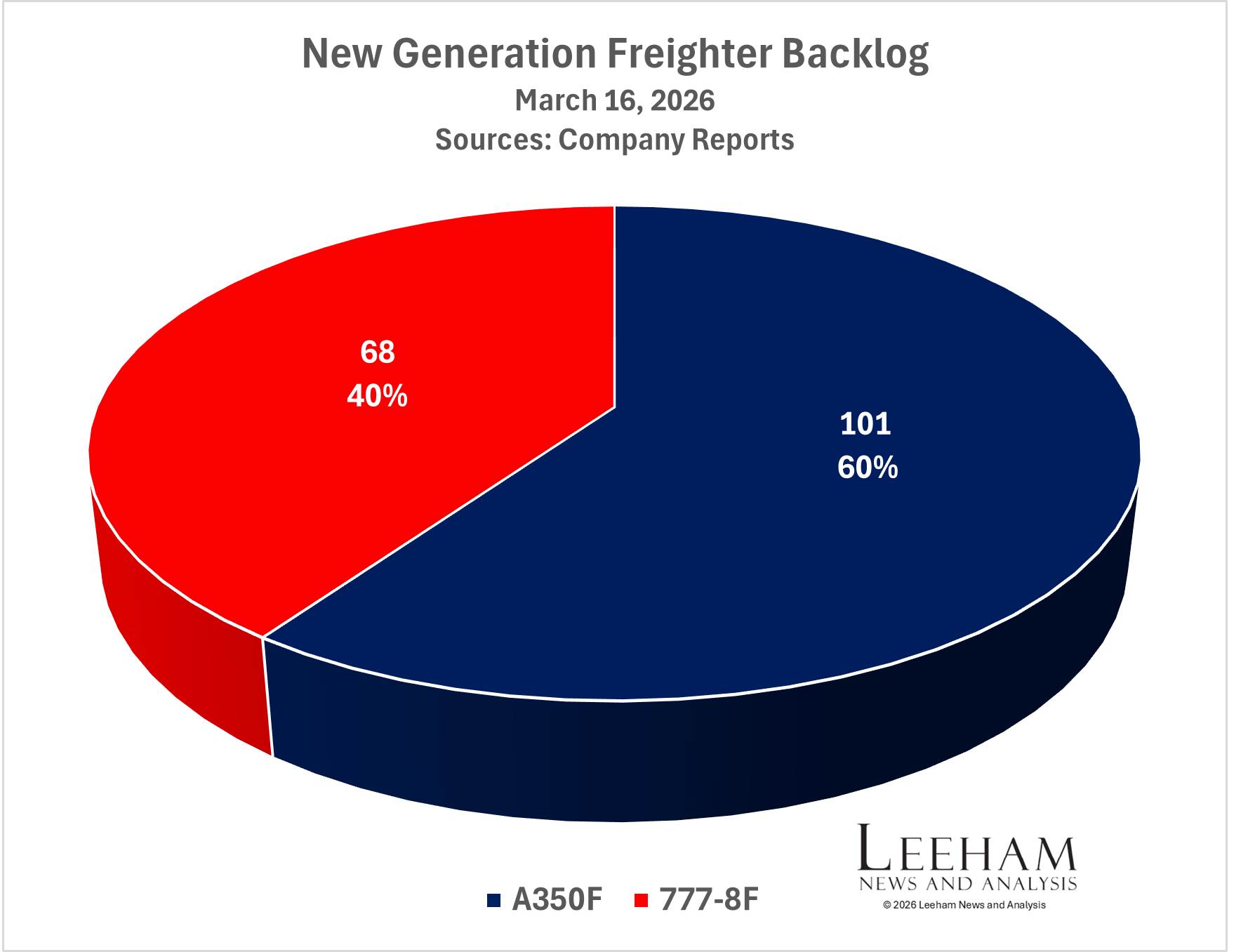

The March 16 order by cargo carrier Atlas Air for 20 A350Fs gives Airbus a 60% market share of orders for the next generation of freighters. Since the dawn of the jet age, Boeing has had a lock on jet airliner freighters. It vanquished Douglas Aircraft Co and its successor, McDonnell Douglas. Airbus had modest success with the new build A300-600F, with about 100 ordered. But Airbus bombed with the new production A330-200F; only 38 were sold.

Figure 1. The backlog of new generation freighter orders gives Airbus a 60% market share. Sources: Airbus, Boeing.

However, Airbus now has 101 orders for the A350F. Boeing has just 68 for the competing 777-8F. This is a far cry from the 359 777F Classics, based on the 777-200LR, that have been ordered. There are 47 in the backlog. Production will conclude at the end of next year due to emissions standards that the old generation 777F does not meet. Boeing asked the Federal Aviation Administration (FAA) for an exemption to build 35 more. It requested a decision by May 1.

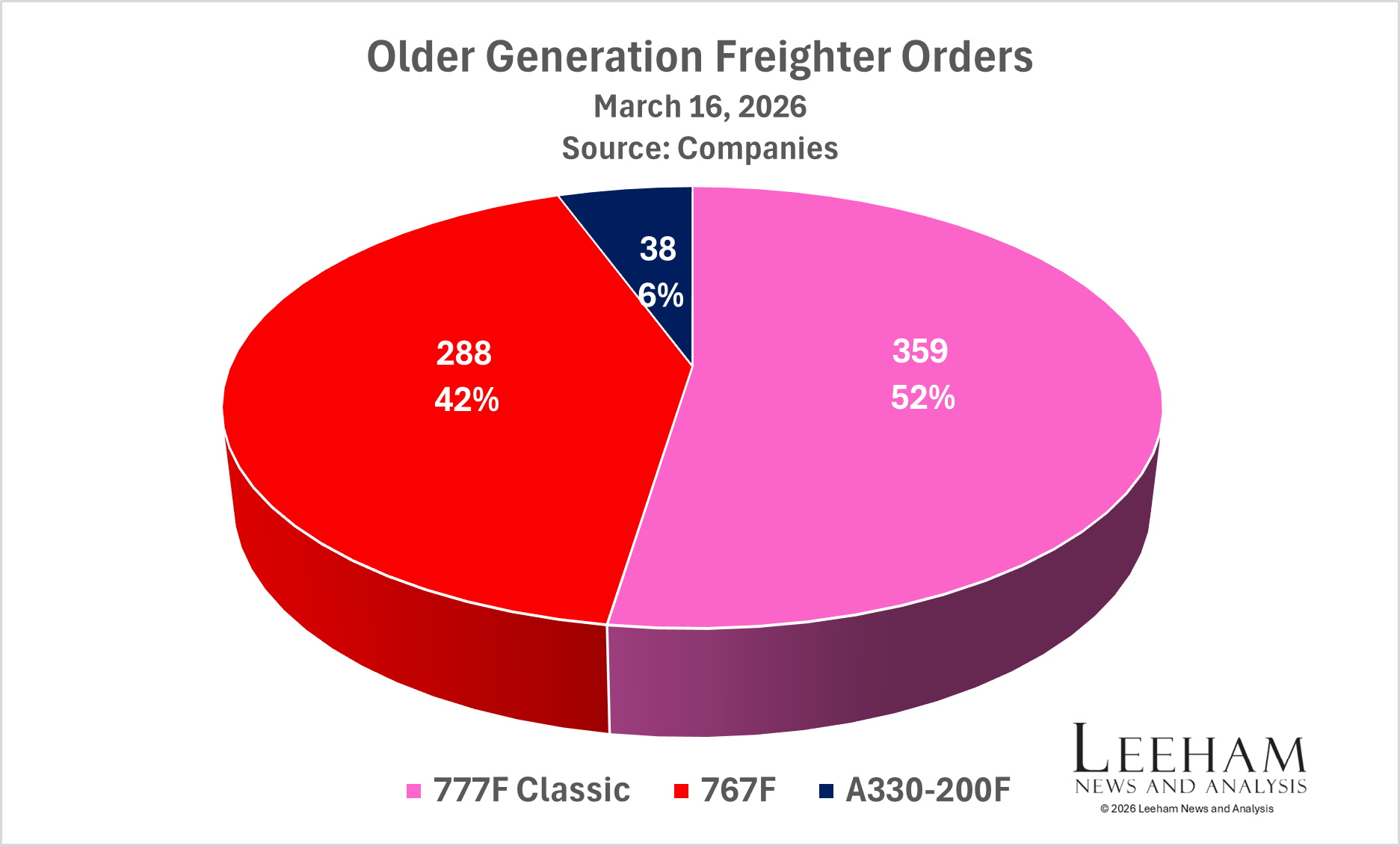

Figure 2. Boeing dominated the jet freighter market from the 1960s. The recent, old generation freighter market was still overwhelmingly owned by Boeing. Sources: Airbus, Boeing.

Additionally, Boeing sold 288 767-300ERFs. There are 18 in the backlog. Production concludes at the end of next year.

How did Boeing lose its overwhelming dominance in the freighter market? How did Airbus overtake Boeing, as it did in the early 2000s in the passenger airplane arena?

The answers about Boeing rest in a combination of negative fallout from the 737 MAX crisis, a suspension of production of the 787, shifting priorities and Boeing’s inbred arrogance.

For Airbus, the answer lies in the tortoise-and-hare analogy and a willingness to listen to potential customers more than Boeing did in key campaigns.

Who has authority to close US airspace–DOD, DHS or the FAA?

Figure 1. A Locust laser direct energy weapon, shown here mounted on an infantry squad vehicle, was used in the area near El Paso International Airport in February. Photo: US Army.

By Colleen Mondor

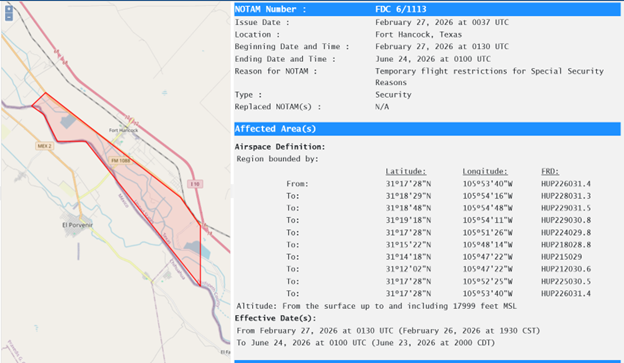

April 1, 2026, © Leeham News: On Feb. 26, the Federal Aviation Administration (FAA) announced another Temporary Flight Restriction (TFR) in southern Texas airspace. As it did two weeks prior when closing the airspace over El Paso International Airport and a portion of southern New Mexico, the agency cited “Special Security Reasons.”

Figure 2. Fort Hancock TFR #FDC 6/1113 courtesy tfr.faa.gov.

Within 24 hours of the new closure, which was centered on Fort Hancock, about 50 miles southwest of El Paso, multiple media outlets reported that the TFR involved operations of the Customs and Border Protection Service (CBP) and were not coordinated with the FAA. The Fort Hancock closure, coupled with a recent report of the military’s plans to possibly fire lasers near Reagan National Airport, has reinforced concern over the FAA’s control of the national airspace, a task with which it has been legally mandated by Congress since its 1958 inception.

Who Controls the Movement of the Aircraft?

By R. Michael Baiada

ATH Group, Inc.

Special to Leeham News

Michael Baiada.

March 31, 2026, © Leeham News: “We’ll tell you where we want you to be in three dimensions…and we’ll tell you where we want you to be to hit that top of descent mark to [meet] the constraints of the runway.”

Bryan Bedford. Credit: Federal Aviation Administration.

Bedford believes telling airlines/users how to operate their aircraft is a good thing. As a 45-year pilot (USAF, United Airlines, and business jets), with decades of airline operational and ATC expertise, I do not agree. If implemented, FAA’s plan will increase airline costs and reduce airline quality.

In fact, airlines and FAA need to switch this around to where airlines/users do the telling and FAA/ATC does the listening.

Next, the FAA’s $31.5 Billion Brand New ATC System (BNATCS) will not reduce airline delays since it fails to focus on the root cause of delays (random Point Overloads). That said, BNATCS is a positive for equipment replacement, which is needed.

Even worse for airlines/passengers, as currently planned, the BNATCS ATC Centric Flow Management plan will, as Bedford’s statement above shows, further institutionalize ATC’s decades old process of control over the movement of the airline’s/user’s aircraft. This will haunt the airline’s “day of” operation for decades into the future, eliminating any chance of airlines achieving “day of” Operational Excellence.

Think about it. Who wants a government agency to control their primary production asset, or who believes a government agency can make an airline’s operation efficient? No one.

Boeing’s Starliner history shows safety, quality concerns exist systemically across the company

Editor’s Note: The National Aeronautics and Space Agency (NASA) on Feb. 19 released its investigative report of the failures in 2024 of the Boeing Starliner space vehicle. Defects in the Starliner resulted in its crew being housed in the International Space Station for nine months before being returned to earth in a SpaceX capsule.

Boeing Starliner, docked at the International Space Station. Source: Boeing.

The investigation into the failures faulted NASA and Boeing. The 311 page report was triggered by the Starliner incident, and examines the NASA-Boeing Defense, Space and Security (BDS) cultures that led to the Starliner problems. The Boeing Co. is engaged in high profile efforts to change the culture at Boeing Commercial Airplanes (BCA). The Starliner incidents reveal similar cultural and safety issues at BDS that corporate CEO Kelly Ortberg must address.

The NASA report may be downloaded here: nasa-Starliner report 021926

In this Special Report, LNA dissects the NASA study. The shortcomings at BDS are eerily similar to those at BCA.

Special Report

By the Leeham News Team

Three Disasters

Lion Air and Ethiopian Airlines

The first Boeing 737-8 delivered, in May 2017, which happened to be to Lion Air. Source: Leeham News.

March 30, 2026, (c) Leeham News: On Oct. 29, 2018, Lion Air Flight 610—a Boeing 737 MAX 8—crashed into the Java Sea, killing all 189 aboard. The Maneuvering Characteristics Augmentation System (MCAS), a flight control system that Boeing had withheld information about from airlines and the Federal Aviation Administration (FAA)—including its existence and how it works—drove the aircraft into an unrecoverable dive.

The pilots had never been trained on it because Boeing determined that disclosing MCAS would require simulator training, which would make the MAX less competitive against the Airbus A320neo. Southwest Airlines, for example, which ordered hundreds of MAXes, required Boeing to pay $1m per airplane if simulator training was required.

Less than five months later, on March 10, 2019, Ethiopian Airlines Flight 302 crashed under virtually identical circumstances. It was another MAX 8 with another MCAS-driven dive. Another 157 people were killed. Combined death toll: 346 passengers and crew, plus one recovery diver in the Lion Air accident. The global fleet was grounded for 21 months.

Congressional investigations revealed what investigators called Boeing’s “culture of concealment” and the FAA’s systematic overreliance on Boeing’s Organization Designation Authorization (ODA) for self-certification. While federal government agencies routinely designate company employees to represent the overseeing agencies, the level of the FAA’s hand-off to Boeing came under withering criticism.

Following the long recovery period, the FAA clamped down on Boeing’s production of the 737 and to a lesser extent (and for different reasons), production of the 787. By late 2022, Boeing executives appeared confident that BCA was on the path to normal operations.

Open Forum, Week of March 30

LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

Maintain civility and follow Reader Comment rules.

A new Open Forum will be posted weekly.

Fuel prices up sharply, but not sustained at record levels–yet

Subscription Required

Now open to all readers

By Scott Hamilton and Karl Sinclair

March 28, 2026, © Leeham News: Oil prices skyrocketed this month with the beginning of the 2026 Iran War.

Yet, as sharply as prices spiked, they are not yet a record relative to inflation-adjusted prices since the 1973-1974 OPEC-inspired oil embargo and other regional or global events, an analysis by LNA shows.

West Texas Intermediate Crude oil prices topped $100/bbl. Brent crude briefly hit $197/bbl on March 20. On March 27, Brent topped $100.

Some airlines worldwide hedged fuel against dramatic price hikes. Our detailed analysis is below.

There are dire predictions that the prices could reach $170 or even $200/bbl if the Iran War continues. Bombing of Iran by the United States and Israel began on Feb. 26. Shortly after, tanker traffic through the Strait of Hormuz all but ceased. Twenty percent of the world’s oil transits through this bottleneck. Some countries, such as Japan and China, obtain more than 90% of their oil via the Strait.

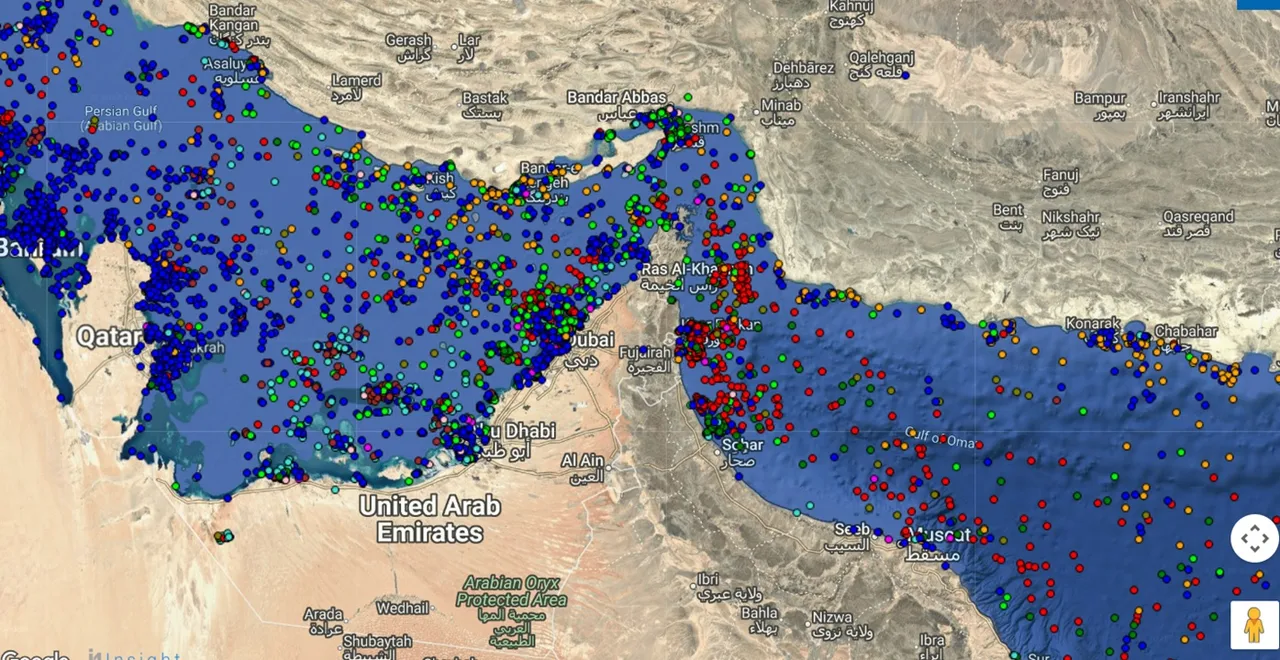

More than 300 tankers are trapped. Some were attacked by Iran. Hundreds of ships of all kinds are blocked on both sides of the 35-mile-wide Strait.

Figure 1. Source: About 750 ships were trapped at the peak. Iran is allowing limited traffic through. Seatrade-Maritime magazine.

The price of oil is being whipsawed as President Donald Trump mixes messages about the war’s progress, sometimes within minutes. Sometimes the war is “won,” but more troops and ships are being sent to the region. Trump threatened to increase bombing, attack Iran’s power stations, invade an island, and then take it back. Allies are needed to reopen the Strait, and then they are not.