Leeham News and Analysis

There's more to real news than a news release.

Fourth EU Clean Aviation funding proposal recognises hydrogen’s upcoming importance

Subscription Required

By Charlotte Bailey

Feb. 3, 2026, © Leeham News: The European Union co-funded Clean Aviation project has announced its fourth call for proposals, with an initial draft set to be followed by a formal version issued this month.

The upcoming call will provide up to €329.5m ($386m) in EU funding for disruptive new aircraft technologies, providing an estimated €824m ($966m) when combined with input from the private sector.

Speaking at the November 2025 Sustainable Aero Lab’s Future Aviation Festival in Amsterdam, EU Clean Aviation executive director Axel Krein explained that the next round will focus on technologies applicable to short-to-medium range aircraft, including regional aircraft architectures.

Speaking at the November 2025 Sustainable Aero Lab’s Future Aviation Festival in Amsterdam, EU Clean Aviation executive director Axel Krein explained that the next round will focus on technologies applicable to short-to-medium range aircraft, including regional aircraft architectures.

These will be augmented by the development of “transverse activities” (such as applicable certification standards) and other complementary “fast track areas.” The largest of five separate funding streams will be allocated to the development of ‘Ultra-Efficient Short to Medium Range (SMR)’ aircraft, with €130m ($114m) split across five projects.

The research and technology roadmap focuses on demonstrators up to ground testing, “addressing all key technologies,” states the proposal. This will validate the performance of technologies up to Technology Readiness Level (TRL) 6.

Flight demonstrations could also be used to validate testing “in realistic operational conditions.” Clean Aviation expects to complete a flight test demonstrator configuration freeze by the end of 2026 to support the start of flight testing by the end of 2029. A hybrid-electric Ultra-Efficient Regional Aircraft has been proposed as the baseline concept for this 50-100 passenger regional aircraft. Clean Aviation will also award €40m ($46m) for the development of an “advanced airframe for ultra-efficient regional aircraft.”

Net Zero by 2050 is beyond reach, but R&D, SAF work continues

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Feb. 2, 2026, © Leeham News: When the International Air Transport Assn. (IATA) adopted its carbon Net Zero by 2050 policy at the October 2021 Annual General Meeting, it included milestones for increasing the use of Sustainable Aviation Fuel (SAF). The outline also included the adoption of alternative energy technologies like hydrogen, batteries, and hybrids.

Tim Clark, president of Emirates Airline. A voice of reality when it comes to eco-aviation. Credit: Emirates Airline.

Some, including LNA, quickly concluded that the timeline and some of the technologies were unachievable. Tim Clark, the president of Emirates Airline, attended the IATA AGM. Don’t make promises you can’t keep, he told the assembly.

Since then, airlines across the globe have relaxed or even abandoned the IATA goals for their internal efforts.

SAF remains an elusive alternative. So does hydrogen. Battery-powered eVTOLs appear just around the corner for certification. However, developers of battery-powered commuter and regional airliners hit the reality that the weight of the batteries needed for even flights of a few hundred miles weighs more than is feasible. Some hybrid technologies appear to have promise, yet likely are technologies that appear to have promise for certain aircraft architectures, but need higher-performance batteries, which pushes these into the next decade.

Still, Europe continues to place a priority on sustainable aviation. Airbus, engine manufacturers and key suppliers continue their drive toward more sustainable aviation. However, Airbus backed off its 2035 target for a hydrogen-powered airplane. Rolls-Royce, key engine supplier MTU, and components supplier GKN, and others, strive for improving fuel efficiency and reducing emissions. Safran, a partner with GE Aerospace in the 50-50 joint venture CFM International, and an interiors manufacturer, likewise seeks environmental improvements to their products.

Related Article

In Asia, China is making a big bet on eVTOLs (and solar and automobile electric power). Its eVTOL industry is already flying in China. The country is the biggest producer in the world of solar panels and high-performance battery cells. China’s auto industry has a line-up of electric cars from small to luxury based on its battery technology.

Open Forum, Week of Feb. 2

Feb. 2, 2026: LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

Feb. 2, 2026: LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

Maintain civility and follow Reader Comment rules.

A new Open Forum will be posted weekly.

Singapore Air Show coverage begins Feb. 3 (local time)

Feb. 1, 2026, © Leeham News: The Singapore Air Show begins on Feb. 3 local time (Feb. 2 in the US and Europe). LNA’s sister publication, AIN, is on site and will be reporting from the show. LNA will pick up selected stories.

Feb. 1, 2026, © Leeham News: The Singapore Air Show begins on Feb. 3 local time (Feb. 2 in the US and Europe). LNA’s sister publication, AIN, is on site and will be reporting from the show. LNA will pick up selected stories.

AIN’s coverage already is underway with some pre-show posts:

Flash: SPEEA union at Boeing Wichita OKs new contract with 85.8% voting yes

![]() Jan. 30, 2026, (c) Leeham News: Members of the engineers and technicians union at Boeing Wichita (the former Spirit AeroSystems plant) approved a 4.8 year contract 85.8% to 14.2%.

Jan. 30, 2026, (c) Leeham News: Members of the engineers and technicians union at Boeing Wichita (the former Spirit AeroSystems plant) approved a 4.8 year contract 85.8% to 14.2%.

“The contract was approved by a 671 to 111 vote of dues-paying members of SPEEA’s Wichita Technical & Professional Unit (WTPU),” the union announced tonight.

“The average WTPU-represented worker will be making more than $117,000 a year when this contract is done in 2030. In addition, we’ll see significant improvements to our health care benefits with lower premiums, we’ll have more days off from work and we’ll have a higher incentive pay target,” the union said in a press release. Union negotiators unanimously endorsed the Boeing offer.

Bjorn’s Corner: Faster aircraft development. Part 25. The Difference between Continuing and Continuous Airworthiness.

By Bjorn Fehrm

January 39, 2026, ©. Leeham News: We have done a series about ideas on how the long development times for large airliners can be shortened, while at the same time describing all the regulatory work that must be done, regardless of work practices.

It’s now time to sum up what we have looked at in terms of speeding up the development of a Part 25 Air Transport airliner in the 200-seat segment. But before we do that, we will look at what an operator of the aircraft we have delivered will have to do to qualify it for operation with its local regulator.

For an operator to operate our aircraft, Continued Airworthiness, as described in last week’s article, is not enough; the Operator must add what can be called Continuing Airworthiness. These words are close but not the same, and there is a substantial difference in what’s behind them.

Rolls-Royce 2026 Outlook: It’s back in large engines; can it get back into the Single Aisle as well?

Subscription Required

By Bjorn Fehrm

January 29, 2026, © Leeham News: Rolls-Royce has posted a string of increasing profits over the last few years after a tough period that  started in 2017, when its Trent 1000 engines on ANA’s Boeing 787s developed a turbine-corrosion problem, cutting time on wing to a fraction of what it should be. These turbine problems escalated into a global issue, affecting all Trent 1000-equipped 787s.

started in 2017, when its Trent 1000 engines on ANA’s Boeing 787s developed a turbine-corrosion problem, cutting time on wing to a fraction of what it should be. These turbine problems escalated into a global issue, affecting all Trent 1000-equipped 787s.

The Trent 1000 on Boeing’s 787 has since experienced a series of problems, beginning with the need to replace turbine blades, followed by compressor vibration that required replacing blades on the intermediate compressor. Engines must be removed from the wing to remove the turbine and compressor blades during engine overhaul, resulting in Rolls-Royce Trent-equipped 787s being grounded for periods.

The result has been a dwindling market share for the 787, with the competing engine OEM, GE, now claiming an 78% market share for its GEnx-1B engine, and charges to the business for the cost to fix the problems for the airlines.

The drama surrounding the 787 was not expected. The Rolls-Royce RB211-535 had been the best engine on the Boeing 757 (versus Pratt & Whitney’s PW2040), and on the Airbus A330, the Trent 700 has a dominant market share versus GE’s CF6 and Pratt & Whitney’s PW4000, as it offers solid performance and maturity.

To add to injury, a former management had decided that the Single Aisle market was too small a fish for Rolls-Royce and exited the cooperation with Pratt & Whitney for the A320/A321 V2500 in 2011. The aftermarket income from spares for the V2500 began to decline as the Trent 1000 kept 787s on the ground and COVID-19 hit. When COVID hit in 2020, Rolls-Royce struggled with losses because of these engine problems and strategic mistakes.

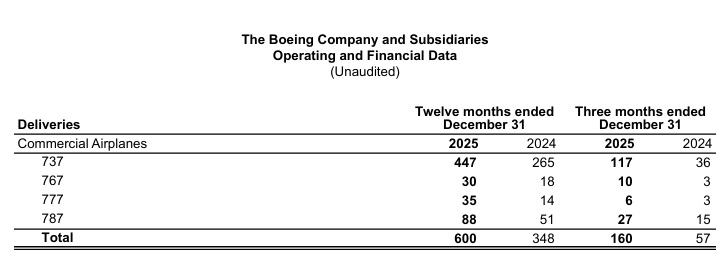

Boeing FY2025: Company posts small profit on Services division; BCA still losing money

By Karl Sinclair

Jan. 27, 2026, © Leeham News: The Boeing Company (BA) released its full-year 2025 results, and indications are that the company is headed in the right direction. However, some monumental tasks face the corporation in the short-to-medium term.

Jan. 27, 2026, © Leeham News: The Boeing Company (BA) released its full-year 2025 results, and indications are that the company is headed in the right direction. However, some monumental tasks face the corporation in the short-to-medium term.

Boeing Commercial Aircraft (BCA) is still in a loss-making position. BCA lost $7bn, compared with $8bn in 2024. Boeing Defense, Space and Security (BDS) was near break-even. Boeing Global Services (BGS) was the only profitable division, boosting the corporation to an annual profit on the back of the $10.6bn sale of part of its business.

BCA delivered 160 aircraft during 4Q2025, including 117 of the cash-cow 737 MAX series and 27 Dreamliners.

This boosted BCA revenues in the final quarter to $11.379bn, up from $4,762bn, year-over-year (YoY). Full-year revenues hit $41.494bn, almost doubling 2024 sales of $22.861bn.

Source: All tables and images via Boeing.

The company is adamant about demonstrating stability in production and the supply chain at rate 42/mo, before making the leap to 47/mo by mid-2026.

787 rates are expected to stabilize at 8/mo, as investments in the Charleston (SC) production facilities begin to take shape, boosting output into the double digits in 2026.

RTX 2025 Earnings: Commercial Aerospace Leads Growth as Pratt Advances GTF Recovery

By Chris Sloan

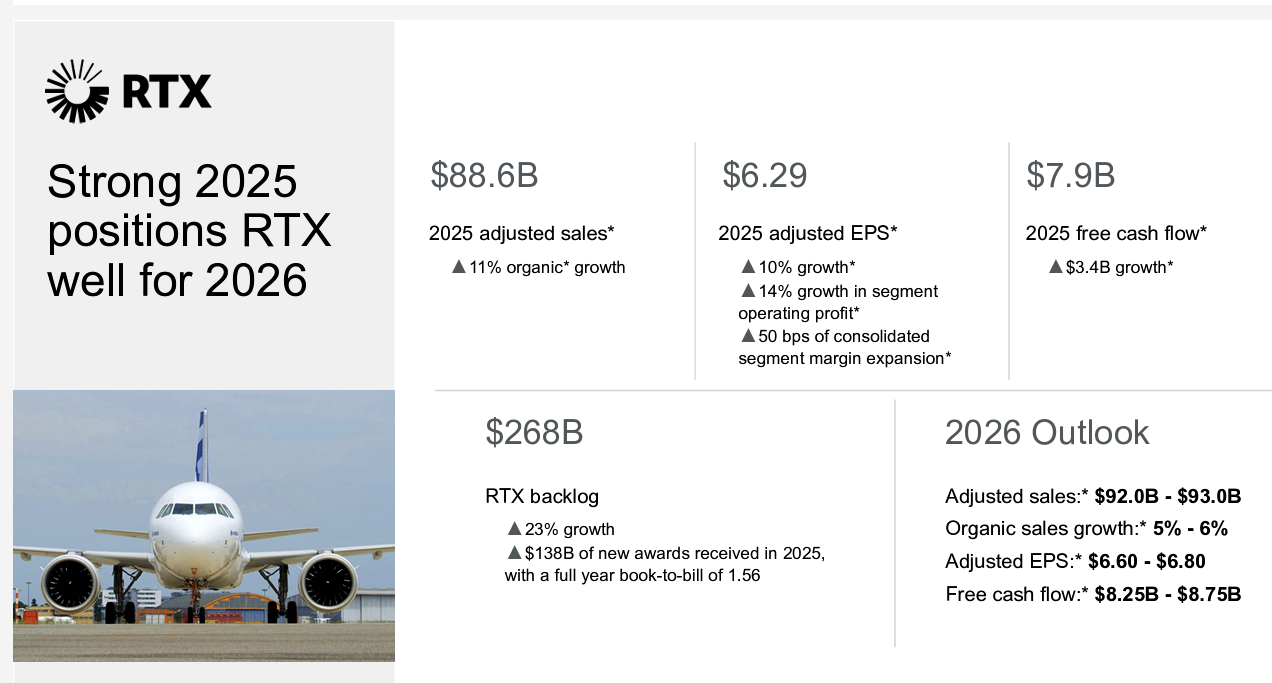

![]() Jan. 27, 2026 © Leeham News: “RTX is constructed to meet the moment—by the moment I mean the ramp both in defense and commercial—and to drive long-term value for customers and shareholders,” RTX President and Chief Executive Officer Christopher Calio said as the company closed 2025.

Jan. 27, 2026 © Leeham News: “RTX is constructed to meet the moment—by the moment I mean the ramp both in defense and commercial—and to drive long-term value for customers and shareholders,” RTX President and Chief Executive Officer Christopher Calio said as the company closed 2025.

The company has strong order momentum and a record backlog, driven by commercial aerospace demand and continued progress at Pratt & Whitney as the company works through the Geared Turbofan (GTF) powder metal issue.

RTX ended the year with a full-year book-to-bill of 1.56 and a $268bn backlog, up 23% year over year, including $161bn of commercial orders and $107bn of defense awards. Commercial backlog rose 29%, supported by higher aircraft production rates and resilient passenger air travel, while organic growth was led by commercial OE and aftermarket.

At Pratt, management emphasized improving performance as the GTF program continues to grow and newer contracts begin to reshape the business. Chief Financial Officer Neil G. Mitchill Jr. said Pratt is “growing out of the older contracts,” with improved pricing on new work and legacy businesses remaining intact, positioning the segment for margin expansion over the next several years as backlog is executed.

Looking ahead, RTX outlined several areas that will shape results in 2026 and beyond, including continued improvements in GTF fleet management, rising MRO output, and the transition to the GTF Advantage engine. Management also pointed to alignment with OEM production ramp-ups, continued improvement at Collins Aerospace, and increased focus on defense output and capital deployment following recent comments from the Trump Administration, framing the company’s outlook as it balances near-term execution with longer-term growth across commercial and defense markets.

RTX Q4 and FY 2025 Earnings Call Slide Image: RTX

Open Forum Week of Jan. 26

Jan. 26, 2026: LNA’s Comments Open Forum allows Readers opportunities to comment about any post (note, we said “Post”, not any “Topic”). All comments will be held for review and Moderation per our new policy. The Open Forum enables Readers to Comment on paywall articles (to the extent the paywall preview is open to all readers).

Maintain civility and follow Reader Comment rules.

A new Open Forum will be posted weekly.