Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: Embraer reports weak quarter; MRJ FTV #1 assembly; JAL, ANA politics

Embraer’s Third Quarter: Embraer delivered fewer commercial airplanes in the third quarter than had been expected. The maker of E-Jets and the E-Jet E2 re-engined versions due beginning in 2018 listed its deliveries and backlog in its press release. Analysts expects 22 E-Jets would be delivered in the quarter. But the backlog is up 44% year-over-year, largely on the strength of the launch of the E2 (150 orders, 100 of which are for the smallest E-175 E2 and 25 each for the E-190/195 E2), and orders from Republic Airways Holdings and SkyWest Airlines for the current generation of E-Jets. The E-175 remains to most frequently-ordered airplane.

Although Embraer is expanding the size of the E-195-E2 by up to 12 seats, orders have been few. The E-190 has proved a better-selling model than the E-195.

Source: Embraer

Officials expect to have a healthy fourth quarter delivery stream.

Mitsubishi MRJ: Assembly for the first Mitsubishi MRJ Flight Test Vehicle (to borrow Bombardier’s term for the CSeries) is underway. The first delivery was originally planned for this year; it’s now planned for 2017, four years late. This rivals Boeing’s 787 and exceeds the Airbus A350 and as yet the CSeries.

JAL, ANA Politics: Reuters has an analysis about the suspicion politics may have been involved in the decision by Japan Airlines to buy the Airbus A350 and the pending order by ANA of an Airbus or Boeing airplane.

Odds and Ends: ANA, Airbus and Boeing; Era of the jumbo jet; Repo wars

ANA to stay with Boeing? After losing Japan Airlines to Airbus, analysts are split over whether ANA will also defect. Some say JAL’s order will give ANA cover to defect. Others say JAL’s order will increase the pressure on ANA to stay with Boeing. The Seattle Times this story. Our take: compare this with what happened following American Airlines’ order with Airbus. The Delta Air Lines competition was next, and Boeing was determined not to lose that competition–and it didn’t. Market talk says Boeing’s price to Delta was 10%-15% below Airbus’ offer, though this has never been confirmed. We understand there were other considerations besides costs. Regardless, both sides are going to go all-out to win.

SuperJumbo Era: The Financial Times has a story about whether the era of the super-jumbo (the Airbus A380 and the Boeing 747-8) is over (free registration required). Bloomberg has a story about the Boeing 777X being a jumbo killer.

Repo Wars: Here’s an departure from our usual coverage–tactics used to repossess an airplane from a delinquent airline. A decade ago, we were involved in a similar situation, planning the repossession of a Boeing 767-300ER from a South American airline. The lessor obtained a court order while we did some behind-the-scenes plotting to “arrest” the airplane at Miami. It was at the gate, full of passengers when the sheriff served the pilot with the court papers. Secrecy was imperative, as the story linked above references. Once the airplane was seized, the airline rescheduled a second 767 to stay on domestic service so the lessor couldn’t seize that airplane, too.

Low Cost Carriers dominate Top 10 single aisle customers at Airbus, Boeing

Low Cost Carriers (LCCs) dominate the backlog of the Top 10 single-aisle customers for Airbus and Boeing, data from the two OEMs show through August.

The importance of LCCs to the OEM backlogs has been increasing during the past decade, as has been the shift over the past 20 years from a dominance by US airlines to non-US carriers.

The backlog of LCCs today demonstrates the shift toward this sector as well as the shift toward non-US airlines.

|

|

Boeing 737 (All Models) |

|

|

|

Airbus A320 (All Models) |

|

||

|

1 |

Southwest |

317 |

18% |

|

1 |

Air Asia |

351 |

21% |

|

2 |

Lion Air |

313 |

17% |

|

2 |

Lion Air |

234 |

14% |

|

3 |

American |

187 |

10% |

|

3 |

Indigo |

196 |

11% |

|

4 |

Ryanair |

175 |

10% |

|

4 |

ILFC |

165 |

10% |

|

5 |

United |

172 |

10% |

|

5 |

Lufthansa |

146 |

9% |

|

6 |

Norwegian |

162 |

9% |

|

6 |

easyJet |

145 |

8% |

|

7 |

Air Lease |

151 |

8% |

|

7 |

American |

130 |

8% |

|

8 |

GECAS |

120 |

7% |

|

8 |

Qantas |

129 |

8% |

|

9 |

Delta |

100 |

6% |

|

9 |

Spirit |

115 |

7% |

|

10 |

GOL |

99 |

6% |

|

10 |

Norwegian |

100 |

6% |

|

|

August 2013 |

1,796 |

|

|

|

August 2013 |

1,711 |

|

|

|

LCC Total |

1,066 |

59% |

|

|

LCC Total |

1,141 |

67% |

Sources: Airbus, Boeing

For Boeing, 59% of the Top 10 single-aisle order backlog is with LCCs–more than 1,000 737NGs and MAXes. Over at Airbus, the dominance of LCCs is even greater: 67% for all A320 family members, including ceos and neos.

As we reported last week, Asia’s LCC, Lion Air has more firm orders for single-aisle aircraft than any other customer: 547. Lion Air is said to be planning to place an order as early as year end for a “double-digit” number of Bombardier CSeries. The next closest: the USA’s Southwest Airlines, at 317 737s, and American Airlines, with a combined 317 from Airbus and Boeing.

Europe‘s Norwegian has a combined 262 single-aisles on order from the two OEMs.

The dominance of LCCs in the backlogs reflect the changing nature of the airline industry, both in terms of service demand but also with the increasing growth in developing nations, with major growth coming out of Asia–the domain of Lion Air and AirAsia.

It also reflects the strategy of flipping aircraft around the end of the maintenance holidays in six or seven years after delivery, which may be a decent strategy for the airline but one which hazards lease rates and residual values and a potential imbalance of supply-and-demand at that sixth or seventh year. With a much greater reliance on LCCs than Boeing, Airbus’ A320s are most at risk on the RVs and lease rates.

Airbus sequence shift of A350s coming, reports customer. Airbus says ‘no’

Airbus will likely shift the sequence of the entry-into-service of the A350, a customer tells us. Other sources report the same, with another customer calling the prospect of a shift “inevitable.”

A tantalizing clue may have come from Airbus CEO Fabrice Bregier. In Airbus’ own video of Bregier talking about his first ride on the A350, he remarks at 3:10 into the video that the next effort is for “the development of the next member of the family, the -1000.” The subtitles alter this to the next “challenge,” but Bregier’s words can clearly be heard. The Youtube post is below, which is the same as the video on the Airbus website.

[youtube=http://www.youtube.com/watch?v=J6yX-1ESX88&w=420&h=315]

Right now, only one A350-800 is scheduled for delivery in September 2016 (to lessor ILFC), according to one data base, with several more following in 2017–when the more popular A350-1000 is scheduled to enter service.

But Airbus’ media relations department says no re-sequence has been made.

“No change in sequence A350-900 EIS H2 2014, A350-800 EIS mid-2016 and A350-1000 mid-2017,” says a spokesperson.

“The video you refer to was intended first and foremost for internal audiences, and Fabrice was referring to the development effort for the -1000 being the next priority as the -800 is a shrink so less effort than the -1000.”

The -800 is a straight-forward derivative of the -900, with several frames removed from the fuselage. The -1000 has some changes to the wing and a slightly different engine fan diameter than the baseline -900.

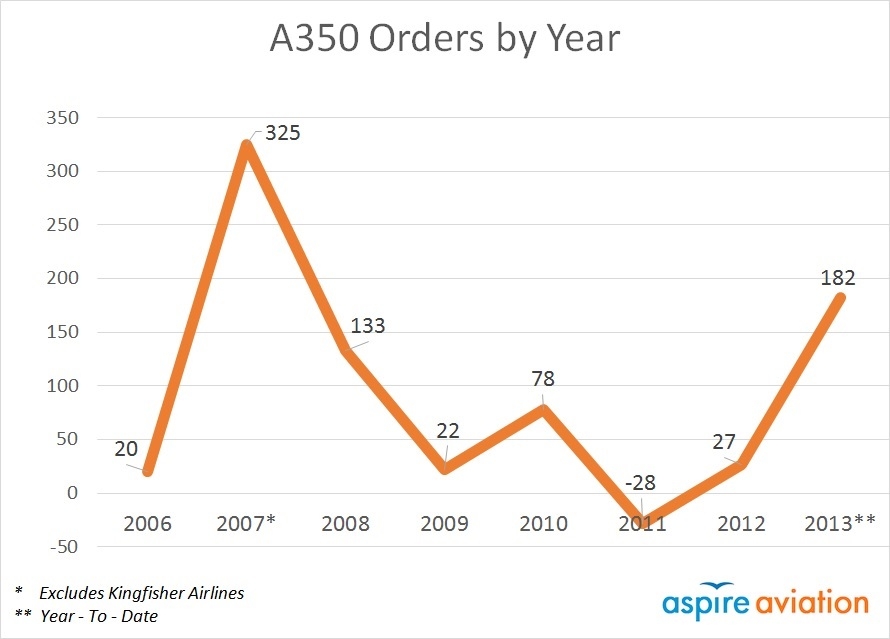

Analyzing A350 backlog: special to Leeham News and Comment

Special to Leeham News and Comment:

Vinay Bhaskara of Aspire Aviation has provided the following analysis of the A350 XWB sales, on a variety of metrics, exclusively to us.

Analyzing the A350 Backlog

With the recent order for 31 A350s from Japan Airlines, we thought it would be instructive to take a look at the A350’s backlog. To date, the A350 has won 759 orders from 39 different customers (we are excluding Kingfisher Airlines in India and its order for five A350-800s – Kingfisher has been shut down for more than a year now, and it’s chances of re-starting appear bleak).

After slow sales in 2011 and 2012, 2013 has been an excellent rebound year for the A350, its second best behind 2007, with 182 orders to date. We expect South African Airways to place its delayed order for the A350s by the end of the year, and there are several upcoming fleet replacement decisions, most notably at ANA and Qantas, in which the A350 is a major player. The chart below shows A350 orders by year since it launched:

Digging further into the backlog, the following two charts discuss the geographic breakdown of the A350’s orders. Asia and the Middle East currently account for more than 55% of the program’s orders, and it has made limited inroads in the Americas relative to the 787.

.

Odds and Ends: ANA to be battle royale; Boeing’s top salesman; Delta and the A380

All Nippon Airways Wide-Body Battle: Having lost a bombshell order to Airbus at Japan Airlines, the focus in Japan now turns to ANA, reports Reuters. Will Boeing shift work from Japan? Reuters has this story.

Boeing’s Top Salesman: Jon Ostrower has a very interesting and candid story about Boeing’s top airplane salesman, John Wojick, and the 787 program. Via Google News in a new Wall Street Journal format, it looks like it’s not behind the paywall.

Delta and the A380: Delta Air Lines flies the Boeing 747-400 but it doesn’t look like it will fly the Airbus A380. See this story by Motley Fool.

Backstory on the JAL deal from Bloomberg; ‘Boeing blew JAL, others’ says Aboulafia

Japan Airlines deal: Two items of note came across our desk concerning the Japan Airlines’ order from Airbus for the A350-900/1000. The first is from Bloomberg, which has an interview with Airbus CEO Fabrice Bregier. Lots of speculation exists that JAL ordered the A350 because of the problems with the Boeing 787. While this may have played a role at some level, Bloomberg reports that Bregier began his efforts prior to the JAL 787 fire in January.

The other is the October newsletter from Richard Aboulafia of The Teal Group that takes Boeing to task for essentially blowing the opportunity to retain JAL’s business for the 787-10 and/or the 777X. At this writing, Aboulafia hasn’t uploaded his newsletter to his website (so keep checking). In a nutshell, Aboulafia raps Boeing management for dithering on both airplanes. Had Boeing authorized the 777X six months ago, Aboulafia writes, Boeing could have kept IAG (British Airways) and if launched in 2012, Cathay Pacific could have been kept.

Aboulafia also predicts JAL’s rival, ANA, will buy the A350. Otherwise it will be at a competitive disadvantage, he writes. The newsletter is quite harsh.

Latest twin-aisle orders shift market share; Plus Odds and Ends

The flurry of orders in September and this month from Lufthansa Airlines and Japan Air Lines tightens the wide body race between Airbus and Boeing.

Airbus and JAL on Monday announced a firm order for 31 A350s and options for 25 more. Last month, Lufthansa announced a firm order for 34 777-9Xs and 25 A350-900s.

Sources: Airbus and Boeing

Sources: Airbus and Boeing

Airbus traditionally has significantly trailed Boeing in the twin-aisle sector, but so far this year the race is running about even through September. The Lufthansa orders for the Boeing 777-9X and the Airbus A350-900, announced in September, are not reflected yet, nor is the Japan Air Lines order for A350-900s and -1000s. None of these orders has been booked yet by either OEM. Airbus would take the lead.