Leeham News and Analysis

There's more to real news than a news release.

Fundamentals of airliner performance, Part 2.

By Bjorn Fehrm

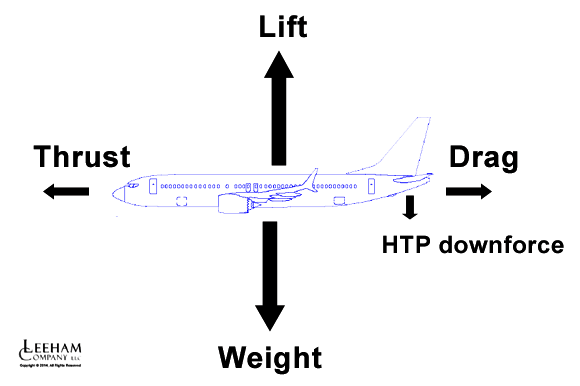

In our first article on how to understand the fundamentals that make up airliner performance we defined the main forces acting on an aircraft flying in steady state cruise. We used the ubiquitous Boeing 737 in its latest form, the 737 MAX 8, to illustrate the size of these forces. ![]()

Here a short recap of what we found and then some more fundamentals on aircraft’s performance, this time around the engines:

When flying steady state (Figure 1) we only need to find the aircraft’s drag force to have all important forces defined.

Figure 1. Elementary forces acting on an aircraft at cruise. Source: Leeham Co.

The lift force is given as equal to and opposite to the aircraft’s weight and the tail downforce that we need to add to this was small. We also presented the two classes of drag that we will talk about:

- Drag independent of lift or as we often call it drag due to size as almost all drag components here scale with the aircraft’s size.

- Drag due to lift or drag due to weight as we call it as this drag scales with weight when one flies in steady state conditions.

We could see that the aircraft’s flight through the air created a total drag force of 7900 lbf, Figure 2 ( lb with an f added as we prefer to write it as this is a force and not a measure of mass. Mass we denote with just lb or the metric units kg or tonne = 2205 lb).

Figure 2. Drag of our 737 MAX 8 and how it divides between lift and non lift drag. Source: Leeham Co.

We also learned that if the drag is 7900 lbf then the engine thrust is opposite and equal. It is then 3950 lbf per engine when cruising at our mean cruise weight of 65 tonnes or 143.000 lb on our 1000 nm mission. Drag due to size consumes 63% of our thrust and drag due to weight 37%. Read more

Zhuhai Airshow: China’s aircraft industry is gaining speed

The 10th Chinese airshow at Zhuhai opened today. It was a day with fewer announcements than expected from the usual suspects (Airbus, Boeing…) but the Chinese industry did not disappoint. China is now showing more and more of its coming might as a player on the aeronautics arena.

The most prominent displays at this show were on the military side, where China has two stealth aircraft projects flying (the large Chengdu canard J-20 and the smaller Shenyang J-31) while their canard Chengdu J-10 was flying the display circuits overhead (Figure 1).

Figure 1. Chinas latest fighter developments; the J-31 and J-20 stealth fighters and the canard J-10. Source: China internet.

All aircraft are of latest structural and aerodynamic design if not in engines and systems. This is a big difference to previous shows where the Russian Sukhoi and MIG aircraft and their local copies did the flying display until 2008. Since then everything has changed and now China and USA are the only countries in the world with two different stealth designs flying. USA has one in operation (F-22) and one close to (F-35) whereas China still has many years to go until they have their new aircraft operational. But it is significant that the old aeronautical behemoths Europe and Russia have none respective one (PAK-50) stealth fighter in flight test.

Odds and Ends: 787 donation; Alenia sues Bombardier over CSeries; 2016 777 delivery slots opening up

787 donation: The Boeing Co. handed over 787 test airplane #3 (ZA003) to the Museum of Flight Saturday in an elaborate ceremony marking an unprecedented donation of a modern airliner to an aviation museum.

Boeing 787 ZA003, which went on a world sales tour, was donated to Seattle’s Museum of Flight Nov. 8, 2014. The logos of customers bracket the #2 door. Photo by Leeham News and Comment. click to enlage.

To be sure, the donation was made possible by the fact that ZA003 (and 002 and 001) can’t be sold due to the massive rework necessary, and these three airplanes have been written off for more than $2bn. But this doesn’t make the event any less significant.

Del Smith, aviation icon, dies

Del Smith, an icon in aviation for decades, died in Oregon.

Smith was the founder of Evergreen Aviation, an MRO in Arizona and the highly regarded air museum that houses the Spruce Goose in Oregon.

Evergreen cargo airlines was widely believed at one time to be owned by the CIA. The MRO in Marana (AZ) was one of the top airliner graveyards. It is now under new ownership.

The museum in McMinville (OR) has been regarded as one of the finer ones in the country. It’s been mired in controversy over allegations Smith failed to pay for the Spruce Goose, the huge wooden airplane designed by Howard Hughes, per the contract to buy the airplane.

Evergreen Airlines was the first operator of the Boeing 747 Dreamlifters, a contract now held by Atlas Air.

We met Smith on several occasions. Always affable, Smith never admitted (to us, anyway) whether Everegreen had CIA connections.. His enthusiasm for aviation history was always infectious.

Airbus, Boeing freighter demand forecasts optimistic, says P2F company

Special to Leeham News

By Cliff Duke

LCF Freighter Conversions

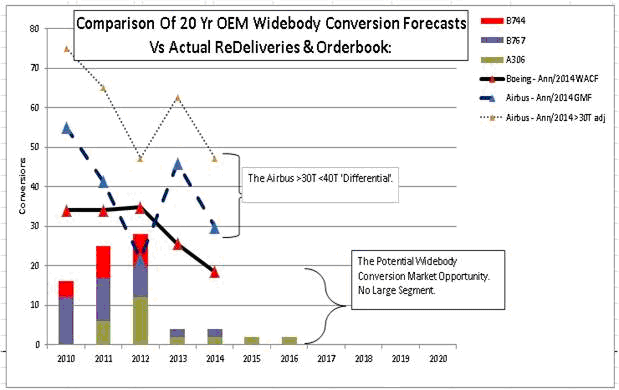

I have mapped out below the last five years of OEM forecasts (Boeing World Air Cargo Forecasts and Airbus Global Market Forecast data) on widebody conversions calibrated against the actual widebody aircraft conversions redelivered and the current respective order books. If this is half right, it suggests that if in 2010 you were a widebody aficionado and you set your stall out on the Boeing or Airbus 20 year forecasts published that year, you would, reading their 2014 forecasts, now be looking at a 46% reduction in that forecast and your 2010 business plan might be developing cracks.

In terms of performance to date, a quarter the way through the 20 year 2010 forecast (assuming an equal spread of conversions across the 20 years of the forecast) we are currently some 70 conversions behind the Boeing 2010 forecast, a 50% drop off from where we thought we would be. It looks unlikely that the variance can be recovered in the remaining 15 years of the 2010 forecast. In the meantime Boeing and Airbus have updated their 20 year forecasts, and the overall drop off forecast is significant.

One question is, have the OEMs now updated their outlooks enough? Could both forecasts still be too optimistic and could our 2010 investor be looking at a further 50% drop off when revisiting the OEM forecasts in five years’ time (2020)?

Figure 1. LCF Conversions says the Airbus and Boeing 20 year freighter demand forecast have been substantially over-optimistic. Click on image to enlarge for crisp image. Source: LCF

MD-11’s final pax flights contains lessons for McBoeing as NSA targets 2030

- Boeing’s CEO, Jim McNerney outlines his vision for the next New Small Airplane in this report from Reuters. We believe this will cement Airbus’ dominance in the single-aisle market for the next 15 years.

A retrospective of the McDonnell Douglas MD-11 and the last passenger flights for enthusiasts contains lessons for Boeing, or McBoeing as many still call the combined companies.

![]() Aviation Week’s story by highly respected technical reporter Guy Norris contains this key paragraph:

Aviation Week’s story by highly respected technical reporter Guy Norris contains this key paragraph:

Despite its many technical advances, most notably on the flight deck, the MD-11 was handicapped from birth by its derivative dependence on the obsolete DC-10. Created on the eve of the era of the fuel-efficient big twin, the MD-11 emerged as a committed three-engined product too early to be redesigned around the new generation of big turbofans. Notoriously starved of serious investment by its ‘MD’ leadership, all attempts by the Douglas product development group to develop either twin-engined or larger stretched versions of the MD-11 sadly came to nothing. (Emphasis added.)

Boeing, burned mightily by the twin program development debacles of the 787 and 747-8, isn’t about to take any more “moonshots,” says CEO Jim McNerney. Yet Boeing is now at a crossroads where another moonshot is needed.

Airbus poised to overtake Boeing in wide-body sector, bracket Boeing at both ends

Subscription required.

Introduction

Airbus is poised to produce more medium twin-aisle airplanes than Boeing by the end of 2017 and maintain ![]() the lead into the early 2020 decade, according to production rates that have been announced, unannounced and based on estimates according to production gaps; and other information, a Leeham News and Comment analysis shows.

the lead into the early 2020 decade, according to production rates that have been announced, unannounced and based on estimates according to production gaps; and other information, a Leeham News and Comment analysis shows.

The wide-body arena has traditionally been Boeing’s to dominate. Although Airbus has outsold Boeing in this sector in recent years, Boeing’s greater production capacity and earlier-to-market 787 vis-à-vis the A350, which will only deliver to its first operator next month, maintained the advantage for Boeing’s market share for years.

The A340 wasn’t a high-demand airplane, eclipsed as it was by emerging ETOPS authority and a highly desirable, very efficient 777 Series.

Airbus and Boeing each face challenges with their aging wide-bodies. The 777 Classic is now on its downward life cycle following the launch of the re-engined, re-winged 777X. Boeing claims it can maintain current production rates of the Classic, but the official line is about the only one that believes this.

Airbus’ A330 Classic, now called the ceo after the launch of the A330neo program, similarly was headed toward sharp declines in the production rates. Airbus quickly achieved 121 commitments for the neo, but first delivery isn’t planned until December 2017 (which probably means 1Q2018) and it still needs to bolster the backlog of the ceo, which drops sharply in 2016. Airbus has been far more transparent than Boeing about the risk to the production rate, and announced a reduction from 10/mo to 9/mo in 4Q2015. We don’t think this will be enough, and Airbus has talked about rates of 7-8/mo.

With this as a backdrop, we believe Airbus will begin out-producing Boeing in medium-wide-bodies within a few years. We leave out the Very Large Aircraft as highly niche. But inclusion would only make the case worse for Boeing. We expect the 747-8 production rate to be cut from 1.5/mo to 1/mo, with an announcement coming as early as next month. Airbus is currently producing the A380 at 2.5/mo.

Summary

- We forecast the crossover point in production favoring Airbus in 2017.

Airbus has notified the supply chain to plan for a higher-than-announced rate of 10/mo for the A350. - We expect the A330ceo rate to be further reduced, offset by the ramp-up of the A330neo.

- We expect the 777 rate to begin falling in 2017 and continue to fall up to the EIS of the 777X in 2020.

- Ramp up of the 777X rate will take several years, providing Airbus a production rate advantage from 2017 through at least 2022.

- Airbus already has the advantage over Boeing in the single aisle sector. Gaining the advantage over Boeing in the twin aisle sector brackets Boeing in a way that has never been done before.

Fundamentals of airliner performance, Part 1

By Bjorn Fehrm

As part of our premium content we provide a briefer form of our airliner performance analysis than we provide to our consulting clients. As we present this material, we presume a lot of knowledge on the part of the reader on the definitions we use and how these are employed. We thought it would be appropriate to give an easy-to-digest clinic on some of these definitions and concepts that we are using. Aired at the same time when we run our analysis series, we thereby present the background to our different analysis steps and some of the key parameters that influence these.

![]() We will provide these articles as free content to make them available to a broader audience. To make them more interesting and easy to digest we refrain from using formulas as much as possible, instead we illustrate our findings with real values from a modern aircraft , for that we have chosen the most common of them all, the Boeing 737.

We will provide these articles as free content to make them available to a broader audience. To make them more interesting and easy to digest we refrain from using formulas as much as possible, instead we illustrate our findings with real values from a modern aircraft , for that we have chosen the most common of them all, the Boeing 737.

We will fly this aircraft in the latest MAX 8 version on a typical short haul mission of 2.5 block hours covering a distance of 1,000 nautical miles. Starting from the cruise we will explain the factors that determine the performance of the aircraft and how we can estimate their influence. As we present the real values for the performance for the aircraft, we can also give the background to the different characteristics that contribute to the overall efficiency of the aircraft. Read more

Boeing 737 MAX 8 as a long and thin aircraft and how it fares in general versus Airbus A320neo.

Subscription required.

By Bjorn Fehrm

Introduction

Over the last weeks we have looked at Boeing’s 757 replacement possibilities on its long and thin network niche, including a ground breaking launch interview for the A321neoLR with Airbus Head of Strategy and Marketing, Kiran Rao. In the series we have seen that the A321neo has the potential to replace the 757-200 on long and thin international routes. Boeing’s equivalent single aisle entry, 737 MAX 9, has problems to extend its range over 3,600nm. It is too limited in the weight increase necessary to cover the longer range.

Marketing, Kiran Rao. In the series we have seen that the A321neo has the potential to replace the 757-200 on long and thin international routes. Boeing’s equivalent single aisle entry, 737 MAX 9, has problems to extend its range over 3,600nm. It is too limited in the weight increase necessary to cover the longer range.

Many have asked how the less- restricted Boeing 737 MAX 8 would fare, suitably equipped with the necessary extra tanks. This is the subject of this week’s sequel on the theme long and thin. At the same time we look at Airbus entry in this segment, the A320neo, to see how it stacks up to the 737 MAX 8, both in their normal 1,000 to 2,000nm operation and then also in a long and thin scenario.

Let’s first summarize what we found so far in our four articles around the Boeing 757 and its alternatives:

Summary

Figure 1. Boeing 737 MAX 8 overlaid with Airbus A320neo. Source: Leeham Co.

Read more

4 Comments

Posted on November 9, 2014 by Bjorn Fehrm

Airbus, Airlines, Boeing, CFM, GE Aviation, Leeham Co., Leeham News and Comment, Pratt & Whitney, Premium, Rolls-Royce

737, 737 MAX, 737NG, A320, A320NEO, Airbus, Boeing, CFM, Pratt & Whitney, Rolls-Royce