Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: AirAsia on A330neo, A380; 777X specificiations; A380 engine PIPs

AirAsia on Airbus: AirAsia Group is one of Airbus’ largest customers, and its CEO Tony Fernandes is increasingly influential in the Asian sector. He’s also into car racing, often betting Virgin Group’s Richard Branson. This short interview details Fernandes’ view on the prospective A330neo–something Fernandes has been pushing for some time–and what he thinks Airbus should do with the A380.

Looking at the 777X: Aviation Week has a detailed look at the Boeing 777X “under the skin.” Fuel burn, engine thrust and general specifications are in the article. Aviation Week also has a series of videos from the Dubai Air Show here. Topics: 777X, Qatar Airways and A380 engines. On the latter, Emirates CEO Tim Clark suggests putting the new GE9X or Rolls-Royce Trent on the A380 to reduce fuel burn by 10%.

Implications of the Dubai Air Show orders

With the Dubai Air Show wrapped up, it’s time to assess the events and the implications.

Boeing launches 777X

Boeing launched the 777X at the show with orders and commitments for 182 777-9s and 43 777-8s, the latter the Ultra Long Range (ULR) version. These orders were driven by Emirates Airlines, which ordered 115 -9s and 35 -8s.

All had been widely telegraphed, and follow Lufthansa Airlines’ order for 34 777-9X previously anounced.

The 777-8 competes directly with the 350-passenger Airbus A350-1000; the 777-9, at 407 passengers, is in a class by itself between the -1000 and the 467-seat Boeing 747-8.

Boeing forecasts a 20-year demand for 670 350-400 seat (including the 405-seat 777-9) sector. Airbus forecasts a need for 779 aircraft in this sector. Airbus had booked 176 A350-1000 orders going into the show and added 10 more.

This means Airbus and Boeing have sold 186 and 259 aircraft in this sector respectively, or 445 in total. Boeing converted three options of the 777-300ER to a firm order. Now we’re at 448, of 67% of the Boeing forecast or 58% of the Airbus forecast. There are 278 777-300ERs in backlog, for a total of 692.

There are 306 747-400 passenger models in service and another 23 Combis, or 329. There are 501 777-300s in service. This equals 830 excluding the 777-300ER backlog or 1,108 including the backlog,

|

|

747-400 |

777-300ER |

A350-1000 |

777-8 |

777-9 |

|

In Service |

329 |

501 |

0 |

0 |

0 |

|

Backlog |

0 |

278 |

186 |

43 |

182 |

|

Total |

329 |

779 |

186 |

43 |

216 |

Sources: Airbus, Boeing

We believe the Airbus and Boeing forecasts understate the 20 year demand just on the replacement potential of today’s 1,108 747-400s and 779 777-300ERs in service or on backlog. In addition to the replacement requirement, traffic growth will support more aircraft orders.

Airbus and the “A350-1100”

We previously analyzed the Airbus dilemma over how it should meet the development of the 777-9. Airbus doesn’t have a direct competitor to this aircraft, though officials claim the A350-1000 is this competitor. We disagree and so do Emirates Airlines and Qatar Airways. According to our Market Intelligence, Airbus has held conversations with Emirates about a stretch “A350-1100” version. Qatar’s CEO, Akbar Al-Baker, publicly expressed interest in an “1100” model.

Airbus previously dismissed the idea of an “1100” of roughly equal capacity to the 777-9 because it did not see a market for the airplane of this size. Based on its forecast of 779 airplanes and the existing sales, this logic is apparent. Since then, however, Airbus officials indicated they are at least looking at the possibility, though no formal study is underway.

There is a concern in some quarters that Airbus has already missed this opportunity and Boeing has too great a lead.

We continue to believe Airbus will eventually proceed with the “1100.”

Boeing 747-8

We think it significant that no orders were announced for the Boeing 747-8I passenger model or for the 747-8F. We have long believed the 777-9 spells the end of the 747-8I. While Lufthansa Airlines has ordered the 8I, the 777-9 and the Airbus A380 and sees a need for each of these as each serves different market sectors, there is little the 747-8I can do that the more economical 777-9 can’t. Lufthansa likes the 747-8I for hot-and-high airports, such as Mexico City, but there are few of these markets that support the continuation of this airplane now that the 777-9 is official.

The 747-8F’s future depends on the recovery of the cargo market. Boeing forecasts this to occur next year. But one cargo conversion company, which doesn’t play in the 747 space, doesn’t see the business case of a new-build 747-8F when there are abundant 747-400Fs parked in the desert and those 329 more passenger and combi aircraft available for conversion at a far less expensive price than it costs to buy new. Additionally, this company believes the belly capacity of the 777-300ER and Airbus A330-300, and the existence of the 777-200LRF, provides plenty of capacity that diminishes the economics and requirement for the 747-8F.

Airbus A380

The order by Emirates Airlines for 50 A380s is a badly needed shot in the arm for the program, which saw sales stall at 262 for an extended period (259 net of cancellations). There are several orders that are iffy (Hong Kong Airlines, Virgin Atlantic, two for Air France) and dead (Kingfisher Airlines), among others. Emirates plus a pending confirmation of an MOU for Doric Lease are needed to fill near-term production slot vacancies and boost the book-to-bill deficit in the program.

But customer concentration is increased with the Emirates order, now accounting for 140 (42.5%) of the 329 orders confirmed and announced. Airbus continues to bank on airport congestion and traffic growth combining to boost sales. We think the 777-9 will cut into this demand. The question is whether Airbus proceeds with an A350-1100 to retain some of this diversion in the family or whether it allows Boeing the monopoly to do so.

Loyalty is a one-way street at Boeing

Boeing’s move to shop around the 777X assembly site, while telegraphed and certainly expected, is another example of the shifting loyalties at Boeing that have been more than a decade in the making.

Before we start, it must be acknowledged that Boeing is a publicly traded stock company and it has fiduciary duties to make sound financial decisions. That being said, one can debate endlessly whether the decisions executives have made have been financially sound (and there is ample evidence with respect to 787 outsourcing and opening a second line in Charleston that the decisions were not sound). Setting aside this debate, since Boeing moved HQ to Chicago in 2001, loyalty appears a thing of the past.

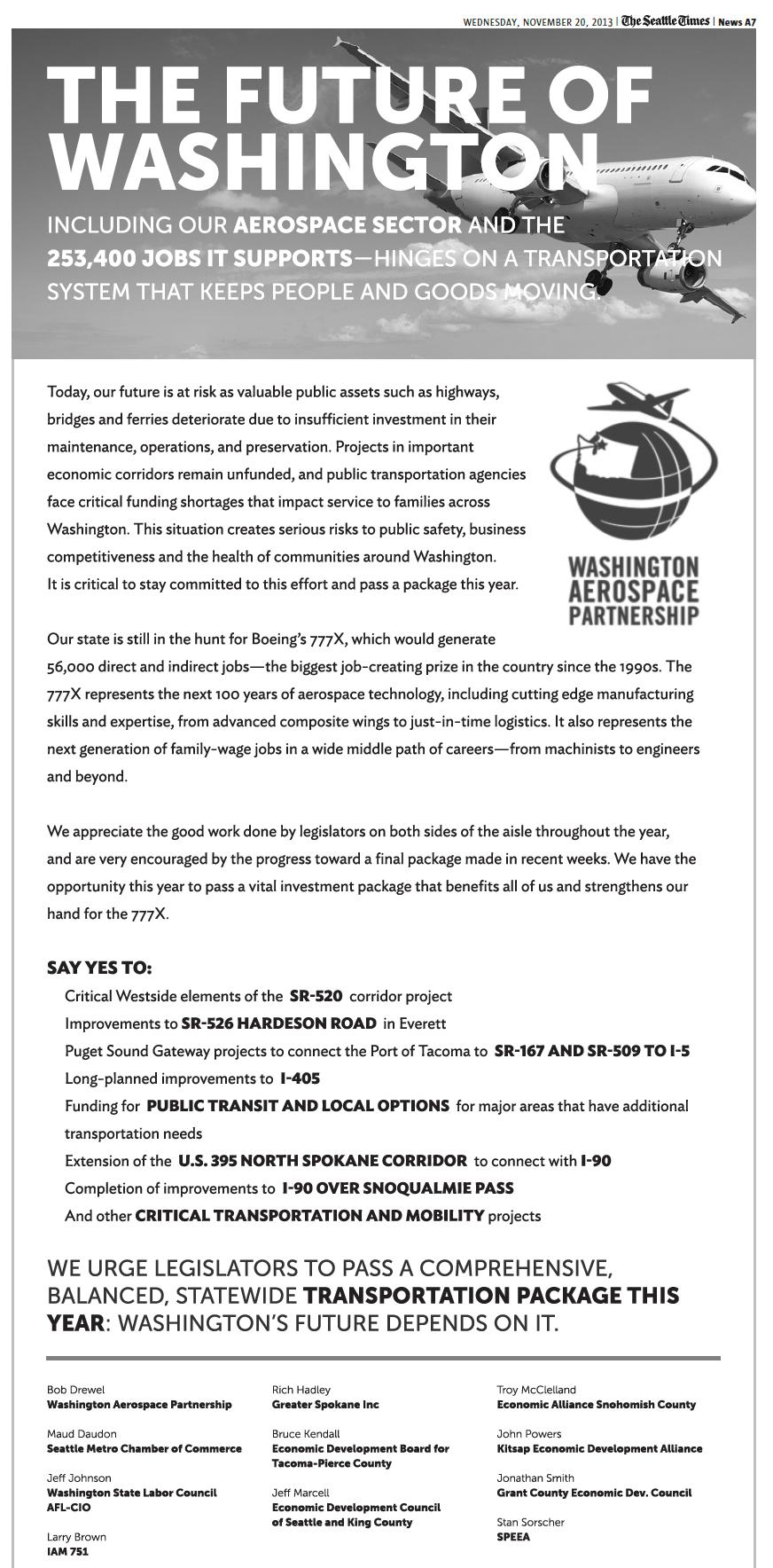

Washington State wants Airbus business but this is a big oops

The Washington Aerospace Partnership is a state agency to promote aerospace in Washington.

We’ve written about WAP before, criticizing its membership as totally devoid of any industry representative–it’s all economic development commissions, chambers of commerce and bureaucrats. We think the absence of industry representation is a major defect.

This full page ad in The Seattle Times today illustrates the point. We’re sure our readers will spot why.

Dominic Gates of The Seattle Times certainly did.

Odds and Ends: 777X site; A380 reconfiguration; 777 flashback; PNAA’s 13th annual conference; A350; MC-21

Build 777X “where it makes the most sense:” A Boeing executive, in a CNBC interview, said the 777X would be built “where it makes the most sense.”

CNBC writes that Shephard Hill, president of Boeing International, said, “Honestly, we’re looking within the United States at this point because of the large infrastructure we have there. But again, with the mandate to do it on time, to do it in a quality way, that will drive the decision.”

Meanwhile, Alabama officials revealed they talked with Boeing about locating “some [777X] work” at Boeing’s Huntsville operation. Stories are here and here.

A380 reconfiguration: After our post concerning the secondary market of the Airbus A380 and a figure cited by a lessor that it could cost as much as $20m to reconfigure the airplane (assuming all bells and whistles), we received two emails from readers giving a different perspective.

One wrote that Airbus took the Emirates Airlines specification, which is not as customized as perceived, and outlined three scenarios for reconfiguration.

- Simply change the cabin colors: $600,000 from Airbus and $500,000 for Buyer Furnished Equipment (BFE).

- Change three class to two class, with only the upper deck changing: $3.6m in Airbus costs, $1.6m for BFE.

- High-density, all Y-class, both decks: $4.3m for Airbus costs, $3.5m for BFE.

Another reader wrote that the $20m figure is correct if all existing cabin stuff is tossed and the reconfiguration starts from scratch, but seats and other equipment could be sold to reduce the cost. Going one class, this reader wrote, had a price of between $8m-$10m (slightly higher than that reported by the first reader) and a two class configuration would cost about $5m, roughly the same as noted above.

Flashback on 777 successor: Jon Ostrower, when he was with Flight Global, Tweeted out a flashback down memory lane when we did a podcast with him six years ago, talking about a Boeing 777 successor. We looked pretty smart back then, as it turns out.

PNAA’s 13th Annual Conference: The Pacific Northwest Aerospace Alliance has released the agenda for its 13th Annual Conference held Feb. 4-6, 2014, in Lynnwood (WA), north of Seattle and south of Everett. Crafted well before the Boeing 777X events of last week, the conference is entitled “What’s Driving Change in the Aerospace Industry”.

Boeing says it will decide within three months where it will build the 777X, or in December or January, the latter just before the conference. Whatever this decision, this specific action will clearly come up at the conference, though it is not specifically a topic on the agenda.

We’re presenting on the State of the Airline Industry on the first day and share a panel on the third day with analysts Michel Merluzeau of G2 Solutions and Richard Aboulafia of The Teal Group. We’ve done this panel each year for several years now, and it’s a free-wheeling discussion of what we’ve heard throughout the conference and events generally.

This conference has now become the largest of its kind on the US West Coast, with nearly 450 attendees this past February. The Big Four airframe OEMs, the Big Three engine OEMs and a host of suppliers and lessors present.

MC-21 program update: ATO.ru, a Russian publication, has this update on the Irkut MC-21 program.

A350-1000: Akbar Al-Baker, CEO of Qatar Airways, is known for his about-faces at a whim, so much so that he has the nickname U-Turn Al. Once a vocal critic of the Airbus A350-1000, he now says it is a great airplane, according to this interview in Gulf Business. He urges Airbus to consider a larger version of the plane.

Emirates urges 777X be built in US: Wall Street Journal

Emirates Airlines has urged Boeing to build the 777X and its components in the US to avoid the issues that bedeviled the 787, according to The Wall Street Journal. (Subscription required.)

“Tim Clark, president of Emirates, said Boeing should assemble the 777X family in its own facilities to better manage the process and deliver the aircraft on time in 2020,” The WSJ wrote.

“‘All we said to [Boeing] was, ‘Please don’t do to 777X what you did to the [787],'” Mr. Clark said in an interview on the sidelines of the Dubai Air Show, adding that outsourcing the manufacture-and-build process to companies in Asia or Europe might mean Boeing loses quality and control of assembly. “Don’t do that to us,” he said,” The WSJ wrote.

“Qatar Airways Chief Executive Akbar Al Akbar similarly expressed a desire that Boeing assemble the 777X at a single U.S. facility. “Frankly, we would rather everything was built in one place, and I think Boeing from the 787 experience have learnt a lesson,” he said in an interview Tuesday,” reported The Journal.

There is broad consensus that Boeing’s Everett plant is the best place to build the 777X, given its experienced workforce, a mature factory and the continuing challenges of the Charleston 787 plant. But Boeing CEO Jim McNerney’s antipathy toward the IAM specifically and the Washington State business climate generally are “wild cards,” a source familiar with the dynamics tells us.

Boeing is entertaining business offers from other states, and is widely reported to be considering locations at its facilities in Utah, California, Texas and Alabama. The Charleston plant is said not to be on the list due to the plant challenges with the 787, but Boeing hasn’t confirmed any of these possibilities.

A380 orders boost backlog but future risk remains

The order by Emirates Airlines for 50 more Airbus A380s had been hinted at for some time, and it is certainly welcome for the backlog. This deal, coupled with the MOU announced at the Paris Air Show for 20 from lessor Doric, expected to be firmed up by year end, adds 70 orders to the long-stalled total count, which was 259 prior to either deal (net of three cancellations from Lufthansa Airlines). This now brings Airbus to 329 orders.

It’s still well short of the 650 orders Airbus expects to snare over the next 20 years from its September 20-year forecast. These expectations are on top of the existing order stream, and a figure that hasn’t changed much since its first Very Large Aircraft forecast in 2000.

(The current forecast is for about 1,300 VLA passenger models; Airbus expects to receive 50% of the market. This is before the 777-9X, barely qualifying as a VLA at a nominal 407 passengers, entered the picture. Up to now, Airbus has been capturing nearly 90% of the VLAP market against Boeing’s 747-8I.)

AIN Online beat us to our plan to assess the future risks for the A380, particularly as it heads into the secondary market, with this analysis. We agree with the broad conclusion that there will be little secondary market opportunity for the airplane beginning in 2020 when the first of Emirates Airlines’ behemoths start coming off lease.

One lessor, who is not an A380 owner, says it will cost about $20m to reconfigure an A380 in a typical three-class layout with the usual bells and whistles. Doric Lease, in an interview with Bloomberg, says Airbus needs to standardize configuration to make re-leasing the giant plane easier.