Leeham News and Analysis

There's more to real news than a news release.

It’s official: Boeing launches 787-10 with 102 orders, commitments

Here’s the Boeing press release.

Boeing expects the 787-10 to perhaps be the best selling model of the family over time. With a range of 7,000nm, it will have the ability to do most airline missions; 8,000nm-8,500nm range airplanes (let alone the proposed 9,400nm range of the 777X) is really more than most carriers need. We expect the orders to double by the end of the year.

In other Paris Air Show news, easyJet chose to stay with Airbus for its fleet renewal ordering a combination of 35 A320ceos and 100 neos. This was hard-fought competition. Boeing thought it won the deal on price, and Bombardier was ready to go with its own contract when Airbus came in at the last minute with a low price of its own, blowing both competitors out of the water.

Bombardier: This story explains in part why Bombardier has been challenged in selling the CSeries. The US Scope Clause inhibits sales to regional airlines; and lessors want to see a broader customer base. This is in addition to Airbus under-pricing Bombardier in key campaigns to block sales.

ATR landed an order for up to 90 ATR-72-600s.

Boeing will market the Embraer KC-390 to the Pentagon. After all the Boeing campaign about the Pentagon buying a foreign airplane for a tanker, this really takes the cake.

Paris Air Show Day 1

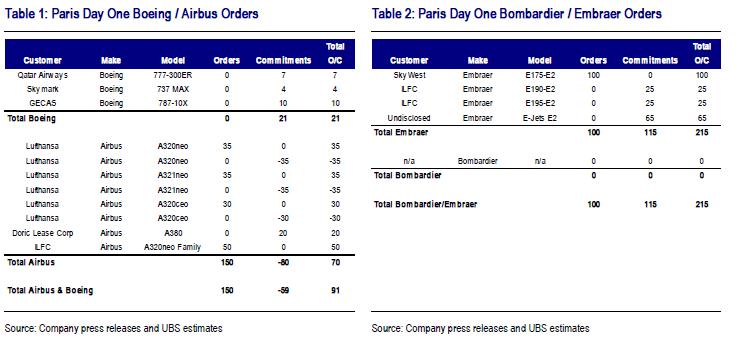

UBS has this easy-to-read Table of the orders and commitments announced on Day 1 of the Paris Air Show:

The big news, of course, is the launch of the Embraer E-175/190/195 “E2” (second generation). The press release is here.

Embraer Rendering

Airbus scored an unexpected order for the A380: 20 from specialty lessor Doric Leasing, which has financed a number of A380s. We think this is an odd deal, and it must be one that already has some A380 customers lined up.

Tomorrow is expected to be the day Boeing launches the 787-10, so it should be Boeing’s day. We also believe tomorrow will be the day Airbus does a fly by of the A350 XWB. A little tit-for-tat, perhaps.