Leeham News and Analysis

There's more to real news than a news release.

Single aisle or Widebody over the Atlantic at low load factors, Part 3?

Subscription Required

By Bjorn Fehrm

Introduction

November 11, 2021, © Leeham News: Last week, we compared the economics of an Airbus A321XLR and A330-200 on our thin route over the Atlantic. The XLR improves the capabilities of the A321 quite a bit, not only on range but also on load-carrying ability.

The more efficient use of the space below the floor leaves room for cargo once the passenger bags are loaded. The margin race between the A321XLR and the A330-200 depended on the cargo pricing in the end. Now we finish the series with a more challenging setup for the twin-aisle.

We assume we use an A330-900, a nominal 300 seater on the Dublin to Newark route with only 130 passengers per departure. The load factor is then at 43%. Can the twin-aisle still earn the margin of an A321XLR on this route by virtue of its cargo capacity?

Summary

- The margin generation of the A321XLR versus the A330-200 was close. It boiled down to cargo pricing.

- The A330-900 adds costs but also more cargo room. Will it cover the extra costs?

Single aisle or Widebody over the Atlantic on thin routes? Part 2

Subscription Required

By Bjorn Fehrm

Introduction

November 4, 2021, © Leeham News: Last week, we compared the economics of an Airbus A321LR and A330-200 on a thin route over the Atlantic. We found the Widebody could compensate for its higher operating costs as long as the route has a sizable cargo stream and that this is paid at today’s elevated air freight prices. The A321LR has extra center tanks that take away all cargo space and thus has negligible cargo revenue.

Now we repeat the analysis with the more capable A321XLR. It stores four ACTs worth of extra fuel in the space of two. This leaves room for cargo. Will it be enough to restore the supremacy in margin generation over the twin-aisle?

Rendering of the A321XLR. Source: Airbus.

Summary

- The check last week surprised with how close a mid-age A330-200 can come in margin generation to an A321LR on a thin route, thanks to its higher cargo revenue.

- The A321XLR, with its more efficient tank setup, rebalances the fight in favor of the single-aisle.

Single-aisle or Widebody over the Atlantic on thin routes?

Subscription Required

By Bjorn Fehrm

Introduction

October 28, 2021, © Leeham News: The headline seems like a no-brainer. On long thin routes over the Atlantic, we have learned a Boeing 757, or its replacement, the Airbus A321LR, is the right aircraft (as long as it’s within its range).

This was the situation in a pre-pandemic market where freight yields were half of today. The single-aisle has lower operating costs than the widebodies, and if the passenger stream and range fits, it was the transport to have on the route.

With the high cargo prices, does this change? We check for several Atlantic routes.

Summary

- The increased yields for air cargo challenge the mantra; a single aisle is preferred for trans-Atlantic service as long as the passenger number and range fits.

- Going forward it will be all about the cargo prices and the number of passengers to transport.

Air freight demand explosion: a long-term trend?

Subscription Required

By Judson Rollins

Introduction

October 18, 2021, © Leeham News: Much ink has been spilled over the surge in demand that has washed over every corner of the cargo world: air, sea, road, and rail.

Amazon Air’s first parcels being unloaded at Amazon.com’s new Cincinnati (US) sort hub. Source: Amazon.com.

Before the COVID-19 crisis, air transport was reserved primarily for items with high value and/or time sensitivity, such as laptop computers or express documents. And growing competition in the cargo market meant that average yield (revenue per ton-mile) was declining by more than 2% per year, according to past editions of Boeing’s World Air Cargo Forecast.

But now the cost of sea transport has exploded, shifting a significant chunk of cargo from ocean freighters to their airborne equivalents. This is driving some retailers to use air transport. Home Depot, an American home-improvement retailer, is resorting to air freight to bring in smaller, higher-value items like power tools that it needs to keep on the shelves at all times.

Even before COVID-19, a growing share of air freight has come from e-commerce — thereby shifting the volume-to-weight considerations relative to “traditional” freight.

Will these trends continue even beyond the COVID crisis? And what impact will it have on the market for factory-built freighters and passenger-to-freighter (P2F) conversions?

Summary

- Soaring sea freight yields mean small shipments are now more economic by air than sea.

- Volumetric capacity matters more than max gross weight.

- New freighter options will compete with a glut of conversion feedstock.

- Air freight yields will eventually revert to historical trendlines in most regions.

Is the cargo capacity deciding the airliner variant? Part 3.

Subscription Required

By Bjorn Fehrm

Introduction

October 7, 2021, © Leeham News: In last week’s article, we could see today’s high cargo prices can motivate a 325 seat Airbus A350-900 even though the passenger load on the routes would point to a 240 seat A330-800.

How far does this “paying for a larger aircraft with belly cargo” paradigm go? Today we see if Airbus’ largest aircraft, the A350-1000, can generate the margins of the A350-900 on freight-rich routes. Can an airline that has an A350-900 sized passenger demand for such routes go to an A350-1000 instead?

Summary

- The increased yields for air cargo leads to surprising effects. Oversized passenger models can survive the passenger drought on today’s international routes as long as it’s a route with good freight demand.

Is cargo capacity deciding the airliner variant?

Subscription Required

By Bjorn Fehrm

Introduction

September 23, 2021, © Leeham News: In last week’s article, we put the question: Has the increased cargo pricing started to affect the choice of airliner variant?

We listed recent decisions between the Boeing 787-8 and -9 or Airbus A330-900 and A350-900 where the traffic levels post-pandemic would motivate the smaller variant, but the larger was retained or selected.

It makes you wonder whether the higher cargo capacity of the larger variant compensates for flying a larger cabin at a lower load factor? We make a cost and revenue analysis to find out.

Summary

- Cargo was an additional revenue stream on top of the main source, the passenger traffic.

- The lower traffic levels for international long-haul traffic and the increase in cargo pricing have changed this. Cargo is now as important in the decision of which aircraft to choose as the passenger capacity.

Is cargo capacity deciding passenger airliner choice?

Subscription Required

By Vincent Valery

Introduction

Sep. 16, 2021, © Leeham News: LNA has so far compared the performance of both factory and converted freighter aircraft. We will continue the cargo-themed series by analyzing how cargo capacity might decide what passenger aircraft airlines buy.

LNA has extensively discussed Airbus and Boeing’s struggles in accumulating orders for their larger aircraft, the A350-1000, and 777X. However, as seen in a recent article, smaller twin-aisle airplanes face skinny order books as well.

One could think that the COVID-19 pandemic would lead airlines to down-gauge their twin-aisle orders to the smallest available variants, the Airbus A330-800 and Boeing 787-8. Such moves make sense at face value to accommodate a reduced demand in passenger traffic.

So far, only Singapore Airlines has converted two 787-10 orders to the 787-8. Instead of down-gauging, American Airlines converted a portion of its 787-8 order to the larger 787-9. Condor recently announced replacing its aging 767-300ER fleet with A330-900s instead of opting for smaller aircraft.

We now investigate whether airlines’ decision not to down-gauge their twin-aisle order books to the smallest variants has to do with a reduction in cargo capacity.

Summary

- A drought of small twin-aisle orders;

- Airline conundra on choosing best variant;

- Comparing cargo capacity of in-production passenger aircraft;

- Setting the analysis framework.

Boeing; 20-year aircraft demand back to pre-pandemic level

By Bjorn Fehrm

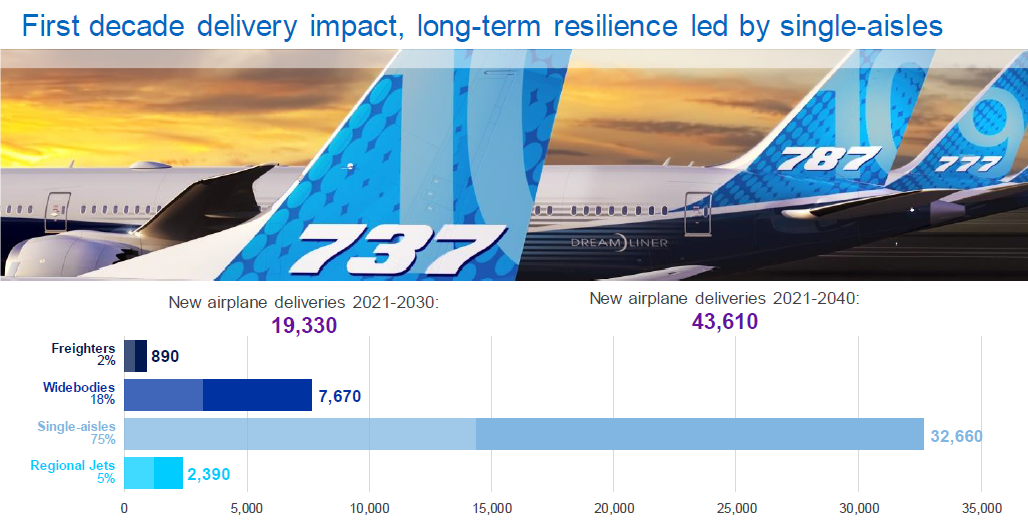

September 14, 2021, ©. Leeham News: Boeing released its yearly commercial aircraft demand forecast today. Over the next 20 years, the demand for single-aisle aircraft is past pre-covid levels at more than 32,000 aircraft, with widebodies down 8% compared to 2019 at 7,500 aircraft, Figure 1.

The forecast for freighters is up at 890 aircraft making a total of 43,600 aircraft until 2040, the level of the 20 years forecasts before the pandemic.

Figure 1. Boeing’s forecast of deliveries of commercial aircraft to 2030 and 2040. Source: Boeing 2021 CMO.

The single-aisle freighters, 737-800BCF versus A320P2F.

Subscription Required

By Bjorn Fehrm

Introduction

September 2, 2021, © Leeham News: In our series about freighters, we now look at domestic single-aisle freighters based on the Boeing 737-800 and the Airbus A320. The 737-800BCF is the follow-on small Boeing freighter conversion from the 737-400, as more 737-800 passenger feed-stock becomes available.

There is also ample feed-stock of older A320-200 with market values that make these interesting as a P2F freighter.

Which one of the two offers the lowest costs per tonne-km? We use our performance model to find out.

Boeing’s 737-800BCF Source: Boeing.

Summary

- Both the 737-800 and A320 older aircraft are available at prices that make freighter conversions attractive.

- Which of these freighters has the best operating economics, and what is the difference in capacity?

Rejuvenating the current in-service cargo fleet

Subscription Required

By Vincent Valery

Introduction

Aug. 30, 2021, © Leeham News: The COVID-19 pandemic lingers on passenger airlines, delaying a full traffic recovery. At the same time, the freighter market is very active and shows no signs of abating.

Credit: Airbus

A surplus of passenger aircraft and record cargo demand means that passenger-to-freighter conversion lines are firing on all cylinders. On top of the existing Boeing 757 and 767 lines, new ones are coming online to convert Airbus A321s, A330s, and 777-300ERs.

Airbus launched the A350F program while Boeing is pondering a 777X-F program. Airbus is also discussing the launch of a factory A321F. The European OEM wants to increase its footprint in a Boeing stronghold.

Boeing also keeps accumulating new freighter orders at a healthy pace.

While some factory-built and converted freighters will be for growth, a significant portion will replace older in-service aircraft.

To complement the ongoing series comparing the economics of freighter aircraft and analysis of historical deliveries, LNA now examines the current in-service fleet. Analyzing aircraft in operation will help determine the most promising replacement opportunities for converted and factory freighters.

Summary

- Overall jet freighter fleet view;

- Significant single-aisle replacement opportunities;

- One market concentrates most small dual-aisle fleet;

- One large freighter fleet up for replacement;

- A factor that could accelerate replacements.