Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: Supply chain demands; Southwest hints?; Retrospective on A320/737 replacements

Supply chain demands: Earlier this week, we talked about the prospect of production wars as Airbus and Boeing ramp up over the next five years, combined with the new entrants and the new offerings from Bombardier and Embraer.

We noted that this will mean opportunity and risk for the supply chain. Ryan Murphy from Salem Partners has a long analysis the starts with the finishing sector but which goes beyond this to discuss the broader implications. It makes for an interesting read.

Southwest: Hints of things to come? Yesterday we wrote about Southwest Airlines and the demise of the Wright Amendment that restricts travel from Dallas Love Field. We suggested several routes that Southwest would launch from Love once the Amendment passes into history.

Here’s a display Southwest erected on its countdown to the end of the Wright Amendment. We think it hints at things to come. Going clockwise: Chicago, New York and Charlotte seem to be where the airplanes are going. Then Los Angeles and Salt Lake City seem to be implied destinations. But the last one? Boise, or some other obscure city?

Or are we reading too much into the placement of these airplanes?

Source: Dallas Morning News

Our thoughts:

Retrospective: We were looking at previous posts for some specific information and in the process re-read one about replacing the Airbus A320 and Boeing 737. The post dates from 2009. In light of subsequent events, it makes for interesting re-reading. We discuss the internal views of Airbus and Boeing about replacement or re-engining their aircraft and the engines from Pratt & Whitney and GE Aviation/CFM. We also touch on Boeing leaning toward not replacing the 777.

Retrospective, Part 2: Airchive has a nice set of historical looks at the development of the Boeing factory at Everett: Part One and Part Two.

Odds and Ends: Embraer reports weak quarter; MRJ FTV #1 assembly; JAL, ANA politics

Embraer’s Third Quarter: Embraer delivered fewer commercial airplanes in the third quarter than had been expected. The maker of E-Jets and the E-Jet E2 re-engined versions due beginning in 2018 listed its deliveries and backlog in its press release. Analysts expects 22 E-Jets would be delivered in the quarter. But the backlog is up 44% year-over-year, largely on the strength of the launch of the E2 (150 orders, 100 of which are for the smallest E-175 E2 and 25 each for the E-190/195 E2), and orders from Republic Airways Holdings and SkyWest Airlines for the current generation of E-Jets. The E-175 remains to most frequently-ordered airplane.

Although Embraer is expanding the size of the E-195-E2 by up to 12 seats, orders have been few. The E-190 has proved a better-selling model than the E-195.

Source: Embraer

Officials expect to have a healthy fourth quarter delivery stream.

Mitsubishi MRJ: Assembly for the first Mitsubishi MRJ Flight Test Vehicle (to borrow Bombardier’s term for the CSeries) is underway. The first delivery was originally planned for this year; it’s now planned for 2017, four years late. This rivals Boeing’s 787 and exceeds the Airbus A350 and as yet the CSeries.

JAL, ANA Politics: Reuters has an analysis about the suspicion politics may have been involved in the decision by Japan Airlines to buy the Airbus A350 and the pending order by ANA of an Airbus or Boeing airplane.

Southwest’s forthcoming expansion will offset AA-US consolidation

Southwest Airlines has begun a one year countdown to the day the Wright Amendment will disappear.

The Amendment, named after former US House Speaker Jim Wright, restricts Southwest’s ability to fly from in-town Dallas Love Field. Originally Southwest was restricted to Texas and the immediately adjacent states. The Amendment has been modified several times. Today the carrier may fly anywhere within the US beyond the exceptions with one stop. Love Field is now restricted to 20 gates; Southwest controls all but a few of them.

.

The restrictions were put into place to protect the then-new Dallas-Ft. Worth Regional Airport, which was constructed mid-way between the two cities. All the airlines at the time served Love Field and when DFW was created, they all agreed to move to the new airport and close Love Field to airline traffic. Except Southwest, which didn’t exist at the time of the agreement but which began service from Love in the interim between the signing of the agreement and the opening of DFW. The attempts by Braniff International Airways and Trans Texas International (nee TRANS Texas) to put Southwest out of business are industry folklore.

The fear was that Southwest and Love would hurt DFW and the airlines competing from the distant airport, including American Airlines. When Southwest a few years ago launched a full-scale attack on the Wright Amendment, American led the charge to block the effort. The compromise was the gate restriction, the one-stop service and a five year phase out.

Who could have foreseen that this now could help come to the rescue of American and US Airways as they fight the US Department of Justice’s attempt to block the merger of these two carriers?

Here’s why.

Odds and Ends: ANA, Airbus and Boeing; Era of the jumbo jet; Repo wars

ANA to stay with Boeing? After losing Japan Airlines to Airbus, analysts are split over whether ANA will also defect. Some say JAL’s order will give ANA cover to defect. Others say JAL’s order will increase the pressure on ANA to stay with Boeing. The Seattle Times this story. Our take: compare this with what happened following American Airlines’ order with Airbus. The Delta Air Lines competition was next, and Boeing was determined not to lose that competition–and it didn’t. Market talk says Boeing’s price to Delta was 10%-15% below Airbus’ offer, though this has never been confirmed. We understand there were other considerations besides costs. Regardless, both sides are going to go all-out to win.

SuperJumbo Era: The Financial Times has a story about whether the era of the super-jumbo (the Airbus A380 and the Boeing 747-8) is over (free registration required). Bloomberg has a story about the Boeing 777X being a jumbo killer.

Repo Wars: Here’s an departure from our usual coverage–tactics used to repossess an airplane from a delinquent airline. A decade ago, we were involved in a similar situation, planning the repossession of a Boeing 767-300ER from a South American airline. The lessor obtained a court order while we did some behind-the-scenes plotting to “arrest” the airplane at Miami. It was at the gate, full of passengers when the sheriff served the pilot with the court papers. Secrecy was imperative, as the story linked above references. Once the airplane was seized, the airline rescheduled a second 767 to stay on domestic service so the lessor couldn’t seize that airplane, too.

Low Cost Carriers dominate Top 10 single aisle customers at Airbus, Boeing

Low Cost Carriers (LCCs) dominate the backlog of the Top 10 single-aisle customers for Airbus and Boeing, data from the two OEMs show through August.

The importance of LCCs to the OEM backlogs has been increasing during the past decade, as has been the shift over the past 20 years from a dominance by US airlines to non-US carriers.

The backlog of LCCs today demonstrates the shift toward this sector as well as the shift toward non-US airlines.

|

|

Boeing 737 (All Models) |

|

|

|

Airbus A320 (All Models) |

|

||

|

1 |

Southwest |

317 |

18% |

|

1 |

Air Asia |

351 |

21% |

|

2 |

Lion Air |

313 |

17% |

|

2 |

Lion Air |

234 |

14% |

|

3 |

American |

187 |

10% |

|

3 |

Indigo |

196 |

11% |

|

4 |

Ryanair |

175 |

10% |

|

4 |

ILFC |

165 |

10% |

|

5 |

United |

172 |

10% |

|

5 |

Lufthansa |

146 |

9% |

|

6 |

Norwegian |

162 |

9% |

|

6 |

easyJet |

145 |

8% |

|

7 |

Air Lease |

151 |

8% |

|

7 |

American |

130 |

8% |

|

8 |

GECAS |

120 |

7% |

|

8 |

Qantas |

129 |

8% |

|

9 |

Delta |

100 |

6% |

|

9 |

Spirit |

115 |

7% |

|

10 |

GOL |

99 |

6% |

|

10 |

Norwegian |

100 |

6% |

|

|

August 2013 |

1,796 |

|

|

|

August 2013 |

1,711 |

|

|

|

LCC Total |

1,066 |

59% |

|

|

LCC Total |

1,141 |

67% |

Sources: Airbus, Boeing

For Boeing, 59% of the Top 10 single-aisle order backlog is with LCCs–more than 1,000 737NGs and MAXes. Over at Airbus, the dominance of LCCs is even greater: 67% for all A320 family members, including ceos and neos.

As we reported last week, Asia’s LCC, Lion Air has more firm orders for single-aisle aircraft than any other customer: 547. Lion Air is said to be planning to place an order as early as year end for a “double-digit” number of Bombardier CSeries. The next closest: the USA’s Southwest Airlines, at 317 737s, and American Airlines, with a combined 317 from Airbus and Boeing.

Europe‘s Norwegian has a combined 262 single-aisles on order from the two OEMs.

The dominance of LCCs in the backlogs reflect the changing nature of the airline industry, both in terms of service demand but also with the increasing growth in developing nations, with major growth coming out of Asia–the domain of Lion Air and AirAsia.

It also reflects the strategy of flipping aircraft around the end of the maintenance holidays in six or seven years after delivery, which may be a decent strategy for the airline but one which hazards lease rates and residual values and a potential imbalance of supply-and-demand at that sixth or seventh year. With a much greater reliance on LCCs than Boeing, Airbus’ A320s are most at risk on the RVs and lease rates.

Chasing the 777X assembly site

Washington State is ramping up its all-out effort to land the assembly site of the Boeing 777X.

Gov. Jay Inslee appointed a bi-partisan panel from the Legislature to come up with an incentive package to present to Boeing. He’s already proposed extending the Boeing 787 tax incentives adopted in 2003 another 16 years, to 2040, though these incentives were ruled illegal by the World Trade Organization.

Predictably, Airbus pounced on Inslee’s proposal, though mistakenly assuming Boeing asked for the incentives. According to The Everett Herald, the initiative is entirely Inslee’s. Said Airbus:

This is another example of Boeing’s refusal to accept to play by the rules by continuing to solicit and receive subsidies which are especially potent in distorting trade. The 787 tax credits were ruled illegal subsidies by the WTO in the final verdict of March 2012. After breaking the WTO rules on the 787, with a repeat of measures for the 777X Boeing continues to show total disrespect for WTO obligations and the compliance process.

These are the quotes from the reports on

adverse effects:

– The WTO Panel found that “the availability of … the B&O tax subsidies, enabled Boeing to lower its prices beyond the level that would otherwise have been economically justifiable” (7.1818) giving Boeing a “pervasive and consistent pricing advantage” (7.1819) that is “felt most acutely in particular sales campaigns of strategic importance” (7.1822) and results in illegal adverse effects to EU LCA interests (7.1823)

– The WTO Appellate Body generally upheld that finding (para. 1273), emphasizing the importance of the subsidy given the price-sensitive nature of many sales, and Boeing’s market power in a duopoly context (para. 1260)

The analysis of the B&O tax rate reduction “subsidies” do not provide any great quotable statements by the Panel, which isn’t surprising given that the dollar value of those subsidies was quite low during the period of review, when the subsidy programs were just starting to take effect. The numbers now are much larger!!

The quote on the subsidy side is in 7.302 of the panel report:

“For the foregoing reasons, the Panel finds that the Washington B&O tax reduction; the B&O tax credits for preproduction development, for computer software and hardware and for property taxes; and the sales and use tax exemption for computer hardware, peripherals and software are specific subsidies to Boeing within the meaning of Articles 1 and 2 of the SCM Agreement. The Panel estimates that the amounts of the subsidies to Boeing’s LCA division are $13.8 million; $21.3 million; $20 million; $1.1 million; and $8.3 million respectively”

Inslee’s office said that the WTO ruling is under appeal and until that’s settled, the tax breaks are legal.

Washington has been often criticized, including by its own politicians, as having a worse tax structure than competing states. But Washington has the sixth best tax climate in the country, according to the Tax Foundation. A low number on the map is good.

Airbus sequence shift of A350s coming, reports customer. Airbus says ‘no’

Airbus will likely shift the sequence of the entry-into-service of the A350, a customer tells us. Other sources report the same, with another customer calling the prospect of a shift “inevitable.”

A tantalizing clue may have come from Airbus CEO Fabrice Bregier. In Airbus’ own video of Bregier talking about his first ride on the A350, he remarks at 3:10 into the video that the next effort is for “the development of the next member of the family, the -1000.” The subtitles alter this to the next “challenge,” but Bregier’s words can clearly be heard. The Youtube post is below, which is the same as the video on the Airbus website.

[youtube=http://www.youtube.com/watch?v=J6yX-1ESX88&w=420&h=315]

Right now, only one A350-800 is scheduled for delivery in September 2016 (to lessor ILFC), according to one data base, with several more following in 2017–when the more popular A350-1000 is scheduled to enter service.

But Airbus’ media relations department says no re-sequence has been made.

“No change in sequence A350-900 EIS H2 2014, A350-800 EIS mid-2016 and A350-1000 mid-2017,” says a spokesperson.

“The video you refer to was intended first and foremost for internal audiences, and Fabrice was referring to the development effort for the -1000 being the next priority as the -800 is a shrink so less effort than the -1000.”

The -800 is a straight-forward derivative of the -900, with several frames removed from the fuselage. The -1000 has some changes to the wing and a slightly different engine fan diameter than the baseline -900.

Analyzing A350 backlog: special to Leeham News and Comment

Special to Leeham News and Comment:

Vinay Bhaskara of Aspire Aviation has provided the following analysis of the A350 XWB sales, on a variety of metrics, exclusively to us.

Analyzing the A350 Backlog

With the recent order for 31 A350s from Japan Airlines, we thought it would be instructive to take a look at the A350’s backlog. To date, the A350 has won 759 orders from 39 different customers (we are excluding Kingfisher Airlines in India and its order for five A350-800s – Kingfisher has been shut down for more than a year now, and it’s chances of re-starting appear bleak).

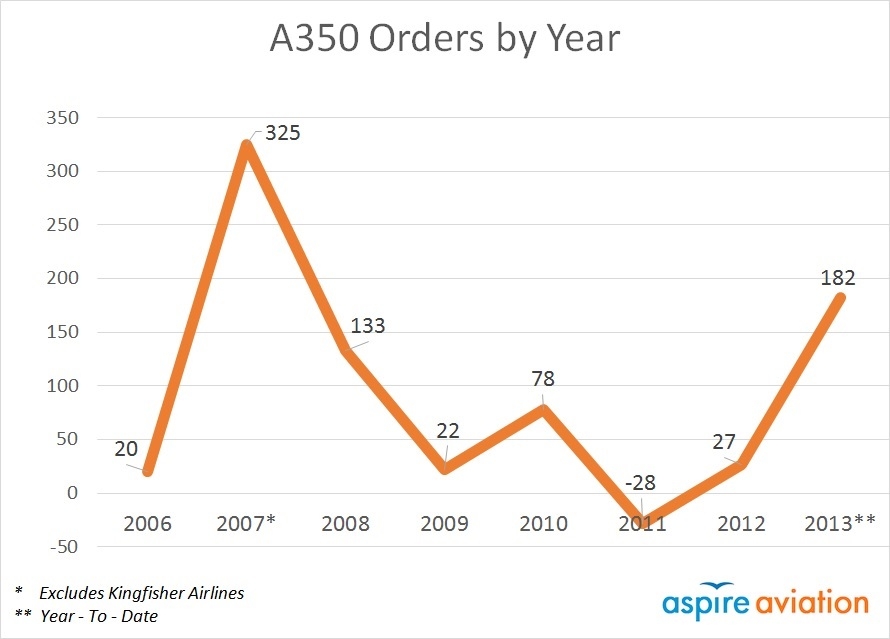

After slow sales in 2011 and 2012, 2013 has been an excellent rebound year for the A350, its second best behind 2007, with 182 orders to date. We expect South African Airways to place its delayed order for the A350s by the end of the year, and there are several upcoming fleet replacement decisions, most notably at ANA and Qantas, in which the A350 is a major player. The chart below shows A350 orders by year since it launched:

Digging further into the backlog, the following two charts discuss the geographic breakdown of the A350’s orders. Asia and the Middle East currently account for more than 55% of the program’s orders, and it has made limited inroads in the Americas relative to the 787.

.