Leeham News and Analysis

There's more to real news than a news release.

CFM LEAP accelerating in test program; Airbus and the A350-800

Aviation Week has a long, detailed story about the test program for the CFM LEAP engine, which is accelerating rapidly.

In its 737 MAX program update yesterday, Boeing said the LEAP-1B has begun testing and it will benefit from the testing already underway for the LEAP-1A, the version that is designed for the Airbus A320neo family. The LEAP-1C for the COMAC C919 is on its original schedule for certification in 2015, despite the fact the C919 has slipped to at least 2017, reports AvWeek.

The 737 MAX is exclusively powered by the LEAP, as is the C919. The former has more than 1,600 firm orders and the latter just hit its 400th order/commitment. CFM faces competition on the A320neo family from Pratt & Whitney’s P1000G Geared Turbo Fan, where PW holds a 49% market share against CFM, which previously held a larger, more dominate position in the A320ceo competition. A large number of orders don’t yet have an engine selection.

PW is the sole-source engine provider for the Bombardier CSeries, the Mitsubishi MRJ and the Embraer E-Jet E2. PW splits the engine choice on the Irkut MC-21 (soon to be renamed the YAK 242) with a Russian engine.

Just as Boeing’s LEAP-1B will benefit from the experience of the LEAP-1A now in testing for Airbus, Airbus will benefit from the testing and experience of PW’s testing of the GTF on the Bombardier CSeries.

Aviation Week also has a story about the Airbus A350-800 with the blunt headline, The airplane Airbus doesn’t want to build. This refers to the A350-800. AvWeek muses that the outcome of the merger between US Airways, now the largest customer for the airplane, and American Airlines, may be the deciding factor for the airplane. We agree. With American’s large order for the Boeing 787-9, the A350-800 would be unnecessary.

That would then leave Hawaiian Airlines as a key decision-maker. We hear in the market that Hawaiian is just sitting back and waiting to see what kind of incentives Airbus will offer to entice a switch to the larger A350-900.

Odds and Ends: AA, US and DOJ have mediator; new C919 order; A380 break even

Movement on AA-US merger: Terry Maxon of The Dallas Morning News reports that American Airlines, US Airways and the Department of Justice have picked a mediator to sort out the DOJ’s lawsuit to block the AA-US merger. See also this Maxon report.

Maxon has a long piece, asking several pontificators (including yours truly) what they think the outcome will be.

Bloomberg reports that American CEO Tom Horton “sees a way” to a settlement but did not elaborate.

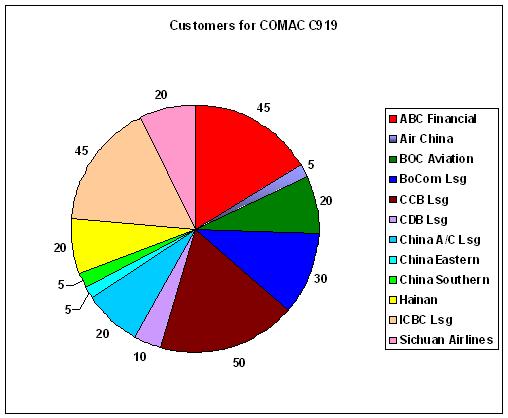

COMAC orders: COMAC says it received 20 more orders for the C919, but it once again is from a Chinese lessor, not an airline. A majority of orders for the C919 are from Chinese lessors, in stark contrast to standard practice among established lessors that they want to see a solid base (or a likely solid base) for a new aircraft type from airlines before signing up.

COMAC orders: COMAC says it received 20 more orders for the C919, but it once again is from a Chinese lessor, not an airline. A majority of orders for the C919 are from Chinese lessors, in stark contrast to standard practice among established lessors that they want to see a solid base (or a likely solid base) for a new aircraft type from airlines before signing up.

Although COMAC says this latest order brings the total up to 400, a data base shows only 275 so far (meaning the other 125 haven’t been converted to firm orders yet).

A380 Break Even: Airbus CEO Fabrice Bregier says hitting break even on the A380 program in 2015, which is the current plan, will be difficult if deliveries fall below the target of 30 per year. Airbus should deliver 25 this year, he said.

Future for the 777, A330 as 777X nears launch, A350 nears EIS

With the launch of the Boeing 777X expected to be approved this month by the Boeing Board of Directors, followed by the public launch at the Dubai Air Show next month, the future sales of the in-production 777 will be closely watched by the industry as well as by Boeing itself.

It is conventional wisdom that sales will fall off as entry-into-service nears for the 777-9X, said to be “late this decade” by Boeing but more likely 2020 or even 2021, according to customers.

Sales of the Airbus A320ceo and Boeing 737NG families have, so far, held up surprisingly well despite the launch in 2010 of the A320neo and in 2011 of the 737 MAX families. Most of the neo and MAX orders have been combined with the current generation aircraft. This has been viewed as a way to keep the production lines full in advance of the EIS of the new airplanes.

Further, Airbus and Boeing plan an overlap of production of the two generations of about two years. This contrasts with Boeing’s decision to cease production of the 737-300/400/500 concurrent with the launch of production of the 737NG, a move Boeing today says was an arbitrary choice.

Boeing plans to begin building the MAX on a third line in its primary Renton (WA) factory before phasing out the NG. Airbus hasn’t specified how it plans to integrate the production of the ceo and neo.

What will happen for the current Airbus A330 and Boeing 777 lines as the A350 and 777X come on line?

Odds and Ends: Airbus to rethink A380 strategy, says Reuters; Boeing B-29

A380 Strategy: Airbus may rethink the near-term strategy of the A380, with an eye toward reducing production rates, reports Reuters. Earlier this week, Boeing announced a rate reduction for the 747-8. Very Large Aircraft (VLA) continue to be a tough sell. YTD, Airbus has net orders of minus three for its VLA, although a Memorandum of Understanding for 20 was signed at the Paris Air Show and is expected to be firmed up by year end and possibly at the Dubai Air Show next month.

Still, the VLA market is very tough. Boeing sold five 747-8s this year and had cancellations of five. Airbus hasn’t met its annual sales target for the A380 for a couple of years.

787-9 Video: In a change of pace, enjoy this video that is nothing but a relaxing visual.

[youtube=http://www.youtube.com/watch?v=eUZmTzPyR-A&w=560&h=315]

,

Boeing B-29: Here’s a sight not seen much anymore: take off and landing of a B-29. As interesting as this is, the weather and the photography is pretty cool, too.

[youtube=http://www.youtube.com/watch?v=3-r8p97vPt0&w=560&h=315]

Odds and Ends: Repairing the Ethiopian 787; more on A350-1000 stretch; new RR engine study

Ethiopian 787: Dominic Gates at The Seattle Times has a detailed story about how Boeing is repairing the Ethiopian Airlines 787 damaged by a fire at London Heathrow Airport earlier this year. Boeing doesn’t comment for the story–nor for any others–but Gates’ detail in his piece makes for quite interesting reading.

Stretching the A350-1000: More on this topic from Aviation Week. Aside from the technical considerations for the airframe, Rolls-Royce would need to bump up the thrust of the engine to around 104,000 lbs, we’re told. Also: there is the matter of production. Airbus is considering a second production line for the A350, but no decision has been made.

Rolls-Royce studies new engines: Rolls-Royce is studying a new line of engines, according to this Bloomberg article.