Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: 787 teething; IAM-777X continues; Boeing in Puget Sound; Dubai Air Show

787 teething issues: Flight Global has this report from the Dubai Air Show in which it quotes Boeing as saying there will be another six months of teething issues on the 787. We hear it will be longer than this.

IAM-777X: These stories will continue for some time. The latest: Reuters has this exclusive interview with IAM International President Tom Buffenbarger, posted Friday. But a Boeing official later denied Buffenbarger’s claim.

Buffenbarger said the IAM won’t make a counter offer; Boeing previously said it has “no plans to re-engage” the IAM. As we noted in our posting Thursday, both sides retreated to their corners in a testosterone posture. Buffenbarger screwed this up. It’s up to him to come up with a counter-proposal.

This from the Dubai Air Show via Twitter:

Boeing exec’s lament quick timing of IAM vote on 777X labour deal, believe members did not “digest” all info completely.

This is more evidence of the completely botched effort. If Boeing is lamenting, then it, too, ought to come back to the bargaining table.

Reuters has this article from Dubai, quoting Ray Conner, CEO of Boeing Commercial Airplanes, saying the ball is now in IAM’s court.

Boeing in Puget Sound: After the IAM vote debacle, the Tacoma News Tribune has a long article (picked up in the Everett Herald) about the future of Boeing’s Frederickson plant, which makes stuff for a variety of 7-Series airplanes. It would have been a participant in the 777X program.

Dubai Air Show: This opens tomorrow; follow on Twitter at #Dxb13 and @Dubaiairshow

Some key articles:

Odds and Ends: Volcano protection; Airbus trims guidance on A350; More on Boeing

Volcano protection: No, we’re not talking about any eruptions from IAM 751. Instead, Airbus and Europe’s easyJet created some man-made volcano ash to conduct tests for detecting the real thing.

Airbus trims guidance: EADS/Airbus trimmed its financial guidance on A350 development costs, according to The Financial Times (free registration required). According to The Times, the entry-into-service of the A350–slated for 3Q2014–“is at risk.” We have EIS in 1Q2015. EADS for now is sticking with the 2014 EIS.

Boeing 777X: As might be expected, there continues to be a lot of news on the 777X.

- Reuters: Boeing vote brings out rivals

- Los Angeles Times: Long Beach seeks 777X

- Wall Street Journal: Boeing moves to evaluation sites

- KING5 (NBC-Seattle): Has a number of stories at this link.

- Seattle Times: The morning after

- Fox Q13 (Seattle): Can Washington lawmakers save the day?

- Puget Sound Business Journal: 777X alternatives hotter climate but cheaper housing

- KUOW (NPR Seattle): What rejection means for unions

Odds and Ends: Right to Work; Middle East influence; latest on Boeing-IAM

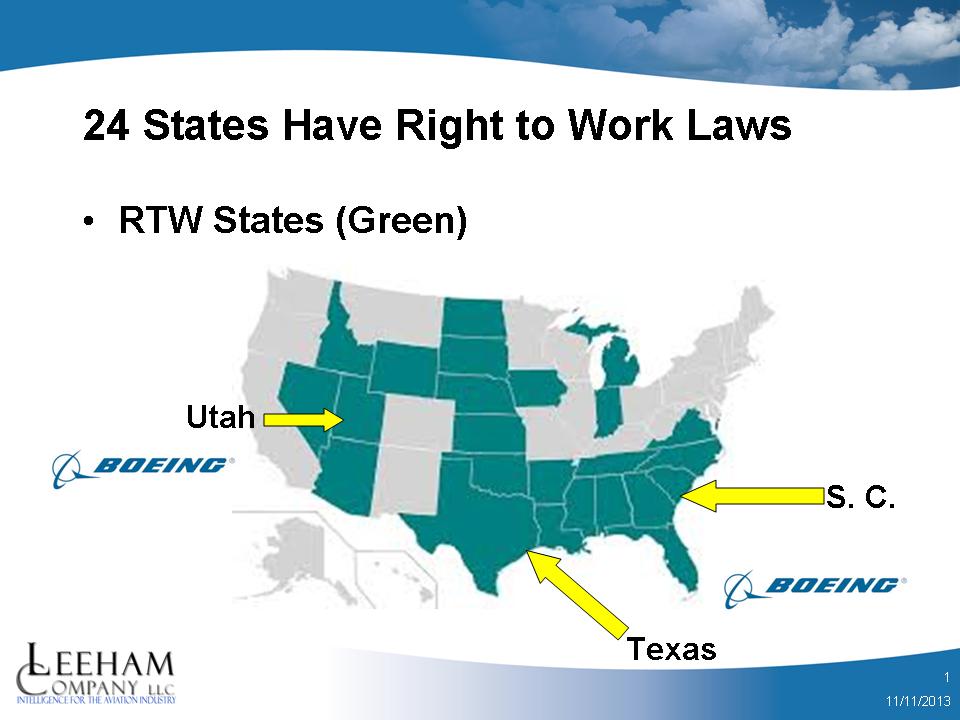

Right to Work or Right to Worse: One of the more controversial issues in the relationship between Boeing and the IAM is Boeing’s continuous threat of removing work from union-heavy Washington and putting it in Right to Work states. South Carolina, of course, is at the top of this list.

KIRO Radio (CBS-Seattle) has a story about a Seattle transplant to Boeing’s Charleston plant who finds some interesting differences between the two locations.

As the IAM prepares to vote Wednesday whether to accept a contract extension that includes significant give-backs in exchange for landing the 777X Final Assembly Line and wing production, Boeing holds the prospect of locating the work in Right to Work states. These have been assumed to be or identified (though not by Boeing) as South Carolina, Texas and Utah. Boeing has facilities in each of these states.

As Readers know, we have suggested Washington needs to become a Right To Work state, which labor characterizes Right To Worse. It’s not that we favor RTW per se (though we do but not dogmatically), it’s more driven by the fact that Washington’s competition is RTW–and Boeing is very effectively using this as leverage over the Washington unionized labor force, and to extension, over the Washington Legislature when it compares our state’s cost of doing business with other states.

Meantime, Boeing has launched its website with its view of the contract proposal.

This is the letter Ray Conner, CEO of Boeing Commercial Airplanes, issued last week.

Middle East Influence: Aviation Week has a good piece about the evolution of the influence of the Middle Eastern airlines on aircraft design. Flight Global has this analysis of the Airbus A350-1000 vs the Boeing 777X in advance of the Dubai Air Show (free registration required).

Boeing IAM-Update: The Seattle Times has the latest from IAM 751 and from Boeing pending the vote tomorrow. Ray Conner, CEO of Bo9eing Commercial Airplanes, said Boeing is “under siege” from foreign competitors, including the Japanese, Chinese and Russians.

Maybe so, but Boeing has been helping these countries and their aerospace industries by outsourcing to them.

We also find it difficult to have sympathy for Boeing at a time when it is posting record profits and undertaking billions of dollars in stock buybacks instead of plowing the cash flow back into research and development instead of designing derivative airplanes.

Airbus lowers range of A350 on increased capacity assumptions

Airbus this week quietly lowered range for the A350 family on increased capacity assumptions.

The range changes appeared without fanfare on the company’s website. When we inquired, a spokesman said,“Seat figures in our public documents have been changed from typical three-class to two-class layouts, as it’s turned out to be a more realistic scenario for most of our customers. Consequently, as passenger capacity has gone up, the new pax numbers and their calculated weight give lower range figures.”

However, as of Thursday’s close of business, the website still refered to three-class configurations:

A350-800 landing page:

The A350-800 is the shortest fuselage version in Airbus’ new A350 XWB all-new family of mid-sized widebody airliners. It accommodates 276 passengers in a typical three-class cabin configuration, with a flight range of 8,250 nautical miles.

A350-900 landing page:

This jetliner typically accommodates 315 passengers in a three-class configuration, while offering unbeatable economics in high-density seating and true long-haul capability with a range of up to 7,750 nautical miles.

The A350-900 Specification page still contained this statement:

The A350-900 offering a typical passenger capacity of 314 seats (in a three-class layout) and operating range 8,100 nautical miles.

A350-1000 landing page:

In a typical three-class configuration, the A350-1000 seats a total of 369 passengers. Combined with a range of 8,000 nautical miles, this represents a significant revenue-generating advantage for operators. The aircraft also can be configured for a higher-density layout to accommodate up to 400 passengers.

The ranges were previously 8,400nm, 8,100nm and 8,400nm respectively. The previous three-class seating configurations listed were 250, 301 and 350 respectively.

By Friday morning (PST), these landing pages had been fixed, and these now refer to two-class configurations with the capacities as listed above: 276, 315 and 369.

Assessing the 777X events for Washington State, IAM, Boeing

Update, Nov. 6, 10:00am PST: A summary by IAM 751 of the contract details is here.

Original Post:

Here’s our take on the news that the IAM and Boeing reached a tentative agreement leading to the selection of Washington State as the assembly site for the 777X, contingent on contract ratification and the Legislature approving an incentive package:

- IAM 751 is both a winner and a loser. Members lose the defined pension plan benefits and pays more for health care benefits. But they keep jobs assembling the 777X, and the siting of the composite wing production here reinforces the expertise of composite development in the Seattle area. These wins outweigh the loss of the benefits.

- Washington State is a winner. This is self evident. The fact that a transportation package is a must–one has been stalled for a long time–not only benefits Boeing but it benefits the state as a whole. Let’s hope the “no new taxes under any circumstances” Republican Party finally wakes up and votes for this thing. These extremists could kill the entire deal.

- Boeing is a winner. It gets labor peace from the IAM through 2024. It gets an experienced, high quality workforce instead of gambling Boeing Charleston–which remains problematic–would be up to the task in five years, when assembly begins. It gets cost reductions on the pension plans and health care benefits.

- Customers are winners. See number 3 re: Everett vs Charleston.

- SPEEA is probably a winner. With the wing and airframe coming to Puget Sound, SPEEA engineers here will certainly get its share of the work, despite the recent announcement that Boeing was putting engineering everywhere but here.

- Boeing Charleston and South Carolina, the presumptive alternative site, are losers. No explanation required.

A big question mark:

As we previously wrote, extending the 787 tax breaks to the 777X through 2040 (with a value of $8bn, more or less) is problematic. These were ruled illegal by the World Trade Organization in the US (Boeing) vs Europe (Airbus) trade dispute claims and counter-claims. The finding is under appeal, but what happens if the finding is upheld? Then what?

Lots to do:

The IAM membership has to approve the tentative contract; a vote is planned next week. Members will have to get past the benefit reductions, offset to some degree by a generous signing bonus and additional benefits for early retirees.

The Legislature has a lot of moving parts to look at in the next week. The challenges are daunting.

Recommendation:

IAM: Although perhaps painful and anathema, ratify the contract.

Legislature: Approve the package, including the new transportation taxes.

Airbus’ A350-800 dilemma

Last week we discussed Airbus’ A350-1000 dilemma. The -1000 will be a fine airplane, but we concluded the company needs to go forward with a larger capacity “A350-1100” to match the size of the Boeing 777-9X, but take the Boeing 787-10 approach and be content with sacrificing range in lieu of designing a new wing and engines.

Airbus’ A350 dilemma doesn’t end there. What’s it to do with the A350-800? One fleet planner told us a year or more ago that the “-800 is an expensive A330-300” with the same operating costs as the larger capacity A350-900.

Airbus has been encouraging customers to move up to the larger A350-900, with Hawaiian Airlines and US Airways the key hold outs. Conventional wisdom says US Airways will swap its order once the merger with American Airlines goes through (which is looking more and more likely, given settlement talks with the Department of Justice). American has a large order for the Boeing 787-9, making the -800 unnecessary in a combined carrier fleet plan.

There are now around 80 -800s in Airbus’ backlog, and even officials at Airbus have been ambiguous about green-lighting production of the -800, which is supposed to enter service in 2016 (after the -900 but before the -1000). We have written several posts in which we concluded the -800 would be re-sequenced to 2018, after the 2017 EIS of the -1000.

We believe there is a very good chance the A350-800 will be dropped in favor of proceeding with an A350-1100.

So what’s Airbus to do in the 250-300 seat space now occupied by the -800 and the aging A330 family?