Leeham News and Analysis

There's more to real news than a news release.

The Airbus A350F versus Boeing’s 777-XF.

Subscription Required

By Bjorn Fehrm

Introduction

August 5, 2021, © Leeham News: Two weeks ago we compared the launched Airbus A350 freighter with Boeing’s in-service 777F. We found the 777F is a freighter with a very high payload capability, but it faces an ICAO emission and noise ax by 2028, should the present engines be kept.

Boeing’s CEO David Calhoun recently said a freighter version of the 777X might replace the 777F. With seven years to 2028, a development decision for a 777-XF is then imminent. We use our performance model to look at how an A350F and 777-XF would compare.

Summary

- A new Boeing 777-XF freighter, based on the 777-8 (picture), has to equal or beat an Airbus A350 freighter both on payload and economics.

- Beating an A350F on capacity and payload is straightforward, the 777-8 is the larger aircraft. On operating costs, it’s a tighter race.

Boeing’s apparent shifting product strategy

Subscription Required

By Scott Hamilton

Introduction

Aug. 2, 2021, © Leeham News: Boeing last week reiterated it believes the 777-9 will be certified and delivered in late 2023. CEO David Calhoun also said, “I’m confident that might be the next of our programs.”![]()

Let’s set aside for the moment whether the EIS prediction becomes reality and assume Boeing will be correct. Let’s assume the 777-XF will be the next program launched. The larger question then becomes, what does this mean for the Next Boeing Airplane (NBA)? And what are the implications for Airbus?

Summary

- The NBA launch seems unlikely in 2022; 2023 may be the target.

- But with the 777-XF moving up in priorities, will the NBA continue to slide to the right?

- What is the Airbus response to an NBA?

- Or, should Airbus move first to further preempt the NBA?

A history of jet freighter aircraft

Subscription Required

By Vincent Valery

Introduction

A Cathay Pacific 747-8F

July 29, 2021, © Leeham News: Last week, LNA compared the performance of the 777F against the A350F, launched today. As a follow-up, we thought it relevant to look at the history of freighter aircraft derived from passenger jets at the major OEMs.

Shortly after the dawn of the jet age, Boeing and McDonnell Douglas started selling freighter variants of their 707 and DC-8, respectively. Most aircraft families developed later at both OEMs would receive a freighter variant in one form or another.

We will stick for our analysis to Freighter aircraft delivered off the assembly line at the world’s Western OEMs: Airbus, Boeing, Lockheed, and McDonnell Douglas.

Summary

- What is a Freighter aircraft?

- A minor but worthwhile market after initial euphoria;

- Single-aisle against twin-aisle;

- A Queen of the Freighters;

- An OEM’s fortress is another’s weakness.

Major upcoming carrier re-fleetings

Subscription Required

By Vincent Valery

Introduction

July 26, 2021, © Leeham News: As passenger traffic in the USA recovers, carriers’ operating cash flow turned consistently positive. With increased confidence in a sustainable passenger recovery, some airlines started ordering or purchasing planes again.

United Airlines 787-10

LNA outlined in a previous article that the pace of passenger traffic recovery differs significantly by region and country. Several domestic markets, notably China and the USA, are back to levels approaching those seen in 2019. Other markets, notably intercontinental or intra-Asia travel, remains depressed.

The carriers that placed large orders undoubtedly did so to capitalize on favorable pricing from OEMs and cheap financing. However, behind the headline-grabbing order figures lie that their fleets are aging fast and had under-ordered in previous years.

LNA singles out in this article the carriers that will have to place sizable orders to rejuvenate their fleets in the next five years, considering regional factors.

Summary

- The 40,000 feet view of re-fleeting needs;

- US carriers lead in old metal needing replacement;

- Potential acceleration of replacement plans in Europe;

- Lower near-term replacement needs in Asia-Pacific.

How good will an Airbus A350F be? Part 2.

Subscription Required

By Bjorn Fehrm

Introduction

July 22, 2021, © Leeham News: Last week, we compared the probable data for an Airbus A350 freighter with the market-leading Boeing 777F. We found the 777F is a heavy-duty freighter with a very high payload capability.

Airbus has to use the A350-1000 toolbox to design something similar. The aircraft would be shorter than a -1000, however, to optimize its efficiency. How much better in efficiency than the 777F would it be? We put both in our performance model and fly them from China to the US.

Summary

- An Airbus A350 freighter has to come close to the 104t payload of the 777F.

- Can it do that, it has convincing economics compared with the 777F.

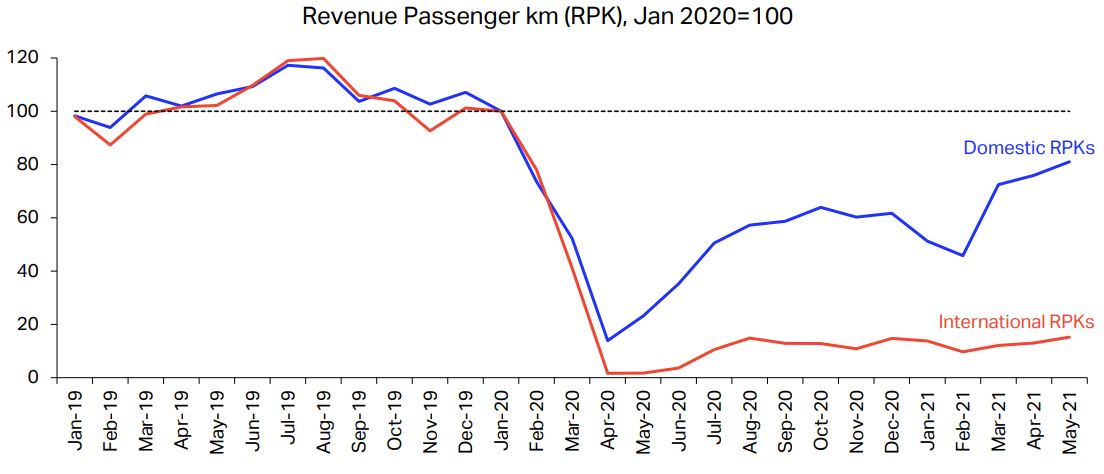

Global airline recovery: LNA’s view shifts from traffic to revenue, but our timeline hasn’t changed

Subscription Required

By Judson Rollins

Introduction

July 19, 2021, © Leeham News: A year ago last week, LNA published what might have seemed an apocalyptic call: global airline passenger traffic would not recover until 2024 at the earliest – and potentially not until 2028.

Early trends and forecast revisions by other parties point to the earlier half of our window. However, one major downside surprise has been an increasingly bifurcated world for airlines as demand returns at widely uneven rates by region and passenger segment.

Air travel is undergoing a “K-shaped recovery” like the global economy, with fairly obvious delineation between winners and losers. The upper leg of the “K” represents countries with large domestic markets, leisure travel, short-haul routes, and low-cost carriers.

The lower leg applies to developing countries, international traffic, business travel, long-haul routes, full-service airlines – and most airline suppliers.

Source: International Air Transport Association.

In hindsight, our prediction probably answered the wrong question, because the key driver of renewed profitability and future investment in commercial aviation isn’t the recovery of airline traffic, but revenue. The many changes to business and long-haul travel make revenue more difficult to forecast, but it will clearly be even slower to return than traffic.

Most industry forecasts don’t call for airline traffic to fully recover until 2024 or 2025, even if large domestic markets recover sooner. That means airline revenue – and profitability – will still be hampered until late this decade.

Summary

- Advanced and developed economies are on widely divergent economic trajectories.

- Global travel recovery statistics are distorted by a couple of large domestic markets.

- Vaccine rollout and documentation issues are likely to keep borders closed for longer.

- Revenue recovery matters more than volume, both to airlines and the aviation supply chain.

How good is an Airbus A350 freighter?

Subscription Required

By Bjorn Fehrm

Introduction

July 15, 2021, © Leeham News: Airbus is working on a freighter of the A350 to compete with Boeing’s larger freighters, such as the 777F.

The 777F is quite a different aircraft than the 777-200LR, which shares its external dimensions, and the 777-300ER that has donated a lot of the internal structure. So will the A350 freighter be based on the A350-900, as the rumors say, or A350-1000? And how good will it be compared to the 777F?

We use our performance model to find out.

Summary

- The A350-900 is the rumored base for the new Airbus freighter that shall compete with the Boeing 777F.

- Is it the correct assumption? When we look under the hood with our performance model, we see it isn’t.

Is the Redhawk Development process the future at Boeing?

Subscription Required

By the Leeham News Team

Boeing wants to converge advanced design and production processes from across the 7-Series platforms and the Defense unit into one commercial airplane–its Next Boeing Airplane, or NBA. Photo: Boeing.

July 12, 2021, © Leeham News: It may be an overstatement to say that Boeing CEO David Calhoun will be the future of Boeing Commercial Airplanes on a radical production makeover.

But it’s not an understatement to say that the production moonshot contemplated is critical to BCA.

However, advanced production processes are only part of the challenge facing Boeing. A radical shift in employee culture is also required for success.

Boeing Defense, Space & Security (BDS) is doing good things with respect to the T-7 Redhawk Trainer Integration. BDS slid the first fuselage together in 30 minutes. But the question before us is this. Is this 30 minute join process a revolutionary process change that Boeing can scale for transport category aircraft, or a byproduct of Great Hardware Variability Control in a simple non-variable end item. Fighter-sized aircraft are simple to build. Highly variable Commercial aircraft are another story completely.

Calhoun, and before him CEOs Dennis Muilenburg and Jim McNerney, would lead you to believe that some new magic occurred in the digital design and that this new magic will transfer to the next Boeing airliner and new engines are not necessary. That’s a bold position to take, so let’s look at what might be involved behind his thinking.

Asia-Pacific airline recovery held back by slow vaccination, border closures

Subscription Required

By Judson Rollins

Introduction

July 5, 2021, © Leeham News: The passenger air travel recovery from COVID-19 has been wildly uneven, even between neighboring countries. Most countries with large domestic markets have seen dramatic rebounds in passenger volumes, although yields have been held back by a continued slump in long-haul and business travel.

Aircraft parked at Hong Kong International Airport, with construction on a third runway in the background. Source: Bloomberg.

In the Asia-Pacific region, however, even short-haul international traffic has been disrupted by virus outbreaks, a painfully slow vaccine rollout, and a largely stagnant web of border closures.

Summary

- Much of Asia is well behind global average in the vaccine rollout.

- Domestic markets in China, Australia, and New Zealand are performing strongly.

- Border closures continue to cripple international travel.

- Many Asian countries are likely to stay closed well into 2022.

- Most Asian airlines are reporting slow progress toward capacity restoration.

China distorts progress in Boeing 737 MAX return to service

Subscription Required

By Scott Hamilton

Introduction

June 28, 2021, © Leeham News: There are now 265 Boeing 737 MAXes in airline service, according to data reviewed by LNA.![]()

There are 263 MAXes in storage that appear to be previously delivered airplanes. This number is artificially inflated by the 95 MAXes that are grounded in China. China’s regulator hasn’t recertified the MAX, a move widely considered political due to the long-running trade war between the US and China initiated by the Trump Administration.

When the MAX was grounded in March 2019, there were 387 in service. The math indicates 147 MAXes were delivered from inventory or new production since the airplane was recertified by the Federal Aviation Administration in November 2020 and other regulators shortly afterward.

There were 400 MAXes in inventory at the end of the first quarter, down from 425 at the end of the year. Boeing resumed production in the single digits. Boeing does not reveal its rate, but it is believed to be about 10-14/mo going to 16/mo in the third quarter.

In contrast, there are 106 A320neos and 38 A321neos in storage as of last Friday.