Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

- Engine makers tout “Plan A” but have “Plan B” backups in R&D June 23, 2025

EADS earnings and Airbus A350, A380 updates

EADS reported its first quarter earnings and in the process reiterated plans to fly the Airbus A350 in June.

Speculation remains rampant that Airbus will fly the airplane in time for the Paris Air Show.

Meantime, sales for the giant A380 languish, with open delivery slots in 2015–the year Airbus has said the program will break even. Like the rival Boeing 747-8I, sales of the Very Large Aircraft have stagnated while sales of the Big Twin engined airplanes have flourished. Airbus, like Boeing on the 747-8, took a huge write off years ago on the A380 program.

Airbus is sticking with its 20 year forecast of 1,300 VLA Passenger sales for Airbus and Boeing, and officially expects to capture 50% of the market. We’ve believed the forecast to be, kindly, optimistic. But the A380 has nearly 90% of the VLAP market and we expect this to remain the case. Airbus might reach its goal of 650 sales over 20 years, but even this is likely to be generous. This are new sales on top of the 272 already sold.

In a lawsuit between Rolls-Royce and Pratt & Whitney a few years back, it was revealed Airbus expected 630-650 program sales, which means about 42% of the sales have already been reached. (It took Boeing nearly 40 years to reach 1,300 747 sales, and for a time the 747 held a monopoly in the “jumbo jet” market). No orders for the A380 have been booked so far this year.

777X for Washington State: Reports Jon Ostrower

The Temporary Surge Line or TSL is prospectively slated for retirement in 2016 to make way for 777X as to not disrupt current 777 production. This plan mirrors a temporary third line in Renton for 737 Max.

But who will design the wing?

So reports Jon Ostrower on his Facebook page.

Washington State to roll out 777X retention plan; here’s what needs to be done

Washington Gov. Jay Inslee will announce today his plan to keep the Boeing 777X assembly here, at the Everett plant where the current 777 series is built.

Inslee previously has said the State needs to pass some additional gas taxes to improve the highway transportation infrastructure. We expect him to talk about this further.

Improving STEM (Science, Technology, Engineering and Math) education has been a goal of Inslee and before him Gov. Christine Gregoire, so we expect more of this.

Tax breaks will likely be a part of his plan. One tax in particular has to go: a 1.9% tax on goods being imported into the Port of Everett; South Carolina doesn’t have this (and, we will guess, neither does Alabama, but we don’t know if it does or doesn’t.)

More of the same.

Beyond these three general areas, we have no idea what Inslee will offer. But we know what is needed for Washington, and these are things that won’t happen.

How Boeing planned installing 787 fix in the field-a worldwide exclusive for CNN

Boeing held at least three press conferences to explain the battery system fix for its 787 and it dropped hints here and there about the teams going into the field to install the fix over a five day period per airplane, but officials never revealed the planning that went into the world-wide effort.

Until now.

We sat down with Boeing Commercial Aviation Services (CAS) last week for a world-wide exclusive on assignment for CNN International to get the story about the planning, the logistics, the mobilization not only of the teams of 300 that deployed into the field but for the first time learned of how Boeing drew from across the enterprise–the “One Boeing–” in greater detail than has been previously revealed.

Sizing up the 777X vs Airbus–and Boeing

It was no surprise that Boeing’s Board of Directors authorized the sales force to begin showing the 777X to customers for sale, as opposed to the concepts. As we’ve reported (and as did others), this move was expected this week. Entry-into-Service (EIS) is slated for late 2019, and will be driven in part by development of the GE9X engine.

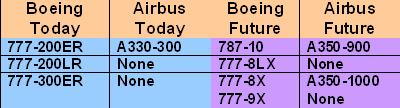

The 777X replaces the 777-200LR and 777-300ER, with the 777-9X at nominally 406 passengers giving Boeing a monopoly position similar to that currently enjoyed by the -300ER. The 8X/8LX is 353 passengers.

.

The 777-9X falls just within the Very Large Airplane category of +400 passengers. We believe this will sound the death knell for the struggling 747-8I. The 747-8 nominally carries 467 passengers but Lufthansa, the only operator so far, configures the airplane for 362-386. The 777-9X will likely be far fewer than 406 in Lufthansa’s configuration but plane mile costs should be far superior to the 748. In high density configuration, the 9X will be solidly in VLA territory.

Update, 900am PDT: Boeing dropped five orders for the 747-8F from ailing lessor Dubai Aerospace. The 8F backlog is now down to 33, plus 26 for the 8I.

Sizing up engine market share on the A320 family

While competition between Airbus and Boeing snares nearly all the headlines and all the “sex,” competition for engine orders is less sexy and receives less attention.

Part of this is because of the increasing trend toward sole-sourcing. The Boeing 737 has been sole-sourced by CFM International since the creation of what is now called the Classic series: the 737-300/400/500. Pratt & Whitney believed at the time Boeing was upgrading the 737-200 that airplanes were up-gauging and bet its future on the Boeing 757 size. It was one of the classic corporate blunders of all time.

Shut out of the 737, P&W joined with Rolls-Royce and MTU to build the International Aero Engine V2500 for the Airbus A320 family. IAE came to the table late, giving CFM a solid head start on the program with a variant of the CFM 56 that powers the 737 Classic and later the 737 NG.

IAE trails to this day, but has done a remarkable job of coming from behind. CFM tends to be favored on the A319 and A320 while IAE is the preferred engine on the larger A321. IAE offers more thrust and better economics on the A321 while the CFM has better economics for the smaller Airbuses. CFM’s reliability is legendary and tends to be better than the V2500.

The blog PDXlight has done a marvelous job of dissecting the engine market share of the A320 family for the New Engine Option. We asked PDXlight to do the same exclusively for us for the A320ceo family. The results are below the jump.

Boeing Board OKs offering 777X

It’s been the worst kept secret of the past few weeks: the Boeing Board of Directors has authorized offering the 777X to airlines. Dominic Gates has this story, and more are coming from The Wall Street Journal, The New York Times and others.

Update, 6pm PDT:

Here’s the WSJ article (subscription may be required).

Here’s the NYT article (we got this off Google News so it should be readily available to anyone).

Update, 7pm PDT: Dominic Gates has more information, including where the 777X might be built