Leeham News and Analysis

There's more to real news than a news release.

Airbus comes up for air, responds to Boeing’s Form 41 reliance

Airbus came up for air from the Paris Air Show and provided this response on the DOT Form 41 debate. Readers can now compare closely Boeing’s response to our queries with the Airbus response and draw their own conclusions. As with Boeing, we print their verbatim replies to our questions.

DOT form 41 Maintenance cost comparison

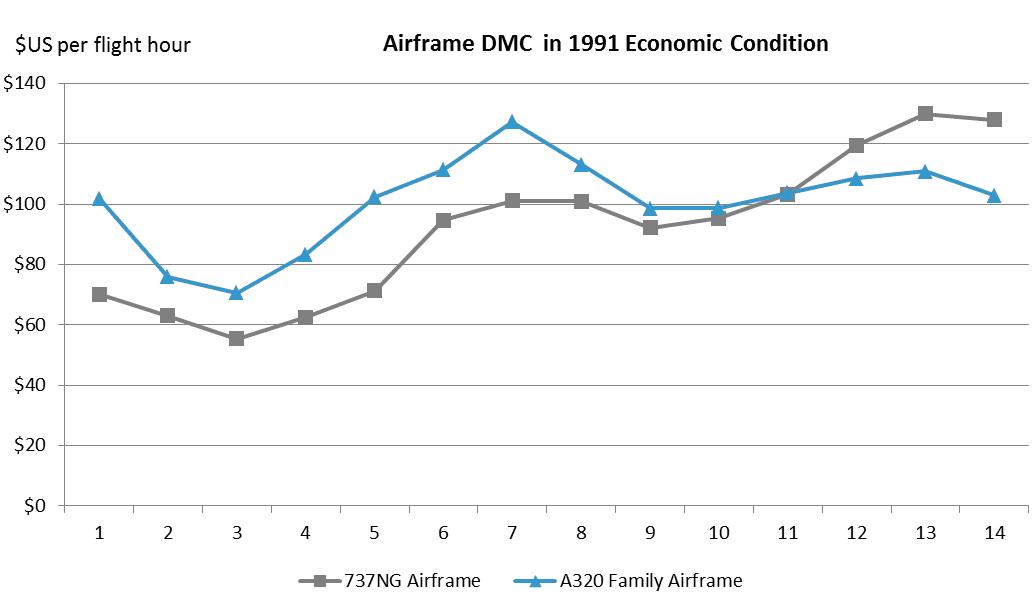

Boeing uses F41 data of the period 2004 to 2011 to demonstrate lower maintenance cost of the 737NG compared to the A320. Without debating about the relevancy of F41 data for aircraft maintenance performance and the “correctness” of the data, let’s have a look at the reported F41 data from the point in time when the A320 entered the US market (1991).

We see why Boeing is focusing on the 2004 to 2011 period, the reported data are at the first glance favourable for the 737NG.

However, the NG entered in the market in 1998, seven year later than the A320, hence at any point in time the graph compares aircraft with at least a seven year age difference. Is this a “like for like” comparison?

Let’s just shift the 737NG curve to the left, starting in the same year than the A320, in 1991:

The picture does now look quite different, but money over time does not have the same value and this is in the above graph penalising the NG.

To be fair the reported cost data need to be harmonised respecting the economic conditions. Let’s put all reported data in year 1991 economic condition:

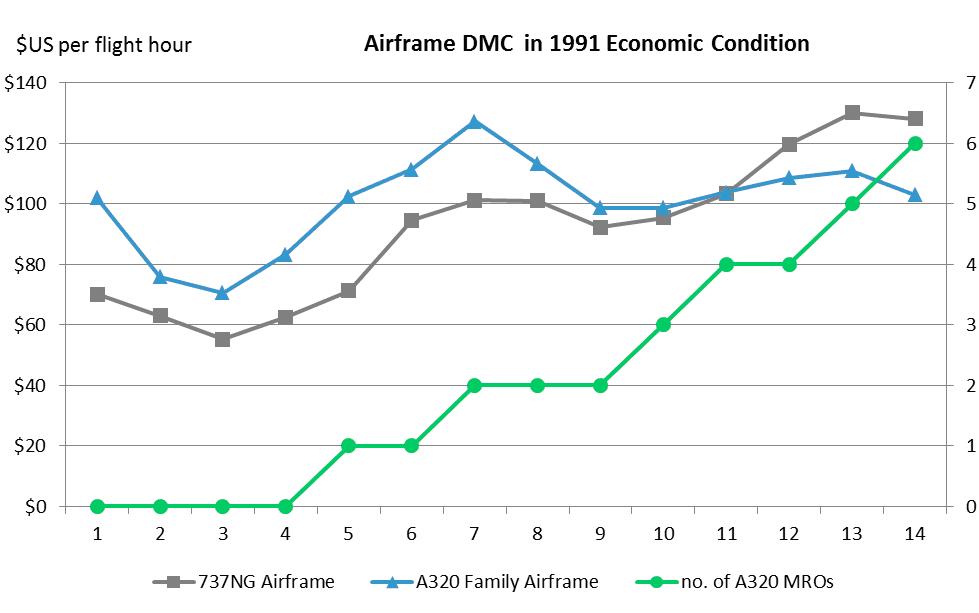

At the time A320 entered the US market barely any MRO capacity was in place. This has changed over the years and from a certain point in time MROs started to make money with performing maintenance work on the A320. Competition started to take place between the MRO’s, which impacted the pricing of maintenance work in reducing the money spent for the operators. For the NG the maintenance market condition has not been the same. Due to the derivative nature of the NG to the 737 Classic a wide MRO base has been proposing maintenance work on the NG right form the entry into service in 1998.

The graph below illustrates this effect in showing the evolution of independent MROs in the US market.

![]()

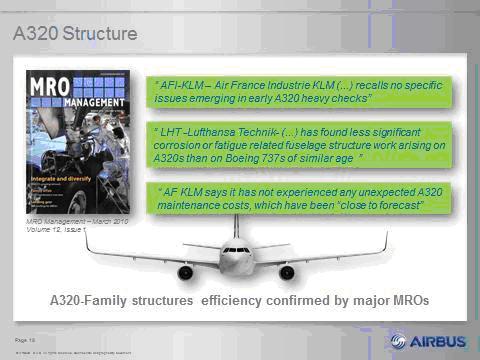

Another fact leads to lower maintenance cost for the A320 compared to the NG. It is the solid structure, which has been fully fatigue tested during the certification of the aircraft. An advantage the NG does not have, because again due to the derivative nature of the NG compared to the Classic, no full fatigue test has been performed and certification of the airframe has been obtain by “grandfather rights”.

Some quotes from leading MRO’s illustrate the well maturing structure of the A320:

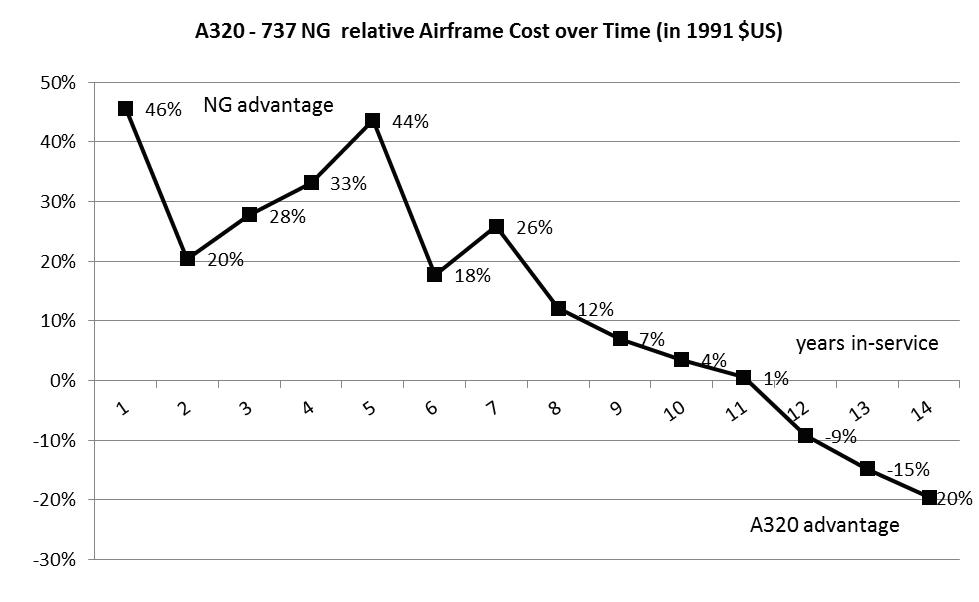

Conclusion:

· Instead of focusing on the “sweat spot” for the NG, data of the entire reporting period must be compared

· Comparing different fleet ages is not leading the sensible results

· Market forces e.g. competition have an impact on maintenance cost

The A320 airframe is better maturing than the NG and improvements on the A320 are showing tangible results.

Paris Air Show wrap; and other Odds and Ends

It’s over and here are the Airbus and Boeing press releases, followed by some Odds and Ends:

Airbus books almost US$70 billion at Paris Air Show 2013

· 466 Airbus aircraft orders & commitments across all product families;

· A320neo Family retains 60 percent market share;

· A350 XWB, A330 and A380 all continue to outsell the competition.

At the 2013 Paris Air Show, Airbus won US$68.7 billion worth of business for a total of 466 aircraft, which shows the resilience of the commercial aviation industry. The deals comprise Memoranda of Understanding (MoU) for 225 aircraft worth US$29.4 billion and firm purchase orders for 241 aircraft worth US$39.3 billion.

The A320 Family, spearheaded by the A320neo, continues its trailblazing success in the single-aisle market with 371 orders and commitments from six customers announced at the show, worth approximately $37.8 billion. Of these, 88 were for the A320ceo – showing that today’s in-production aircraft is still the most sought-after industry workhorse. A stand-out commitment during the show for the A320 Family was the announcement from easyJet for 100 A320neos plus 35 A320ceos – the winning result of a very intense competition. Another major endorsement for the A320 Family came from Lufthansa with the firming-up of 100 more aircraft. Additional A320 Family orders and commitments came from: Hong Kong Aviation Capital for 60; ILFC for 50; Spirit for 20; and Tunisia’s Syphax Airlines for three – significantly the first A320neo commitment from Africa.

Another star at Paris was the A350 XWB which flew for the first time on Friday 14th June 2013 and successfully completed its second flight on Wednesday 19th June. At the show this aircraft gained 69 more orders & commitments worth $21.4 billion from four customers on different continents. Air France-KLM placed a firm order for 25 A350-900s. Meanwhile, Singapore Airlines, already a large customer for the type, returned to order 30 more A350-900s; United Airlines also placed an additional A350 order for 10 A350-1000s — not only bringing its total A350 orders to 35, but also upgrading its previous order for 25 A350-900s to the larger A350-1000 model to replace its Boeing 777s. In addition, Sri Lankan signed a commitment for four A350-900s to complement an order for six A330-300s at the show.

At the top end of the product range, the flagship A380 received a commitment for 20 aircraft from the world’s third largest wide-body lessor, Doric Lease Corp, in a deal worth more than $8 billion. The contract with Doric is significant as it opens up a new, additional route to market for the A380, which is now available to airlines who wish to acquire the aircraft under the flexibility of an operating lease agreement.

John Leahy, Airbus’s Chief Operating Officer, Customers said: “The dramatic rainfall and thunder storms at Le Bourget this year didn’t dampen our order intake.” He added: “Our A350 XWB has been out-selling the 787 by better than 2- to-1 over the last five years. In addition our A320neo Family retains a 60 percent market share lead. That’s a ‘corner’ I want to stay boxed into.”

Boeing Launches New Commercial Airplane; Highlights Innovation, Efficiency and Partnerships at 2013 Paris Air Show

LE BOURGET, France, June 20, 2013 –Boeing (NYSE:BA) enjoyed a strong and productive Paris Air Show launching its newest model, the 787-10 Dreamliner, announcing important commercial airplane orders and strengthening alliances and relationships with customers and partners around the world.

“The 50th Paris Air Show has been important for Boeing with a number of historic milestones,” said Charlie Miller, Vice President of International Communications. “Our airline customers have strongly endorsed Boeing’s innovative family of commercial airplanes with outstanding orders and the launch of our latest 787 Dreamliner model.”

“The excitement and enthusiasm among customers, partners and suppliers for the products and technologies Boeing showcased across the commercial and defense businesses validated our commitment to innovation and customer focus,” said Miller.

Boeing highlighted its family of efficient commercial airplanes in both the single and twin-aisle market segments. The 787-10 Dreamliner was launched with 102 orders and commitments from five customers, including Air Lease Corporation (30), GE Capital Aviation Services (10), International Airlines Group / British Airways (12), Singapore Airlines (30) and United Airlines (20).

The new 787-10 covers more than 90 percent of the world’s twin-aisle routes with seating for 300-330 passengers. Design of the 787-10 has already started at Boeing and international partners will be involved in detailed design in the months ahead, with first delivery targeted for 2018.

The innovative 787-8 Dreamliner in Air India livery flew for the first time at the Paris Air Show, and the Qatar Airways 787 on static display attracted hundreds of customers, partners, government officials and news media. The ScanEagle unmanned aircraft system, produced by Boeing subsidiary Insitu, was part of the U.S. Corral display throughout the show.

Over the past week, customers have demonstrated their strong confidence in the full family of Boeing commercial products – the Next-Generation 737, 737 MAX, 787, 777 and 747-8, announcing orders and commitments for 442 Boeing airplanes, valued at more than $66 billion. Additional orders for 20 Next-Generation 737s and 20 737 MAX airplanes from unidentified customer(s) were posted on the Orders & Deliveries website today. The number of Boeing net orders for 2013 currently stands at 692.

Boeing announced during the show key partnerships with Embraer on the sales and marketing of Embraer’s KC-390 medium-size transport, and with Sikorsky on a joint venture to compete for sustainment services in support of the Kingdom of Saudi Arabia’ s rotorcraft fleet. The U.S. Marine Corps V-22 Program Manager reported that operational success of the Bell-Boeing tilt-rotor played a key role in the recent award of a $6.5 billion multi-year contract for 99 aircraft. Boeing also announced that work has begun at Le Bourget on a $354 million Mid-Life Upgrade contract with Air France Industries to upgrade four French E-3F Airborne Warning and Control System (AWACS) aircraft.

Customer announcements this week

(Note that Boeing is including a May 31 announcement from TUI in this tally–Editor)

|

Customer |

Quantity and Model |

Approx. List Price Value |

Status |

|

(60) 737 MAX |

$6.1 billion |

Commitment |

|

|

(4) 737 MAX |

$400 million |

Commitment |

|

|

(10) 787-10 |

$2.9 billion |

Commitment |

|

|

(2) 777-300ER (7) 777-300ER |

$2.8 billion |

Firm order (2) Commitment (7) |

|

|

(30) 787-10 (3) 787-9 |

$9.4 billion |

Commitment |

|

|

(12) 787-10 |

$3.5 billion |

Commitment |

|

|

(30) 787-10 |

$8.7 billion |

Firm order |

|

|

(20) 787-10 |

$5.8 billion |

Firm order |

|

|

(5) 747-8 Intercontinental (6) 777-300ER |

$3.6 billion |

Commitment |

|

|

(30) 737 MAX 8 |

$3.0 billion |

Firm order |

|

|

(175) 737-800 |

$15.6 billion |

Firm order |

|

|

(5) 737-900ER |

$473 million |

Firm order |

|

|

(3) 737 MAX 8 |

$301 million |

Commitment |

|

|

(20) 737 (20) 737 MAX |

$3.8 billion |

Firm order |

* First announced by customer on May 31

Odds and Ends

Embarer has good show: Embraer launched its E-Jet E2 with 375 orders and commitments, most for the E-175-E2 75 seat model.

Aerodynamics of the goose in flight: The video is a hoot (or should we say honk); you will enjoy this a lot.

By your finger tips: If you thought the video was a hoot, get a “load” of this story.

787-9F: Boeing plans to make a freighter, some day, of the 787-9.

Boeing’s future in Puget Sound, Washington–maybe Airbus, too

Yesterday we opined that the Boeing “exodus” from Washington State is a tad overblown so far. Here’s why we think so.

- As long as the airplane programs are derivatives of in-production aircraft, Puget Sound’s place in aerospace is solid. We don’t think the 777X will be assembled anywhere but here, just as MAX–a derivative of the 737 NG–was certain to be assembled here (and it was). The debate, such as it was, over where to assemble the MAX was in our view nothing more than making the airplane a pawn in the labor dispute with IAM 751 and the NLRB lawsuit over the second 787 assembly line. IAM dropped the suit in exchange for the MAX. Or so it appeared.

- So what if the 787-10 is assembled in South Carolina? Boeing has to take production to 14 a month, in our view, in order to accommodate the 787-10 and to open up delivery slots for the 787-9 and 787-8. We think this means seven 787s a month at Everett and seven at Charleston.

- Demand for the 737NG and 737 MAX is such that Boeing has to take production rates higher. The Renton factory has the capacity for 63/mo.

- Demand for the KC-46A tanker may boost rates on the 767 line. Also, as we previously reported, Market Intelligence tells us FedEx is preparing to order the civilian freighter version of the KC-46A, the 767-2C. This also means higher rates.

- In fact, our Market Intelligence tells us Boeing is already reaching out to the supply chain to plan on production boosts for the 737, 767 and 787 lines.

Source: Leeham Co. Market Intelligence. 777 and 747 rates not included.

Will Boeing continue to shift jobs from unionized Washington to non-union states? You betcha. But if these production rates come to pass (and the supply chain will have to gear up to meet these rates), not only will Boeing be adding jobs but so will the suppliers.

Airbus is talking to suppliers about similar rate hikes. For Washington, this means more jobs, to0, because our state is the No. 2 US supplier to Airbus by company count.

The Seattle Times reports that Airbus may consider opening an engineering center in Washington.

Note the comment about the USAF tanker in the story. We asked Gov. Jay Inslee about his relationship with Airbus during a conference call Wednesday, the final one held by the State to recap its daily activities at the Paris Air Show. Inslee bowed out of the trip to deal with Washington’s lack of a budget.

When he was in Congress, Inslee was one of the most vociferous opponents of the Airbus/EADS bid for the USAF tanker in competition with the Boeing KC-767. Inslee introduced legislation to require the Air Force to take into account WTO findings that Airbus received illegal subsidies for the A330, the plane on which its tanker design was based. Even the US Trade Representative’s office said such legislation violated WTO rules and the effort went nowhere.

Inslee’s efforts at the time offended Airbus officials, who were considering holding a suppliers fair in Washington, which is the No. 2 US supplier to Airbus. Because of the vitriolic opposition by Inslee and other members of the Washington delegation, Airbus shelved consideration of the fair.

We asked Inslee Wednesday how he might mend fences now that he is governor, seeking to expand our supply chain business with Airbus. Inslee was beginning to answer when US Rep. Rick Larson, who was leading the State’s Paris Air Show delegation in Inslee’s absence, interrupted to say he had talked with McArtor, who said the tanker wars were over.

Airbus has a suppliers event scheduled here next month.

Boeing’s “exodus” from Washington State a tad overblown–so far

Boeing has been eliminating thousands of jobs–union jobs–in Washington State and moving them to other states–non-union states.

Boeing won’t say where it will assemble the 777X. Nor will it say where it will assemble the 787-10.

So, predictably, new hand-wringing has begun among local officials and state politicians that Boeing is leaving the state. An “exodus,” in the headline over an OpEd piece in The Seattle Times by State Sen. Mike Hewitt, a Republican.

There is much in Hewitt’s piece with which we agree. Just yesterday we commented that Washington leaves a lot to be desired in its competitive stance against the Southern States. In May we offered specific ideas of what needs to be done.

The State’s new Aerospace Strategy, unveiled in May, reads more like a history than a forward-looking document. And as a state aerospace strategy, it’s woefully lacking in innovation or looking beyond Boeing to the rest of the aerospace industry. Washington’s supply chain is the No. 2 supplier by company count to Airbus and No. 6 by dollar volume. Yet the Aerospace Strategy doesn’t detail how to increase this business with Airbus, nor does it address the rest of the global business opportunities except in the most general way.

Hewitt is right that there is little to really point to in Washington’s strategy. But Hewitt omits the biggest sin of his own party: the Republican budget proposal eliminates funding for the Governor’s Office on Aerospace, which was created less than a year before.

That was a dumb move, and it hardly supports Hewitt’s decrying the shortcomings of the Democratic governors he is so keen to criticize (with justification, we repeat).

Washington’s Legislature, like Congress, is divided, and we’re at a budget impasse. The Office of Aerospace funding is in the Democratic budget, and the contrasts haven’t been resolved. Hewitt needs to buck his party and put this funding back. (Maybe he’s done so, but he certainly didn’t mention it in his OpEd piece.)

But there’s more in the flaw of Washington’s aerospace strategy.

Paris Air Show, Day 3: A320, 737 production rates of 50+ seen

Highlights from the show, as we see it:

- Boeing said the entry-in-service for the 737 MAX will be accelerated from the fourth quarter 2017 to the third quarter. Southwest Airlines of the USA is the first operator. Bloomberg reported this is a six month acceleration, but we believe this is no more than three months at the outside. We had EIS for October 2017. Ascend data base shows the first delivery now for September 2017 and a total of four in 2017, the latter unchanged from when we wrote a story for Flight Global about the order from Southwest.

- Update on the above item: Boeing has clarified that citing “six” months was a mis-speak; the EIS moves from Q4 to Q3 [along the lines we’ve written–editor].

- The long-awaited order for Airbus A350s from Air France finally happened.

- Ryanair firmed up its order for 175 737-800s.

- Airbus says it’s alerted suppliers about the prospect of boosting A320 production to 50/mo by 2020. Boeing didn’t reveal at the air show (as far as we can tell from news reports) but our Market Intelligence tells us that Boeing has alerted suppliers about the prospect of boosting 737 production to 52/mo by 2019.

- For all the hoopla of the Embraer E-Jet E2 launch, most of the orders and commitments were for the smallest E-175 E2.

Paris Air Show, Day 2

To us the biggest news coming out of Day 2 was not the launch of the Boeing 787-10–this was widely expected–but the suggestion by Boeing CEO Jim McNerney that he might seek a waiver to the mandatory age 65 retirement to hang around a bit more.

We comment on this in another post.

Otherwise, today was pretty anti-climactic: Airbus won easyJet–this had been reported as likely. Boeing launched the 787-10 with the expected launch customers. Boeing added five sales to the largely dormant 747-8I program. The Wall Street Journal has a somewhat cheeky view of Airbus’ sales targets, with Boeing’s Randy Tinseth predictably churlish.

And it rained and rained and rained. We’re glad we’re in Seattle.

McNerney may seek retirement waiver: our view

Boeing’s Jim McNerney may seek a waiver to the mandatory retirement age of 65–he’s 64 this year–to continue as chairman and CEO.

As soon as the news was out, we got a call from one Wall Street analyst who opened the call by saying, “Short the stock.” We initially thought this was some solicitation call.

We’re not that pessimistic but we do have these observations:

- McNerney staying beyond 65 is good news for Charleston, where Boeing is increasing its presence at a rapid rate. McNerney has a clear affinity for South Carolina: its local, county and state governments seem to have an open check book for Boeing. And it’s non-union and has lower wages. As long as McNerney is CEO, Charleston will continue to grow rapidly.

- It’s bad news for the unions. He just doesn’t like them. We don’t really need to pontificate on this point. Boeing is cutting back on union jobs here and transferring the work to non-union locations.

- It’s generally bad news for Washington State. It’s pretty clear that McNerney isn’t a fan of this state, given it’s costly to do business here, wages are higher, environmental rules are stricter and the State hasn’t exactly been innovative when it comes to thinking up stuff with which to incentivize Boeing. Gov. Christine Gregoire, like Gary Locke before her, pretty much took Boeing for granted until the company used the proverbial 2×4 upside the head to get their attention. Gov. Jay Inslee, Gregoire’s successor, so far has offered up more of the same to “win” the 777X assembly: more workforce training, better infrastructure and faster permitting–all-in-all, not at all innovative or outside-the-box thinking.

- More blackmail for Washington: Boeing has always been good at prying concessions out of states and local jurisdictions. McNerney has elevated this to an art. Assemble the 737 MAX derivative in Renton? Of course, said Jim Albaugh, CEO of Boeing Commercial Airplanes. Not so fast, said McNerney, in a highly public and humiliating rebuke to Albaugh (who was gone within the year after this faux pas). Assemble the 777X derivative here? Don’t count on it, says McNerney. Assemble the 787-10 derivative here? Don’t bet on this, either. In the end, the MAX was located here, but we think that was payoff to labor (which also gave in return) in exchange for dropping the NLRB 787 lawsuit. Without this card, it’s up to the State to be blackmailed for more incentives (we really don’t think Inslee’s package is worth much on 777X).

We were pretty happy with McNerney’s ascension to chairman and CEO after the disastrous rule of Phil Condit and Harry Stonecipher. But McNerney’s performance throughout the 787 and 747-8 debacles was wanting, we (and many others) concluded. We think McNerney was slow to make changes in these programs, and he was on the Board of Directors who signed off on the McDonnell-Stonecipher-driven outsourcing approach on 787 that proved so disastrous. McNerney has been at war with the unions, who saved Boeing’s bacon during these programs. We certainly understand the need to control costs and we opined a lot on the medical and pension cost issues, generally coming down on the side of the company. But we can’t help but sense ingratitude from Chicago for all the hard and dedicated work performed here in Puget Sound.

Most significant, perhaps, is the thin bench there is to succeed McNerney. Shortly after he became CEO, McNerney said one thing that was his priority personally and professionally was to create a good succession plan. Who is there from within to possibly succeed McNerney in a year or 18 months? The answer is, at this point, nobody.

Ray Conner is well regarded, but he probably needs a couple of more years than a McNerney retirement timeline suggests. Pat Shanahan hasn’t any commercial sales experience. Dennis Muilenburg has no BCA experience.

McNerney may well have to get a waiver because so far he has utterly failed to have a succession path.