Leeham News and Analysis

There's more to real news than a news release.

A350 XWB program update at the PNAA conference

Daniel Wenninger, senior director of the Airbus A350 XWB program out if the Airbus Americas office, appeared at the 2014 Pacific Northwest Aerospace Alliance conference last week in the Seattle area.

http://www.youtube.com/watch?v=8RdszdH0egE

.

[youtube=http://www.youtube.com/watch?v=QMyM5NLu3V8]

.

[youtube=http://www.youtube.com/watch?v=1YNb0UFKiMw]

Simon Pickup of Airbus Americas joins Wenninger for questions and answers.

[youtube=http://www.youtube.com/watch?v=eMtO4AfpZB4]

Development of the GE9X for the Boeing 777X

Jason Brewer, general manager of GE Commercial Engines Marketing, appeared at last week’s Pacific Northwest Aerospace Alliance 2014 conference on the Big Engines panel.

Brewer discussed the development of the GE9X for the Boeing 777X, outlining the new technology going into this big engine for Boeing’s latest 7-Series aircraft.

One slide–which is available to the conference attendees–showed a market forecast of 3,000 aircraft in a context that appeared to suggest GE sees a market of this number of airplanes for the 777X. We clarified this with Brewer after the panel; the forecast is for the 350-400 seat sector. Brewer told us that GE hopes to capture 1,700 of these aircraft.

This is the first time we’ve seen this sub-sector broken out–Airbus and Boeing typically forecast for the larger 300-400 seat sector in their 20 year forecasts. Airbus and Boeing have previously indicated they think the demand for the 400-seat aircraft (i.e., the 777-9X) is between 670-780 respectively.

The sound is pretty soft on this. It will best be heard with headphones.

Boeing’s Randy Tinseth provides mythbusting assessment at PNAA conference

Boeing’s vice president of marketing, Randy Tinseth, appeared at the annual Pacific Northwest Aerospace Alliance conference this week in the Seattle area. He talked about Boeing’s annual Current Market Outlook update as well as taking a light-hearted approach to some mythbusting, a la the television show.

http://www.youtube.com/watch?v=b4cSIkbCP5M

http://www.youtube.com/watch?v=nqXvG0Kh8Ho

http://www.youtube.com/watch?v=Ki2ps2Lt7-k

Richard Aboulafia analyzes state of industry, opines on A380neo, what it works for Emirates and other stuff

Richard Aboulafia, an analyst for The Teal Group, is a headline speaker at the Pacific Northwest Aerospace Alliance every year. Below are a series of videos of his presentation this year.

He provides an overview of the commercial airline industry in one, and addresses specific issues in others, such as the prospect of an Airbus A380neo. Aboulafia has been a long-time critic of the A380 but he also remarks why this airplane works for Emirates Airlines, its biggest user.

Aboulafia also talks about a variety of other issues, including remarking on Boeing’s cost-cutting Partnership for Success program, which has resulted in a ” no fly” list of Boeing suppliers unwilling (or unable) to cut costs to Boeing’s liking.

Odds and Ends: A boost for the A330? Problems continue at Boeing Charleston

A boost for the A330? Aviation Week reports Airbus is offering China an A330 completion center in return for an order for 200 A330s. At the current production rate of 10/mo over the Airbus production year of 11 months, this is nearly two more years on to the current 27 month backlog.

Problems continue at Boeing Charleston: The Seattle Times has a long piece about the continue problems at Boeing Charleston, the 787 plant there.

Updating the A380: the prospect of a neo version and what’s involved

Recent headlines and this column report that Airbus is considering re-engining the popular A330 with GE Aviation GEnx or Rolls-Royce Trent 1000-TEN power plants. A New Engine Option and other changes would improve the A330’s economy by an estimated 10% percent after offsets for increased drag and weight.

But the A330 isn’t the only Airbus airplane being considered for new engines made popular by the A320neo family. Tim Clark, president and chief operating officer of Emirates Airlines, urged Airbus to improve efficiency of the giant A380 with engine technology found in newer generation aircraft.

How feasible is an A380neo? What are the technological issues? Would there be enough of an economic gain? And is there a market for an A380neo?

The A380 of today

The A380 has been hailed as a highly efficient airliner since it went into service 2008, assuming the giant plane can be filled. But only six years later, the first voices have been raised that this will not continue to be the case should the continuous improvements that have been flowing into the airframe not pick up speed.

The launch of the Boeing 777X also brought focus on the state of the A380 come the latter part of this decade when the 777-9X enters flight testing in advance of its planned 2020 entry-into-service. Tim Clark expressed that “it is time that the A380 gets an injection of the new technology which is now becoming available for the A320/737 in the form of GTF/LEAP and GE9X for the 777X. “

Before we look into what can be done short-to–mid-term to inject improved efficiency, let’s establish the baseline as it exists today. The A380 is considered by some the most efficient way of flying passengers between two long haul points if there is enough of demand. The competition today is the Boeing 777-300ER and 747-8i. (Qantas Airways is dropping some A380 flights that have 50% load factors, demonstrating the aircraft is inefficient if the demand is insufficient.)

Let’s assume we want to transport passengers between San Francisco and Hong Kong, one of the longer flights which are made non-stop in both directions. Going West, it takes a Cathay 777-300ER 15 hours and going East, 12 hours, the difference being due to prevailing headwinds going West. For our check, we will use the more demanding of these legs, which then works out as the equivalent of flying 7,200nm. To compare the three different aircraft in a fair way, we need to load them to the same payload, in our case passengers with luggage. We will not consider cargo in this initial analysis. The leg chosen is not one which allows much weight for cargo, but cargo certainly belongs to a complete analysis of an airplane and we will point out where it will affect any conclusions.

When comparing the standard three-class seating numbers between the OEMs, it is clear these are not made to the same standards of comfort. Airbus has admitted that the A380 is too lightly loaded at 525 passengers. The 777-300ER at nine abreast and 365 seats is equipped with a comfortable 18’’ economy class at 32’’ pitch but the business class is modeled with a non-standard 48’’ pitch. The 747-8i at 467 seats is not laid out to any comfort standards comparable to the other two. To ensure an apples-to-apples comparison we have equipped all aircraft with the same three-class cabin with a standard seating consisting of first class at 81’’ pitch, business class at 60’’ pitch and economy class with 32’’ pitch. Seat widths are 37’’, 22’’ and 18’ respectively and the ratios of the different premium seatings vs. economy are kept the same. Here the aircraft are listed with the in-service year and with their respective payload capabilities:

Odds and Ends: A330neo decision could be near; KC-46A; Countdown to Superbowl; A400M

A330neo decision: Aviation Week reports that a decision to proceed with the Airbus A330neo could be “imminent.” The report also discusses the advocacy by Tim Clark, COO of Emirates Airlines, to re-engine the Airbus A380. As with the Reuters and Bloomberg articles we previously linked, the Aviation Week piece also confirms much of what we were the first news outlet to report in December. We have a launch in 2014 rather than 2015 reported in Aviation Week, although we both have a decision to proceed for this year. Aviation Week and Bloomberg report that the decision could come as early as March.

Aviation Week confirms our report that Pratt & Whitney would be unlikely to bid on the project because the short time lime precludes development of the big engine version of the Geared Turbo Fan.

KC-46A at ‘high risk’ for delay: A US government report suggests the Boeing KC-46A tanker is at ‘high risk’ of a six month delay.

These are not unusual for military programs, nor, it seems, is it any longer unusual for new or derivative aircraft programs. Boeing believes the program is on time, but even if a six or 12 month delay does emerge, by today’s standards, this indeed is “on time.”

Countdown to Super Bowl: Boeing painted a Boeing 747-8F test plane in the Seattle Seahawks livery and this week “skywrote” the number 12 on a flight. The Seahawks play the Denver Broncos Sunday in New Jersey for the Super Bowl. The number “12” represents “the 12th man,” of the collective Seahawks fan base.

We think it would be super for the 747 to overfly the game Sunday, the ultimate 12th man appearance. Alas, Boeing says there are no plans to do so.

A400M: Cool picture. No other words needed.

Odds and Ends: A330neo; The 12th Man; Boeing’s earnings

Clearing the air on the A330neo, again: Bloomberg News has an extensive story on the prospective development of the A330neo. Following a report from Reuters, these two news articles basically confirm everything we reported in December.

The 12th Man: The Seattle Seahawks, which plays in the Super Bowl Sunday against the Denver Broncos, is well known within the National Football League for its “12th Man.” This is the fan base which has set records for being the loudest fans in football, at a record 137db. They’ve also been recorded on the Richter Scale for their stomping at the Seahawks’ Century Link Field (that’s a local phone company, and the name is routinely shortened to “the Clink”).

Boeing is a corp0rate sponsor of the Seahawks and rolled out its 747-8F house test plane in a new Seahawks livery.

Boeing’s earnings: Boeing reported its 2013 earnings and while they were a record profit, the forecast disappointed and the stock took a major hit Wednesday. The Seattle Times has the recap.

Odds and Ends: ATR presses parent Airbus for 90 seat go-ahead; Stratoliner; 777 model

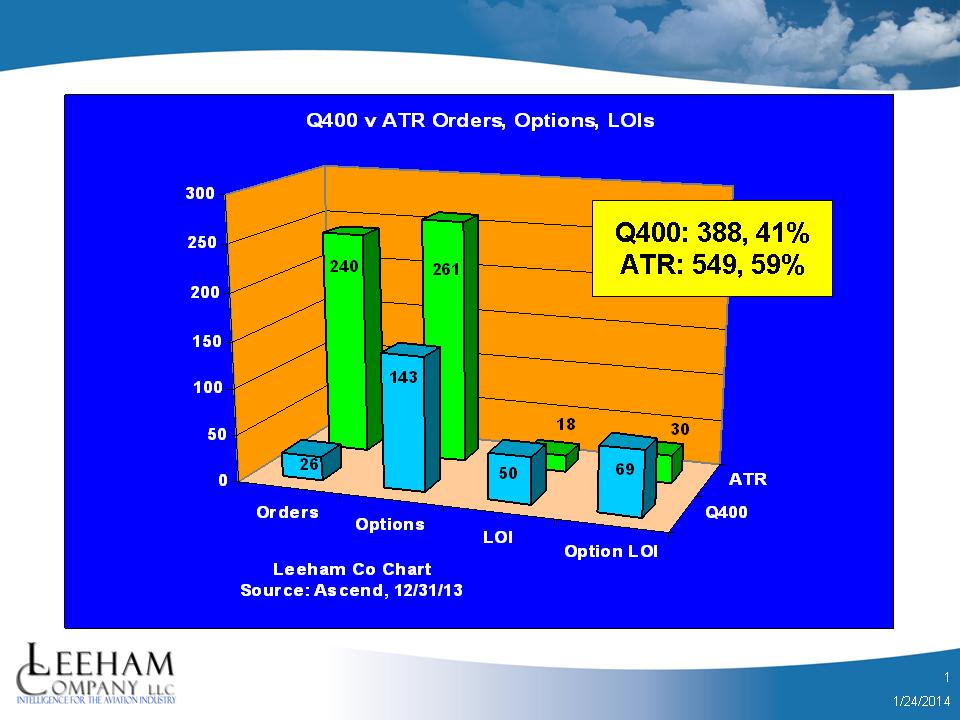

ATR presses Airbus: ATR, the world’s leading maker of turbo-prop airliners, is pressing Airbus Group to green-light its proposed 90-seat, clearn-sheet turbo-prop, Bloomberg News reports.

Airbus Group owns 50% of ATR; Alenia owns the other 50%. ATR’s CEO wants to change this legal structure, reports The Wall Street Journal.

According to the news reports, Airbus is concerned about the diversion of engineering resources. Maybe this is why. Airbus is studying a “mega-twin” concept, reports Aviation Week. Of particular note is the reference that Airbus doesn’t plan to launch a new airplane in the next 10 years. We think these plans are going to have to change when Boeing launches a replacement for the 757, followed by the 737RS, which we have for the end of this decade.

But let’s get back to ATR.

Bombardier, the world’s #2 turbo-prop airliner producer, launched a high-density, 86-seat version of its venerable Q400 last year. China is going forward with a 90-seat turbo-prop and India is also interested in joining the fray.

ATR currently holds a 59% share of the future orders, options and Letters of Intents backlog.

Bombardier made some significant progress last year, signing large LOIs with Russia for 100 and with China. These should be converted to firm orders this year, but even so, ATR has a lopsided market lead.

Boeing Stratoliner: Boeing has a short profile of the B307 Stratoliner, the first pressurized airliner. It’s the 75th anniversary of this important airliner. The last surviving example is on display at the Steven Udvar-Hazy Museum at Washington Dulles Airport.

Boeing 777 model: It’s been over the Internet already but in case you’ve missed this, a 1/60th, highly detailed model of the Boeing 777 was carved out of manila folders. This is an amazing piece of artistry.