Leeham News and Analysis

There's more to real news than a news release.

Charleston plant continues to give Boeing headaches for 787

Boeing is adding hundreds of workers to its Charleston (SC) 787 plant top deal with continued quality problems, reports The Wall Street Journal.

The details in the article are at odds with statements from Boeing throughout the last year that all was well at the plant, including that plans to produce three 787s a month by the end of last year were on track. When the Charleston Post-and-Courier prepared to report that the Charleston plant would fail to meet this goal, Boeing’s Charleston spokeswoman issued a rather snarky response that proved to be at odds with statements from Boeing’s own officials.

We heard all year that there were continued quality control issues at Charleston and production was slower than expected. Further, we had heard of traveled work that required IAM 751 members at the Everett (WA) plant to fix this work–which the WSJ reports has been climbing and now exceeds the 2011 level.

Odds and Ends: CSeries timeline; KC-46A roll-out; China’s new airplane

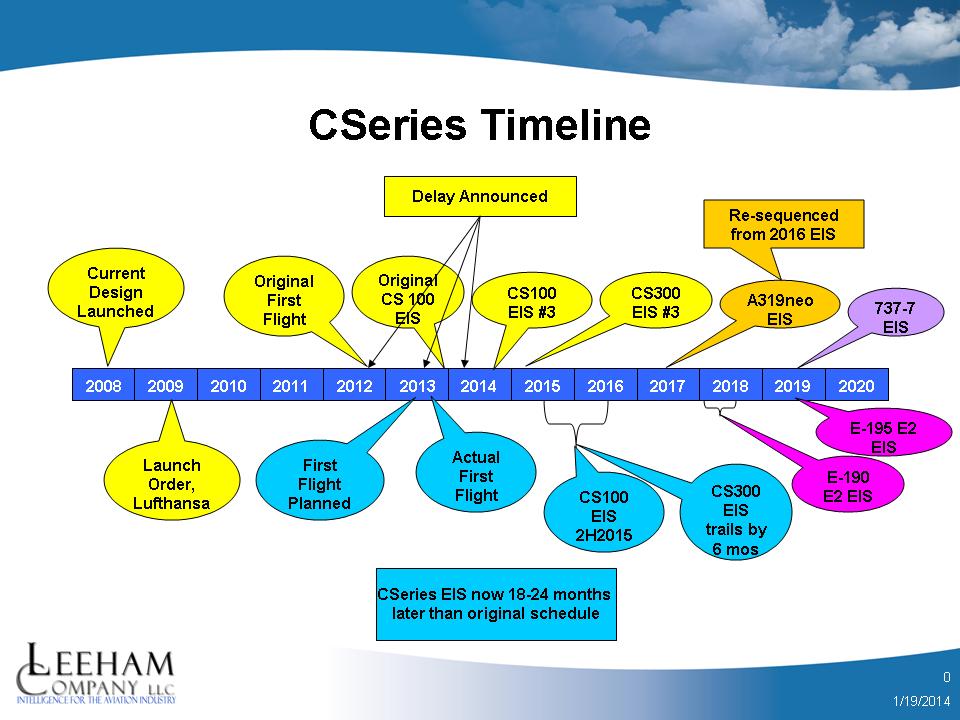

CSeries timeline: Bombardier last week announced a third delay in the CSeries program, this time for as much as a year.

This probably should have been expected. BBD originally planned a five year period between program launch and entry-into-service. As we saw with the Boeing 787, launched with a four year timeline, even five years was too ambitious.

CSeries Timeline. Leeham Co Chart

The EIS period for the 787 turned out to be the standard seven years, almost eight–and even then, the EIS was anything but smooth.

Airbus’ launch-to-EIS for the final A350 version is somewhat more than eight years. Even though BBD is a sub-contractor on the 787 program and said it benefited from lessons learned, it’s clear officials were far too ambitious.

KC-46A roll-out: Boeing’s first tanker for the USAF based on the 767-200ER will roll out this summer. The Everett Herald has this story. The airplane is a somewhat revised 767-200ER called the 767-2C. In addition to upgrades with the airframe, the Pratt & Whitney PW4000 engines will have upgrades which improve fuel consumption.

China’s new airplane: China isn’t just developing the ARJ21, C919 and some military airplanes. It’s also developing the world’s largest amphibian.

Boeing notified supply chain: prepare for 52 737s per month

In a letter dated January 3, Kent Fisher, vice president of supplier management, set the date for going to 47/mo in July 2017. The year had previously been announced by Boeing. Fisher continued that demand is “sufficient” to take the “protection rate” to 52/mo “later in the decade.”

“Protection rate” means the Boeing and the suppliers need to protect the ability to increase to the desired rate in terms of tooling, machinery, parts, and their own suppliers. This notification isn’t as firm as announcing an actual production rate increase, but it’s pretty close.

Airbus, meanwhile, continues with construction of its Mobile (AL) plant, with a target operational date of next year. Initial production will be 2/mo, ramping up to 4/mo. The plant has the capacity of 8/mo. This means Airbus increases production of the A320 family to 44 in late 2015 or early 2016, then 46 later in 2016 and 48 to 50 thereafter.

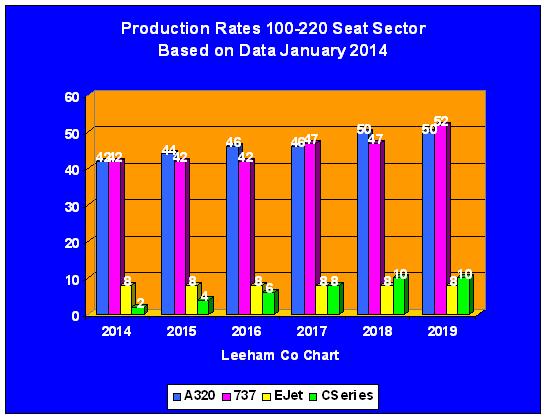

The Airbus and Boeing production rates dwarf those of Bombardier, which is challenging the Big Two OEMs at the lower end of the 100-220 seat sector with the 110-145 seat CSeries, and Embraer, which produces the 100-122 seat E-190/195 E1 today and which is offering the 132 seat E-195 E2 for delivery beginning in 2018.

Airbus’ factories are in Hamburg, Toulouse, Tianjin and from next year, Mobile. Hamburg and Toulouse are currently producing 38 A320 family members a month, weighted toward the latter, and Tianjin is at 4/mo. Tianjin and Mobile have the capacity of 8/mo each; we don’t know the total capacity of the Hamburg and Toulouse plants but are told these are at capacity; Airbus declined comment. This means Airbus has the capacity to go to 54 A320s/mo among the four plants after Mobile is fully operational.

Boeing has the capacity for 63 737s a month at its single Renton (WA) factory. Embraer has the capacity for 17 E-Jets a month. Bombardier plans a capacity of 20/mo for the CSeries.

Seattle Seahawks to the Super Bowl!!!!

Odds and Ends: CSeries EIS rescheduled, new deal announced; Airbus seeks unprecedented ETOPS rule

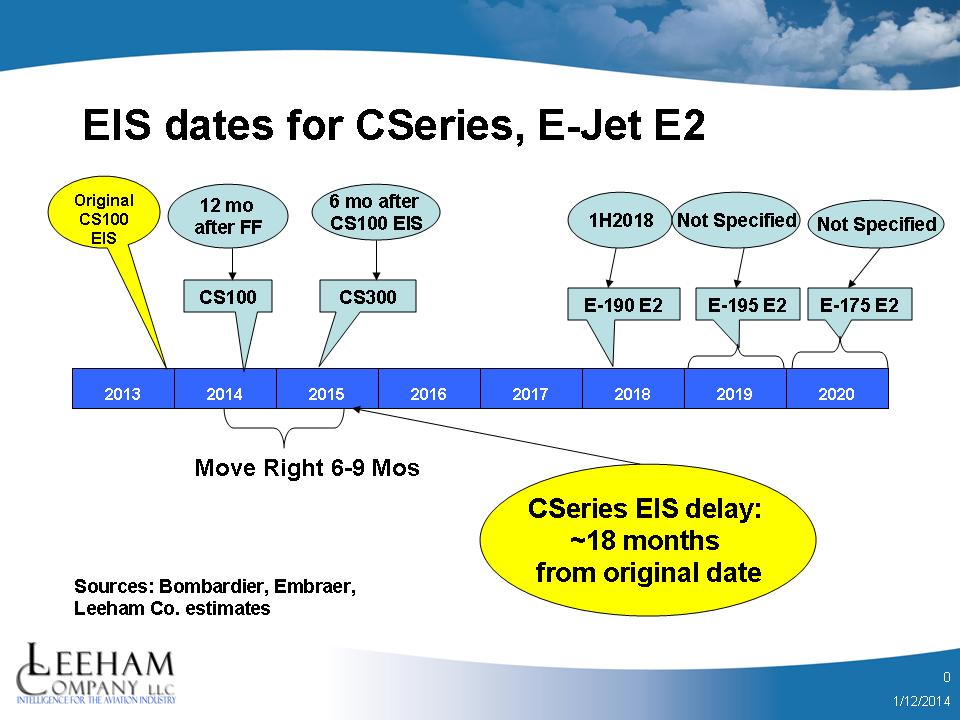

New CSeries EIS: Bombardier today announced a new delay in the entry-into-service of its CSeries, confirming what we reported Monday. BBD now says EIs will be in the “second half” of 2015, compared with the September 2014 planned EIS. We forecast a 6-9 month delay, so this now is a 9-15 month additional delay.

BBD’s statement: “The CS100 aircraft’s entry-into-service is now scheduled for the second half of 2015 and will be followed by the CS300 aircraft’s entry-into-service approximately six months afterwards.

“We are taking the required time to ensure a flawless entry-into-service. We are very pleased that no major design changes have been identified, this gives us confidence that we will meet our performance targets,” said Mike Arcamone, President, Bombardier Commercial Aircraft. “While the process has taken more time than we had expected, our suppliers are aligned with the program’s schedule and together, we will continue to work closely to move the program steadily forward. With the first flight of flight test vehicle 2 (FTV2) successfully completed on January 3, 2014, the CSeries aircraft program will continue to gain traction over the coming months.”

Below is what we published Monday.

We’re now looking at an 18-27 month delay for the originally planned EIS of December 2013.

Update: BBD tells us the the “software maturity” is behind the rescheduling. Basically, this means that all the various software systems have to completely and correctly talk to each other and avoid the issues that “have affected our competitors.” BBD declined to name the specific affected systems nor the suppliers, instead saying that this is a Bombardier “team” project and that the “team” is on board with the new timeline.

In addition, Bombardier and a Middle East airline announced an order for the CSeries.

Airbus seeks big ETOPS OK: The Wall Street Journal reports that Airbus is seeking regulatory approval for a 420 minute ETOPS for its A350. (Subscription may be required.) This means the airplane could fly seven hours on one engine if the other one fails. It opens trans-polar and trans-Antarctica route opportunities.

The Boeing 787 is restricted to 180 minute ETOPS. The Boeing 777 has 330 minute ETOPS.

Via Jon Ostrower, here’s an example of what works beyond 330 minute ETOPS.

Meanwhile, Boeing has begun high speed wind tunnel testing for the 777X.

Airbus v Boeing: The Seattle Times published a good graphic of the Airbus v Boeing order outcome for 2013.

{kind=link}

IAM 751’s president Tom Wroblewski steps down

Tom Wroblewski, president of IAM 751–the Boeing touch labor union in Puget Sound (WA)–announced last night he is retiring on January 31.

The Seattle Times has the full story. In a nutshell, Wroblewski’s health blew up alongside the labor relations with Boeing over the 777X site selection and the relationship within the District 751 and between 751 and the International.

We’ve casually known Wroblewski for many years. We like Wroblewski and knew he had the welfare of his members at heart. We disagreed with him and 751’s positions on many occasions, just as we did with Boeing’s position toward labor, but we always respected Wroblewski.

More to the point, we also believe Wroblewski was more in tune with his membership and more concerned for 751’s welfare than the International. We felt so strongly about this that in February 2010, at the Pacific Northwest Aerospace Alliance conference, we suggested that it would be in 751’s interest to “divorce” itself from International.

Wroblewski, who shies away from the press, called us protesting our suggestion. We later learned that he got into hot water with International over our opinion that he knew better what was important for 751 than the International leadership.

Wroblewski was further cranked with us a few years later when we advocated that Washington State needed to become Right To Work to make it more competitive with other states competing for our aerospace business. And he didn’t like our recollection that it was the IAM (though a different District) that lead to the shutdown of Eastern Airlines rather than grant concessions to save 10,000 jobs. (International president Tom Buffenbarger had a hand in that one.)

Readers know well what we think of how International handled the 777X contract negotiations and ran roughshod over 751. We opined that International was more concerned with retaining 751’s membership dues than it was about what was best for the members.

Under Wroblewski, 751 engaged in several philanthropic activities, most notably raising money for guide dog training and related needs. These activities got little press (including from this venue), who instead focused on the “sexier” stories of labor contract negotiations and strife with Boeing management.

A new leader for 751 may well be more militant than Wroblewski. While there now is a contract in place well into 2024, a militant leader for 751 can nonetheless make things difficult in an already tense situation for years to come. We think this has the potential to be a negative development for Boeing.

We’re sorry to see Wroblewski leave under these circumstances but not surprised. We wish Wroblewski a speedy recovery.

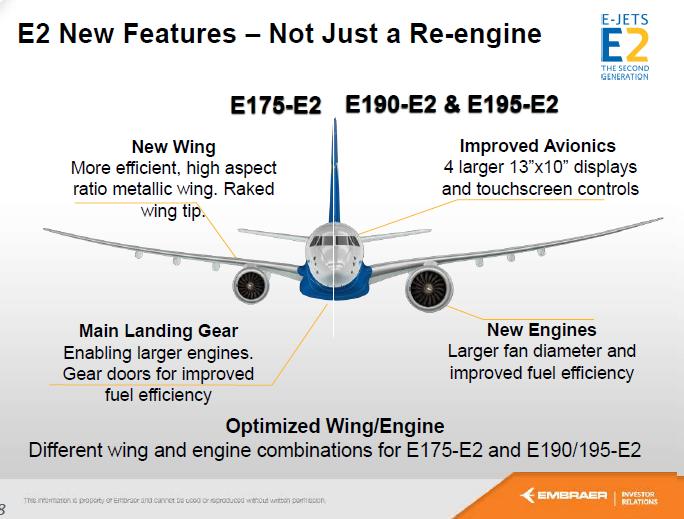

Embraer continues and refines its strategy at the low-end of 100-149 seat sector

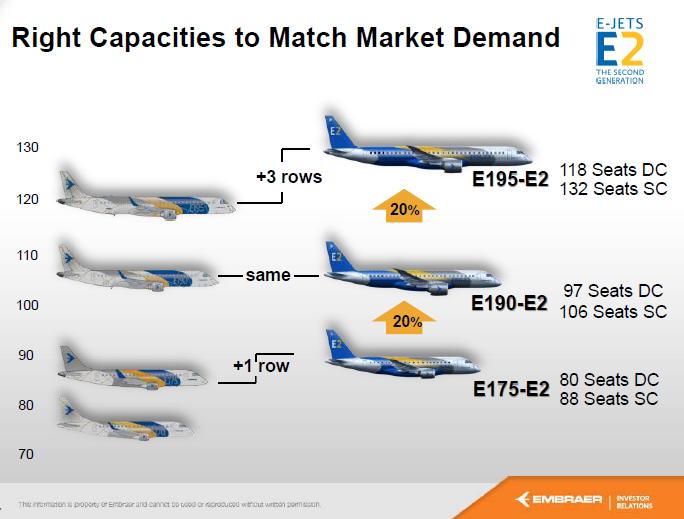

While Airbus and Boeing slug it out in the competition for the duopoly and Bombardier struggles to gain respect as an emerging mainline jetliner producer, Embraer continues and refines its strategy in the smaller-end of the jet market with its E-Jets, E-Jet “Plus” (our term) and the E-Jet E-2.

Source: Embraer, Reprinted with permission.

Embraer is broadening its offering from a maximum of 122 seats to a maximum of 132 and dropping its low-end E-170 from future variants. This brings the EMB family to 90-132 seats, following the decision to undertake an extreme makeover of the current E-175/190/195 line by adapting the Pratt & Whitney P1000 Geared Turbo Fan engine to a new wing design and upgrading a variety of systems in the E-Jet E2.

Source: Embraer. Reprinted with permission.

Airbus wins annual results, trails Boeing in deliveries

Airbus announced 1,619 gross orders for 2013–1,503 net orders–and a backlog of 5,559 aircraft. The company delivered 626 aircraft for the year. It ended the year with 51% of the market vs. Boeing.

Boeing won the delivery race but came in second in orders.

CEO Fabrice Bregier said that 10 years ago Airbus delivered only half the aircraft it did in 2013.

Bregier, at the annual press conference, says “re-engining [the A330] is always an option, but not only option,” reports Reuters. “[Airbus COO-Customers John] Leahy says Airbus could eventually add 1-2 rows to A350-800.”

Aviation Week reports the A350-800 EIS could be moved back a couple of years, also reporting it could be enlarged by two rows.

Bregier says A320 production could increase, reports say from the press conference. (We report in our e-mail distribution today what the production rates will be over the next few years–this will be published on this website next Monday.)

The case for an A330neo

With the increasing possibility that Airbus will defer or even drop the A350-800, the case for an A330neo becomes much stronger. Absent the A358, Airbus has no effective competition to the Boeing 787-8. The current A330, which we will call the A330 Classic, is a very good airplane but it is not as fuel efficient as the 788. The Airbus argument that the A330 Classic is competitive is based on the most favorable of assumptions and rests in part on the key capital cost assumption and moderate fuel prices.

In a story on Friday Reuters confirmed our December 23 e-newsletter report (which subsequently was published at Leeham News and Comment December 29) that Airbus is seriously considering an A330neo. This certainly clears the air on this score.

Source: Airbus

Airbus argues that the lower capital cost offsets the higher operating costs of its A330s vs Boeing’s 787-8 and forthcoming 787-9.

The following table includes Airbus’ assumption as well as 2013 lease rates reported by the appraisal firm Collateral Verifications (CV). Airbus assumes a higher lease rate for the 787-8 than CV reports. CV does not yet have an estimated lease rate for the 787-9.

Current Market Value is the price an airplane can be expected to sell for in today’s environment. Current Base Value is the theoretical price in a stable supply-and-demand market.