Leeham News and Analysis

There's more to real news than a news release.

One A380 departure or two 777-200ER alternatively 787-9?

Subscription Required

By Bjorn Fehrm

Introduction

December 2, 2021, © Leeham News: With the last Airbus A380 rolling of the production line in days, we started looking at why the A380 didn’t sell last week. Now we check its economics for an airline that can fill it. We fly one A380 versus two departures of smaller aircraft on a typical trunk route.

Our analysis takes British Airways as an example and whether it shall use an A380 on Heathrow to LAX at peak traffic or rather two departures with its Boeing 777-200ER or 787-9.

Summary

- When you can fill the A380, it’s surprisingly competitive even against a more modern aircraft like the 787-9.

- This is when we focus on passengers and cost.

- We change the analysis angle next week when we add cargo and look at margins rather than cost.

It’s time for a reality check on ecoAviation

Subscription Required

By Scott Hamilton

Introduction

Nov. 29, 2021, © Leeham News: The goals are admirable and lofty: cut carbon emissions dramatically.

Boeing wants to have its 7-Series airplanes be 100% compatible with Sustainable Aviation Fuel (SAF) by 2030. Whatever Boeing can do, so can Airbus.

Airbus wants to produce the first hydrogen-powered airliner, probably in the 70-seat sector, by 2035.

IATA, the International Air Transport Assn. industry trade group, set 2050 at the target for net-zero emissions.

All great ideas. Industry officials understand the challenges and realities. Tim Clark, president of Emirates Airline, minced no words at the IATA AGM in October: Don’t make promises you can’t keep.

For the pie-in-the-sky crowd, the sheer numbers don’t add up. Replacing the thousands of Airbus A320ceos, A330ceos, Boeing 737 NGs, 757s, 767s, 777 Classics, Mitsubishi CRJs, and Embraer E1 jets with their successors—let alone, the successors to the successors—will take decades.

And this doesn’t even count replacement of today’s turboprops with a successor that doesn’t exist, followed by their successors.

Summary

- 20-year Forecast to 2040 shows about 4,000 single-aisle, mainline jets will remain in service by 2040. The majority of these flying today are older generation aircraft.

- There will be about 1,000 twin-aisle jets flying today that will be flying in 2040. These can be expected to be Boeing 787s, Airbus A350s and a small number of A330neos. Each is more environmentally friendly than previous generations.

- There will be a handful of four-engine jets flying by 2040, most likely cargo aircraft.

- Of the sub-100 seat category, there will be fewer than 300 jets flying in 2040 that are flying today. Some of these will likely be end-of-line CRJs plus late-model, older generation E175-E1s. Deliveries of the latter continue well into this decade because the future of the Embraer E175-E2 is uncertain.

Why the A380 didn’t sell

Subscription Required

By Bjorn Fehrm

Introduction

November 25, 2021, © Leeham News: The last A380 will be delivered to Emirates in the coming week, after a production run of only 251 units. Why didn’t Airbus sell more?

What was the trouble with the A380? Was it uneconomical, or was there some other problem? We look into the different factors that made it a hard sell to the world’s airlines and support this with comparisons with aircraft that sold better.

Summary

- The A380 had its shares of development problems, mainly in the installation of a complex electrical system. Still, overall the development and production went reasonably well for being a new type for Airbus.

- We have over the years shown that its seatmile costs were competitive versus alternatives. What was then the problem? Why didn’t it sell?

The end of A380 production

Subscription Required

By Vincent Valery

Introduction

Emirates’ 100th A380 delivered

Nov. 18, 2021, © Leeham News: The 251st and final A380 delivery to Emirates will happen in the next few weeks before the end of the year. With that in mind, LNA thought it relevant to look back on the Superjumbo. The program meant so much for Airbus but ultimately failed to live up to its high commercial expectations.

Summary

- Competing visions to meet future air travel growth;

- A relatively less delayed entry into service;

- Ongoing struggles to accumulate new orders;

- Future operational prospects;

- Where the Superjumbo works and does not.

Air Lease Corp.’s A220 order may be followed soon by others

By Scott Hamilton

Airbus A220-300 for Air Lease Corp. Photo credit: Airbus.

Nov. 16, 2021, © Leeham News: Air Lease Corp. added another 25 Airbus A220s to its backlog with Airbus. The letter of intent, announced at the Dubai Air Show, brings ALC’s A220 backlog to 75, the most of any lessor.

ALC also is the first customer to publicly order the new Airbus A350F.

ALC announced the LOI yesterday at the air show. It was part of a package of 111 aircraft. In addition to the A220s, ALC signed for 55 A321neos, 20 A321XLRs, four A330neos and seven A350Fs.

Airbus has 643 firm orders for the A220: 90 for the smaller A220-100 and 553 for the larger A220-300. The -300 competes directly with the Airbus A319neo and the Boeing 737-7.

With the Dubai Air Show underway, LNA learned that there are at least two big orders that might emerge before year end that boost the book to nearly 800. One deal is with an exclusive Boeing operator, who also is in talks for an A321neo order. The sub-type couldn’t be learned, but given the carrier’s route system, it almost certainly will include the LR and/or XLR.

Interest in the A220 continues to pick up under the Airbus ownership. With the pandemic slowing, additional orders appear to be in the offing sooner than later.

Airbus continues its cost-cutting efforts on the program. LNA reported detail in a Sept. 28 post. During the IATA AGM Oct. 3-5 in Boston, Airbus’ chief commercial officer, Christian Scherer, elaborated.

Air Lease Corporation tops LOI with launch order for Airbus new freighter

By Bjorn Fehrm

November 15, 2021, ©. Leeham News Dubai: Air Lease Corporation (ALC) crowned its agreement for 111 Airbus single-aisle and wide-body aircraft with a launch order for the new A350F freighter.

The order for seven A350F was part of a 111 unit long-term deal to top up ALC’s 100 aircraft order from Le Bourget Airshow 2019. With 25 A220-330s, 55 A321neos, 20 A321 XLRs, four A330neos, and seven A350Fs, Air Lease is now covered until after 2025.

“We think it’s timely to order these aircraft now, before the post COVID rush for new aircraft sets in,” said Air Lease’s Executive Chairman Steven Udvar-Hazy. The leasing company thus secures its availability of aircraft in a market with rekindling demand and an Airbus that’s approaching capacity limits.

Update on twin-aisle production rates

Subscription Required

By Vincent Valery

Introduction

Nov. 15, 2021, © Leeham News: Airbus and Boeing updated their commercial production plans a few weeks ago, including rates on their twin-aisle families.

As a result of solid freighter demand, Boeing is considering increasing the 777F production rate from around 1.5 per month. Lingering production issues leave the Dreamliner assembly line at two per month until deliveries resume. The 767 line stays at three per month for now.

Airbus delayed an increase in the A350 production rate from five to six per month to early 2023. However, the OEM surprised the market by announcing an increase in the A330 production rate to three per month by late 2022.

LNA has repeatedly pointed out the weak A330neo order book in recent years. Airbus said that recent commercial successes allow it to ramp up A330 production.

While Boeing was more cautious about a near-term recovery in twin-aisle aircraft orders, Airbus recently stated that interest was picking up. LNA investigates the latest production plans on commercial twin-aisle programs and compares them with early 2020 and 2021.

Summary

- A head-scratching A330 production increase;

- Pushing 777X deliveries to the right;

- Differing plans for the A350 and 787;

- Sustaining the 767 production rate.

Indigo Partners airlines kick-start single-aisle recovery with large joint order

By Judson Rollins & Bjorn Fehrm

Introduction

November 14, 2021 © Leeham News: Airbus made a splash on the first day of the Dubai Air Show, announcing a firm order for 255 A321neo family aircraft from the Indigo Partners portfolio of airlines.

This is the first large order for single-aisles since COVID-19 struck early last year, comprising 226 A321neos and 29 A321XLRs.

Indigo Partners, headed by airline veteran Bill Franke, is an Arizona-based private equity firm with stakes in several low-cost carriers around the world. Franke was present at today’s announcement along with the chief executives of all four airlines, two of whom joined the event virtually.

The airlines included in today’s order are US-based Frontier, Mexico’s Volaris, Chile’s JetSmart, and Central European giant Wizz Air. Joint orders like this are relatively uncommon except from multi-carrier conglomerates like Lufthansa Group or IAG. Indigo’s last joint order was for 430 A320neo family aircraft, announced at the 2017 Dubai Air Show.

Airbus issues “conservative” post-COVID forecast

By Judson Rollins

Introduction

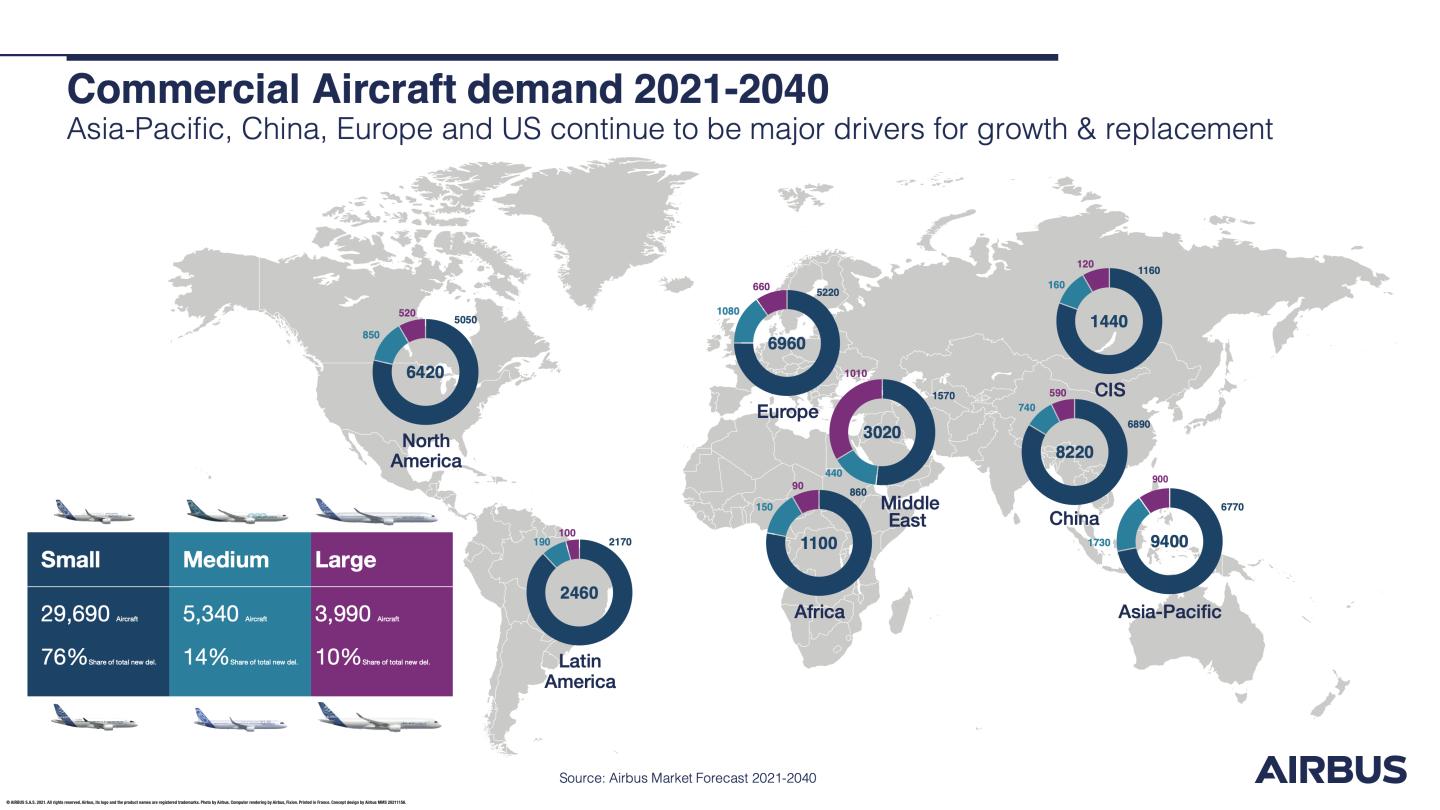

November 13, 2021, © Leeham News: On the eve of the Dubai Air Show, Airbus released the first edition of its annual Global Market Forecast (GMF) since the COVID-19 crisis began.

The manufacturer sees approximately 39,000 passenger aircraft with 100+ seats and freighters being produced by 2040. 29,690 will be small aircraft, 5,340 medium, and 3,990 large. Airbus’s category definitions now take both size and range into account; the A321XLR is categorized as a “medium” airplane, reflecting its inroads into routes currently operated by smaller widebodies.

Chief Commercial Officer Christian Scherer said that Airbus took a “corridor” approach to forecasting a global traffic recovery using high and low scenarios. In the low case, traffic would recover to 2019 levels by 2023, or 2025 in the high case. He said the high scenario is basically an extrapolation of recent traffic trends across key markets.

He expressed optimism that the wave of COVID-driven order cancellations had peaked. “The resilience of our industry has been remarkable. Owners continue to believe in their investments and put capital into their fleets.” Read more

Airbus details A350F specifications

By Scott Hamilton and Bjorn Fehrm

November 11, 2021, © Leeham News: Airbus has given more information about what led to their new freighter, the A350F, and its data. Scott Hamilton talked to Airbus Chief Commercial Officer Christian Scherer at the IATA AGM on Oct. 3-5 in Boston, and Bjorn Fehrm spoke to Head of Freighter marketing, Crawford Hamilton, about the technical details. (The two Hamiltons are not related.)

The A350F is the most capable new-build freighter Airbus has designed, posing the most serious threat to Boeing’s dominance of jet freighters since the dawn of the jet age. Some expect Boeing to respond next week with a program launch of the 777XF, but LNA understands this won’t be the case.

“The market has asked us to produce it,” said Scherer of the A350F. “So we launched the program based on our own belief of the strength of the business case.”

“The A350F beats the competing production freighter (Boeing’s 777F, our note) on payload, volume, and economics,” says Crawford Hamilton. “We have taken extra care to make the door larger and the floor extra sturdy to ease loading planning and execution. The A350F will be the freight forwarder’s preferred machine.”

The Airbus new freighter, the A350F. Source: Airbus.