Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: A350 batteries; A350 V 1.0; Southwest schedule

A350 batteries: Flight Global has a detailed story about the Airbus approach to lithium-ion batteries in the A350. The approach is more conservative than Boeing’s for the 787.

A350 Version 1.0: A blog called A350 XWB News has a retrospective on the A350’s original proposal (which we call Version 1.0, because the design went through so many iterations). It’s got the original brochure reproduced. It’s an interesting recollection, and one to compare with the A330neo. Boeing dismisses the A330neo as A350 V 1.0, but it’s really not when you compare.

A350 Final version: A350 XWB production is tracking to plan, first A350 after Qatar’s initial 8 (MSN6 to 13), MSN14 to Vietnam Airlines is going to ground tests (Station 30) after getting wings and empennage in Station 40 at the Airbus Final Assembly Line (FAL) in Tolouse. We are following this program carefully since start and the roll out of the latest XWB from wing join was within days of our prediction 6 months ago, thereby the A350 ramp to three FAL starts by end of year is tracking so far.

A380 downed by mops: Aviation Week has the story on how Qantas cleaners got the water flowing in their A380s when it should not. The incident is old (80 gallons of water flowing around in the fittings of the A380 when climbing out of LAX to Melbourne, first time in June) but one has now found the cause; the cleaners mops were getting the water couplings in a galley unlatched. Small things having big impact.

Boeing record: Qatar airways took delivery of three 787 and one 777 in one day this week; here the Flightglobal version of the Boeing announcement. Airline CEO Al Baker says ““Never in the history of an airline have so many aircraft been taken in just one day.”

Southwest schedule: Southwest Airlines adjusted its schedule two months ago to improve its on-time performance, and revealed that the new times are working.

Southwest, once boasting of being #1, 2 or 3 in on-time ratings among US major carriers, saw a steady decline in recent years as it ramped up service in congested airports, expanded in regions that were more prone to weather delays, added larger airplanes (the Boeing 737-800) to its schedule. After acquiring AirTran, Southwest tightened the schedule in an effort to cut turn-times. But AirTran’s traditional hub operation vs WN’s largely point-to-point didn’t lend itself to the tighter turns Southwest scheduled. It didn’t take a lot of insight to understand why delays were showing up on the AirTran fleet. Southwest’s OT performance is still not where it once was–it’s currently at 78.9% when it used to run in the 80s–but it’s better.

BABC Conference, Part 1: WA State’s position, Boeing’s outlook

The British American Business Council-Pacific Northwest is sponsoring a conference today on the Advanced Technologies for Next Generation Aircraft in Seattle. We’ll have several reports, starting with this one.

Alex Pietsch of the Governor’s Office of Aerospace, kicked off the conference, saying that Boeing employees more than Microsoft, Starbucks and Amazon combined.

“No one should question Wasnhington’s place in aircraft production,” Pietsch said, noting the siting of the 777X assembly and wing production, a rate increase to 52/mo for the 737 and expansion by suppliers.

Thanks to the 777X, Washington will be the only location in the US where composite wings are built, Pietsch said.

Kourosh Hadi senior director of Boeing Airplane Product Development, said that trends in commercial aviation during the next 20 years indicate that single-aisle aircraft and demand remains the “fastest growing, most dynamic segment” in the industry. Traffic demand continues at 4%-5% per year, despite four recessions, two financial recessions, two Gulf Wars and other global factors.

Hadi indicated that “advanced designs” fall within the 2021-2030 timeframe and “future concepts” fall from 2031 and beyond. Advanced designs include advancements in aerodynamics, systems and propulsion. Future designs might include SST and other concepts.

Technology has to add value, Hadi says, for performance, cost, production rates, Cash Airplane Related Operating Costs (CAROC, a common Boeing term) and environmental issues are focus areas.

First flight of the 737-8 MAX is early 2016, with EIS with Southwest Airlines in July 2017.

Hadi said it was “mind-boggling” that Boeing is improving the 777 by 20% with the 777X, a plane he characterized as one of the finest aircraft ever produced.

Flight test of the 777X is slated to begin in 2019, with firm configuration next year and detailed design in 2016 and the production to begin in 2017.

- Our observation: Hadi detailed the 777 Classic, 777X and 787 families but only talked about the 737-8. FWIW.

- In a change from practice, and a refreshing one, Boeing compared its next round of aircraft with its own current and past generation aircraft rather than bashing Airbus at every opportunity.

Delta’s wide-body fleet plan: could it include used 777-200ERs?

Delta Air Lines is supposed to make a decision on its Request for Proposals for 50 wide-body aircraft before the end of this year, perhaps as early as next month. The competition is hot between the Airbus A330-900, the A350-900 and the Boeing 787-9.

Delta is understood to use the aircraft to beef up its growing Seattle hub across the Pacific; for its Detroit hub, also to Asia; and its New York JFK trans-Atlantic hub.

In addition, Delta is phasing out the last 14 of its Boeing 747-400s inherited from its merger with Northwest Airlines by the end of next year.

The A330-900 is viewed as a trans-Atlantic airplane, while the others are viewed as largely, but not necessarily solely, trans-Pacific aircraft, according to our information.

But there could be another wrinkle. On Delta’s third quarter earnings call, CEO Richard Anderson made some intriguing comments that could raise another possibility: acquisition of used Boeing 777-200ERs.

To put this in context, recall that Anderson and Delta actively seek out inexpensive used aircraft which, while hardly competitive at high fuel prices when comparing operating costs vs new aircraft, provide low capital acquisition costs and low ownership costs.

Here’s the exchange on the earnings call, as recorded by Seeking Alpha’s transcript:

Oct. 28, 2009: five years ago today, Boeing announced 787 Line 2 goes to Charleston; then, now and the future

This is about eight pages when printed.

It was five years ago today that Boeing announced it would locate the second assembly line for the 787 in Charleston (SC).

The decision was expected and, some say, had actually been made months before–as early as the preceding February. We take a look back at the events leading up to Boeing’s decision to put the second line in Charleston, what’s happened since then and where Boeing will be in five more years.

CASM Paradigm: Lower Seat Mile Cost or Higher Yield; Evaluating the GOL competition

Subscription Required

Introduction

As Brazil’s budget airline GOL reportedly evaluates whether to acquire 20 Boeing 737-7s or Embraer E-195 E2s, the principal of the “CASM Paradigm” is a concept worth examining.

![]() This head-to-head evaluation of the E-195 E2 and the 737-7 MAX is a rarity. Typically the head-to-head involves the Bombardier CS300 and the Airbus A319neo. All three have the same seating capacities. The E-195 E2 has slightly fewer passengers than the 737-7 with similar seat pitch.

This head-to-head evaluation of the E-195 E2 and the 737-7 MAX is a rarity. Typically the head-to-head involves the Bombardier CS300 and the Airbus A319neo. All three have the same seating capacities. The E-195 E2 has slightly fewer passengers than the 737-7 with similar seat pitch.

The competition is also what might be seen as a contrary competition. Airframers agree: the airline industry is upgauging. Capacity discipline, long elusive until after the global financial collapse of 2008, has been driving load factors higher. But lowering unit costs, or the Cost per Available Seat Miles (CASM) has long been the principal measure by which airlines, OEMs and aerospace analysts measure efficiency.

Although Trip Costs of aircraft operating over a route is important, the trend toward upgauging at all levels clearly is the driving force.

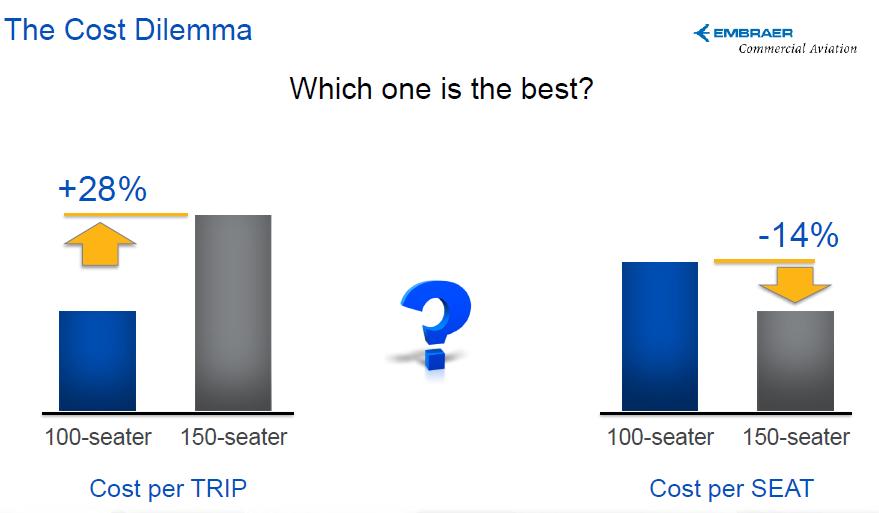

Figure 1. It’s an age-old debate: the cost per available seat mile (CASM) vs trip cost. CASM typically wins, and the airline industry is migrating toward larger aircraft. Embraer, not surprisingly, thinks this has gone too far. Graphic: Embraer, reprinted with permission. Click on image to enlarge.

Embraer takes a different view, arguing that trip costs and a smaller airplane should trump the CASM obsession. A smaller airplane will mean higher yields, EMB says. A larger airplane provides lower trip costs but drives yield lower.

We visited Embraer’s headquarters earlier this month and received a full briefing on what EMB calls the CASM Paradigm. In our report today, we detail the presentation and discuss other considerations beside CASM vs Trip Costs that drive the size of the aircraft acquired.

Summary

- The CASM Paradigm becomes a vicious, circular cycle, driving airlines to larger aircraft but lower yields.

- Extra seats on larger aircraft mean lower unit costs but at the cost of profits.

- Scope Clauses remain an issue in the US.

- Connecting traffic, pay scales also are issues.

- We analyze the operating costs of the E-195 E2 vs the 737-7.

- We discuss the GOL competition.

Odds and Ends: MTU on A380; lessons learned; Alaska Air v Delta; GOL looking for airplanes; Boeing downgrade and upgrade

MTU on A380: The German company MTU, which is a key supplier on a variety of Airbus and Boeing engines, questions the potential market for an A380neo, according to this article from Reuters. Our Market Intelligence indicates Airbus is moving toward a re-engined airplane, although an Airbus official denied this to us this week. Reuters’ sources suggest work is ramping up.

Tapping lessons learned: The Puget Sound Business Journal has a somewhat different approach to the story earlier this week on the groundbreaking for the Boeing 777X wing factory. Steve Wilhelm focuses on Boeing’s tapping of lessons learned on the 737 and 787 programs.

Alaska Air v Delta Air: Months and months ago (almost a year), we were the first to write that hand-wringing over Delta Air Lines’ growth at Seattle, viewed as a major run at Alaska Airlines, was over-wrought. The growth was to support Delta’s growing international hub and while the growth came on many Alaska routes, Alaska’s dominance would prevail. A few months later, we pointed out that Delta’s growth was coming at the expense of Southwest and United airlines; Alaska was solidifying its position. (It also posted record 3Q earnings this week.)

The Puget Sound Business Journal has this story about how the three generations of the Boeing 737 is helping Alaska face off Delta.

GOL looking for planes: Brazil’s GOL is looking at the Boeing 737-7 and the Embraer E-195 E2 to renew its 737NG fleet, according to this Bloomberg report. Next week we’ll be taking another in our series of looks at EMB’s approach to the market with a discussion of the CASM Paradigm.

Boeing downgrade and upgrade: Credit Suisse yesterday downgraded Boeing from Outperform to Neutral (Buy to Hold) on the basis of 787 deferred costs and lower free cash flow. Wells Fargo reiterated its Hold rating. Zacks went from Neutral to Buy. Stern Agee reiterated its Buy.

Part 2: Boeing 757: Airbus A321neoLR as a replacement on long and thin routes

Subscription required.

By Bjorn Fehrm

Part 2 of 3

Introduction

In Part 2 of our three-part 757 Replacement analysis, we take a close look at Airbus’ new 97 tonnes take off weight A321neo, revealed by Leeham News and Comment October 21. We call the 97t airplane the A321neoLR (Long Range); Airbus has yet to name the aircraft, which it began showing to airlines last week.

![]() We analyze the A321neoLR’s capabilities and limitations when compared to the aircraft it intends to replace, the Boeing 757-200W. We have chosen to do so using a real airline configuration as opposed to an OEM’s typical seating layout. By comparing the 757-200W and the A321neoLR over the route structure that United Airlines is using the 757 today, we can better see the characteristics of the A321neoLR and what operational consequences the differences between the types would mean for the airlines. Before we start, a short recap of Part 1 about the 757 and its replacement candidates. Here is what we found:

We analyze the A321neoLR’s capabilities and limitations when compared to the aircraft it intends to replace, the Boeing 757-200W. We have chosen to do so using a real airline configuration as opposed to an OEM’s typical seating layout. By comparing the 757-200W and the A321neoLR over the route structure that United Airlines is using the 757 today, we can better see the characteristics of the A321neoLR and what operational consequences the differences between the types would mean for the airlines. Before we start, a short recap of Part 1 about the 757 and its replacement candidates. Here is what we found:

- the seating capacity of the A321 is within 10 seats of the 757-200 in a standard configuration; the 737 MAX9 is trailing with about 20 fewer seats.

- the myth about the strong engines of the 757 is just that, a myth.

- the good field performance of the 757 is coming from its wing more than any advantage on the engine side

- the A321neo and 737 MAX9 were hindered in their capability to replace the 757 for long and thin international routes by characteristics that can be changed. For the A321neo, this may be accomplished with rather modest changes to Max Take Off Weight (MTOW) and tankage. For the 737 MAX9, more elaborate changes to the wing and engines are required, both hard to do.

Figure 1. Boeing 757-200 of British Airways which launched the 757 together with Eastern Airlines 1983. Source: Wikimedia.

Summary, Part 2

- We will now look in detail on the changes Airbus is doing on the A321neoLR, what each change brings and any restrictions that remain.

- We will also detail why we think it will be harder for Boeing to match the A321neoLR with a 737 MAX9 development.

- We detail prime, present 757W long-thin routes.

- We present 757W international, A321neoLR and 737 MAX9 “long range” configurations.

- We provide economic comparisons such as Payload-Range charts and Fuel consumption per trip and per seat diagrams.

In the final Part 3, will look at Boeing’s alternative to an A321neoLR, a clean sheet New Single Aisle (NSA) and a prospective Small Twin Aisle (STA) design and how much such an approach would surpass the A321neoLR on medium and long haul networks and when it could be available.

Boeing’s on the defensive in single aisle market as Airbus enhances A321neo

Subscription required.

Introduction

Boeing is on the defensive in the single-aisle market.

The Airbus A320neo family has about a 57% market share against the Boeing d 737 MAX. As recently as Wednesday’s third quarter earnings call, Boeing CEO Jim McNerney expressed confidence in market share recovery to parity. We don’t see this happening.

The development by Airbus of a 97t “A321neoLR” (Long Range) airplane as a 757 replacement for the long, thin routes of around 3,900nm, although a small market of perhaps 100 airplanes, enhances the A321neo model and could give a boost the the A320neo campaigns.

We had the worldwide exclusive on the development of the A321neoLR Wednesday.

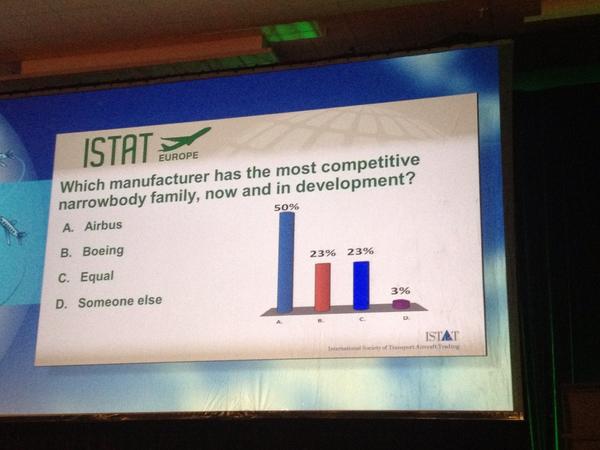

Boeing’s image in the single-aisle sector took a big hit at the ISTAT Europe conference last month. About 1,200 people attended the event and in an audience poll, only 23% voted that Boeing has the most competitive narrow body family; 50% voted for Airbus.

Photo taken at the ISTAT Europe conference in Istanbul last month. Photo via Twitter.

Despite Boeing’s public, professed optimism, our Market Intelligence tells us that Boeing is indeed worried about its single aisle market position. And even though the market potential for the A321neoLR is small, there is the knock-on effect to consider. There is demand for a 757 replacement from airlines and in market perception. The same ISTAT Europe conference asked what Boeing should do next; 54% said replace the 757 and another 18% said replace the 737-9, a combined 72% pointing to a need for Boeing to do something with the single-aisle sector.

Photo from the ISTAT Europe conference at Istanbul last month. Photo via Twitter.

Summary

- Airbus’ latest move with A321neoLR increases pressure on Boeing

- A321neoLR could support additional A320neo sales

- 737-9 can’t be further enhanced to match A321neoLR.

- 737-7 unlikely to be built; A319neo becomes niche model

- Market perception gives “most competitive” edge to Airbus

- What Boeing has to do next

Part 3: Boeing 757 replacement: 757 and Airbus A321neoLR versus clean sheet designs.

Subscription required.

By Bjorn Fehrm

Part 3 of 3

Introduction

In Part 2 of our three-part 757 Replacement analysis, we took a close look at Airbus’ new 97 tonne take-off weight A321neo, revealed in a world exclusive by Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

Summary

For Part 3 we can summarize:

Figure 1. Fuselage cross sections of our models of NSA and NLT. Source: Leeham Co.

Read more

5 Comments

Posted on October 28, 2014 by Bjorn Fehrm

Airbus, Airlines, Boeing, CFM, China, Comac, CSeries, Embraer, GE Aviation, Irkut, Leeham Co., Leeham News and Comment, Pratt & Whitney, Premium, Rolls-Royce, Uncategorized

737, 737 MAX, A320, A320NEO, Airbus, Boeing, Bombardier, CFM, Comac, CSeries, Embraer, GTF, Pratt & Whitney, Rolls-Royce