Leeham News and Analysis

There's more to real news than a news release.

No surge in new-build freighters from COVID expected

Subscription Required

Now open to all Readers.

By Scott Hamilton

Introduction

Aug. 17, 2020, © Leeham News: Coronavirus caused a spike in freight demand. But don’t look for Airbus or Boeing to see a spike in demand for new build freighters.![]()

Boeing hoped to advance the timeline for the launch of the 777-8F. The original plan for the 777X family was entry-into-service of the -9 in late 2019 or early 2020. The 777-8 passenger model (8P) would follow by two years. The -8F would follow two years after that.

As the -9 EIS slipped to late 2020 and the 737 MAX grounding took its toll, -8 development was suspended. The -8P EIS was unofficially reset to 2024.

Now, the 777-9 EIS is rescheduled to 2022. Production of the 777 line is going to 2/mo. With freight demand spiking due to COVID and widebody passenger production not expected to recover until 2025, Boeing thought advancing the -8F launch could boost the X line.

It’s not to be.

Summary

- Boeing hoped to launch the 777-8F with 2024 EIS.

- No market interest scotched the plan.

- P2F conversions of 777-300ER gain interest.

- Airbus hopes for A330-900F are dashed.

A lingering shakeup in European skies

Subscription Required

By Vincent Valery

Introduction

Aug. 11, 2020, © Leeham News: There is a shake-up still to come for European airlines.

LNA wrote in early March about the financial vulnerability of several European airlines as the COVID-19 outbreak was intensifying. The article was released before European countries closed their borders, and the US banned inbound travel for non-residents from the old continent.

Fast forward five months, and the airline industry is in its gravest crisis since World War II. After bouncing from the lows in April and May, a passenger traffic recovery remains elusive. Some European countries are re-implementing travel restrictions as new (for now localized) outbreaks emerge.

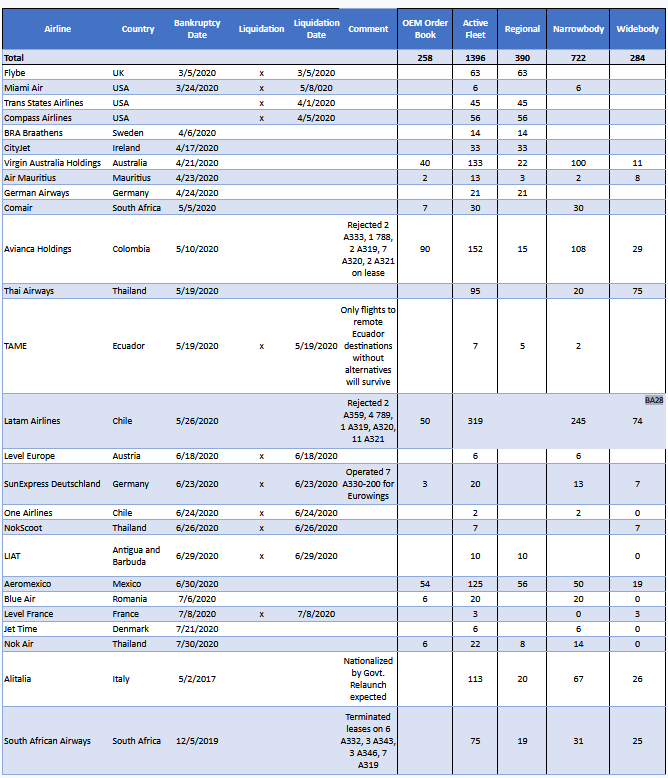

Despite the unprecedented slump in passenger traffic, Flybe is the only sizable European carrier to have ceased operations since the beginning of the COVID-19 outbreak. Several smaller carriers declared bankruptcies or ceased operations.

LNA analyzes why some carriers went under while others did not, and assesses how various market segments might recover.

Summary

- Numerous airlines too interconnected to fail;

- The worst-case comes true for European regional airlines;

- Some unlikely (relative) winners and losers;

- A treacherous road to recovery.

Pontifications: No, it’s not time to fly

Aug. 10, 2020, © Leeham News: Frontier Airlines’ CEO Barry Biffle says “it’s time to fly,” reports The Points Guy.

By Scott Hamilton

Well, good luck with that.

Air fares are ridiculously cheap. Some airlines in the US continue to block middle seats and now require passengers to wear masks throughout the flight. Extra efforts are made to clean the airplanes. (Southwest Airlines, in a truly bizarre move, ceased cleaning seat belts and arm rests between flights—two things passengers are guaranteed to touch.)

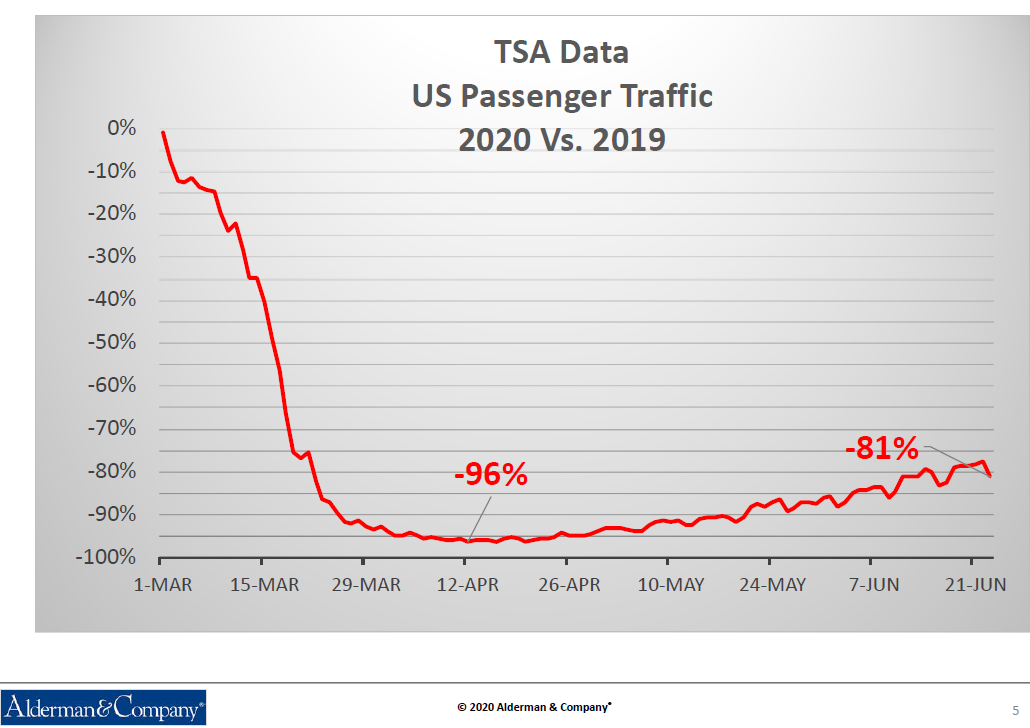

Travel count in in the US is now up to about 800,000 passengers a day. This compares with nearly 3m a day pre-COVID.

I wrote July 6 why I won’t be flying any time soon. I wasn’t concerned about the airplane experience (except for those passengers who refused to wear masks). I was concerned about the experience getting to, from and at the airports and at hotels.

Now, there’s another reason why it’s not time to fly.

US Regional Consolidation Began Before Covid

Second in a Series on the Future of Regionals

Subscription Required

Introduction

By Kathryn B. Creedy

Aug. 6, 2020, (c) Leeham News: Many might assume the recent loss of three regionals – Compass, Trans States and ExpressJet – is Covid related.

![]() What is actually happening is the long-anticipated consolidation of the regional airline industry coupled with fleet restructuring and the most recent fallout of the pilot shortage crisis that began in 2013.

What is actually happening is the long-anticipated consolidation of the regional airline industry coupled with fleet restructuring and the most recent fallout of the pilot shortage crisis that began in 2013.

Reducing the number of regional partners also streamlines the inherent inefficiencies of the regional/major model.

Summary

- Regional airline industry is volatile.

- Mainline-regional model broken for many years.

- Rising costs eliminate some advantages.

HOTR: NOK Air, 3 more bite the dust in COVID fall-out

By the Leeham News Staff

July 31, 2020, © Leeham News: NOK Air of Thailand is the latest carrier to filed for bankruptcy.

LNA’s monthly tracking of failed carriers adds NOK, Jet Time, Level and Blue Air to the list of carriers in bankruptcy since COVID collapsed the global airline industry beginning in mid-March.

Aviation veteran journalist Creedy joins LNA

Kathryn Creedy

July 29, 2020, © Leeham News: Kathryn B. Creedy has joined Leeham News & Analysis as a regular contributor, it was announced today.

Creedy is an award-winning veteran aviation/travel journalist and author who has covered every facet of commercial and business aviation.

Pontifications: The light bulb goes on

By Scott Hamilton

July 27, 2020, © Leeham News: Airlines across the world are pledging aircraft, slots, airport facilities and real estate to raise money.

Some US airlines recently pledged frequent flyer programs to raise billions of dollars in debt to help carry them through the COVID-19 crisis.

Airfinance Journal last week had a podcast with United Airlines and Goldman Sachs to discuss UAL’s doing this and the larger picture.

The rush to pledge virtually everything to raise money is déjà vu all over again.

I’ve been in this business since 1979. I’ve been through the 1991 Persian Gulf War, SARS, downturns, 9/11 and the Great Recession. The impact to the airline and aerospace industry from the virus crisis is by far the worst.

As federal aid comes to end, small suppliers see “blood bath”

Subscription Required

By Scott Hamilton

Introduction

July 20, 2020, © Leeham News: As the Payroll Protection Plan of the US government nears expiration, a blood bath among small suppliers is all but certain unless an extension is approved by Congress.

This is the dire forecast by William Alderman of Alderman & Co. Alderman specializes in representing small suppliers and aftermarket companies wanting to exit the business. Small, in this case, is defined as revenues up to $100m.

Alderman told LNA that some of his clients don’t see business recovery for 10 years. This is a different metric than the one most often cited: air traffic returning to pre-COVID levels in 2023-24, by most accounts.

Summary

- Small companies need PPP extension.

- Small companies need working capital, fast.

- If neither is forthcoming, exiting the business in the other alternative.

Pontifications: Turbulence is not just something in the air

By Scott Hamilton

July 20, 2020, © Leeham News: The timing is coincidental. If you think the airline industry is in a wind shear now, don’t be fooled.

The industry has been in perpetual turbulence for 50 years.

At least that’s the theme of an airline executive’s new book, Turbulence.

At least that’s the theme of an airline executive’s new book, Turbulence.

David Banmiller began his career as a ticket agent, when hand-writing the coupons at the airport as common practice.

He retired three years ago after a career that saw him in executive positions at AirCal, American Airlines and other carriers.

He became a bankruptcy reorganization specialist as well.

Careers

Banmiller weaved through American, TWA, AirCal, the second Pan Am, Aloha and Air Jamaica. He was CEO of AirCal when it was sold to American, where he became an executive under legendary CEO Bob Crandall. Banmiller went on to become CEO of Aloha, Pan Am and Air Jamaica. He took the first two through bankruptcy reorganization and restructured Air Jamaica outside of the courts. He also served as CEO of Sun Country Airlines.

Throughout his careers, Banmiller experienced many of the downturns of the airline industry: oil price wars, 9/11, the SARS pandemic and now, from his retirement, COVID-19.

An economic crisis on top of a medical one: Why airline traffic won’t fully recover until the mid-late 2020s

Open To All Readers

By Judson Rollins

Introduction

July 13, 2020, © Leeham News: As the world waits for the COVID-19 storm to abate, questions are growing over the duration of a demand downturn for airlines.

Many journalists and industry observers have been obsessively searching for “green shoots” indicating the beginning of a recovery, but much of this commentary misses the mark. For instance, much attention has been focused on capacity restoration in the US and China. However, little is known about the percentage of seats filled by Chinese carriers – and last week United Airlines told employees in an internal presentation that while US carrier capacity in July is back to 47% of 2019’s level, it believes industry traffic has only reached 28% and revenue just 19%.

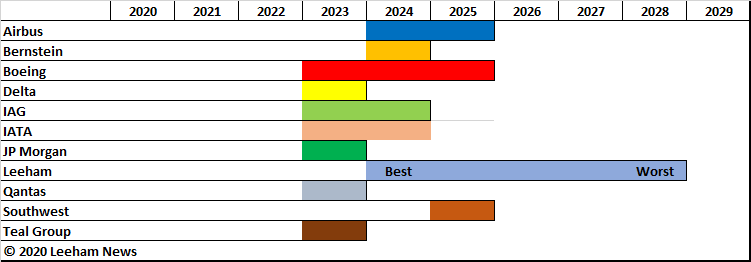

Last month, investment research firm Bernstein published an analysis calling for narrowbody traffic to recover by 2023 and widebody traffic by 2025. This is consistent with most public forecasts from airlines, banks, and industry observers. The firm’s analysts said that single-aisle concentration in short-haul and domestic routes should see them returned to 2019 utilization sooner than twin-aisles due to reduced long-haul demand and lower demand in short-haul markets previously served by widebodies (e.g., in most of Asia).

LNA believes that 2024 is the earliest possible date for a return to 2019 global passenger traffic – and it could conceivably take until 2028. Many obstacles lie between the present situation and a full recovery: deployment of a successful vaccine (or vaccines), rollback of border restrictions, passenger confidence in the medical safety of air travel, and most importantly, restored willingness to pay by business and leisure travelers. Specific countries or regions – especially those with local vaccine production – may recover sooner, but a global recovery to pre-COVID traffic levels requires all these to happen at a global scale.

To be clear, LNA’s definition of “herd immunity” is that of the global medical community: population-level resistance to virus transmission that occurs because a large majority have been vaccinated or previously infected. This differs from an increasingly popular usage of the term in reference to the passive infection-oriented virus management approach taken by Sweden and other countries.

Summary

- Widespread uncertainty means downturn likely to outstrip previous ones in duration, magnitude

- Vaccine development may be expedited; global distribution will take longer

- Herd immunity to COVID-19 is a prerequisite to confidence in travel safety, reopening of borders

- Open borders, restored economic activity are keys to any rebound in business travel

- Consumer travel requires confidence in personal income, availability of lower fares