Leeham News and Analysis

There's more to real news than a news release.

Airbus prepares contrail flight tests

July 21, 2022, © Leeham News at Farnborough Air Show: Airbus is converting two Arcus high-altitude gliders to check if the contrails produced by hydrogen combustion engines create an environmental problem.

The background is that experts can’t agree if the water vapor produced by hydrogen combustion (which merges hydrogen with oxygen to water) can cause global warming or not. The only way to resolve the dispute and gain fundamental knowledge is to fly and measure.

Figure 1. First flight with the Blue Condor program’s test aircraft. Source: Airbus.

The future small twin-aisle market

Subscription Required

By Vincent Valery

Introduction

July 21, 2022, © Leeham News: As outlined in the previous article, there are now only 46 orders for twin-aisle aircraft seating 250 or fewer passengers in long-haul cabin configuration (39 Boeing 787-8s and seven Airbus A330-800s). After adjusting for orders at risk, the tally is 28.

However, there are more than 700 older-generation aircraft in service in this segment. The lack of airline and lessor orders points to an inadequate OEM offering. Boeing is not eager to build 787-8s due to the lack of commonality with the other Dreamliner variants. Airbus’ A330-800 has meaningfully worse economics than the -900.

Among the several aircraft concepts Boeing is currently studying, a twin-aisle aircraft with up to 5,000 nautical miles nominal range for this market segment is among them.

LNA analyses in this article the addressable market for small twin-aisle aircraft.

Summary

- The addressable replacement market;

- New order opportunities;

- The impact of growth assumptions;

- Substitution effects and freighter market.

Few orders at Farnborough Day 3

By Alex Derber

(c) Airfinance Journal, July 20, 2022

The Farnborough Air Show is all but over with a few orders announced on Day 3. Airbus executives have now left the show, with no more orders expected from them.

Basking in Farnborough rebound, Boeing faces contract rejection at Defense unit

By Scott Hamilton

July 20, 2022, © Leeham News: While Boeing is basking in an upbeat Farnborough Air Show with sizable orders for the 737 MAX, it faces the prospect of losing a key contract vote on July 24 with the International Association of Machinists Local 837.

July 20, 2022, © Leeham News: While Boeing is basking in an upbeat Farnborough Air Show with sizable orders for the 737 MAX, it faces the prospect of losing a key contract vote on July 24 with the International Association of Machinists Local 837.

Local 837 represents Boeing workers in St. Louis (MO), where the Defense unit is headquartered. Union leadership recommended rejecting the contract, opening the door to a potential strike. Nearly 2,500 union members are eligible to vote on the contract offer from Boeing. The current contract expires at 12:01 AM St. Louis time on July 25.

Airbus, Boeing, Embraer, ATR orders at Day Two of Farnborugh

By Alex Derber

(c) Airfinance Journal, July 19, 2022

Commercial aircraft

– Airline investor 777 Partners placed firm orders for 30 737 Max 8200 aircraft and agreed to a further 36 commitments for the high-density Max model. The aircraft have been earmarked for 777 Partners’ two airline investments: Flair Airlines in Canada and Bonza Airline in Australia.

– Porter Airlines exercised purchase rights and signed a firm order for 20 Embraer 195-E2 passenger aircraft, adding to its existing 30 orders. Porter’s first delivery is scheduled for the second half of 2022, when the Canadian carrier will become the North American launch customer for the E195-E2, while will be powered by Pratt & Whitney Geared Turbofan engines.

– Aercap ordered five additional 787-9s, taking its existing and on-order portfolio for the widebody family to 125 units.

– Aviation Capital Group ordered 12 additional 737 Max 8s, which have expanded the lessor’s Max order book to 34 aircraft.

– Delta Air Lines confirmed additional orders for 12 Airbus A220-300 aircraft. The US airline has now ordered 107 A220-family aircraft, the first of which it received in late 2018. The aircraft are powered by Pratt & Whitney Geared Turbofan engines.

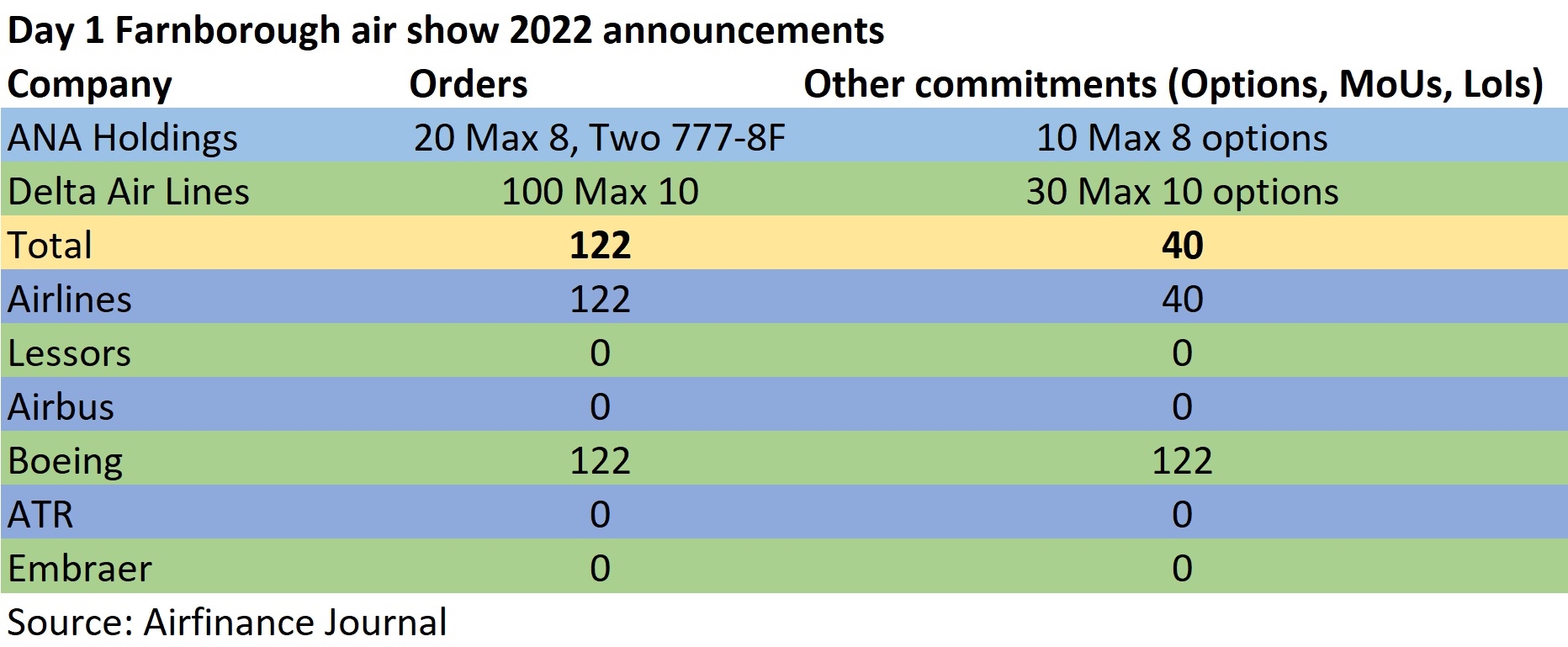

Boeing monopolizes Day 1 at Farnborough Air Show

By Alex Derber

(c) Airfinance Journal

July 18, 2022: A sweltering first day at the 2022 Farnborough air show produced only a trickle of orders, with much of what was announced having been extensively trailed in recent weeks.

Commercial aircraft

– All Nippon Airways formalised a firm order for 20 Boeing 737 Max 8 aircraft plus 10 options. The Japanese carrier was also revealed as the customer behind an order for two 777-8 Freighters, which was previously unidentified on Boeing’s website. ANA had converted an order for two 777-9 passenger aircraft to the -8 freighter.

– Delta Air Lines confirmed an order for 100 Boeing 737 Max 10 narrowbodies, signing also for 30 options for the largest member of the Max family.

Commercial engines

– Delta Air Lines ordered CFM International LEAP-1B engines to power the above order for 100 737 Max 10 aircraft. The engine order includes additional spare engines and an option to purchase up to 60 additional engines.

– Lufthansa Group ordered 14 General Electric GE9X and four GE90 engines to power its fleet Boeing 777 Freighter aircraft. The group recently announced the purchase of GE9X-powered 777-8 Freighters and GE90-powered 777 Freighters to upgrade its cargo fleet.

Boeing and Airbus make important Sustainability announcements at Farnborough.

By Bjorn Fehrm

July 18, 2022, © Leeham News at Farnborough Air Show: Boeing started the Sustainability announcements by the big two by summarizing its Sustainability efforts to date and previewing Cascade, a web tool where we all can check the lifecycle effects of actions to support Net Zero at 2050. The tool supports all technologies and any real or concept aircraft of your making. Boeing also made announcements about supporting the Global scaling of SAF (Sustainable Aviation Fuel) together with Alder Fuels.

Airbus closed the day by announcing it had pre-ordered 400,000 tonnes of CO2 Direct Air Capture performed by 1PointFive. The pre-order is in cooperation with Air Canada, Air France-KLM, easyJet, IAG, LATAM, Lufthansa, and Virgin Atlantic. One million tonnes of CO2 will be captured at a new Texas site by 2024 and then permanently stored in old oil wells.

Both companies stressed that Sustainability is, like Safety, not a competition item; instead, we must all contribute, and there is no single solution or entity that will get us to net zero by 2050.

Figure 1. Boeing’s VP of Sustainability Brian Yutko shows Cascade. Source: Leeham Co.

Assessing future twin-aisle production rates

Subscription Required

By Vincent Valery

Introduction

July 18, 2022, © Leeham News: There were 98 twin-aisle passenger aircraft deliveries in 2021, the lowest number since 1987 (90). The 2021 tally was down 73% compared to the peak of 362 deliveries in 2015.

Credit: Boeing

The minimal number of Boeing 787 Dreamliner deliveries in 2021 explains why 2021 twin-aisle passenger deliveries fell so low. However, the twin-aisle passenger market slowed down before the Covid-19 pandemic. The travel restrictions imposed during the pandemic brought long-haul traffic to levels last seen in the 1950s at the start of the jet age.

With international travel restrictions progressively lifting, long-haul traffic is gradually recovering. However, the draconian travel restrictions imposed by China and the closure of the Russian airspace to numerous airlines have slowed down the return of demand.

Airbus and Boeing reduced passenger twin-aisle production rates to a minimal: five per month on the A350 and 787 (before the production issues) and two per month on the A330neo. Boeing stopped producing 777-300ERs, with one unit pending delivery to China Southern Airlines. The extensive 777X production delays led Boeing to halt its production.

In its 2021 Commercial Market Outlook (CMO), Boeing envisioned a market for 7,670 passenger twin-aisle deliveries over the 2021-2040 period.

LNA analyses the size of the passenger twin-aisle market, both for replacement and growth. The goal is to assess the range of possible twin-aisle production rates over the next two decades.

Summary

- Outlining the analysis hypothesis;

- Assessing production rates for replacements;

- An outsized impact of growth assumptions;

- Geopolitical and environmental considerations;

- A segment with more uncertainty.

P&W, Collins Aerospace launch hybrid-electric demonstrator

By Scott Hamilton

July 18, 2022 (BST), © Leeham News: Pratt & Whitney and sister company Collins Aerospace announced the launch of a hybrid-electric technology demonstrator, it was announced today at the Farnborough Air Show. This program is for future advanced air mobility vehicles.

Collins and Pratt & Whitney Canada, the turboprop engine unit, also announced the completion of the preliminary design of a 1MW motor for the demonstrator. A De Havilland Canada Dash 8-100 will be the platform for the commercial hybrid-electric application.

Future of 737-10 MAX clouded by Calhoun: What it means

By Scott Hamilton

CEO David Calhoun said Boeing might cancel the 737-10 MAX program if the FAA doesn’t certify it by year-end or Congress doesn’t grant an extension of a mandated deadline. Photo Credit: Leeham News.

July 17, 2022, © Leeham News: Boeing CEO David Calhoun cast doubt over the future of the 737-10 MAX in a July 7 interview with Aviation Week magazine.

With questions about whether the Federal Aviation Administration will certify the MAX 10 by year-end, doubts about the program’s future had been whispered in the market for weeks. A Congressional mandate adopted in the wake of the MAX crisis established the Dec. 31 deadline for the MAX 10. Boeing already has talked with customers about swapping MAX 10 orders for the 737-9 MAX, according to market sources.

The 737-7 MAX also remains uncertified even though flight tests have been completed.