Leeham News and Analysis

There's more to real news than a news release.

Orders at risk: Year-End 2022 snapshot

Subscription Required

By Vincent Valery

Introduction

Feb. 6, 2023, © Leeham News: With the publication of the Airbus and Boeing announcing 2022 orders and deliveries last month, and Boeing’s published its 2022 Annual Report (10-K), we undertake our annual analysis of at-risk deals on their books.

Airbus and Boeing have outstanding orders with airlines where there is a material probability some orders won’t translate into deliveries. Most were the result of airlines encountering financial difficulties, but some were related to contractual disputes. Boeing flags such orders as subject to an ASC 606 accounting rule adjustment.![]()

Unlike Boeing, Airbus isn’t subject to an accounting rule like the ASC 606 adjustments at a program level. Therefore, the European OEM does not break down the orders at risk of cancellation by the program. Airbus only discloses the nominal value of its total adjusted order book in its annual report.

LNA analyzed July 2020, November 2020, August 2021, February 2022, and August 2022 Airbus’ and Boeing’s order books to identify orders at risk and come up with an apples-to-apples comparison. We update this analysis with the latest order books from both OEMs. The above links explain our methodology and its differences with Boeing’s ASC 606 adjustments.

Summary

- Lingering order book cleanup for older programs;

- Improving single aisle order book quality;

- Country-level single-aisle market share

- One order materially affects OEM twin-aisle market share.

A deep dive into the single-aisle market

Subscription Required

By Vincent Valery

Introduction

Jan. 23, 2023, © Leeham News: Boeing’s share of outstanding single-aisle orders has fallen significantly behind Airbus. If we include the order book for single-aisle aircraft seating 100 or more passengers of Airbus, Boeing, COMAC, Embraer, and UAC, the American OEM’s market share is now 37% (Airbus has 58%, COMAC 3%, Embraer 2%, and UAC 2%).

Richard Aboulafia sees a risk that Boeing’s market share in the single-aisle market will dip below 30% without the entry into service of a new aircraft before 2035. Boeing Commercial Airplanes CEO Stan Deal said that it is viable for the American OEM’s single-aisle market share to stay around 40%.

A321neo Credit: Airbus

In the 2022 Boeing outlook, LNA also noted that there are significantly more A320ceo than 737 NG operators. A broader operator base means more opportunities to place new orders with a more diversified group of airlines. In the context of no new single-aisle family entering service in the next 10 years, convincing operators to “flip” to the competition will be the primary way to increase market share.

Exclusively looking at the nominal order books and A320ceo and 737 NG operators does not provide a comprehensive view of Airbus’ and Boeing’s relative positions in the single-aisle market, though.

In their 2022-2041 commercial market outlooks (CMO), Airbus and Boeing indicated that nearly half of all single-aisle deliveries would replace older-generation aircraft. Looking at the existing in-service fleet of older-generation aircraft provides a better picture of replacement order opportunities by the OEM.

LNA investigates in this article the existing order books of the five major OEMs and operator bases to better assess their relative competitive positions and quantify the current replacement order opportunities.

Summary

- A comprehensive single-aisle fleet snapshot;

- Breaking down the order books between replacements and growth;

- Keep track of order choices for older-generation operators;

- Remaining replacement order opportunities;

- A word about single-aisle freighters.

Outlook 2023 for China’s COMAC and Russia’s UAC

Subscription required

By Bjorn Fehrm

Jan. 12, 2023, © Leeham News: China’s civil airliner OEM, COMAC, made significant progress during 2022. It achieved Chinese certification for its C919 158-seat domestic airliner in September last year, with the first delivery to the launch customer, China Eastern Airlines, in December. The first aircraft will be used in trial operations during 2023. The C919 follows the regional ARJ21, which has been in operation in China since 2016.

The progress, after several delays, of the COMAC programs is in stark contrast to the airliner progress of Russia’s UAC. The slow progress for the SSJ100, MC-21, and Il-114 programs has now ground to a standstill since the invasion of Ukraine and the ensuing Western sanctions.

Figure 1. Test flight of the first series delivery C919 of China Eastern Airlines. Source: Wikipedia.

Summary:

- China and COMAC have made significant progress in 2022 and will gradually build a viable airliner industry from 2023 onwards with a regional and single-aisle offering.

- The opposite is true of Russia’s UAC. A once viable airliner industry is now crushed by the Kremlin’s decision to invade Ukraine.

China still needs Boeing as much as Boeing needs China, despite interminable limbo

Subscription Required

By Scott Hamilton

Oct. 31, 2022, © Leeham News: China needs Boeing as much as Boeing needs China was the conclusion of an analysis by LNA in July 2021. A trade expert last week agreed. Airbus and China’s COMAC won’t be able to fill the future demand forecast for China.

Michael McAdoo, Partner & Director, Global Trade and Investment of the Boston Consulting Group (BCG) in Montreal and a former strategic chief of Bombardier Commercial Aircraft, told LNA in an interview last week that China needs the Boeing 737 MAX and widebody airplanes to meet demand in the near-to-medium term.

It will be long-term before China’s commercial aviation industry will be competitive with airplane designs and production.

Summary

Forecasts for China’s demand for jet aircraft are consistent between Airbus and Boeing. But COMAC, which is the leader of China’s burgeoning commercial aviation industry, is significantly higher in its forecast. The independent Japan Aircraft Development Corp (JADC) is significantly lower.

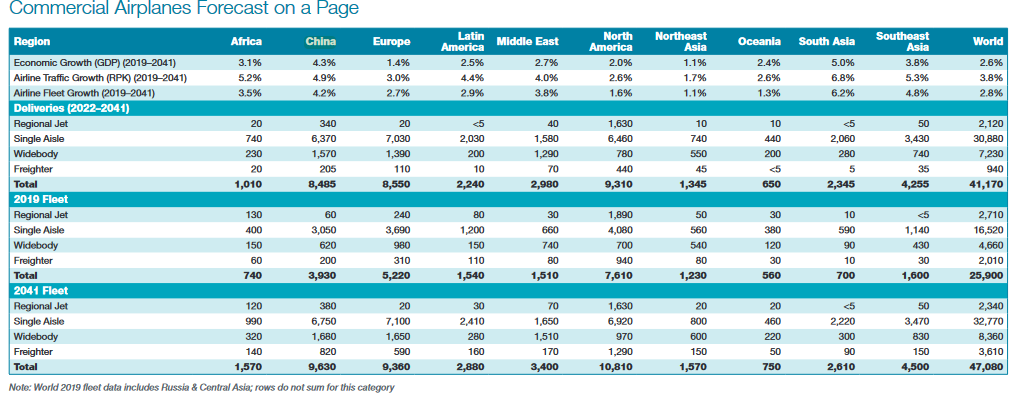

- Boeing forecasts that China needs 8,485 new jets through 2041.

- Airbus forecasts 8,420 new aircraft will be needed through 2041.

- COMAC forecasts China will need 9,084 aircraft through 2040.

- JADC is more conservative, forecasting a requirement for 6,172 new jets in China through 2041.

Source: Boeing Current Market Outlook.

China will account for 21% of the world’s new aircraft deliveries through 2041, Boeing says.

Pontifications: From the aviation perspective, there’s something in China to watch

March 21, 2022, © Leeham News: Eyes are focused on Ukraine and the Russian War. In our corner of the world, commercial aviation, the stakeholders follow the fallout from the war: sanctions placed on Russia which affect overflights, supply chains, oil to Europe (fuel), and Russia’s confiscation of about $10bn worth of airliners from Western lessors and lenders.

By Scott Hamilton

But there is another drama playing out on the other side of the world, too. This one involves China and one of its commercial aviation companies, AVIC.

AVIC is a major aerospace company in China. It also has a variety of none-aerospace companies. It’s one of these that caught our eye last week.

The Wall Street Journal on March 14 reported that AVIC subsidiaries involved in solar energy filed for bankruptcy to avoid an $85m judgment after allegedly absconding with intellectual property from two US companies. The firm had to settle for 30 cents on the dollar.

It’s another example of China companies simply ignoring international IP laws.

2022 Forecast: C919 EIS unlikely before 2023-24

Subscription Required

By Scott Hamilton

Introduction

Jan. 17, 2022, © Leeham News: COMAC, the Chinese aerospace company developing the C919, suffered yet another setback last year.

It hoped to deliver the first aircraft, designed to compete with the Airbus A320 and Boeing 737-800/8, to China Eastern Airlines by year end. Not only didn’t this delivery take place, but the program is also only about 15% through the certification flight testing.

COMAC C919. Source: China Factor.

At this rate, certification, and delivery this year is questionable. LNA’s forecast for EIS is in 2023 or 2024.

COMAC’s other airplane, the regional jet ARJ21, landed its first order outside China (other than from lessor GECAS years ago).

Summary

- C919 is overweight, shortening range, and adversely affecting fuel economy.

- Commercial success of the C919 won’t be possible.

- ARJ21 lands first foreign operator, but it’s not an arm’s length deal.

2022 Outlook depends largely on pandemic, Boeing recovery

Subscription Required

By the Leeham News Team

Dec. 13, 2021, © Leeham News: Attempting a forecast for the new year historically has been reasonably easy. One just started with the stability of the current years, and maybe the previous one or two years, and looked forward to next year.

Until the Boeing 737 MAX grounding, COVID-19 pandemic, and the Boeing 787 suspension of deliveries.

These events upended everything. Boeing’s outlook for 2020 depended on what happened to return the MAX to service. The grounding, initially expected by many to be measured in months, ultimately was measured in years.

The 2020 outlook for the rest of the aircraft manufacturers blew up that March with the global pandemic.

Then, in October 2020, Boeing suspended deliveries of the 787, exacerbating its cash flow crunch.

Commercial aviation began to recover some in late 2020. Airbus, which reduced but didn’t suspend deliveries throughout 2020, saw signs of hope for the narrowbody market—less so for widebody airplanes.

There is a lot of uncertainty, however, that makes looking even one year ahead challenging.

C919 EIS target year end; production rate forecast is aggressive

Subscription Required

By Scott Hamilton

Introduction

Sept. 13, 2021, © Leeham News: The first COMAC C919 is supposed to be delivered to China Eastern Airlines before the end of the year.

If so, it will be the milestone of the program launched in 2008, 13 years ago, becoming one of the longest launch-to-EIS in aviation history. COMAC’s ARJ 21 took one year longer. This regional airliner program was launched in 2002. Entry-into-service was in 2016.

The C919 is China’s direct challenge to the Airbus A320 and the Boeing 737. Similar in appears to the A320, for which there is an assembly line in Tianjin, the C919 is powered by the CFM LEAP 1C and a domestically-produced engine. But the C919 only has an advertised range of 2,200-3,000nm. The A320 and 737-8 have ranges of 3,500 and 3,550nm, respectively.

COMAC forecasts producing 150 C919s a year by the middle of this decade. Achieving this rate in this period should be a major challenge. Based on normal learning curves, a more realistic ramp up to 150 a year will take until early 2031.

Summary

- China forecasts a production rate of 150/yr by the middle of the decade.

- History suggests a much lower rate by then.

- LNA’s production rate forecast is detailed through 2030.

Here’s why China needs Boeing as much as Boeing needs China

Subscription Required

Now open to all readers.

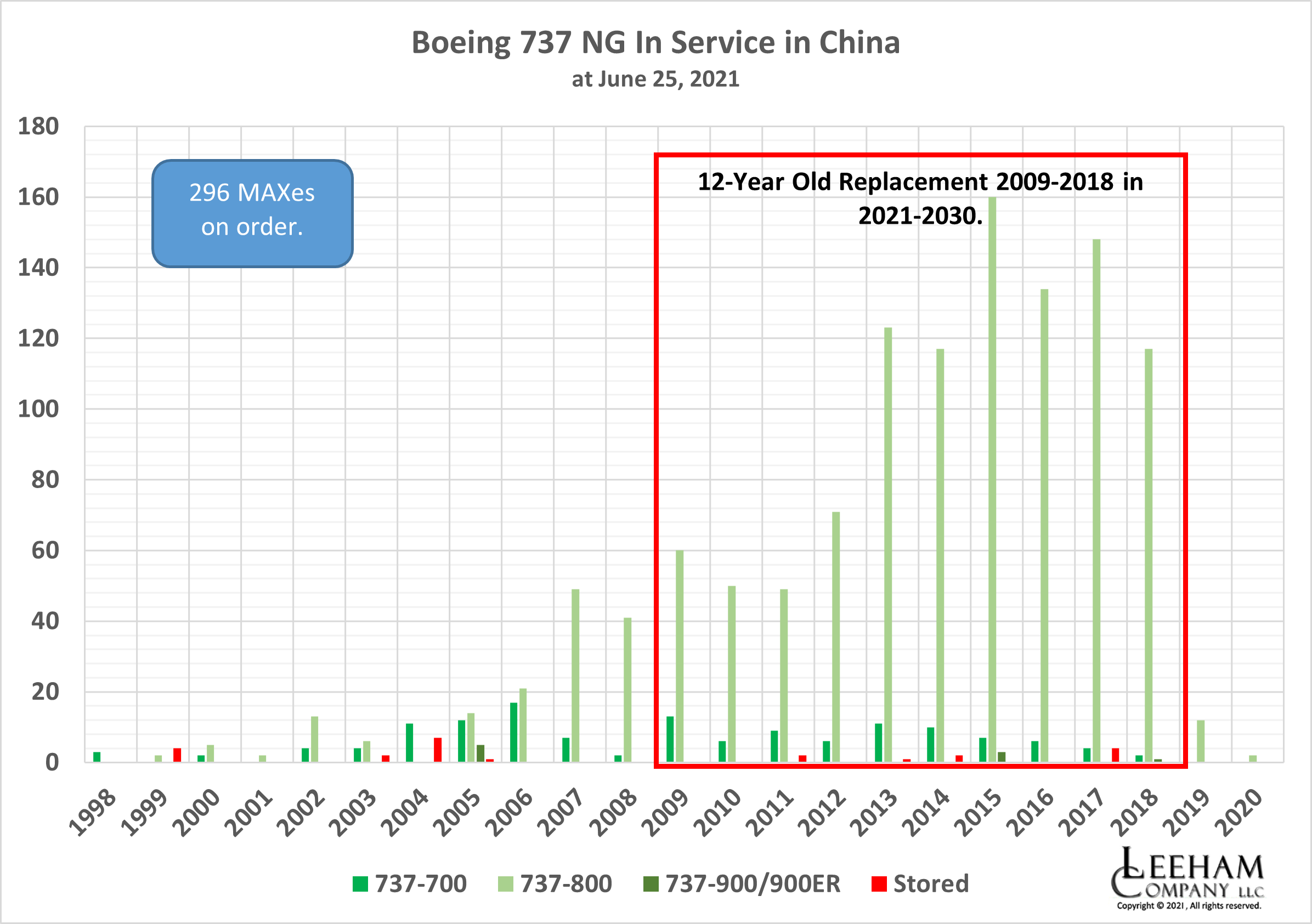

July 7, 2021, © Leeham News: China’s government policy of operating commercial aircraft that generally are no more than 12-15 years old means the carriers face a replacement bubble that the home market can’t possibly meet.

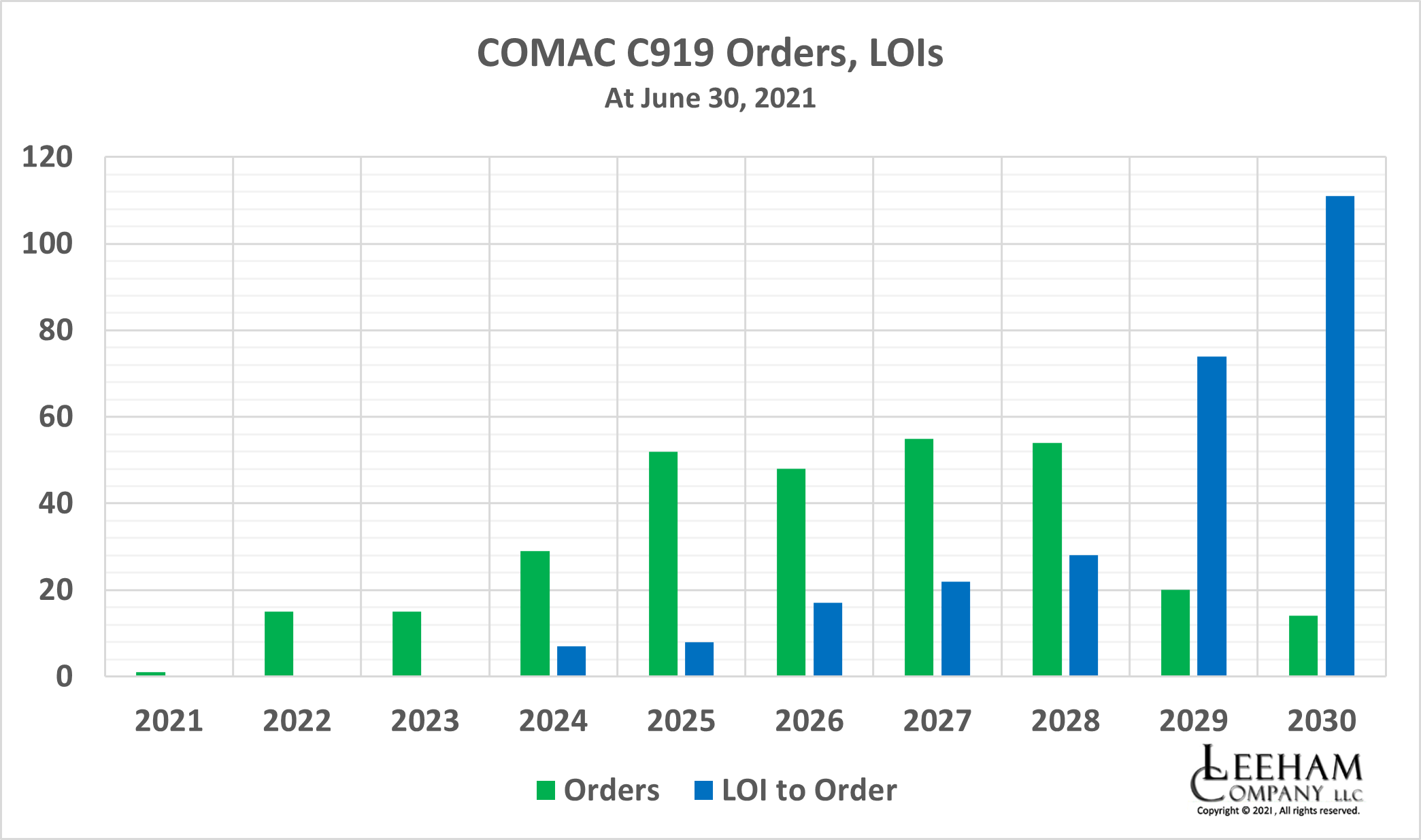

According to data reviewed by LNA, there are just 303 COMAC C919s on order. Delivery is supposed to begin this year with one airplane. Currently, the peak year for deliveries is 2027 with 55 aircraft scheduled.

There are about 1,116 Boeing 737 NGs built between 2008-2018 operated and stored by Chinese carriers. China has just 296 737 MAXes on order—a deficit of 820 aircraft needed for replacement of these aging airplanes. (Boeing’s website shows just 104 outstanding orders, but Chinese-owned lessors aren’t included in this tally.)

Pontifications: The WTO Airbus/Boeing standstill and pursuing China

June 28, 2021, © Leeham News: The US and European Union agreed on June 15 to a standstill in the 17-year old trade dispute over illegal subsidies to Airbus and Boeing.

The World Trade Organization (WTO) found each violated international rules. By the time all was said and done, the US was authorized to levy tariffs on $7.5bn worth of European goods. The EU received authorization to levy tariffs on $4bn of US goods.

Tariffs on goods went beyond Airbus and Boeing products. But it was 15% tariffs on Airbus planes imported into the US and Boeing planes imported into the EU that were the highest-profile and most costly.

Despite initial reports in some uninformed media that the long-running dispute was “resolved,” in fact, only a standstill was agreed. The US and EU now have five years to negotiate a permanent settlement to Airbus’ “reimbursable launch aid” and Boeing’s benefits from tax breaks and NASA.

The two sides also agreed to put China’s commercial aerospace industry in the crosshairs.