Leeham News and Analysis

There's more to real news than a news release.

Bombardier’s crisis of confidence perhaps the biggest challenge for CSeries

Subscription Required

Introduction

Feb. 18, 2015, c. Leeham Co.: Alain Bellemare, Bombardier’s new president and chief executive officer, has his work cut out for him.

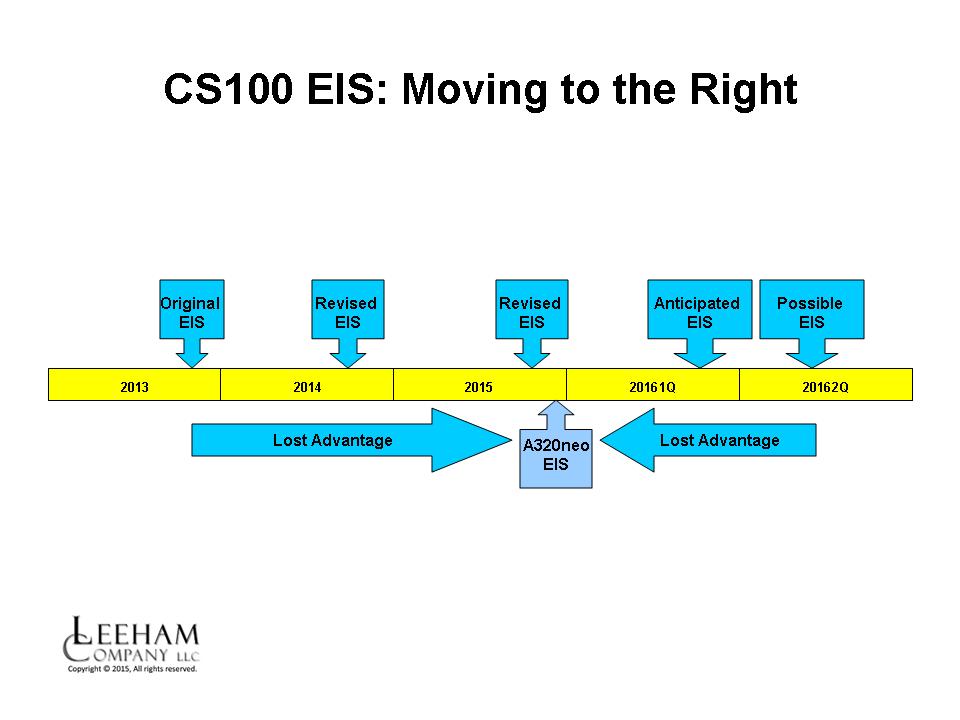

Figure 1. The CSeries was supposed to enter service in late 2013, two full years ahead of the Airbus A320neo. This market advantage has been lost with repeated delays. BBD is sticking to its public statement that EIS is now the second half of this year (most put EIS in the fourth quarter), but there is growing belief EIS will slip to the first or even the second quarter of next year–after the A320neo EIS. Source: Bombardier, Airbus, Leeham Co. Click on image to enlarge into a crisp view.

We outlined the corporate and market perception challenges ahead of him in our Feb. 13 post. Investor and media reception to the CEO leadership change was mixed. Although Bellemare’s appointment was seen as a positive, stock traded down and Bombardier took a pounding in the press (see some reaction at the bottom of this post).

He also has challenges with a changing market place, driven by two years worth of delays in the CSeries program and exacerbated by a changing global political environment.

Summary

- Bombardier faces a crisis in confidence from customers that has to be fixed.

- The CSeries has lost its entry-into-service advantage over the Airbus A320neo and has reduced its advantage over the A319neo, the Boeing 737-8/7 and Embraer E-190/195 E2 EIS due to delays.

- A changing global political environment poses additional risks to the CSeries skyline.

Regional operations with the Turboprop, prop-jet or Jet

- We examined the future of turboprop airliners Jan. 5, 2015, analyzing the backlogs of Bombardier and ATR–and the ATR overwhelming dominance of the current turboprop sector. This is the second of a series looking at this sector.

By Bjorn Fehrm

Subscription required

Introduction

08 Feb 2015: Passenger traffic is growing the world over on a regional, domestic and international level. For domestic and international airlines the choice of mainline transport aircraft is clear today: there are only two vendors, Boeing and Airbus, and they produce similar products.

For regional transportation there is more choice. First of all, one can chose type![]() of aircraft, turboprop or jet. Within jet, there are several OEMs that are active. The choice in turboprop is more restricted. In practice, the choice stands between the classical turboprop with ATR and a faster type from Bombardier, the Q400 “Prop-Jet” as it is called, as its speed lands between the classical turboprop and regional jet.

of aircraft, turboprop or jet. Within jet, there are several OEMs that are active. The choice in turboprop is more restricted. In practice, the choice stands between the classical turboprop with ATR and a faster type from Bombardier, the Q400 “Prop-Jet” as it is called, as its speed lands between the classical turboprop and regional jet.

The question is, what are the real differences between them in terms of design, passenger comfort and economics and what is the right choice for a market segment? We will take a deeper look into this by analyzing the ATR72 as the classical turboprop, the Bombardier Q400 as the Prop-Jet and CRJ700 as the regional jet.

Summary:

- The ATR72-600, Bombardier Q400 and CRJ700 are all about the same size, around 70-80 seats single class or 60-70 seats dual class.

- They offer different comfort levels, and it is not all about speed.

- In developing the economics in two steps we seek the crossover points between the different types.