Leeham News and Analysis

There's more to real news than a news release.

Airbus COO faces production challenge vs bulging order book

Subscription required.

Now open to all Readers.

Introduction

June 15, 2015, Paris Air Show, c. Leeham Co. Airbus, like Boeing, is faced with an embarrassment of riches: too many  orders for the A320 and A350 production rates that have been announced. There’s pressure from the top commercial officer to hike rates, but the president and chief operating officer says not so fast.

orders for the A320 and A350 production rates that have been announced. There’s pressure from the top commercial officer to hike rates, but the president and chief operating officer says not so fast.

Tom Williams was elevated to the presidency only a few

months ago from his position as EVP-Programs, where he was in charge of production and the Airbus supply chain. Williams, a Scotsman and the first non-French or non-German to be president and COO of Airbus Commercial, ruefully observes he didn’t give up the production and supply chain duties with his new title.

Although Williams agrees with John Leahy, chief operating officer-customers, that demand indicates higher rates are needed for the A320 and A350, the demands on the supply chain for Airbus, as well as the other airframers, also demands caution.

- Summary

- Decision end of this year or early next on A380 production rates.

- A380neo launch aid reported—but it’s premature.

- No decision yet on greater than 50 A320 production rate per month.

- Pondering hike in A350 production rate beyond the 10/mo announced.

- Cabin suppliers a top concern.

Bombardier ‘transformation initiative’ goes after costs across the enterprise, supply chain

June 8, 2015, c. Leeham Co. Bombardier suppliers, already squeezed by Airbus and Boeing to cut costs and prices,

Alain Bellemare, CEO of Bombardier.

will soon face a new effort from Bombardier to do the same.

The new chief executive officer, Alain Bellemare, last week announced a “transformation initiative,” of which going to the supply chain is but one part for cut costs across the enterprise.

Bellemare, who was named CEO in February, knows something about cost cutting. He was an executive at Pratt & Whitney, a unit of United Technologies, before coming to BBD, and has been on the giving and receiving end of demands to cut costs.

Bellemare was named with the charge to restructure Bombardier, after billions of dollars in losses, cost over-runs and delays in corporate and commercial aircraft programs, the highest profile of which is the CSeries. The CSeries is the bet-the-company leap into mainline jet aircraft which, at the lower end, compete directly with Airbus and Boeing.

In an interview with Bellemare at the International Air Transport Assn. Annual General Meeting Monday in Miami, Bellemare covered a wide range of subject about how BBD will be remade.

Paris Air Show: Qatar and others

Subscription required.

Introduction

June 1, 2015, c. Leeham Co. It could be called the Qatar Airways Air Show.

Qatar Airways plans to have five airliners on display at the Paris Air Show in two weeks: the Airbus A319, A320, A350, A380 and the Boeing 787. The carrier hasn’t  announced whether it will provide an aerial display as it has at previous air shows, but Qatar may well have more airliners there than Airbus or Boeing.

announced whether it will provide an aerial display as it has at previous air shows, but Qatar may well have more airliners there than Airbus or Boeing.

As for manufacturers other than Airbus and Boeing, we don’t expect anything of consequence from these.

Summary

- Irkut, COMAC, Mitsubishi, Sukoi and ATR are other major aircraft producers that will be at the Paris Air Show.

- Engine makers CFM International, GE Aviation, Rolls-Royce, Pratt & Whitney and Engine Alliance will also be there.

- An update on Airbus expectations.

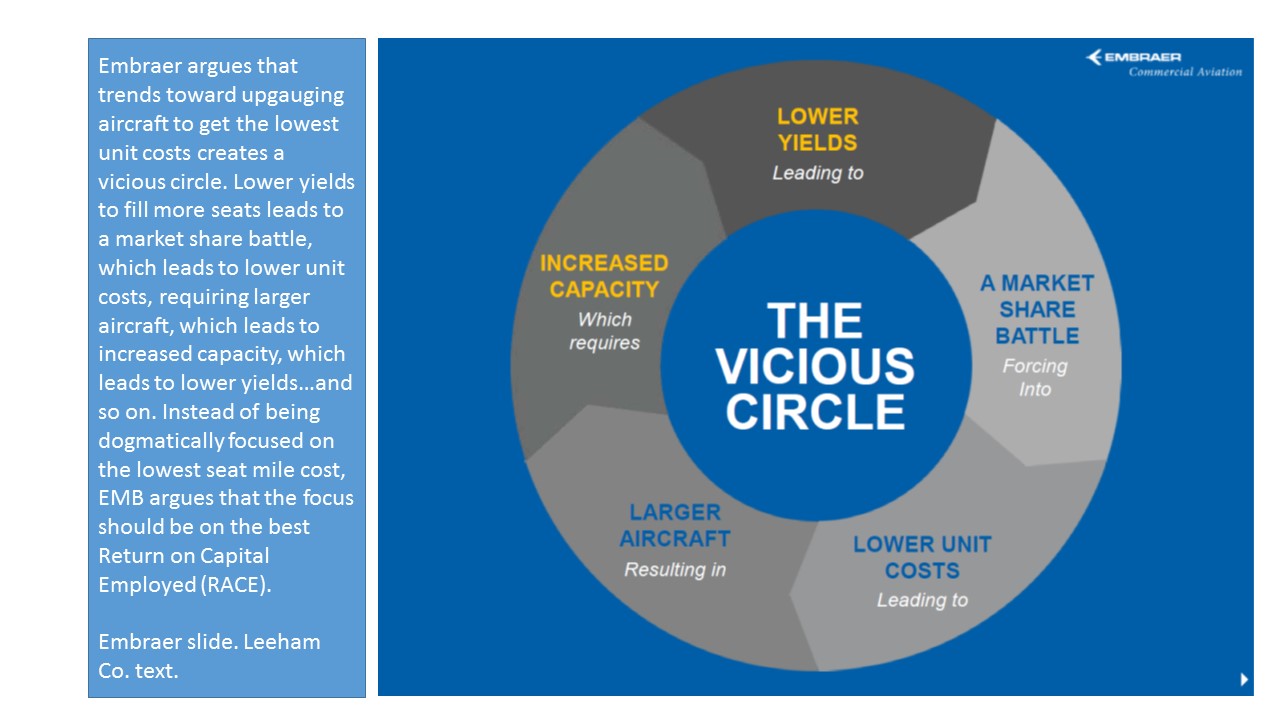

Embraer ramps up smaller airplane messaging

Figure 1. Click on image to enlarge.

May 28, 2015, c. Leeham Co. Embraer is ramping up is messaging that the E-Jet family provides a better Return on Capital Employed in many circumstance than the larger Airbus and Boeing single-aisle family.

In a new push to be unveiled at the Paris Air Show in a little over two weeks, Embraer will describe its “New Metrics for Success” to an international audience in an open forum.

EMB has been showing airlines and lessors the concept for some time, and we received a briefing on the essential elements when we visited EMB last October at is home base in San Jose, Brazil.

New Metrics for Success takes airlines away from the traditional metric of economics, the Cost per Available Seat mile, and focuses trip costs and the higher quality revenue obtained by limiting the number of low-yield seats on a flight that must be offered to fill larger airplanes. Read more

Flying the Airbus A350

By Bjorn Fehrm

Introduction

May 25, 2015, c. Leeham Co. Friday we showed our little video from our test flight of Airbus A350 at end of April. Now it is time to describe the impressions during the flight more in detail. Different from the excellent reports of other magazines that were present, we will look deeper into flying an aircraft with Fly By Wire in contrast to a conventionally controlled aircraft and less in trying to compare the A350 with other airliners, as we don’t have this experience.

Our lack of experience in flying airliners has an advantage when it comes to first impression of how it is to fly the much-discussed Airbus Fly By Wire (FBW) concept. My experience so far has all been non-FBW aircraft, from very small and slow (Tiger Moth) to the fast and a bit larger (Mach 1.7 SAAB Draken). In all, I’ve flown 14 different types. To that, one can add having flown the Embraer KC-390 simulator last October. Some of the aircraft have had no servos. Others had 100% servos with artificial feel through springs working on the stick. Autopilots have differed widely from wings leveler to flight director aircraft with coupled ILS approaches. None has had auto-thrust to date except for the KC-390.

Bjorn’s Corner: Bombardier’s and Embraer’s first quarter

By Bjorn Fehrm.

07 May 2015, C. Leeham Co: Last week we looked at Airbus first quarter result and compared its commercial aircraft unit with Boeing’s. Now with do the same with Bombardier and Embraer. As both have sizeable Business jet businesses we will include these in the analysis as they share many technologies and developments with the commercial aircraft.

Embraer reported their results last week and Bombardier today. Both reported quarters in the aerospace area which were a bit inferior to last years first quarter and for the same reason, the Biz jet market has gone soft.

Bombardier, who has a larger proportion of its turn-over in Biz jets, has managed this better, it has delivered more aircraft and generated slightly higher revenue and profits from the area but new orders has been slower.

Embraer does separate its business segments for revenue but not for profits. It reports that the lower revenue and profit for the quarter was mainly because the Biz jet area delivered fewer aircraft at less margin. Commercial aircraft deliveries were strong, with good efficiencies in the production and delivery of E-Jets. Read more

Paris Air Show Preview: Airbus

Subscription Required.

Introduction

May 3, 2015, c. Leeham Co. The Paris Air Show is June 15-19 for the trade/industrial portion. Beginning this week, Leeham News and Comment will provide our

![]() Market Assessment and insight about what to expect. We begin this weekly exercise by looking at Airbus. Future posts will look at Boeing, Bombardier, Embraer and other major players at the PAS.

Market Assessment and insight about what to expect. We begin this weekly exercise by looking at Airbus. Future posts will look at Boeing, Bombardier, Embraer and other major players at the PAS.

Summary

- First, an overarching look at what to expect;

- What to expect for Airbus at the show;

- The future of the A380neo;

- Outlook for the A330ceo/neo; and

- Outlook for the A321LR.