Leeham News and Analysis

There's more to real news than a news release.

ISTAT: Randy Tinseth: pax traffic going from 3bn today to 7bn by 2033

Randy Tinseth, VP Marketing of Boeing, presented today to the ISTAT conference. Here is a synopsized summary of his comments.

ISTAT: Airlines look at the market and explain differences between the past and today

March 9, 2015: The top four players now are acting differently than previous eras, focusing on profits and return on capital instead of market share, says Mark Eliasen, vice president of finance and treasurer of Alaska Airlines.

Alaska returned 18% on its margin, the highest in the US industry, with low costs relative to its competitors. The company has grown at a rate of 7% year over year for several years. “We’re really happy with a single fleet.” The Boeing 737-focus allowed dramatic gains in lowering costs.

Of the five investment grade airlines, Eliasen notes that four of them are single-fleet carriers.

Nico Buchholz, EVP of Fleet Management of Lufthansa Airlines, said European carriers don’t have capacity discipline and the network carriers have to reinvent themselves. Lufthansa Group includes low cost carriers that are growing while Lufthansa itself strives to be the No. 1 choice for its traditional market.

Eurowings, a Lufthansa company, provides low cost service to short haul routes and soon is expanding to long haul. Eurowings prompted other LH airlines, including Austrian, Lufthansa and Swiss, to lower costs because if they didn’t, growth would happen at Eurowings.

Buchholz predicts consolidation in Europe and says Lufthansa Group and IAG (the British Airways group) will be two of the survivors. “But I wouldn’t go beyond that” in predictions, at least not before the crowd of 1,800 at the ISTAT conference where the remarks were made.

ISTAT: Warning signs for airline industry

March 9, 2015: There are warning signs the global airline industry needs to heed, says John Luth, CEO of the US consultancy Seabury Group.

The economic recovery isn’t uniform across the globe, Luth said in the keynote address to ISTAT, the International Society for Transport Aircraft Traders at its 2015 conference in Phoenix.

Luth said North American airlines had to “fix” themselves before consolidation into four major carriers that now control 71% of the market. In Europe and Asia, the top four carriers control far less traffic. In Europe, low cost carriers now control 40% of the market while in Asia LCCs control 19%, a sharp rise over a few years ago.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 4.

By Bjorn Fehrm

Subscription required

Introduction

08 March 2015, c. Leeham Co: In the third part of the article series around the need for a more capable solution for 180-240 seats and 5,000 nautical miles, we compared different clean sheet single and dual aisle aircraft to the Airbus A321LR and Boeing’s 787-8, the two aircraft that form the border to the segment.

We could see that a single aisle aircraft started to have trouble with weight at around 220 passengers using our normalized seating rule set. This would with normal OEM seating rules be around 230-240 passengers. At the same time the dual aisle aircraft becomes stronger the more seats one assumes. The reason is their thicker fuselage, Figure 1, lends itself better to aircraft which passes 50 meters/160 feet in length.

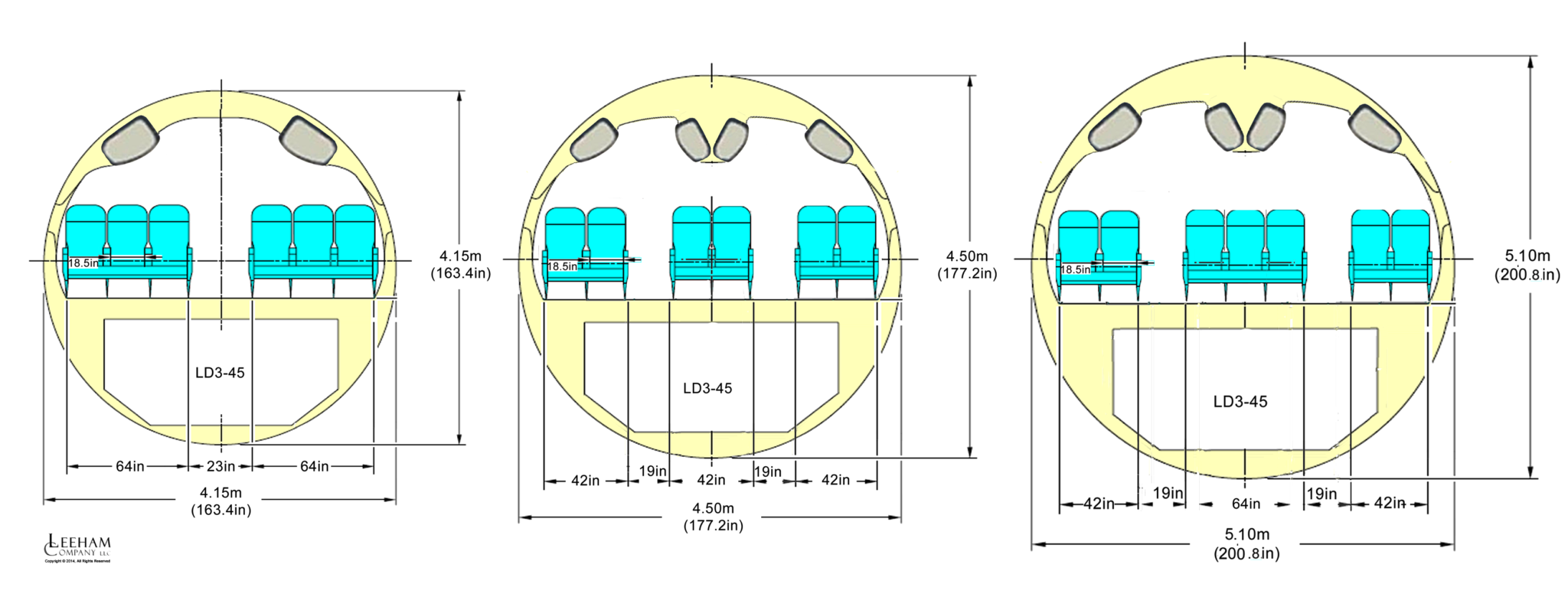

Figure 1. Cross sections for our studied clean sheet designs; NSA6 (New Single Aisle 6 abreast), NLT6 (New Light Twin 6 ab.) and NLT7. Source: Leeham Co.

Their advantages in boarding and deplaning then starts to outweigh their disadvantages in weight and drag. This trend is explored further in this part where we add Cash Operating Cost, COC and Direct Operating Cost, DOC, to the analysis.

Summary

- The trends seen for NAS6, NLT6 and NLT7, our Middle Of the Market, MOM, models in the segment 180 to 240 passengers gets further reinforced when we go to COC and DOC.

- A factor supporting this is the broader spread of fixed and semi-fixed costs over larger aircraft seat numbers.

- Another is that the shorter ground turn-around time for dual aisles increases the utilization for the aircraft, once again forming a broader base for fixed and semi-fixed costs.

- Introducing CFRP for the fuselage brings clear gains in weight and therefore operating costs. Key for its inclusion in the MOM designs will be the manufacturing advances that will have been made by 2025.

Pontifications: Boeing cracks open door to 777 production rate cuts (or not)

By Scott Hamilton

March 8, 2015: Boeing cracked open the door March 5 to a production rate reduction on the 777 Classic, the first time since launching the 777X in 2013 that officials have publicly deviated from their insistence the current rate of 8.3/mo can be maintained to entry-into-service of the 777X.

At least that’s how I see it. Boeing sees it differently. Boeing says nothing has changed in its messaging.

In an appearance at the JP Morgan Transportation Conference, Greg Smith, EVP of Business Development and Strategy and Chief Financial Officer of The Boeing Co., Smith appeared to back away from the Boeing messaging to-date that has been all (to paraphrase) “We’re confident we’ll bridge the gap,” “We have three years of backlog and six years to bridge the gap”, “We’re confident we’ll maintain production at the current level,” etc, etc.

At least that’s how an aerospace analyst for a New York firm expressed it when he called me. After listening to the event, I agree with the analyst.

In the recorded playback of the JP Morgan event, here’s the report of Smith’s comments starting at 9:36 into the presentation.

Pontifications: A350 launch aid, Emirates and the A380, Bombardier and U-Turn Al

By Scott Hamilton

March 5, 2015: A350 Launch Aid: Boeing and the US Trade Representative got in a big twist around 2006 when Airbus said it would accept more than $1bn in launch aid from Germany for the A350. At that time, the US and European Union had recently launched the international trade complaints before the World Trade Organization (WTO), but the A350 came after the complaint was filed and the WTO refused the US request to add it to the proceedings.

Germany, in a political snit, later said it would withhold part of the launch aid because Airbus hadn’t promised the number of jobs in connection with the program to Germany that politicians wanted.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 3.

By Bjorn Fehrm

Subscription required

Introduction

04 March 2015, c. Leeham Co: In the first and second part of the article series around the need for a more capable solution for 180-240 seats and 5000 nautical miles, which we have labeled the 225/5000 Sector, we went through the derivatives we have analyzed as competitors to Airbus A321LR and showed why none of them are effective as a Boeing solution.

We also looked at the wetted area and weight for our common single and dual aisle aircraft. These parameters are the principal components that determine an aircraft’s efficiency given a certain engine efficiency. We also developed the market picture, outlining a substantial market by the time of entry into service of a clean sheet design by 2025, given that certain market requirements could be fulfilled.

We will now project different solutions to the requirements, thereby utilizing the preliminary design part of our proprietary aircraft model. We will look at three different cabin configurations in four different size classes between 180 to 240 seats and calculate size and weights and the resulting efficiency of the different variants. Against the key data for these different aircraft and their operational efficiency we will be able to postulate what will be the next move from Boeing and Airbus in this segment.

Summary

The findings in this our third article include:

- Aircraft capacity and size for 12 different possible aircraft, named NAS6, NLT6 and NLT7 each in the variants 180, 200, 220 and 240 passengers.

- With this collection of characteristics it will be possible to compare the efficiency and costs for the different sizes and to see how competitive a wider dual aisle aircraft will be in this segment compared to a single aisle.

- In a subsequent article will be compare the operational characteristics of these aircraft thereby also covering the increased revenue potential with a dual aisle aircraft compared to a single aisle.

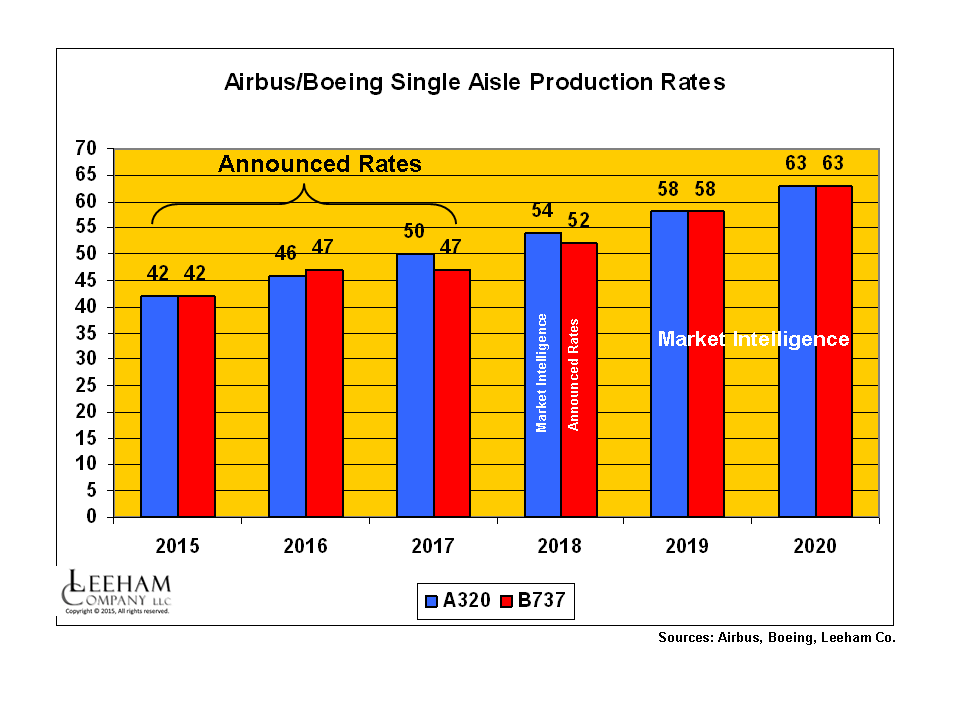

Production rates on single-aisles keep going up, up

Figure 1. Airbus and Boeing production rates for the A320 and 737 lines are going up as announced rates and rates under consideration go to lofty levels. Click on image to enlarge.

Subscription Required

Introduction

March 3, 2015: c. Leeham Co. Production rates for single aisle airplanes continue to go up for the Big Two, following the Airbus announcement last week that the A320 rates will go to 50/mo in 2017 and officials are considering going to more than 60/mo.

We’ve previously reported that Airbus already has notified the supply chain to be prepared to go to 54/mo in 2018.

Rate 50 will propel Airbus ahead of Boeing, which will briefly be ahead of Airbus when the 737 production rate goes to 47/mo next year, compared with the Airbus plan to take A320 rates to 46/mo next year. The two companies are at parity this year. (Figure 1.)

Summary

- Bombardier, COMAC and Irkut add to supply by 2020, but impact will be minimal.

- No 747-8 deliveries scheduled in 2018. We see program termination coming very soon.

- A330ceo production rate reduced, higher rate for 787 than announced.

- We see short-term Airbus advantage coming in wide-body production rates as A350 ramps up. We stick with our call that 777 Classic rates have to come down.

- We reduce A380 production rates in our estimates.