Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Aircraft values vary widely

By Scott Hamilton

Dec. 14, 2015, (c) Leeham Co: Aircraft valuations came to the forefront following comments by Richard Anderson, CEO of Delta Air Lines, over just how much a 10-year old Boeing 777-200ER was worth. He claimed the airplane was only valued at $10m. Boeing’s investor relations department immediately pushed back against this low price, circulating to the aerospace analyst community that a number of appraisers placed the value in the $50m-$60m range.

Anderson later was quoted as saying Boeing Capital Corp. offered Delta the aircraft for that price. BCC didn’t comment.

LNC wrote at the time, and later, that Anderson was correct. We noted, however, there are a lot of caveats that come with the $10m, rooted in the fundamental fact that this price had to be for a “run out” model that would require expensive airframe and engine maintenance, repair and overhaul, and interior reconfiguration. This could add as much as $30m to the price, or $40m all-in–still substantially less than the appraised figures for a “half-life” example.

Appraisals are an inexact exercise that not only depend on the maintenance condition of the airplanes, whether they are “desk-top” or inspection appraisals and the methodology of the various appraisal companies, backed by market intelligence data.

Bjorn’s Corner: Twins or quads?

By Bjorn Fehrm

11 December 2015, ©. Leeham Co: The debate over two or four engines for long range aircraft is as old as the jet airliner. A number of myths have been pedaled over the years over the virtues of the one over the other. The myths have even been presented by airline CEOs as “facts that are known in the industry.”

Having done several in-depth comparisons of two-vs-four engined long range aircraft, we can’t find the patterns that these myths propel: that a quad is less efficient than a twin and should have higher maintenance costs. What we see is that it is all dependent on what one compares and to what technology generation the one or the other aircraft belong.

When we didn’t get the same results as the myths on a number of areas, we started to wonder what could have created the myths in the first place. Looking at what four engined airliners could have been the source of the rumours, we started to see a pattern. It was a pattern of apple-and-oranges being compared and wide ranging conclusions being drawn.

Here is what we found. Read more

IBA recaps Boeing 777 focus conference

Dec. 9, 2015: The aircraft appraisal firm IBA, headquarter in the UK, issued a recap of the Airline Economics one day conference about the Boeing 777 market that focused on values and marketability of the aircraft. These have been topics of international discussion ever since Boeing launched the 777X (and, really, for some time before) and Boeing faced the challenge of bridging the production gap between the 777 Classic and the 777X.

Used B777-200ER or A340-300, Part 3

Subscription required

Introduction

By Bjorn Fehrm

Dec. 9 2015, ©. Leeham Co: We have now covered the Cash and Direct Operating Costs (COC, DOC) for our acquired and refurbished Airbus A340-300E and Boeing 777-200ER. We will now finish the article series by looking at the earnings capability of the aircraft and compare these to the cost.

We will start by examining the payload carrying capability of the aircraft over different stage lengths by means of the aircraft’s payload-range diagram. Any excess payload capability over a cabin filled to a normal load-factor will be used to add cargo to the revenue stream.

Finally, we will value the payload according to the market’s standard yields for Business, Economy and Cargo payload. With the revenue from our long range mission, we can then establish mission margins and see which aircraft is suitable for what mission type.

Summary

- The 777-200ER and A340-300 are very close in operating costs in their base versions.

- With the use of payload-range curves for the aircraft we can see that the 777-200ER not only has a higher passenger capacity (six seats, stretched to 30 with the refurbishment), it can also take more payload weight.

- Excess weight capability can be used to load cargo but only if there is space available for the cargo modules when passenger bags has been loaded. We check if this is the case.

- Finally, we check if the higher purchase price and conversion cost for the 777-200ER can be covered by its earnings advantage.

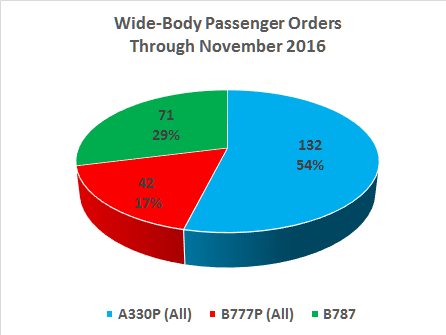

Airbus passes Boeing in wide-body passenger aircraft sales

Dec. 8, 2015, © Leeham Co. Airbus surpassed Boeing in wide-body passenger orders through November, data released yesterday by Airbus shows.

Airbus released its November YTD order book yesterday. Boeing last week updated its weekly order tallies through Dec. 2.

Sources: Airbus and Boeing, YTD November 2015. Click on image to enlarge.

Airbus trailed Boeing in wide-body passenger aircraft orders throughout the year, but now posted 134 orders to 113 for passenger wide-body aircraft. The orders were for 134 A330ceos/neos and for 42 777 Classics and Xs. Cancellations for 19 A350-900s were offset by an equal number of A330-900s as TAP Portugal swapped one model for the other. There were 14 new orders for A350s, leaving a net cancellation of five YTD. This left Airbus with a net of 127 wide-body passenger orders for the year compared with Boeing’s 113.

737 MAX to roll out to Boeing product strategy challenges

Subscription Required

Introduction

The Boeing 737-8 rolls out tomorrow to challenges to Boeing’s product strategy. Image via Google images.

Dec. 7, 2015, © Leeham Co: Boeing rolls out its first 737 MAX tomorrow to no press fanfare. Today there is a limited press tour of the assembly line, but, according to reporters who were invited, there will be no press briefings.

It’s an inexplicably low-key event for what Boeing otherwise touts as a major evolution of the venerable 737 line.

As good as Boeing claims the airplane will be, and as much spin as Boeing’s marketing department tries to put on the rivalry vs the Airbus A320neo, the 737 MAX clearly is second fiddle—and it’s not going to get better.

Summary

- Airbus holds a commanding market share: 60% to 40% of the family comparisons.

- Airbus holds about a 55% share of the A320neo vs 737-8 comparison.

- The A321neo outsells the 737-9 by about 4:1.

- Boeing faces cash flow challenges in 2020 decade.

Pontifications: Assessing the benefit of new airplanes in low oil pricing

By Scott Hamilton

Dec. 7, 2015, © Leeham Co.: Oil for West Texas Intermediate Crude closed Friday at $39.97. International Brent closed at $43.05. These figures continue to breathe life into used aircraft and raise questions about new orders.

In recent weeks, we’ve seen Delta Air Lines extend use of 15 Boeing 757s. Earlier United Airlines decided to refurbish 21 Boeing 767-300ERs. United is also leasing in 38 used Airbus A319s. Southwest Airlines is acquiring more than 20 used Boeing 737-700s through leases.

New aircraft orders are off for Boeing this year. Through Dec. 2, Boeing posted 568 net orders. Unless there is an explosive month in the remaining 24 days of this year, Boeing won’t meet a book-to-bill rate of one.

Airbus hadn’t posted its November orders as of Friday, but through October, the company recorded 850 net orders, comfortably more than a 1:1 book:bill. It announced 108 firm orders in November, with 14 of these representing a swap from A350-900s to A330-900s.

What is the affect of lower oil prices on the new airplanes?

Bjorn’s Corner: Modern IFE

By Bjorn Fehrm

04 December 2015, ©. Leeham Co: During the last two weeks I have been busy explaining how a mid-life long range aircraft is refurbished. The articles have been about how to prepare 10 year old Boeing 777-200ER and Airbus A340-300 for their second half of life.

One of the things that must be done is updating the part of the aircraft that meets the customer, the cabin. Most passengers don’t know much about the aircraft they are flying, but they can tell you if the seats were comfortable, if there was enough leg space and if the movies on the entertainment system were any good.

This means that if the cabin is brought up to a modern standard with lie-flat business seats, refreshed interior surfaces and textiles, and if there is a personal IFE unit with good content, the passenger will not reflect over that he flies an old aircraft.

Such refreshes cost a lot of money. Without changing all items in a 300 seat cabin, one is easily at between $5m-$10m for material and installation. One of the problems when wishing to keep existing seats, for economic reasons, is that it is virtually impossible to implement in-seat IFE to an existing seat. Luckily there are other solutions. Read more

Used B777-200ER or A340-300, Part 2

Subscription required

Introduction

By Bjorn Fehrm

Dec. 3 2015, ©. Leeham Co: Last week we started our article series around acquiring used twin-aisle aircraft to start new long haul services or boost an existing network. We focused on Airbus’ A340-300 and Boeing’s 777-200ER, two capable long haulers, both with a capacity of around 290 seats, using our normalized two class cabin. We wanted to understand which one would have the lowest operating costs over a network which has flights up to 12-13 hours.

We analyzed the Cash Operating Cost (COC) of the aircraft in their standard configuration in Part 1. We could see that their COCs are similar. We now study the aircraft’s capital costs. These will include a necessary cabin makeover where we will use the chance for the 777-200ER to convert it to a 10 abreast aircraft in economy. We aim to amortize its higher acquisition cost by spreading these over more passenger seats.

Summary

- The 777-200ER and A340-300 are very close in Cash Operating Costs in their base versions.

- The 777-200ER has a market valuation which is more than double that of the A340-300. Recently this level has declined but the acquisition cost of a -200ER is still higher than the A340-300.

- We use the potential of 10 abreast in economy to see if we can even the per seat cost of the two by spreading the higher costs of the -200ER over more seats.