Leeham News and Analysis

There's more to real news than a news release.

Singapore Air Show pictorial

Feb. 2123, 2016: The Singapore Air Show ended last week with a dearth of news. William Bain, associate professor and co-editor of International Relations, provided LNC with these photos.

In strategy shift, Boeing backs 7 MAX: sources

![]() Feb. 22, 2016, (c) Leeham Co. In a shift in strategy, Boeing is now fully backing development of the 737-7 MAX instead of urging the only two customers that have ordered the airplane to up-gauge to the MAX 8, sources tell LNC.

Feb. 22, 2016, (c) Leeham Co. In a shift in strategy, Boeing is now fully backing development of the 737-7 MAX instead of urging the only two customers that have ordered the airplane to up-gauge to the MAX 8, sources tell LNC.

Southwest Airlines and WestJet are the only two operating airlines for the 7 MAX. There is a third customer, a start-up in Canada that has yet to begin operations.

Sources have told LNC for months that Boeing really didn’t really want to build the 7 MAX, for which there are only 55 orders. But Southwest needs the airplane for short-runway airports like Chicago Midway and Burbank (CA) and has resisted suggestions to up-gauge, LNC is told.

All this changed when it looked like Bombardier might make a sale of its all-new CS100 to United Airlines, LNC is told.

Transition from McNerney to Muilenburg complete

Dennis Muilenburg, Chairman and CEO of The Boeing Co. Boeing photo.

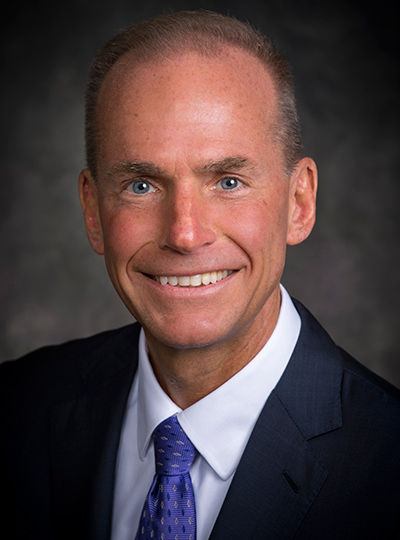

Feb. 22, 2016, (c) Leeham Co.: The transition from the controversial and divisive Jim McNerney to the leadership of Dennis Muilenburg at The Boeing Co. is now complete.

Boeing announced today that McNerney stepped down as chairman and also stepped off the Board of Directors. Muilenburg, who succeeded McNerney as CEO last summer, now also assumes the chairman’s title.

It’s a welcome change.

Welcome news for Bombardier, Mitsubishi

Subscription required

Introduction

![]() Feb. 22, 2016, © Leeham Co.: The large order (Letter of Intent) last week by Air Canada for 45 firm and 30 option CS300s was welcome news for Bombardier.

Feb. 22, 2016, © Leeham Co.: The large order (Letter of Intent) last week by Air Canada for 45 firm and 30 option CS300s was welcome news for Bombardier.

And the LOI from the US lessor, Aerolease, for 10+10 MRJ90s was welcome news for Mitsubishi.

We take a look at both announcements and what this means for the two programs.

Summary

- The Air Canada order breaks the long drought in C Series orders, but it’s not enough for smooth sailing (to mix metaphors) for the aerospace company.

- Continuing the mixed metaphor, Bombardier still has a long hill to climb.

- MRJ order, by little known lessor, helps diversify customer base.

Pontifications: Tax breaks in Washington State

By Scott Hamilton

Feb. 22, 2016, © Leeham Co.: A group of Democratic legislators in Washington State will introduce five bills aimed at repealing some tax breaks and also taking yet another run at holding Boeing’s feet to the fire by tying jobs and tax breaks. The latest effort died in committee this year. This is the second year in a row by Boeing’s two key Washington unions, SPEEA (engineers) and the IAM 751 (touch labor) to get a bill out of committee to tie jobs to tax breaks. Boeing opposes the effort.

Most of the bills relate to non-aerospace industries. Two, however do:

Bjorn’s Corner: Communicate or not?

By Bjorn Fehrm

19 February 2016, ©. Leeham Co: Mitsubishi Aircraft Corporation (MAC) announced on Christmas Day that they delayed the entry into service of the MRJ90 regional airliner by over a year. At the same time, they also announced that they had to reinforce the aircraft’s wing and fuselage.

The market’s reaction to the news was with disappointment. A further delay to a new aircraft from a new player in the market was not good news, but it was not that surprising. Bringing new aircraft to market on time is tough for the established players. Other new entrants, COMAC/AVIC and Irkut, are also running late with their programs, and Sukhoi was late with its SSJ100.

What worried many more was that the aircraft needed reinforcements, directly after its first flights. After only three flights, the aircraft was grounded and was scheduled for changes to its airframe. That was really bad news. “It’s going to be heavier.” How could MAC miss to gravely was the common reaction.

Having worked in a 50% Japanese company for many years, I wondered what was behind this all. Was the aircraft really in dire straits or did we witeness a cultural mismatch I’ve seen many times?

Boeing CEO sees strong fundamentals

Feb. 17, 2016: The fundamentals of the aerospace industry remain strong in commercial and defense, says Dennis Muilenburg, CEO of The Boeing Co. Airlines are becoming more profitable, allowing them to accelerate fleet replacement, he said.

Dennis Muilenburg, Boeing chief executive officer. Source: Boeing.

In his first public appearance since the disappointing 2016 earnings call guidance on Jan. 27 and news of an investigation by the US Securities and Exchange Commission over the practice of program accounting, Muilenburg faced questions at a Barclays investors conference today.

Boeing stock is off about 22% since the beginning of the year and was off about 15% since Jan. 27. Stock has been recovering in recent days. Aerospace analysts say that Boeing has been buying back the stock, propping up the price.

Air Canada orders up to 75 C Series; announced with BBD 2015 financial results

Feb. 17, 2016: The long drought is over.

![]() Air Canada has ordered up to 75 Bombardier C Series.The press conference is at 11am EST today. These will replace 25 Embraer E-190s. BBD now has orders and commitments for 678 C Series.

Air Canada has ordered up to 75 Bombardier C Series.The press conference is at 11am EST today. These will replace 25 Embraer E-190s. BBD now has orders and commitments for 678 C Series.

The announcement comes with the company’s fourth quarter and year-end financial results and a 90-seat version of its Q400 turboprop.

The Air Canada deal is a Letter of Intent for 45 CS300s and options for 30 more, including conversion rights to CS100s. Deliveries are from 2019.

- BBD to cut 7,000 jobs: Bloomberg News. The cut includes 2,000 contractors.

The earnings call webcast summary is below the jump.

Airbus, Boeing cash, stock, dividend strategies similar

Feb. 16, 2016, © Leeham Co.: Boeing has been under pressure since its Jan. 27 earnings call, when its 2016 guidance fell short of analyst expectations. Then the news that the company is under preliminary investigation by the US Securities and Exchange Commission over how its program accounting assumptions were reached.

guidance fell short of analyst expectations. Then the news that the company is under preliminary investigation by the US Securities and Exchange Commission over how its program accounting assumptions were reached.

Free cash flow (FCF), shareholder buybacks and strategy all have come under scrutiny is recent years. But just how different is this compared with its bitter rival, Airbus?

It turns out that other than Boeing’s use of program accounting and Airbus’ use of unit accounting (except for the first several A350 deliveries, for which contract (program) accounting is used), the approaches toward cash flow and shareholder buybacks are very similar.

![]() Credit Suisse’s European analysts who follow Airbus issued a long research note on Feb. 5, just days before the Bloomberg News report on the SEC investigation. The Feb. 5 note doesn’t address program or contract accounting. But as does Credit Suisse’s US analyst who follows Boeing, the Airbus note discusses FCF and stock buybacks at great length.

Credit Suisse’s European analysts who follow Airbus issued a long research note on Feb. 5, just days before the Bloomberg News report on the SEC investigation. The Feb. 5 note doesn’t address program or contract accounting. But as does Credit Suisse’s US analyst who follows Boeing, the Airbus note discusses FCF and stock buybacks at great length.