Leeham News and Analysis

There's more to real news than a news release.

Emirates’ mid-range choice

By Bjorn Fehrm

Nov. 10 2015, ©. Leeham Co: The Dubai Air Show is on its second day and there are no mega orders. The one that should have been, the mid-range requirement for Emirates Airline, has been postponed, not only to “next year” but for “another year.”

What is the reason? Are we seeing a widebody oversupply fueled by used Boeing 777s/Airbus A330s being available in the market “for very low prices,” as suggested by Delta Air Lines CEO Richard Anderson? Are these the first signs of a damping of an order bonanza which has been going on for five years? Will things be more quiet (or should we say normal) going forward?

We don’t think so. Emirates just want to make the right choice and the equation has got more complicated as it has been working the problem. And it is in no hurry.

Pontifications: A380neo? Try A380TXWB. Dubai Air Show and other Odds and Ends

Click on image to enlarge. Airbus photo.

Nov. 9, 2015, (c) Leeham Co. Airbus last week launched its A380 flying test bed with the A350-1000’s Rolls-Royce Trent XWB 97,000 lb engine placed in the number two position.

The first thing that came to mind when I saw the photo was that if Airbus put three more engines on it, you’d have the A380neo. Or maybe call it the A380TXWB. Done and dusted, as they say in England.

Bjorn’s Corner: Aircraft systems, the real nuts to crack

By Bjorn Fehrm

06 November 2015, ©. Leeham Co: COMAC’s C919 was rolled out in the week. We got to see a new shiny aircraft which looked ready to fly. The nicely curved fuselage and wings were immaculate, the paint was shiny and the CFM LEAP-1C engines were ready to go.

Yet many ask, when will it fly for the first time? It used to be that when the airframe was finished and the engines ran reliably it was time to fly. No longer! Today the most challenging part of an aircraft program is the integration of all the complex systems which hide under the skin. This is what kept the Bombardier CSeries on ground longer than it should and the Boeing 787 and Airbus A380 had the same flu (the latter also had to short wires).

It is the part of the aircraft which takes longest to get to work reliably. The A380 is known for its long period of nuisance warnings from the complex avionics system after entry into service and the reliability work for the 787 has to a large extent been one of software tuning of its system side.

As the system function of modern aircraft has grown more complex the whole architecture of how it was built had to be changed. Here’s how.

No fear of C919 for a generation

Nov. 4, 2015, © Leeham Co. The first COMAC C919 was rolled out of the factory over the weekend, China’s mainline entry into the fiercely competitive arena now “owned” by the Airbus-Boeing duopoly.

COMAC C919. Click on image to enlarge. Photo via Google images.

Although the two giants each has said China is the next competitor they will have to face, the Big Two have nothing to worry about for a generation to come.

Here’s why.

“MAD” at Airbus, Boeing?

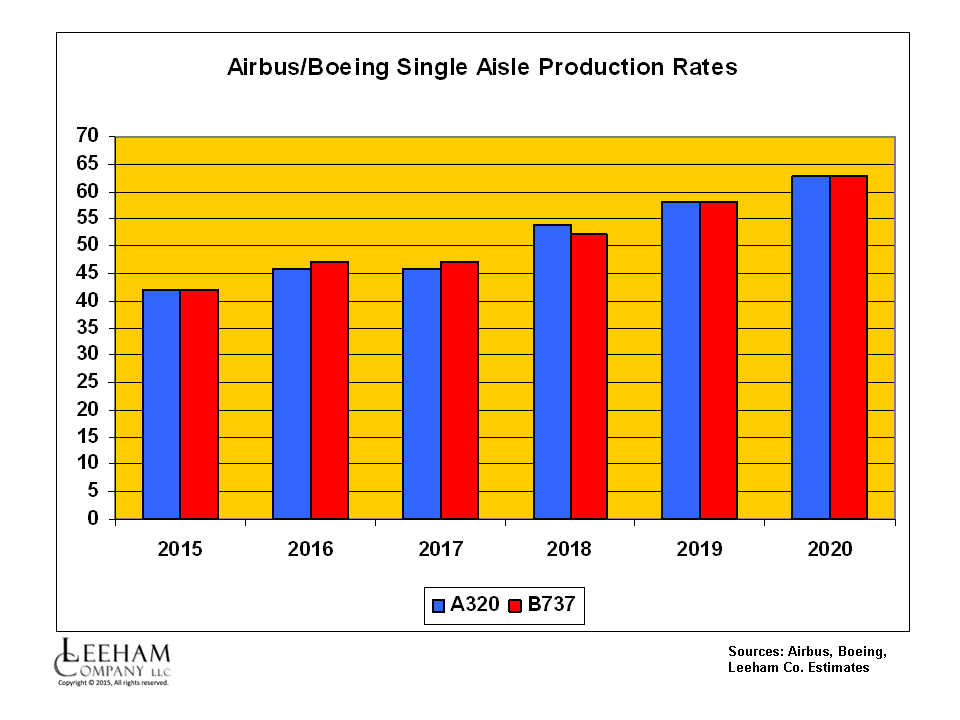

Nov. 3, 2015, © Leeham Co. Aerospace analysts are weighing in on 3Q2015 Friday’s earnings call on the Airbus announcement that it will lift A320 production to 60/mo by mid-2019 and may go to 63/mo the following year.

Figure 1. Click on image to enlarge.

Way back in February we predicted Airbus and Boeing will take their single-aisle production rates to 63/mo. (Figure 1.)

Ken Herbert, the aerospace analyst for Canaccord, noted that even with the same higher rates, Boeing will still out-produce Airbus because Boeing works on a 12-month year and Airbus shuts down the assembly line for a summer vacation. His forecast production chart takes this into account (Figure 2.)

Pointifications: Wide-body orders; Bombardier’s $1bn

By Scott Hamilton

Nov. 2, 2015, © Leeham Co. Boeing gets an order for up to 26 787-10s.

Airbus firms up options to an order for 30 A330s, added to 45 previously announced by the same customer.

Boeing announces an order for nine 787-9s.

For all the talk of a wide-body surplus, this is shaping up to be a good year for wide-body orders.

Through September, Airbus recorded 90 firm wide-body orders, all but three for the A330 family. Boeing recorded 152 during the same period (these are net figures). Not included are any of the orders listed above, which have yet to be recorded as firm contracts.

Based on the YTD-September figures and those above, Airbus has a 42% share of orders this year; Boeing has 58%.

Airbus Group 3Q results; Increase of A320 production to 60 a month

By Bjorn Fehrm

Oct. 30, 2015, ©. Leeham Co: Airbus Group announced its increase of the production rate for the best-selling A320 range to 60 a month in conjunction with its 3Q![]() 2015 results. The rate increase shall be seen against a backdrop of ever-increasing backlog for the A320neo, now at over 4,300 aircraft. The sales bonanza of the A320 is continuing with another 100 aircraft committed at Chancellor Merkel’s visit to China in October.

2015 results. The rate increase shall be seen against a backdrop of ever-increasing backlog for the A320neo, now at over 4,300 aircraft. The sales bonanza of the A320 is continuing with another 100 aircraft committed at Chancellor Merkel’s visit to China in October.

Airbus Group booked solid results for the third quarter, with order intake for Airbus for the year already secured in 3Q at 815 aircraft (791 3Q 2014). Noteworthy are the A330 bookings of 87 aircraft which have also continued in October with another 30 aircraft committed by China.

Revenue was up 6% to €43bn (€40bn 3Q 2014) and core operational EBIT was up 6.5% to €2.8bn compared to €2.59bn 3Q 2014. Free Cash Flow (FCF) was better than 3Q 2014, with €-1.8bn instead of €-2.1bn4. Airbus group expect FCF to be breakeven for the year.

Given the strong results Airbus Group has decided to buy back €1bn of shares before June 2016.

Details from the Airbus programs are:

Bjorn’s Corner: Aircraft programs

By Bjorn Fehrm

30 October 2015, ©. Leeham Co: There has been dramatic news this week around Bombardier’s (BBD) CSeries program. I wrote a subscribers article about what to expect in terms of the cash flow problem that the BBD management has been wrestling with. The announcements yesterday and the following earnings call confirmed the financial modelling I did with our aircraft modelling tool.

Having watched experienced Wall Street analysts being hard pressed to understand what has happened with the CSeries, I thought I could use this week’s corner to explain the overall economical flow of an aircraft program like the CSeries (there will be details in a follow up subscriber article). I will also put it in context with how it affects a company like BBD and what one must think about when it comes to timing of such projects.

To give the timing aspect more colour, I will also compare with Embraer and their E-Jet E2 project and Boeing’s 787 program. The three programs are very different and they demonstrate in an illustrative way the challenges of making a new civil airliner and that one must adapt the project to the company’s position and its strength and weaknesses.

Bjorn’s Corner: Increasing an aircraft’s range, further considerations

By Bjorn Fehrm

23 October 2015, ©. Leeham Co: In last week’s Corner, we went through how Airbus can offer an Ultra Long Haul (ULH) aircraft to Singapore Airlines by increasing the Maximum Take-Off Weight of its A350-900, increasing the tankage and lower the payload. There are a couple of other considerations when extending the range of an aircraft that we did not touch upon. For completeness, we go through them here.

When increasing the allowed weights (really, masses) of a certified airliner, there are a few things that need to be re-evaluated and perhaps modified. First of all, the airframe needs to withstand the higher loads caused by the higher weights. Secondly, the aircraft’s field performance will be affected by higher weights. Required take-off field length must stay within usable limits, as must landing performance.

If the increase in flying weights are significant, it will also require a check on what happens to the aircraft’s flight profile when fully loaded. A heavier aircraft will cruise at lower flight levels and the One Engine Inoperative (OEI) service ceiling will diminish.

We now go through these additional areas and evaluate their impact on overall aircraft performance in general and on an A350-900ULR in particular.