Leeham News and Analysis

There's more to real news than a news release.

With high cargo prices, will airlines fly larger aircraft in their widebody fleets?

Subscription Required

By Bjorn Fehrm

Introduction

October 14, 2021, © Leeham News: Over the last weeks, we’ve seen that the present cargo crunch and high yields will influence what aircraft variants airlines purchase. Models that are too large passenger-wise for years to come will be paid for by a longer belly that can take more cargo.

This trend will remain as long as cargo prices are high. Will the high cargo yields also affect what aircraft to keep stored and which to fly of an existing fleet? We apply the analysis to an airline with a fleet of Boeing 777s.

Summary

- The increased yields for air cargo changes the fleet planning for the widebody fleet. The most suitable passenger models stay in the desert, and the longer siblings fly despite lower load factors.

The Regional Aircraft Fleet

Subscription Required

By Vincent Valery

Introduction

Oct. 11, 2021, © Leeham News: The regional aircraft market, defined as aircraft seating 100 or fewer passengers in standard configurations, has fewer OEM players than before.

Embraer’s E175-E2

The Bombardier CRJ, purchased by Mitsubishi Heavy Industries, ceased production earlier this year. De Havilland Canada will stop Q400 production later this year once it clears its backlog. Both programs might not start production again in the future.

The only latest-generation design, the E175-E2, does not have a single firm order. (There is a conditional order for 100 from the USA’s SkyWest Airlines.) MHI’s SpaceJet development has been “suspended,” but nobody believes it will be restarted.

Therefore, the only regional aircraft in production for the near future will be ATR’s 42 and 72 series, COMAC’s ARJ21, Embraer’s E175-E1, and UAC’s SSJ100.

The ARJ21 and SSJ100 are almost exclusively in service in their respective domestic markets. In practice, that leaves only the ATR42, ATR72, and E175-E1 as new regional aircraft in production for most operators from next year.

However, it is far from guaranteed that ATR and Embraer will enjoy near-monopoly status for the foreseeable future. Embraer has been pondering the launch of a turboprop program for years and is currently looking for an industrial partner.

One also must mention that potential jet fuel alternatives, notably hydrogen-powered aircraft, are likely to come to the regional market first. Therefore, the regional aircraft market could see some significant changes.

With the above in mind, LNA thought it relevant to look at the in-service regional aircraft, both for regional jets and turboprop aircraft.

Summary

- Segmenting the regional aircraft market;

- Regional jet and turboprop prevalence;

- Breakdown by OEM and operator region;

- Age of in-service fleet.

Is the cargo capacity deciding the airliner variant? Part 3.

Subscription Required

By Bjorn Fehrm

Introduction

October 7, 2021, © Leeham News: In last week’s article, we could see today’s high cargo prices can motivate a 325 seat Airbus A350-900 even though the passenger load on the routes would point to a 240 seat A330-800.

How far does this “paying for a larger aircraft with belly cargo” paradigm go? Today we see if Airbus’ largest aircraft, the A350-1000, can generate the margins of the A350-900 on freight-rich routes. Can an airline that has an A350-900 sized passenger demand for such routes go to an A350-1000 instead?

Summary

- The increased yields for air cargo leads to surprising effects. Oversized passenger models can survive the passenger drought on today’s international routes as long as it’s a route with good freight demand.

IATA AGM: Airplanes, engines SAF capable coming; feedstock lags by years

Subscription Required

By Scott Hamilton

Introduction

Oct. 4, 2021, © Leeham News: Engine and airframe makers are well on their way to becoming fully capable of using Sustainable Aviation Fuel (SAF). But the industries providing SAF are way behind in meeting the potential demand.

Rick Deurloo of Pratt & Whitney

Rick Deurloo. Sr. VP & Chief Commercial Officer at Pratt & Whitney said one major US airline would use all currently available SAF in one day.

“The challenge will be the feedstock. How do we grow that technology or grow that ability to provide the feedstock so when we do have 100% SAF-capable aircraft and engines, we have the energy to go with it?” Deurloo said in an interview with LNA at the IATA AGM this week in Boston.

Airlines around the world are partnering with different companies to develop this technology, he said.

PW is already 50% capable and has a “clear path” to getting 100% capable within two years. But there is not enough feedstock in the world today do fill the 50% capability.

Is the cargo capacity deciding the airliner variant? Part 2.

Subscription Required

By Bjorn Fehrm

Introduction

September 30, 2021, © Leeham News: In last week’s article, we put the question: Has the increased cargo pricing started to affect the choice of airliner variant?

We analyzed Boeing’s 787-8 and -9 for margin generation when flying at low post-pandemic load factors. We found the 787-9 is the more attractive alternative as long as air cargo pricing stays high, even though the passenger load factor on the route would motivate a 787-8. The revenue from under the floor cargo compensates for a low load factor in the cabin. Now we subject the Airbus range; A330neo, and A350 to the same analysis.

Summary

- The trend from last week continues. Variants with high cargo capacity can sustain lower load factors while generating the same margin on routes.

- This article develops the passenger load factors where the margin generation is the same between Airbus widebodies.

777 freighter conversion methods and their differences

Subscription Required

By the Leeham News Team

Sept. 27, 2021, © Leeham News: The race for the Boeing 777 P2F Freighter conversion is on.

IAI Bedek Big Twin Boeing 777-300ERF passenger-to-freighter conversion. Lessor GECAS, now part of AerCap, was the launch customer of this, the first 777 P2F program. Source: IAI Bedek.

There are three companies in various stages of development. The first, IAI Bedek, announced its conversion process in 2019 with an order from the giant lessor, GECAS (now a part of AerCap). The second is a program driven by Nair Werx of Wichita (KS) and marketed by Sequoia Aircraft Conversions. The third is the recently announced Mammoth Freighter Conversions of California and Florida.

IAI has cut metal. Mammoth is test-flying a 777-200LR for stress and technical analysis. NAIR is in the pre-production Engineering Phase.

Let’s take a moment to understand the process of a P2F Conversion.

Is cargo capacity deciding the airliner variant?

Subscription Required

By Bjorn Fehrm

Introduction

September 23, 2021, © Leeham News: In last week’s article, we put the question: Has the increased cargo pricing started to affect the choice of airliner variant?

We listed recent decisions between the Boeing 787-8 and -9 or Airbus A330-900 and A350-900 where the traffic levels post-pandemic would motivate the smaller variant, but the larger was retained or selected.

It makes you wonder whether the higher cargo capacity of the larger variant compensates for flying a larger cabin at a lower load factor? We make a cost and revenue analysis to find out.

Summary

- Cargo was an additional revenue stream on top of the main source, the passenger traffic.

- The lower traffic levels for international long-haul traffic and the increase in cargo pricing have changed this. Cargo is now as important in the decision of which aircraft to choose as the passenger capacity.

Behind the latest Boeing CMO

Subscription Required

By Vincent Valery

Introduction

Sept. 20, 2021, © Leeham News: Boeing Commercial Airplanes (BCA) released its latest Commercial Market Outlook (CMO) last week. While the latest total 20-year outlook for commercial aircraft remains below 2019 (43,610 vs. 44,040), it increased by 500 units compared to the previous year.![]()

BCA highlights the headline number of aircraft deliveries to point out the bright long-term growth prospects for the commercial aviation market. The report states that the COVID-19 pandemic erased two years’ worth of growth but did not materially affect long-term prospects.

The delivery figures rely on a large number of assumptions, including market segment and region. LNA takes a deeper look at those assumptions, notably regarding delivery and production rates.

Summary

- Converting to more understandable metrics;

- Assessing the impact of slower 2021 deliveries;

- Plausibility of twin-aisle prospects for the 2020s;

- Can production follow?

Is cargo capacity deciding passenger airliner choice?

Subscription Required

By Vincent Valery

Introduction

Sep. 16, 2021, © Leeham News: LNA has so far compared the performance of both factory and converted freighter aircraft. We will continue the cargo-themed series by analyzing how cargo capacity might decide what passenger aircraft airlines buy.

LNA has extensively discussed Airbus and Boeing’s struggles in accumulating orders for their larger aircraft, the A350-1000, and 777X. However, as seen in a recent article, smaller twin-aisle airplanes face skinny order books as well.

One could think that the COVID-19 pandemic would lead airlines to down-gauge their twin-aisle orders to the smallest available variants, the Airbus A330-800 and Boeing 787-8. Such moves make sense at face value to accommodate a reduced demand in passenger traffic.

So far, only Singapore Airlines has converted two 787-10 orders to the 787-8. Instead of down-gauging, American Airlines converted a portion of its 787-8 order to the larger 787-9. Condor recently announced replacing its aging 767-300ER fleet with A330-900s instead of opting for smaller aircraft.

We now investigate whether airlines’ decision not to down-gauge their twin-aisle order books to the smallest variants has to do with a reduction in cargo capacity.

Summary

- A drought of small twin-aisle orders;

- Airline conundra on choosing best variant;

- Comparing cargo capacity of in-production passenger aircraft;

- Setting the analysis framework.

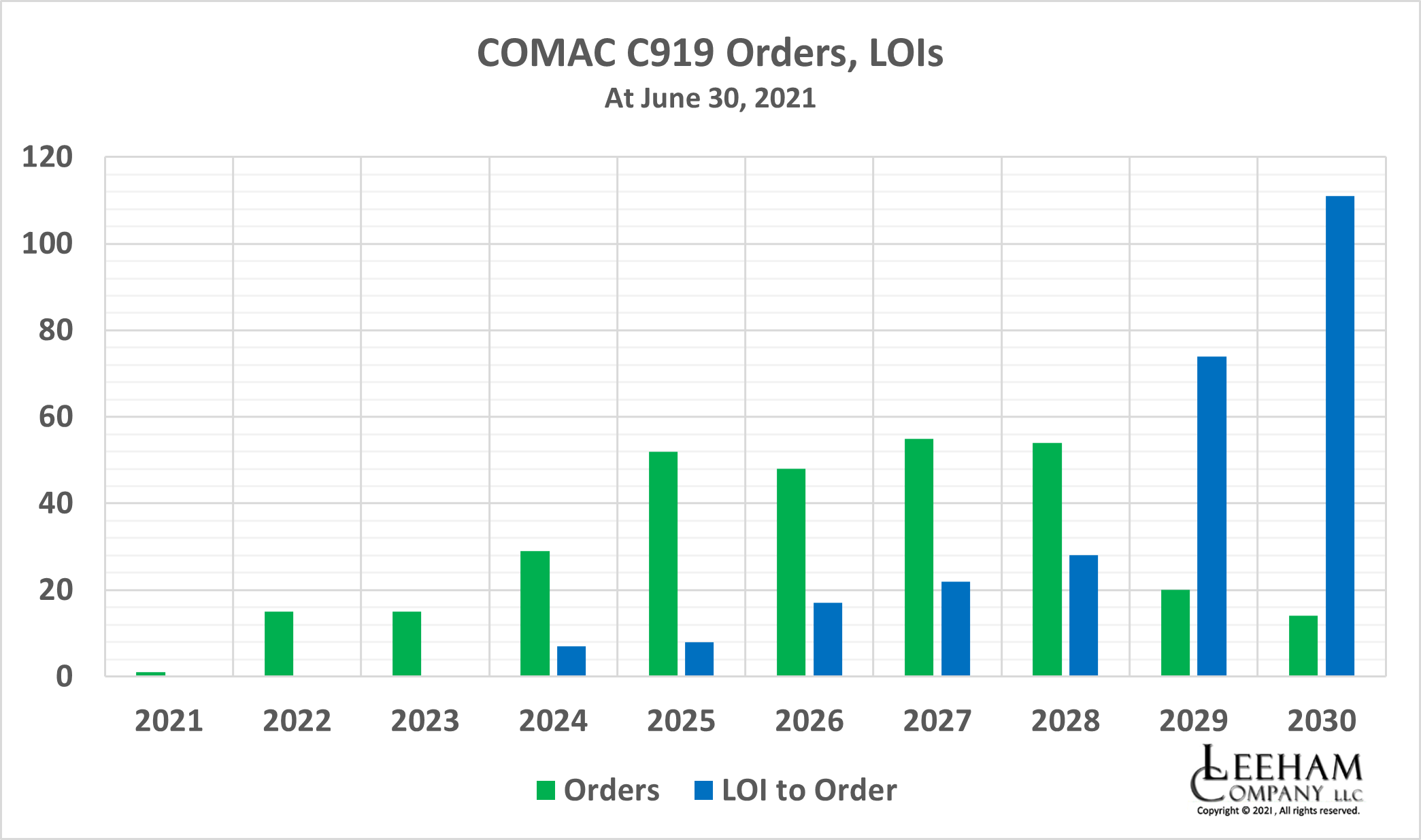

C919 EIS target year end; production rate forecast is aggressive

Subscription Required

By Scott Hamilton

Introduction

Sept. 13, 2021, © Leeham News: The first COMAC C919 is supposed to be delivered to China Eastern Airlines before the end of the year.

If so, it will be the milestone of the program launched in 2008, 13 years ago, becoming one of the longest launch-to-EIS in aviation history. COMAC’s ARJ 21 took one year longer. This regional airliner program was launched in 2002. Entry-into-service was in 2016.

The C919 is China’s direct challenge to the Airbus A320 and the Boeing 737. Similar in appears to the A320, for which there is an assembly line in Tianjin, the C919 is powered by the CFM LEAP 1C and a domestically-produced engine. But the C919 only has an advertised range of 2,200-3,000nm. The A320 and 737-8 have ranges of 3,500 and 3,550nm, respectively.

COMAC forecasts producing 150 C919s a year by the middle of this decade. Achieving this rate in this period should be a major challenge. Based on normal learning curves, a more realistic ramp up to 150 a year will take until early 2031.

Summary

- China forecasts a production rate of 150/yr by the middle of the decade.

- History suggests a much lower rate by then.

- LNA’s production rate forecast is detailed through 2030.