Leeham News and Analysis

There's more to real news than a news release.

Rebuilding confidence at Bombardier

Subscription Required

- This week the Malay government announced an order for 20 CSeries CS100s. for a new airline.

Introduction

March 17, 2015: c. Leeham Co. Turmoil at Bombardier, both financial and with the departure of several key personnel, caused a crisis in confidence among customers and shareholders. The stock price took a tumble and some Canadian aerospace analysts, and the few on Wall Street who also follow the stock, have become increasingly pessimistic. Leeham News and Comment published a long analysis after Ray Jones departed Bombardier Commercial Aircraft in a surprise move, the latest in a series of top-level departures at the unit. Market reaction was decidedly negative.

CEO Pierre Beaudoin stepped up February 12 to executive chairman, relinquishing the chief executive title of Bombardier to Alain Bellemare, a veteran of Pratt & Whitney whose appointment was generally well received.

Still, customers we talked with continue to be cautious. One has a wait-and-see about what Bellemare will be able to achieve, and how soon. This customer believes Bellemare has until the Paris Air Show in June to show some tangible progress.

Another customer was considerably more upbeat, viewing the appointment as a major change in the company for the better.

Canadian analysts were positive about the management changes, in part because the market has lost confidence in the Beaudoin management and in part because Bellemare and his PW experience are viewed as heavy-weight.

Ross Mitchell, vice president of Business Acquisitions and Commercial Aircraft, Bombardier. Source: Fleigerfaust.

We sat down with Ross Mitchell, vice president of Business Acquisitions and Commercial Aircraft for Bombardier, at the ISTAT conference last week in Phoenix for a wide-ranging interview. Here is Part 1.

Summary

- Bombardier needs to restore confidence in the market after all the turmoil. How will this be accomplished?

- Will Alain Bellemare have the flexibility and freedom to do what needs to be done?

- Organizational restructuring has already made some progress.

- The financings are a positive.

Pontifications: USA to the World: “We want to fly everywhere. Period.”

By Scott Hamilton

- Two of the Big 3 Middle Eastern carriers launched a PR counter offensive in Washington DC today. Below are my thoughts.

I haven’t weighed in on the current battle between the Big 3 US airlines and the Big 3 Middle Eastern carriers because it’s largely beyond the scope of LNC. But I like commercial aviation history, so I thought I’d bring up a little.

In the era immediately post-World War II, when third, fourth and fifth freedom rights were being negotiated between the US and the Rest of the World, there was a member of Congress, Claire Luce Booth of Connecticut, summed it up nicely: “American postwar aviation policy is simple. We want to fly everywhere. Period.”

Leahy on 737-8ERX and the prospect of an “A322”

March 16, 2015

737-8ERX: John Leahy, chief operating officer-customers at Airbus, not surprisingly doesn’t think much of the concept Boeing is showing airlines, the 737-8ERX.

“Boeing is getting more and more desperate,” Leahy claimed in a telephone interview we had with him last week. “Boeing is talking the ‘sweet spot.’ They only have one airplane. There isn’t that much of a market at the bottom of the market. I know they are playing around with how do they answer the A321LR. Their answer is focusing on range. There’s no place for bags [in the 737-8ERX], you’re a flying fuel tank. We had to play around quite a bit [to put bags in the A321LR]. If that’s the best they can do, they have a serious problem on their hands.”

This is a pivotal year for the A380 as Airbus considers neo, PIPs

Introduction

March 15, 2015: This is a pivotal year for the future of the Airbus A380.

Tim Clark, the president of Emirates Airline, increased the pressure for development of an A380neo when he said he’d buy up to 200 of the prospective re-engined airplane, potentially doubling the number of neos he previously said he’d buy.

It was widely expected that if Airbus proceeds with a neo, Rolls-Royce will provide the engine. Market Intelligence, however, indicates development of the Advance engine may be running into challenges. Airbus is now talking with Engine Alliance about upgrades to the GP7200.

Summary

- Customers take wait-and-see approach to prospect of a New Engine Option.

- Mixing engine types a consideration for some.

- Some at Boeing quietly rooting for Airbus to proceed.

Pontifications: From the sidelines of the ISTAT conference, Notes #2

March 13, 2015: More Notes from the sidelines at the ISTAT conference this week in Phoenix.

By Scott Hamilton

Boeing 777 production rates and advancing schedule

Randy Tinseth, Boeing VP-Marketing, predictably stuck to Boeing messaging Monday at the ISTAT conference when I asked him about the change in tone I described in my post Monday morning about the 777 Classic production rate to the entry-into-service of the 777X.

Waving a copy of my post in the Q&A session of Tinseth’s market update and saying I had transcripts of every Boeing earnings call and investors presentation in which the “bridge” question was posed since the 777X program was launched, I cited Boeing CFO Greg Smith’s response to orders in the March 5 JP Morgan investors’ day and asked Tinseth about it.

Washington State: tie jobs-for-tax breaks like other states do

By Scott Hamilton, Managing Director of consultancy Leeham Co. and Editor of Leeham News and Comment.

March 12, 2015: Legislators in Washington State are coming down to the wire on a proposed bill promoted by two key Boeing labor unions to tie job levels to tax breaks. Irrespective of party lines, this is a bill that should advance from committees to the full Legislature and win approval. Gov. Jay Inslee should sign this bill if it reaches his desk.

Here’s why.

In 2003, the Washington Legislature, approved $3.2bn in tax breaks provided in a hastily prepared bill in order to win the assembly site for what was then known as the Boeing 7E7. These tax breaks were for 20 years and assured what was renamed the 787 would be assembled here. But there were no jobs-for-tax breaks guarantees. Six years later, in October 2009, Boeing chose North Charleston (SC) to be the assembly site for 787 Line 2. I called former Gov. Gary Locke, who was in office when the 2003 tax breaks were approved, and asked, How could this be? Locke said there was nothing in the tax breaks legislation to prevent Boeing from siting Line 2 outside Washington–nor was there anything to prevent Boeing from moving Line 1 out of Washington, should officials choose–the tax breaks would go away. Read more

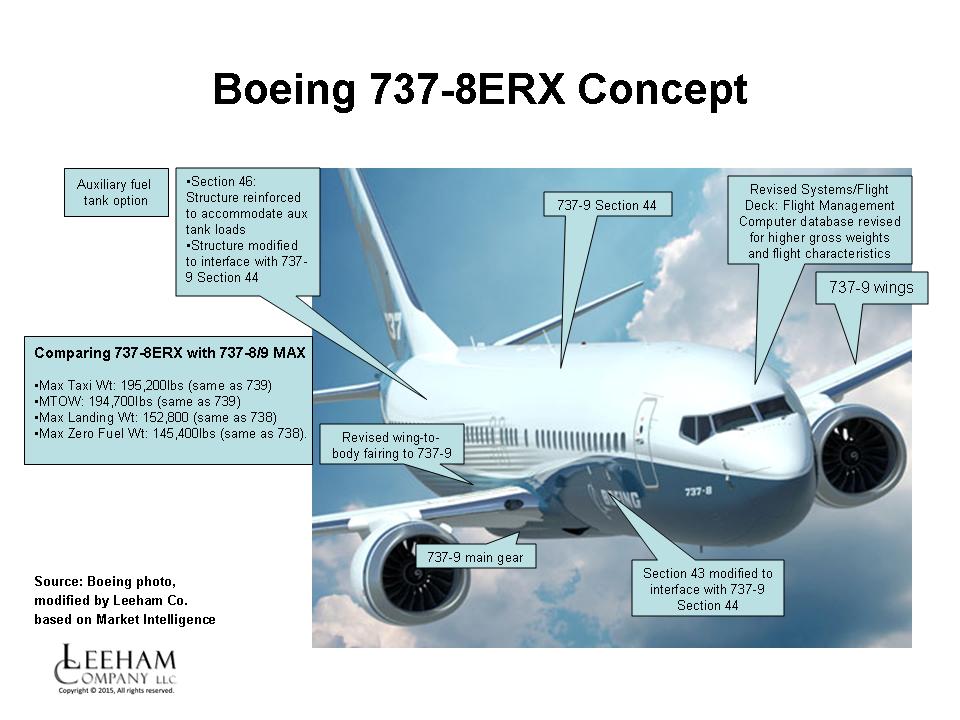

Boeing showing 737-8ERX concept in response to A321LR

By Scott Hamilton and Bjorn Fehrm

March 12, 2015: Boeing is showing some airlines a concept it calls the 737-8ERX, a long range version of the 737-8 MAX, in response to the Airbus A321LR, Leeham News and Comment has learned. Sources within Boeing confirmed the concept but Boeing Corporate Communications did not make someone available for an interview. A spokesman said in an email, “Boeing studies many advanced concepts, innovations and technology. However, just because Boeing studies a particular concept or technology does not necessarily mean that we will be introducing that airplane or concept in the near future. Boeing makes decisions based on market and customer demand.”

Figure 1. The Boeing 737-8ERX concept. Boeing photo, modified by Leeham Co., based on information from Market Intelligence. Click on image to enlarge.

In our article series around A321LR we concluded that Boeings 737 MAX 9 was not a good base from which to launch a long range 737, it could not be stretched in take off weight due to rotation limitations. Better would be to upgrade the take-off weight of MAX 8 for longer range, it can carry the extra fuel tanks needed and is not rotation limited in the same way.

As happened with the A321neoLR (we pointed to the possibility of the concept and Airbus was indeed working on it) Boeing now shows selected airlines a higher gross weight 737 MAX 8, Figure 1. In contrast to Airbus, which beefed up the A321neo to form the A321LR, Boeing is apparently using a concept they developed for the Navy 737 derivative, P8 Poseidon. They grab in their LEGO box of 737 components to form the 737-8ERX with minimal additional development.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 5.

By Bjorn Fehrm

Subscription required

Introduction

11 March 2015, c. Leeham Co: After having analyzed the different alternatives which would be available to Boeing for its Middle Of the Market, MOM, studies and having singled out the most competitive configurations, we will now add revenue to the equation. In the work to establish Cash and Direct Operating Costs for the aircraft, we saw which variant had the best cost for a certain capacity and utilization. We could not see which aircraft would be the most profitable however; this requires that we bring in the revenue side.

Revenue management analysis of different aircraft types on an airlines network is a science in it selves. Sophisticated fare class strategies with connected marketing activities makes such studies elaborate and beyond the scope of our analysis. Our primary goal is to understand the difference in operational efficiency of a single versus dual aisle aircraft with the same seating capacity. For this, a simpler average margin concept will work that shows us the effects of single versus dual aisle for aircraft margins in the MOM segment.

Summary

- We select based on Cash and Direct Operating Costs the best aircraft for the different market segments.

- To understand the revenue earning capability of the different alternatives we introduce a revenue model which takes into account aircraft utilization.

- With the costs and the revenue side represented we can develop a good understanding for the cross over between single and dual aisle for MOM.

- We will use this knowledge as we subsequently look into Airbus response to what Boeing would bring to the market.

ISTAT: Industry stability as good as this CEO has ever seen it

Despite the constant fears of an impending order bubble, the CEO of one of the world’s largest leasing companies says the airline industry’s stability is as good as he’s ever seen it in his career.

Jeff Knittel, president of CIT Transportation, to which CIT Aerospace reports, told a press briefing Tuesday at the ISTAT conference that US network carriers are stronger than they have ever been, low cost carriers (LCCs) are maturing and ultra low cost carriers (ULCCs) are changing the dynamics of business. Read more

Pontifications: Jumping on the MOM bandwagon

By Scott Hamilton

March 15, 2015: There was little “real” news coming out of ISTAT this year, which is probably why the topics of the “757 replacement” and the 200-250 seat, 4,500 mile twin-aisle airplane prospect drew so much attention.

Sitting there in the audience, I could not help but have a feeling of “been there, done that.” Leeham News and Comment has been closely examining these two topics since we exclusively revealed October 21 last year that Airbus was showing the long-range A321 concept to airlines. We dubbed the concept the A321neoLR. Airbus formally launched the program in January and shortened the name to the A321LR.

Between our reveal and the launch, LNC’s economic guru, aerodynamic engineer Bjorn Fehrm, took a very close analysis of the A321LR vs the Boeing 757 and the Boeing 737-9. He analyzed the prospect of a long-range Boeing 737-8. He also looked at the prospect of re-starting the 757 in the form of a re-engined 757 Max.

We concluded: Read more

34 Comments

Posted on March 15, 2015 by Scott Hamilton

Airbus, Boeing, ISTAT, Leeham News and Comment

225/5000 Sector, 737 MAX, 737 MAX 10, 737 replacement, 737-8, 737-8ERX, 737-9, 757, 757 MAX, 757 replacement, 757-200W, 787, 787 Lite, 7X7, 8X8, A321LR, A321neoLR, Air Lease Corp., Airbus, Boeing, Boeing 7X7, Boeing 8X8, ISTAT, Jim McNerney, Middle of Market airplane, MOM, Randy Tinseth, Steve Udvar-Hazy