Leeham News and Analysis

There's more to real news than a news release.

Odds and Ends: Hawaiian orders A330-800, drops A350-800; A330neo market potential; Engines and Airbus

Hawaiian Air’s A350-800s: Hawaiian Airlines July 22 ordered six Airbus A330-800s and simultaneously dropped its order for six A350-800s. HA also took six purchase rights for the A338. Deliveries begin in 2019.

The A338 is slightly smaller, nominally at 252 seats, and has somewhat less range at 7,600nm than the 276-seat, 8,250nm A358, but only Hawaiian knows how much it needed the extra range. Losing the extra seats does give HA a hit to revenue potential, however. For wide-body airplanes, Airbus says each seat has the revenue potential of $2m/yr.

Offsetting the revenue loss is a far lower capital cost for the A338 vs the A358. Our economic analysis, based on technical specifications estimated before the Farnborough Air Show and before Airbus revealed data for the A338, showed the A338 pretty close to the A358 on a pure operating cost basis, not including adjustments for capital cost.

HA also benefits from commonality between the A330neo and the A330-200(ceos) it currently operates. No fleet integration costs, other than for new engines and minor airframe/wing modifications, will be required.

Additionally, based on previous Market Intelligence when A358 orders were swapped (in those cases, for the larger A350-900/1000), we believe it likely Airbus provided some additional incentives for HA to switch.

HA’s cancellation of the A358 means there are now 28 firm orders left for the airplane (as far as we know).

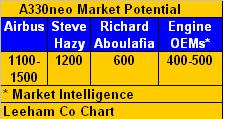

A330neo Market Potential: Just what is the market potential of the A330neo? The data vary widely.

Airbus officials varied publicly from, initially, the “hundreds” (which we more or less narrowed down to about 500 during the Airbus Innovation Days) to 1,100-1,200 and more recently 1,500. Steven Udvar-Hazy, CEO of Air Lease Corp, had a different forecast. Consultant Richard Aboulafia had still another. Finally, based on our Market Intelligence, engine OEMs figured the market to be 400-500.

Airbus officials varied publicly from, initially, the “hundreds” (which we more or less narrowed down to about 500 during the Airbus Innovation Days) to 1,100-1,200 and more recently 1,500. Steven Udvar-Hazy, CEO of Air Lease Corp, had a different forecast. Consultant Richard Aboulafia had still another. Finally, based on our Market Intelligence, engine OEMs figured the market to be 400-500.

Our view is that if there were a market for 1,000-1,500, this could support the business case for GE Engines and Rolls-Royce to be suppliers for the airplane–but not if the market potential were 400-500 (or even 600). According to our Market Intelligence, GE dropped out (Airbus says RR won on commercial terms).

Airbus officials have been quoted as saying the A330neo could be in production to 2030. This seems pretty optimistic–that’s 12+ years from EIS in late 2017. A market of 1,200 airplanes would support production rates of 10/mo (the current rate), and actually stress this rate a bit since Airbus doesn’t work a 12-month year. A demand for 1,500 airplanes would require an annual rate of 125, a slight increase in production rate (highly unlikely, we think).

Airbus officials are already talking about a rate of 7-8/mo for the A330ceo and initially for the neo. 80-92/yr on the truncated Airbus schedule.

Engines and Airbus: Flight Global has an interesting analysis of the migration of exclusive supplier agreements that have evolved with Airbus and Rolls-Royce for wide-body aircraft. Aviation Week has a story that discusses the development of the Trent 7000 for the Airbus A330neo. The AvWeek piece helps explain how Airbus has targeted a much shorter period from program launch to EIS for the A330neo.

It was assumed Hawaiian Airlines did reject offers by Airbus to switch to the bigger A350-900. Therefore I guess the passenger expectations of Hawaiian are not in-between the capacity of A350-800 and -900 but rather around the capacity of the A350-800 or even below.

If the range of 7,600 nm is solid (head winds…) just most parts of Africa are out of reach but the rest of the world is within the range of an A330-800 operating from Honolulu. Sana’a or Dschidda are also out of reach but who cares.

A “revenue potential of $2m/yr” how should this work?

” Therefore I guess the passenger expectations of Hawaiian are not in-between the capacity of A350-800 and -900 but rather around the capacity of the A350-800 or even below. ”

– This could indeed explain HA’s reluctance to upgrade. The A358 may already have been too much capacity for them but since it was the smallest Airbus widebody on offer with the required range, they had to go for it. The 787 may not have come into the picture due to their prior commitments to Airbus aircraft.

Selling and building some 500 copies of the Neo until 2025 sounds like a solid business case.In the meantime Airbus could ramp up production facilities for the A350 and maybe develop a better fit A350-800 or something similar.

A $2 milloin per seat revenue potential seems optimistic, looking at some back of the envelope calculations based on utilisation and long haul yields. And especailly since the additional seats on the A350-800 would be the last ones to be sold, and probably with the lowest yield. That analysis works very well the other way around if the larger aircraft has a small capital cost increase but the marginal revenue you can get for the additional seats offsets that. In this case the capital cost is significant, and the additional revenue marginal. No wonder HA swapped.

To be honest, I’m probably with Aboulafia on this one (gasp!). While I would not rule it out completely, ~1000 seems very optimistic. But: Airbus already has ~120 commitments, so 400-500 over the whole lifespan of the programme seems very conservative. Aboulafia’s 600-odd estimate seems more in the right ballpark than the engine OEM’s and Airbus’ estimates.

Speaking of which – what is Leeham’s estimate?

From the piece above, I would gather that you’re more in line with Aboulafia’s and the engine OEM’s estimates, but there’s no specific indication of what market potential Leeham sees.

We’re in the range of 500-600, mainly because this wound up with one engine supplier and not two.

With the efficiency figures suggesting the 330neo is ballpark with the 787, using a slightly updated version of the same engine, is it possible that the 20-25 year program life talked about last week implies an expectation of a further re-engining next decade in step with or perhaps slightly behind the 1st 787 update/re-engining? And that this might be how the 1k+ figures are coming about?

Why does the lack of engine choice affect your projection? What evidence is their that not having an engine choice hurts sales? It seems to be more and more common for planes to not have a choice when it comes to engines.

I think the argument is that both RR and GE demanded exclusivity, which would indicate that neither engine maker saw enough revenue potential if they had to split the A330neo market 50:50 (or thereabouts).

May make sense – but then, GE demanded exclusivity on the 77W and 777X, and presumably, this wasn’t due to low sales expectations for those variants.

I think 1000-1200 is being ridiculous, as is the potential for production until 2030. That assumes that many operators will forgo the continually improving 787, A350, 777X to buy the increasing older A330. Won’t happen, especially as those aircraft become more available.

Unless Airbus assumes the 787 won’t improve much and they expect/don’t mind sniping more than a few A350 orders.

Leeham is right…400-600 is about the most they can expect to get out of the A330neo.

Well, production to 2030 would only be just over 12 years (EIS slated for December 2017), which really isn’t a problem.

As to selling against the “improving 787” (it’s certainly not competing against the 777X), logic suggests that if Airbus can manage to sell 800-odd A330ceos against the “unimproved 787” that they really should be able to manage a similar number with a significantly better plane.

If Airbus launches an A380-800neo next year using an engine based on the Rolls Royce Advance design having upwards of 20 percent lower TSFC than the Trent-700 engine, then it’s not inconceivable IMJ that the A330neo and the A350-900 could be re-engined further down the road with that engine as well.

This is no major surprise. It was generally considered that the A350-900 was always too much plane for Hawaiian. I suspect most of the remianing -800 orders to be converted to -900s, with Yemania, if they keep their order, switching to A330neos as well.

Longer term, I expect the A330-900 to significantly outsell the -800, especially in Asia. Looking at both OEMs projections for aircraft sales, I could just about see the A330neo reaching the high hundreds. Anything close to 1,000 would be great for Airbus, anything over would be icing on the cake.

Once Airbus has converted the remaining A350-800 customers, expect the plane to be ‘frozen’ a la A380F. I doubt Airbus will have time nor money to revisit it and try and produce a better, more-optimised version. In my view, it was doomed as soon as Airbus decided it would be a simple shrink of the -900 and not optimised.

Airbus is now in a much more competitive position on the widebody front than it was just two weeks ago.

It’s quite likely that we will see other airlines cannibalising their A350 orders with the A330 NEO. AirAsiaX had already mentioned doing this.

FF,

I believe what Air Asia said was that 12-15 of the 50 A330neo order may come form converting exsisting A330ceo orders. Not A350…

True – but there’s also a report by which the CEO Azran Osman-Rani stated that they might drop the A350-900 in favour of the neo “to fit in with its focus on mid-haul routes”.

Erosion on the A350-900 orders would directly provide for available slots on the A350-1000 side. Moving the A350 earlier, faster and further into 777-300ER land?

I would tend to agree with Udvar-Hazy. 1200 units should be doable if the A330 corners the Chinese market for domestic and intra-Asian passenger travel.

A big order by China could include a Chinese FAL for A330CEO.

….or at least an A330 completion center.

http://aviationweek.com/awin/airbus-offers-build-a330-center-china

Their estimates are for A330neo. 1200 units seems far too optimistic… Don’t forget that Airbus is developing a regional A333 for that Chinese and intra-Asian markets, but… ceo version.

As I indicated in my response to TransWorld below, the A330neo will IMJ be very suitable for intra-Asian markets. Due to lower capital costs than the A330neo the 199 tonne A330ceo regional version should still be a very attractive option for the next half decade on very short routes in the Chinese domestic market.

If Airbus manages to continue delivering 25-30 A330s to mainland China every year from 2015 to 2030, then I’d expect to see at least another 100 A330ceo and 250 A330neo deliveries; or about 20 percent of Udvar-Hazy’s projected market demand for the A330neo.

It’s really all about delivery positions and immediate demand. Any Chinese airline in need of an A330 before, say, 2019 would in all likelihood opt for a significant number of “regional” A330ceos. From 2020 an onwards they would just choose to order A330neos in droves, and I would not be surprised if Airbus at that time would also offer a regional version of the A330neo to Chinese customers. 😉

The A330NEO can’t compete with the A330CEO on shorter routes.

Not true.

The increase in operating empty weight (OEW) will at most increase by 4 percent. For the sake of argument let’s assume that in a worst case scenario an increase in OEW by 4 percent results in an increase in fuel consumption 3 percent.

Source: http://web.mit.edu/aeroastro/sites/waitz/publications/Babikian.pdf

–

So, with an improvement in 10-11 percent in TSFC of the new engine; why would an increase in fuel consumption by some 3 percent caused by the heavier engine, nacelle, wing reinforcements and new wing tip devices make the A330neo uncompetitive with the A330ceo on “shorter routes”?

And this is the beginning of the end of A358…

With far lower capital costs and not too much expensive OC than A358, I’m pretty sure that Aeroflot, Asiana and Yemenia (all of them operating A330ceo) are right now considering A330neo.

Not the beginning of the end. It’s at least the middle of the end already!

The business case of the A330 NEO for Airbus is based on the number of planes they sell beyond the number of CEOs they would have sold anyway.

The business case for Rolls Royce is based on the total number of 7000 engines. That’s because Airbus would have chosen another supplier if they hadn’t signed on.

The business case for the A330neo would also include the likelihood of maintaining the value of the frame while getting a higher price for the product than what would have been the case with the a330ceo. Also, the latter would very likely have been produced at ever decreasing rates affecting negatively on the efficiencies of scale that are achieved at a high production rate. Hence, the business case for the A330neo seems to exceptionally good.

I thought part of the business case for the A330neo was cheap acquisition cost.

Yup. But the acquisition cost is still higher than what an A330ceo sells for.

Also, a 2020 vintage A330neo is certainly going to sell for more than a 2020 vintage A330ceo (just before winding down the line, assuming no NEO had been launched) would.

…at higher profit margins as well, I might add.

I think Airbus selling 800 dated A330’s after the 787 Dreamliner launch and starting delivering simplified A350 mk1’s 13 years later is a highly unlikely scenario. Still..

I believe the A330 will sell another 1000 frames quite comfortably; it already has just short of 400 orders and commitments. It is a low-end, economical, small widebody. With its high dispatch reliability, versatility, and ease of maintenance and operations, it has all the traits of a mass-market product akin to the 737 or A320. Most likely, it will be the first widebody to sell 2000 frames, and I believe it will be the first to sell 3000 frames. Truly an icon of the aviation industry, it originally had a 3,900nm range at 212-ton MTOW, but has evolved continuously and in its latest iteration has 6200nm to 7450nm range at 242-ton MTOW and at significantly reduced fuel burn and capital cost. With deregulation and open skies treaties, every carrier should operate a small fleet of A330s to capitalize on existing demand for medium to long haul air travel.

777 is ahead at 1600+, but the A330 could catch up.

In terms of actual deliveries, the 777 is ahead by 1204 to 1099 at the moment. A330’s production rate is only about one more frame per month so it will take some time to catch up, even if the A330 order book fills up quickly.

2003:

” Airbus Chief Commercial Officer John Leahy said the A330-200 would beat the 7E7 and win at least half the 1,800 jet orders expected for mid-sized jets over the next 20 years, expressing surprise that Boeing would spend so much money just to match the A330.”

http://edition.cnn.com/2003/BUSINESS/12/16/boeing.newjet.reut/index.html

Everybody had a good laugh about big mouth Leahy and how sour and uninformed he was. Including Udvar and most analysts.

I think most will now formally apologize for making fun of him, now that he proved to be right on the ball, against the entire mainstream media burrying the A330 and declaring victory for Boeing and the 787. Not, hell will freeze..

well, if Boeing hadn’t totally screwed the pooch on the 787 development and manufacturing strategy, we would be in a different place right now with ~500 787’s in service and lots of open slots in the 2017-2020 time frame and Boeing would be able to compete head to head on price.

But Boeing’s (really McD’s) senior management, under the spell of MBA school culture decided to outsource everything, oversee nothing and start not one, not 2, but 3 pissing matches with their workers at critical times resulted in the current situation.

the success of the A330 and existence of A330NEO has as much to do with Boeing management’s strategic stupidity as it does the qualities of the A330.

Spot ON! (and then some)

Boeing didn’t ( and could not ) lay hands on the pooch.

The Dreamliner as envisioned and announced was unachievable, a PR project.

( and probably the reason why Airbus dropped the A350Mk1 against having the A330 Classic soldier on.)

Cargo Cult on Steroids so to speak 😉

What did Leahy tag the Dreamliner early on? cheap chinese copy ?

The writing is on the wall. The A330 neo will do very well, at least well enough to keep the skeptics quiet.

More A330 neo’s were sold at Farnborough than the 787, A350, and 777. The 777-x from Qatar was on old “order” from Dubai. Nothing new for the 777-x.

Conclusion: The A330 Neo outsold the 787, A350, and 777 (including x’s) at Farnborough.

Even if it sold 500, and not 1000, that is still a pretty nice number. This aircraft will unmistakably be a proven, reliable, efficient, enviable/comfortable 2-4-2 medium and long hauler gem.

Who cares about a single airshow? Boeing is way ahead in orders AND deliveries in 2014. [Edited as a violation of Reader Comment rules.]

Joe:

That is just plain silly (shade of tricked down economics thinking)

The 787-10 outsold the A330NEO recently as well. As the others have been launched at other airshows the bump took place then. The A330 had pent up demand (but I sure would not put any money on Air Asia as shaky an operation as it is). Hazy yes.

A good case can be made that the 787-10 sales (commitments) are slow (too far out to get too excited about probably)

777X continues to firm up orders and more options taken by Qatar than anticipated

You have to wonder if Boeing is oblivious or just in denial. If they can beat the A330 with a 787-10 and shorter range then the A330NEO could do the same to 787-8/9 (and if its all true and does). So does Boeing have a response? And if they do, when do they pull the trigger?

How many A330NEO sale3s will cannibalize A350 salves?

Contrary to a lot of reporter hand wringing, Airbus deliberately killed the A350-800 a long time ago and they offered customers great deals to move up to the -900 (and you can bet Hawaiian got a really sweet deal on the far less planned production of the A330-800 (Leahy specifiably said the 800 would be very low numbers)

Now if they did not need an A350-900, an A330-900 might just be the cats meow.

And you have to count cannibalized A330CEO sales to the A330NEO.

Lot of plate movement and head scratching as to when it releases into a quake.

There hasn’t been a 787-10 sale since the program launch; there are 132 orders.

Did not have the numbers at hand. It looked to me like there was a specific market and current size and its got that. Slower sales long term as needs come up (and availability is out there) .

Lufthansa said it missed 40% or its routes so there is a miss which applies to all of them of course.

Still need to see if the A330NEO keeps going or the same thing.

Delta should be interesting due to the slots it has for 787, A330 operator and apparently as happy as Hawaiian Air with it and the Imp-Ex Bank battle.

Scott are there any reasons for this, apart from availability?

Market talk complains that Boeing has priced the 787-10 too high for what it gives you.

Richard Anderson was one who was really vocal about it – “Prices must come down”.

I believe this is the factor that some people commenting here seemed to overlook or not take seriously. Airbus claimed they could make a good case for the A330 NEO through low initial costs and many said Boeing could do the same for the 787.

Sadly that is not the case. If what Jon Ostrower wrote a few years ago is true, a great majority of the early 787 sales were at very low prices. If so, then these low priced early sales in combination with the extra developement costs would prevent Boeing from offering a lower price on the 787 fleet until they are, or are close to, making a “real” profit on the program.

I say real profit due to the bookkeeping practice that allows them to claim profit on an aircraft sale way before all of the program costs have been recovered. I understand the concept but it still does not mean that the program is in the black just because they can book profit on every plane they deliver from day one.

Having said that, I still believe Boeing is far from a bad position here. It is, unfortunately for them, not the case of overwhelming domination in the widebody class that they had become accustomed to.

Boeing list prices at the time gave you an indication of that – they priced the 787 lower than the 767! (Except the 767-200ER, that is.)

As of 13 August 2005 (first time the 787 was featured in the list prices overview):

https://web.archive.org/web/20050930214914/http://www.boeing.com/commercial/prices/

That’s right – the 787-8 was listed as 2.3-4.6% cheaper than the 767-300ER.

Even if this isn’t the the full story of what prices you’d eventually find in an order contract, it tells you a lot about how aggressively Boeing were selling the 787 at the time.

It wasn’t until late December 2005 that they corrected this to a point.

As of 24 December 2005:

https://web.archive.org/web/20050813185155/http://www.boeing.com/commercial/prices/

Even then, there was only a 6.3-10.9% markup between the 767-300ER and the 787-8.

Today, Boeing no longer gives a price range, but a single price datum. Based on that, you’re looking at ~14% difference between the 767-300ER and the 787-8:

As of 24 July 2014:

http://www.boeing.com/boeing/commercial/prices/

No. It launched with 102 and Cathay I believe ordered 30 later. If it was not cathay..it was another asian carrier. It is over 130 now.

Actually it was Etihad with 30 in November 2013, not part of original launch. Also, United bought additional 787-10s in august 2014. Total: 139

A sale is a sale, whether it oscillates between A330 or A350, and is probably at least as profitable for Airbus if it goes from A350 to A330.

You loose sales on the A350 program to the A330 and you undercut the cost of producing the aircraft. It only works if you take sales from Boeing. So you have one nicely producing program and the other a big loss. Net profits zero (or a loss)

Fewer aircraft produced means cost spread across few frames and ROI moves to the right (Boeing is into the 800-1000 range on the 787, that awfully far to the right). A350 is no different, it needs to sell (have not seen figures) but would guess 500-700 to start returning revenue.

The longer you delay that the worse the ROI gets, Its an ugly spiral

You make money on one hand and loose lots more on the other.

Loosing A350 orders for -800 and maybe even -900 will potentially take pressure from ramping up production _and_ immediately free slots for selling more profitable A350-1000 with a higher market impact on the B lifeline range of products.

Correct.

About making profit …

I guess Airbus makes more profit with one A330CEO or NEO than could have made with one A350-800. I also expect the NEO to be a cheaper development than the -800.

Delayed ROI due to converted A350s to NEOs? I can’t see the problem. Airbus sells more than one type of aircraft. A problem would be a delayed production without any compensation but Airbus will make far more profit for each NEO sold. So the NEOs pay the investment for the A350s.

You should also mind the price gaps:

-800 to -900: 13 % higher price

-800 to – 1000: 35 % higher price

It would be bad to have no aircraft you can sell instead an A350-800 or even delayed EIS and a delayed production ramp up. E.g. Boeing did expected to deliver 10 B787-8 a month by end of 2012. In 2013 Boeing delivered 65 B787-8. It looks like more than one airline is waiting for several 787s.

ROI for NEO: According to list price the NEO costs about $20 million more. Even with a huge discount of 50 % each aircraft will return $10 million more. So with about 200 NEOs delivered the development costs would have been paid off.

I can’t comprehend why this fixation that the A330 is old and vintage. This aircraft was continuously updated and the aircrafts produced today are up to date with current technology. The 777-x will also be an updated aircraft as is the 737 Max which by the way has an airframe older that the A300.

Other than composite wing and airframe, I do not understand what “advanced technology” the 787 has that would make the A3330 Neo low end or vintage.

What exactly does the 787 offer or posess that would make one conclude that it is better to have, more reliable, or safer than the A330? Is is just the ” new thing”?

Let’s ask all those airlines that bought hundreds and hundreds of A330s even though the 787 was available…

No, they bought hundred and hundreds of A330s because the 787 WAS NOT available (and they have 800 or 9000 commitment ahead of anyone that wants one.)

The program was hosed up, delayed by 3 years (and various other add ins like the wing join issue

An A330 in the air is worth more than 3 787s 8 years down the line.

Better yet, ask the people who claim the A330 is 80’s technology just how much of a difference in time there is between the developement of the A330/340 and the 777.

Some people in glass houses really seem to love chucking stones around.

Leahy for one. If the 737 is 60s tech, then the A330 is early 70s tech.

Not true for any of them now as they have been massively changed over the years.

Selective stone throwing me thinks.

Well, it wasn’t Leahy who started calling the 737 60s tech, it was Boeing calling the A330 80s tech. Nonsense either way.

This might help explain the appeal of the A330neo.

http://www.reuters.com/article/2014/07/23/deltaairlines-brief-idUSWEN00DNP20140723

“cost-containment efforts * Carrier says it will continue to be ‘very objective’ evaluator of airplanes, says

Delta might be buyer of Airbus A330neo if it is priced in the ‘low

80s, high 70s'”

That is 28-30% of list price for the A330-900. NB like pricing!

Well, if he’s buying 50 of them…

…and SUH’s comments about the unbeatable price…we can see why.

Of course, you’ve assumed that the price Delta wants is what they get. It won’t be.

Not saying they’ll get the exact same price. But a neo under a 100 mill has to be hard to beat, no?

Not surprising. A lot of the appeal from the A330neo will come from being competitive on price, despite Airbus listing a higher price on the NEO. If Airbus can’t compete on price, they might as well not have bothered with the programme.

Delta might be buyer of Airbus A330neo if it is priced in the ‘low 80s, high 70s’”

That’s without engines.

At $80 million per frame – excluding engines — Airbus would still make a nice profit.

Low pricing, Boeing failures.. Superior technology, reliability, comfort and efficiency are reserved for other products.

Thanks for the laugh, Keesje!

A lot of figures are thrown around and quite a few people make the mistake in comparing the list price for the A330neo with a discounted price that doesn’t include the acquisition costs for the engines.