Leeham News and Analysis

There's more to real news than a news release.

Boeing considers single, twin aisle, co-development 757/767 style for next new airplane

Subscription required.

Now open to all Readers.

Introduction

Boeing is looking at a number of scenarios for its New Airplane Study (NAS) that would replace the 757 and 737, have ranges from 4,000nm-5,000nm, and carry as few passengers as 130 or as many as 240.

![]() To cover this broad range of demands could require reverting back to the 1980s when Boeing simultaneously developed two airplanes serving very different missions, the 757 and 767, that shared cockpits and some other common elements.

To cover this broad range of demands could require reverting back to the 1980s when Boeing simultaneously developed two airplanes serving very different missions, the 757 and 767, that shared cockpits and some other common elements.

Boeing faces some hard decisions in the coming years, as Airbus outflanks Boeing in the single-aisle sector with the A320neo family and its latest offering, the A321neoLR. Our analysis and sales figures show the 737 MAX falling further and further behind in market share as MAX 9 lags vis-à-vis the A321neo.

We spoke with Kourosh Hadi, director of product development at Boeing, during a break at a conference last week organized by the British American Business Council-Pacific Northwest, and covered this and a number of other topics.

Summary

- Boeing is studying a New Light Twin (NLT) and New Single Aisle (NSA) to replace the 757 and 737 airplanes.

- The tipping point between an efficient NSA and the NLT is around the passenger size of the 757-200.

- Boeing is evaluating materials, including metals and composites, for the NAS and the manufacturing process, which will also be a determining factor in the materials for the new airplane.

- Engine advances for the 777X’s GE9X are beyond the GEnx and CFM LEAP of today and could help drive the next new small engine technology.

- Although having a miniscule portion of the 100-150 seat market, Boeing today plans to continue participation in at least the 130 or 150 seat sector even as airplane size moves up every year.

CASM Paradigm: Lower Seat Mile Cost or Higher Yield; Evaluating the GOL competition

Subscription Required

Introduction

As Brazil’s budget airline GOL reportedly evaluates whether to acquire 20 Boeing 737-7s or Embraer E-195 E2s, the principal of the “CASM Paradigm” is a concept worth examining.

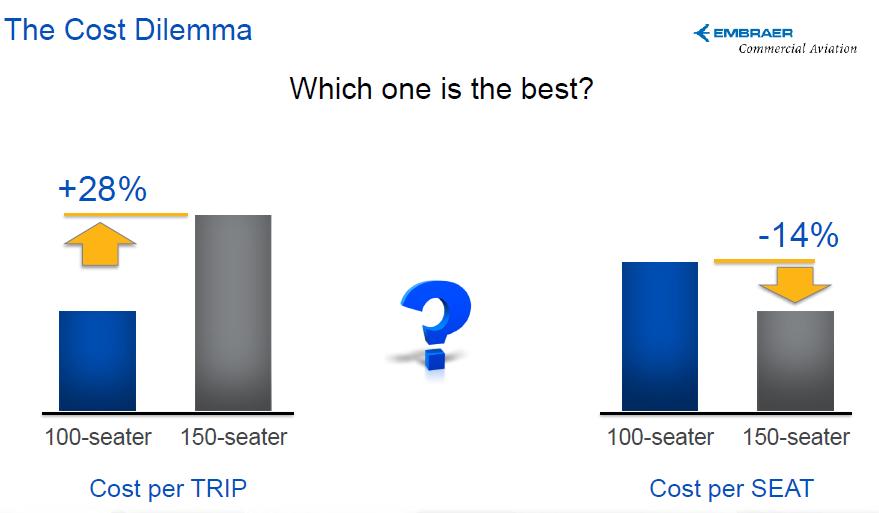

![]() This head-to-head evaluation of the E-195 E2 and the 737-7 MAX is a rarity. Typically the head-to-head involves the Bombardier CS300 and the Airbus A319neo. All three have the same seating capacities. The E-195 E2 has slightly fewer passengers than the 737-7 with similar seat pitch.

This head-to-head evaluation of the E-195 E2 and the 737-7 MAX is a rarity. Typically the head-to-head involves the Bombardier CS300 and the Airbus A319neo. All three have the same seating capacities. The E-195 E2 has slightly fewer passengers than the 737-7 with similar seat pitch.

The competition is also what might be seen as a contrary competition. Airframers agree: the airline industry is upgauging. Capacity discipline, long elusive until after the global financial collapse of 2008, has been driving load factors higher. But lowering unit costs, or the Cost per Available Seat Miles (CASM) has long been the principal measure by which airlines, OEMs and aerospace analysts measure efficiency.

Although Trip Costs of aircraft operating over a route is important, the trend toward upgauging at all levels clearly is the driving force.

Figure 1. It’s an age-old debate: the cost per available seat mile (CASM) vs trip cost. CASM typically wins, and the airline industry is migrating toward larger aircraft. Embraer, not surprisingly, thinks this has gone too far. Graphic: Embraer, reprinted with permission. Click on image to enlarge.

Embraer takes a different view, arguing that trip costs and a smaller airplane should trump the CASM obsession. A smaller airplane will mean higher yields, EMB says. A larger airplane provides lower trip costs but drives yield lower.

We visited Embraer’s headquarters earlier this month and received a full briefing on what EMB calls the CASM Paradigm. In our report today, we detail the presentation and discuss other considerations beside CASM vs Trip Costs that drive the size of the aircraft acquired.

Summary

- The CASM Paradigm becomes a vicious, circular cycle, driving airlines to larger aircraft but lower yields.

- Extra seats on larger aircraft mean lower unit costs but at the cost of profits.

- Scope Clauses remain an issue in the US.

- Connecting traffic, pay scales also are issues.

- We analyze the operating costs of the E-195 E2 vs the 737-7.

- We discuss the GOL competition.

Part 2: Boeing 757: Airbus A321neoLR as a replacement on long and thin routes

Subscription required.

By Bjorn Fehrm

Part 2 of 3

Introduction

In Part 2 of our three-part 757 Replacement analysis, we take a close look at Airbus’ new 97 tonnes take off weight A321neo, revealed by Leeham News and Comment October 21. We call the 97t airplane the A321neoLR (Long Range); Airbus has yet to name the aircraft, which it began showing to airlines last week.

![]() We analyze the A321neoLR’s capabilities and limitations when compared to the aircraft it intends to replace, the Boeing 757-200W. We have chosen to do so using a real airline configuration as opposed to an OEM’s typical seating layout. By comparing the 757-200W and the A321neoLR over the route structure that United Airlines is using the 757 today, we can better see the characteristics of the A321neoLR and what operational consequences the differences between the types would mean for the airlines. Before we start, a short recap of Part 1 about the 757 and its replacement candidates. Here is what we found:

We analyze the A321neoLR’s capabilities and limitations when compared to the aircraft it intends to replace, the Boeing 757-200W. We have chosen to do so using a real airline configuration as opposed to an OEM’s typical seating layout. By comparing the 757-200W and the A321neoLR over the route structure that United Airlines is using the 757 today, we can better see the characteristics of the A321neoLR and what operational consequences the differences between the types would mean for the airlines. Before we start, a short recap of Part 1 about the 757 and its replacement candidates. Here is what we found:

- the seating capacity of the A321 is within 10 seats of the 757-200 in a standard configuration; the 737 MAX9 is trailing with about 20 fewer seats.

- the myth about the strong engines of the 757 is just that, a myth.

- the good field performance of the 757 is coming from its wing more than any advantage on the engine side

- the A321neo and 737 MAX9 were hindered in their capability to replace the 757 for long and thin international routes by characteristics that can be changed. For the A321neo, this may be accomplished with rather modest changes to Max Take Off Weight (MTOW) and tankage. For the 737 MAX9, more elaborate changes to the wing and engines are required, both hard to do.

Figure 1. Boeing 757-200 of British Airways which launched the 757 together with Eastern Airlines 1983. Source: Wikimedia.

Summary, Part 2

- We will now look in detail on the changes Airbus is doing on the A321neoLR, what each change brings and any restrictions that remain.

- We will also detail why we think it will be harder for Boeing to match the A321neoLR with a 737 MAX9 development.

- We detail prime, present 757W long-thin routes.

- We present 757W international, A321neoLR and 737 MAX9 “long range” configurations.

- We provide economic comparisons such as Payload-Range charts and Fuel consumption per trip and per seat diagrams.

In the final Part 3, will look at Boeing’s alternative to an A321neoLR, a clean sheet New Single Aisle (NSA) and a prospective Small Twin Aisle (STA) design and how much such an approach would surpass the A321neoLR on medium and long haul networks and when it could be available.

Part 1–Boeing 757: An analysis of facts and myths

Subscription required.

By Bjorn Fehrm

Part 1 of 3

Introduction

The Boeing 757 was developed in the late 1970s as a replacement for Boeing’s popular 727 mid-range single aisle aircraft. Starting from the smaller 727, it ultimately grew to 180 to 230 seat capacity and US transcontinental range. With initial orders from Eastern Airlines and British Airways, the aircraft nonetheless had poor sales through most of the 1980s, picking up with a surge of orders in 1988-1990 when major deals were announced from American, Delta and United airlines.

Figure 1. Boeing 757-200 of launch customer Eastern Airlines.

Following the 1991 Persian Gulf War and recession, orders plunged until the mid-decade with a respectable resurgence. After 9/11, sales dried up and Boeing terminated the program.

Summary

- The 757 program had slow sales in its first decade, robust sales for a few years then declining sales through most of the 1990s.

- Sales were respectable in the late 1990s but dried up after 9/11.

- Boeing efforts to boost sales with the 757-300 were a failure–only 55 were sold. 757F sales were a moderate success.

- The 757-200 had strong engines for its time (especially the Rolls Royce equipped models), we dissect if this is still true.

- With the 757 being the only narrow-body with trans-Atlantic range, what is missing from today’s Airbus A321 and Boeing 737 MAX9 to make the cut? What can be done with small changes will be answered in part 2.

- How will a future clean sheet NSA perform compared to these three? How much of a game-changer will a clean sheet design be if it enters service 2025? We look at the answers in part 3.

Odds and Ends: Comparing Airbus, Boeing 20-year forecasts; A320neo first flight; 787 battery probe fizzles; Mythbusting

Airbus v Boeing forecasts: The Blog by Javier takes its annual look at and comparison of the Airbus and Boeing 20-year forecasts. Airbus issued its new forecast this week; Boeing’s annual update was issued last summer.

Separately, the A320neo with Pratt & Whitney engines made its first flight today. The CFM LEAP neo is supposed to follow by six months. Showing class, Boeing Tweeted a congratulations for a milestone for the industry.

787 battery probe: The US National Transportation Safety Board hasn’t been able to find the root cause of the lithium ion battery failure in the Japan Air Lines and ANA Boeing 787 incidents. Now, the Japanese investigation has also failed to find the root cause of the ANA battery meltdown.

It’s rare but not unknown for investigators to not find root causes of problems, sometimes for years. A Northwest Airlines Boeing 747-400 split rudder hard over during a flight from Anchorage to Tokyo is one example; it took four years to determine the cause. The root cause of Boeing 737 rudder hard-overs, two of which caused fatal accidents, went unsolved for years.

Boarding airplanes: The reality show Mythbusters, an often entertaining look at myths, conventional wisdom, fact and fiction, takes a deep dive into airplane boarding. The article, with an insert to the episode, is here.

The Southwest Airlines style of boarding, with no seat assignments and derisively called cattle-call boarding, is the fastest and the most annoying, according to Mythbusters. Back-to-front is the longest. The Window-Middle-Aisle works best (but for those of us who like the aisle seat, the overhead bins are usually stuffed by then).

ISTAT Europe Conference in Istanbul: Boeing and Airbus slugging it out with some new twists

Airbus and Boeing squared off once again Monday, this time at the ISTAT Europe conference in Istanbul, once again pretty much over the entire product lines.

Boeing’s VP Marketing Randy Tinseth began with two focal points, the 737 with its latest developments and Boeing’s “superior” Twin Aisle line-up. Tinseth claimed Boeing has caught up to the A320neo with the 737 MAX.

After an A320neo head start of a year, Tinseth says Boeing has kept the same sales rate per year for the 737 MAX. The backlog of 737 MAX now stands at 2,300 aircraft and he described why Boeing thinks it is well positioned in this market segment.

Part 3: Boeing 757 replacement: 757 and Airbus A321neoLR versus clean sheet designs.

Subscription required.

By Bjorn Fehrm

Part 3 of 3

Introduction

In Part 2 of our three-part 757 Replacement analysis, we took a close look at Airbus’ new 97 tonne take-off weight A321neo, revealed in a world exclusive by Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

Summary

For Part 3 we can summarize:

Figure 1. Fuselage cross sections of our models of NSA and NLT. Source: Leeham Co.

Read more

5 Comments

Posted on October 28, 2014 by Bjorn Fehrm

Airbus, Airlines, Boeing, CFM, China, Comac, CSeries, Embraer, GE Aviation, Irkut, Leeham Co., Leeham News and Comment, Pratt & Whitney, Premium, Rolls-Royce, Uncategorized

737, 737 MAX, A320, A320NEO, Airbus, Boeing, Bombardier, CFM, Comac, CSeries, Embraer, GTF, Pratt & Whitney, Rolls-Royce