Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

- Engine makers tout “Plan A” but have “Plan B” backups in R&D June 23, 2025

Odds and Ends: Embraer reports weak quarter; MRJ FTV #1 assembly; JAL, ANA politics

Embraer’s Third Quarter: Embraer delivered fewer commercial airplanes in the third quarter than had been expected. The maker of E-Jets and the E-Jet E2 re-engined versions due beginning in 2018 listed its deliveries and backlog in its press release. Analysts expects 22 E-Jets would be delivered in the quarter. But the backlog is up 44% year-over-year, largely on the strength of the launch of the E2 (150 orders, 100 of which are for the smallest E-175 E2 and 25 each for the E-190/195 E2), and orders from Republic Airways Holdings and SkyWest Airlines for the current generation of E-Jets. The E-175 remains to most frequently-ordered airplane.

Although Embraer is expanding the size of the E-195-E2 by up to 12 seats, orders have been few. The E-190 has proved a better-selling model than the E-195.

Source: Embraer

Officials expect to have a healthy fourth quarter delivery stream.

Mitsubishi MRJ: Assembly for the first Mitsubishi MRJ Flight Test Vehicle (to borrow Bombardier’s term for the CSeries) is underway. The first delivery was originally planned for this year; it’s now planned for 2017, four years late. This rivals Boeing’s 787 and exceeds the Airbus A350 and as yet the CSeries.

JAL, ANA Politics: Reuters has an analysis about the suspicion politics may have been involved in the decision by Japan Airlines to buy the Airbus A350 and the pending order by ANA of an Airbus or Boeing airplane.

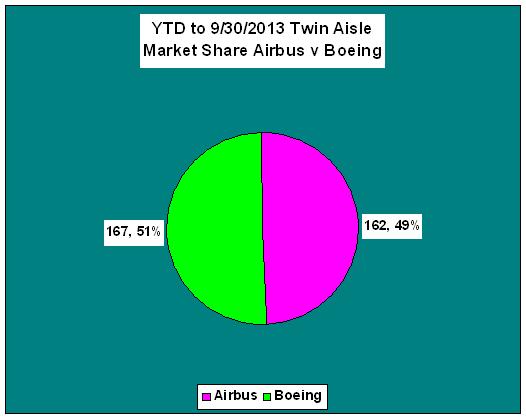

Latest twin-aisle orders shift market share; Plus Odds and Ends

The flurry of orders in September and this month from Lufthansa Airlines and Japan Air Lines tightens the wide body race between Airbus and Boeing.

Airbus and JAL on Monday announced a firm order for 31 A350s and options for 25 more. Last month, Lufthansa announced a firm order for 34 777-9Xs and 25 A350-900s.

Sources: Airbus and Boeing

Sources: Airbus and Boeing

Airbus traditionally has significantly trailed Boeing in the twin-aisle sector, but so far this year the race is running about even through September. The Lufthansa orders for the Boeing 777-9X and the Airbus A350-900, announced in September, are not reflected yet, nor is the Japan Air Lines order for A350-900s and -1000s. None of these orders has been booked yet by either OEM. Airbus would take the lead.

Odds and Ends: Slowing sales; Airbus in Japan; MRJ delay; Crandall on merger

Slowing Jet Sales: Within a few days, Bloomberg, Reuters and The Seattle Times each had stories about slowing jet sales.

Here is the Bloomberg story, focusing on cargo sales.

Here is The Seattle Times story.

The theme of each is worrisome, but with Richard Aboulafia’s comments to The Times, we disagree with his view on American Airlines. American has an ancient fleet of Boeing MD-80s and aging Boeing 757s that have to be replaced, and we believe the Airbus and Boeing orders won’t go away if the merger with US Airways is blocked.

Airbus still trying Japan: Airbus, which has never had a lot of luck penetrating the market in Japan, still appears to have an uphill battle, according to this article. The Reuters piece quotes Airbus’ John Leahy at the Paris Air Show; when we spoke with Leahy by phone from the IATA AGM immediately before the PAS, Leahy wasn’t quite as upbeat as quoted in the Reuters article. Leahy tamped down speculation that he’d have a Japanese order for the A350 at the PAS (and he did not) but neither was he ready to predict any timeline when one might be forthcoming.

Aspire Aviation continues to believe Boeing may place the 777X wing production in Japan as a means to secure 777X orders and block the A350.

Mitsubishi’s delay: Mitsubishi’s latest delay on the MRJ90 program is being blamed on not following FAA process, according to this article.

Poor South Carolina 787 deliveries: All Things 787 reports that Boeing’s Charleston (SC) 787 assembly plant has delivered only four 787s this year.

Crandall on DOJ AA-US lawsuit: Former American Airlines CEO Robert Crandall (who retired in 1998) has a very good analysis of the faults of the Department of Justice lawsuit to block the American-US Airways merger in this Bloomberg TV interview. He’s first up in the 22 minute segment.

Desperation: Kingfisher sued International Aero Engines for $236m over allegedly defective and poorly designed engines on the Airbus A320. This doesn’t pass the laugh test and smacks of desperation. The V2500 has been on the A320 for decades and seems to have been designed just fine and performing well.