Leeham News and Analysis

There's more to real news than a news release.

Bjorn’s Corner: Sustainable Air Transport. Part 44P. eVTOL operating costs. The deeper discussion.

Subscription required

By Bjorn Fehrm

November 4, 2022, ©. Leeham News: This is a complementary article to Part 44, eVTOL operating costs. It discusses the typical operating costs we can expect from an eVTOL when used in an air taxi operation.

Despite the operation of such transports being years off, an eVTOL has dominant cost factors that can be estimated today.

The A350 enhancements, Part 2

Subscription Required

By Bjorn Fehrm

Introduction

Nov. 3, 2022, © Leeham News: Last week, we described the New Production Standard (NPS) of the Airbus A350. Now we look at the economic performance of the A350-900 versus the Boeing 787-10 on the world’s busiest long-haul route, London Heathrow to New York JFK.

We compare the economics with a nine abreast economy cabin and what difference the NPS and a 10 abrest change for the A350 produces.

Summary

- The 787-10, with its long fuselage, is seat mile cost-optimized for medium long-haul routes.

- Airbus gives the airline the option with the A350 NPS, comfort, or seat mile optimization.

China still needs Boeing as much as Boeing needs China, despite interminable limbo

Subscription Required

By Scott Hamilton

Oct. 31, 2022, © Leeham News: China needs Boeing as much as Boeing needs China was the conclusion of an analysis by LNA in July 2021. A trade expert last week agreed. Airbus and China’s COMAC won’t be able to fill the future demand forecast for China.

Michael McAdoo, Partner & Director, Global Trade and Investment of the Boston Consulting Group (BCG) in Montreal and a former strategic chief of Bombardier Commercial Aircraft, told LNA in an interview last week that China needs the Boeing 737 MAX and widebody airplanes to meet demand in the near-to-medium term.

It will be long-term before China’s commercial aviation industry will be competitive with airplane designs and production.

Summary

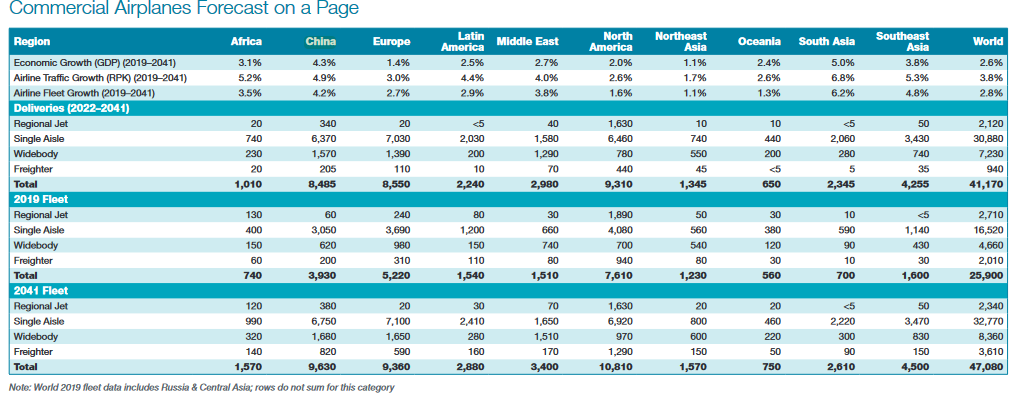

Forecasts for China’s demand for jet aircraft are consistent between Airbus and Boeing. But COMAC, which is the leader of China’s burgeoning commercial aviation industry, is significantly higher in its forecast. The independent Japan Aircraft Development Corp (JADC) is significantly lower.

- Boeing forecasts that China needs 8,485 new jets through 2041.

- Airbus forecasts 8,420 new aircraft will be needed through 2041.

- COMAC forecasts China will need 9,084 aircraft through 2040.

- JADC is more conservative, forecasting a requirement for 6,172 new jets in China through 2041.

Source: Boeing Current Market Outlook.

China will account for 21% of the world’s new aircraft deliveries through 2041, Boeing says.

Bjorn’s Corner: Sustainable Air Transport. Part 43P. eVTOL IFR range. The deeper discussion.

Subscription required

October 28, 2022, ©. Leeham News: This is a complementary article to Part 43, eVTOL IFR range. It discusses the typical maximum range we can expect from a certified eVTOL when it faces IFR weather conditions.

Flying in IFR conditions requires flight planning with increased reserves if the eVTOL can’t land at the destination airport and must divert to an alternate airport.

The A350 enhancements, Part 1

Subscription Required

By Vincent Valery

Introduction

Oct. 24, 2022, © Leeham News: Last month, Airbus announced that it started delivering A350s with a New Production Standard (NPS) with Iberia. The upgrades include weight savings, a maximum takeoff weight increase, and a longer and wider cabin.

A350 Fuselage. Credit: Airbus

Except for a few low-cost operators, the economy-class cabin on the A350 has usually featured a nine-abreast configuration with operators. The wider cabin could lead to a wider adoption of a 10-abreast economy class configuration with more A350 operators, for instance the legacy ones.

Despite the lingering effects of the Covid-19 pandemic on long-haul travel, several airlines still need to place sizeable twin-aisle aircraft orders in the coming years. The A350 enhancements could prove crucial in securing orders for Airbus against the competing Boeing 787 and 777X.

In this article series, we will assess how the A350 enhancements impact the economic performance of the aircraft against its main competitors. Before comparing competing aircraft, we define a methodology for consistent comfort standards among different aircraft families.

Summary

- The A350 enhancements in detail;

- A brief history of adding economy class seats in each row;

- Assessing passenger comfort standards;

- Upcoming twin-aisle sales campaigns.

“The music will stop” because aviation will miss target “green” deadlines: Boeing’s Calhoun

Subscription Required

By Scott Hamilton

David Calhoun. Source: Boeing.

Oct. 24, 2022, © Leeham News: Boeing CEO David Calhoun believes that the plethora of concepts for shifting to “green” aviation may be confusing policymakers.

And, he says, the pace outlined by the commercial aviation industry may contribute to the confusion.

Calhoun also said that Sustainable Aviation Fuel (SAF), while the most promising near-term technology to reduce aviation emissions, isn’t an easy solution, nor is it a complete solution.

Calhoun made his remarks last month at the US Chamber of Commerce Aerospace Summit in Washington (DC).

Bjorn’s Corner: Sustainable Air Transport. Part 42P. eVTOL mission range. The deeper discussion.

Subscription required

October 21, 2022, ©. Leeham News: This is a complementary article to Part 42, eVTOL mission range. It discusses the typical maximum range we can expect from a certified eVTOL by mid-decade.

We have described the vehicle and the mission data in the three previous Corners; now, we analyze the energy consumption for the mission and discuss the range we can achieve.

Engine Development. Part 10. Next generation engines

Subscription Required

By Bjorn Fehrm

Introduction

October 20, 2022, © Leeham News: We finish our series about engine development by looking at the next-generation engines and future trends in airliner engine development.

We limit this look forward to engines that burn Jet fuel (Jet-A1 or SAF) as green propulsion solutions are a vast field and justify their own series. We will pick this up at a future date.

The Boeing 777-9, the first airliner with next-generation engines. Source: Boeing.

Summary

- The major reduction in fuel consumption and, thus, CO2 emissions will come from new engines.

- The technologies to drive fuel consumption down a further 15% are there.

Analysts forecast traffic growth but scant profits for Indian airlines

Subscription Required

By Bryan Corliss

Oct. 17, 2022 © Leeham News: After sustaining major losses in their most-recent fiscal years, India’s airlines will recover in 2022. But rising fuel and labor costs, plus weak prospects for financing will constrain near-term growth.

That’s the analysis of Aairavat Transport & Technology Ventures consulting firm.

An IndiGo Airlines A320Neo on the runway at Mumbai. IndiGo is India’s largest airline. Photo by Timothy A. Gonsalves.

AT-TV’s assessment is less bullish than Boeing’s market outlook, which projects Indian airlines to add 25% capacity over the next year, with long-term growth targeted for 7%. Airbus is slightly more cautious, projecting 6.2% annual growth over the next two decades.

India is one of the world’s largest aviation markets. It’s also been one of the most challenging, with bankruptcies and constant financial distress plaguing the industry.

Summary

- India airlines have been in upheaval

- Tata Group wants new aircraft for Air India

- Indian airlines sustained major losses last year

- OEMs see long-term growth, but near-term outlook is choppy

Engine Development. Part 9. Gearbox or not?

Subscription Required

By Bjorn Fehrm

Introduction

October 13, 2022, © Leeham News: In our series, we look at the development of the latest single-aisle engines. Should these be geared? What do you gain and risk with a geared design? Is this a new development, or has it been around for a long time?

We examine the development of single-aisle engines since 2000, their fuel efficiency, and operational reliability.

Summary

- A geared design fixes some fundamental problems in a two-shaft turbofan.

- CFM proves you could just as well further develop what you have.