Leeham News and Analysis

There's more to real news than a news release.

Airbus and Boeing swing it out at ISTAT Europe 2015

By Bjorn Fehrm

07 October 2015, ©. Leeham Co: This year’s ISTAT Europe conference had been characterized by a “Steady as you go” ambiance until the traditional match between Airbus and Boeing on “Large aircraft segment” panel got going. This is normally when things can get a bit more exiting and this year’s version did not disappoint.

Airbus’ Mark Perman-Wright, Head corporate and Investor marketing, kicked off the jabbing during his coverage of all the usual segments, claiming that Boeing got to know that Airbus held the upper hand in just about all airliner segments.

Randy Tinseth, Vice President Marketing for Boeing, immediately responded that this was all wrong and that indeed Boeing was the market leader in all imaginable measurement dimensions.

The audience of 1.200 financiers, lessors, airlines, consultants, etc., could see that a drastically lower fuel price had changed nothing. Airbus’ and Boeing’s fight over the market dominance, both real and verbal, is as fierce as ever. As we could get a hold of Boeing’s presentation and both OEMs followed the same route through their product programs we will use Tinseth’s slides as a base for our ringside review.

Both OEMs choose to start with their weakest segment, the VLAs. Their focus was colored by where they had business, with Boeing describing their recent order for 747-8F and other freighters:

Airbus focused its part on how much better the A380 is getting without changing engines. Through several cabin programs, the operator would gain $23m in revenue on a yearly basis given increased cabin density and re-position of galleys etc. It is clear that both OEMs have disappointing sales in this market and therefore give the segment prime exposure during any customer facing activity.

Next up was widebodys. Airbus proved that they had outsold Boeing in the 300 seat widebody field by 561 airplanes since the 787-9 was launched in April 2004. They achieved that by bundling A330-300, -900 and A350-900 sales to a total of 1,255 orders. Boeing has in the same time sold 691 787-9, -10 and 777-8X said Airbus.

Our comments are that the 777-8X does not belong here; it is a competitor to the A350-1000 at the 350 seat level. Furthermore, 300 seats is a bit narrow, normally the segment would be 250-300 seats and the A330-200/-800 and 787-8 would be counted in. That would change the picture to more of a 50:50 basis. If one goes 300-350 seats instead, the 777-300ER sales of 700-800 units in the period would tip the balance in Boeing’s favour versus the A350-1000’s 172 orders.

Boeing focused the segment time on its success with the 787. Here a slide with some key numbers:

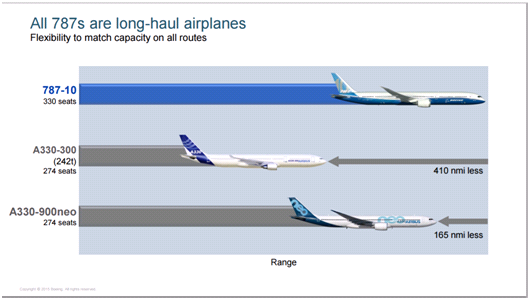

Boeing then chose to go on attack regarding the perceived insufficient range of the 787-10. Tinseth showed this picture, which establishes that Airbus has a much larger problem with its widebody portfolio regarding range that does Boeing with the 787-10:

Tinseth’s argument was that all 787 aircraft are long range and they fly further than the competition. In a subsequent discussion, Airbus and Boeing agreed that Boeing has been the stronger in the widebody market but Airbus disputes that this will continue now that it has A350 and A330neo.

Finally the parties got to the single aisle corner of the ring. Here things got a bit muddy. Pearman-Wright showed how Boeing’s 737 MAX has gotten 3.1t heavier whereas the A320neo has stayed at 1.6t for the Pratt&Whitney’s GTF and 1.9t with CFM’s LEAP. “When they start as the same level, the MAX then is heavier,” continues Pearman-Wright.

This is the key, they don’t. There is plenty of data out there (Turkish Airlines fleet sheets for their A320 and 787-800 being one source) that show the 737NG is considerably lighter than an A320ceo.

Pearman-Wright then focus on the fact that the P&W A320neo has confirmed weight, -15% fuel consumption and can take-off with up to 2t higher take-off weight. He said delivery to launch customer Qatar Airways will happen before year end.

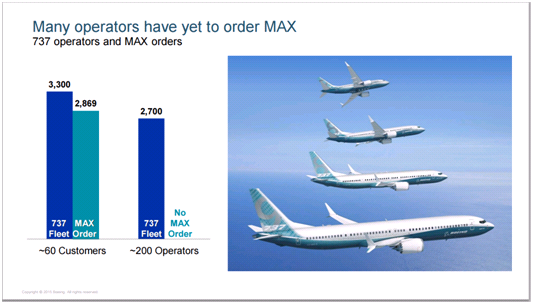

Tinseth said large 737 operators like RyanAir have not ordered their replacement 737NGs yet. The MAX therefore has a large captive market still not harvested:

Tinseth’s argument was that the MAX has an operator base which is more conservative with orders (RyanAir, Soutwest), whereas Airbus has booked mega orders for carriers with relatively small to no A320 fleets (Indigo, Norwegian). This increases the risk of overbooking by Airbus.

In summary, the only thing one can get these OEMs to agree on is that they cannot agree on anything of substance in the market. I guess that is how it should be.

Hello Bjorn !

Nice report !

Thanks

What are you thinking of the NEO/MAX order book and market share ? And boeing’s analysis of the captive market ?

Bonne journée

Hi Poncho,

re NEO/MAX sales and order book. I think both have a point. Airbus say they deliberately overbook and underproduce and have therefore not been forced to drastically reduce single aisle production (for the 330 to 330neo transition they had to) so any mega orders that is not taken is absorbed by others that take these aircraft happily.

Boeing has a more conservative order book at the moment for whatever reason. It could be that their sales teams have not historically been as aggressive on the up and coming LCCs in some corners rather then a deliberate policy.

Bjorn

I would say that’s a deliberate policy then if they are not working intensively in that segment in a somewhat negative way of assessing it.

‘Lies, damn lies and statistics’ Disraeli

I think we have introduced Bananas to Apples and Oranges. Great report, must have been an entertaining conference. Do the delegates laugh when some of the more outrageous ‘sleight of hand’ stats are discussed?

I have always thought we should have a L:T Index (Leahy: Tinseth) where 1 represents the view of Leahy, 7 represents the view of Tinseth and 4 is the objective view. All ‘posters’ should now be required to post their position in relation to this index going forward. Just a thought…

Well everyone would present themselves as a four of course!

But I thought I was the only objective one in a world of bias….. Have I missed something?

“Captive market”?

They’ve managed to lose significant share on some major ‘captive’ customers already – AA, Norwegian, Lion. I wouldn’t be so cock-sure in their position.

Yes, it’s true that Southwest & Ryanair will order many more MAX, but it’s pretty arrogant to think that all those existing 737 customers who have yet to order will automatically select MAX.

I actually think there’s a reasonable chance that Ryanair will go to the A321NEO for at least part of their order. Wizz Air are the only European carrier to approach Ryanair on unit costs[1], and with their order for the 321NEO, I could see Wizz reaching or surpassing Ryanair’s cost base on certain routes.

And I don’t see Ryanair letting that happen. They’re too aggressive a competitor to leave much of Eastern Europe to Wizz without a fight.

[1] http://centreforaviation.com/analysis/wizz-air-and-ryanair-are-well-matched-in-the-competition-for-eastern-and-central-europe-markets-235286?utm_source=twitterfeed&utm_medium=twitter

Where do I find the Turkish Airlines fleet sheets? I remember seeing them somewhere, but would like to find them again.

cheers

“I have always thought we should have a L:T Index (Leahy: Tinseth) where 1 represents the view of Leahy, 7 represents the view of Tinseth and 4 is the objective view. All ‘posters’ should now be required to post their position in relation to this index going forward. Just a thought…”

If two plus two is four and I don’t like it, I can say “eight!” and a majority will settle for the average, six..

I feel this is actually practiced sometimes, communicate a half lie and confuse the public a bit away from the harsh truth.

About the 787-10 and its range, isn’t it competing with the A350-900 instead of the A330s? If not, why?

As than the picture doesn’t work anymore?!?

http://i298.photobucket.com/albums/mm262/ferpe_bucket/PayloadrangeA350-900vs7810GIF2012_zpsec7c1065.jpg

all the quibbling and statistical fudgery that these salesmen spout is meaningless.

I would love it if Leeham would use their new updated LOPA models and just drop a “facts only” table showing A v. B sales & deliveries by year by seat count bucket

also interesting would some data regarding practical maximum range for each aircraft in Leeham LOPA configuration (i.e. longest route where you could guarantee both directions nonstop given winter bad headwinds one leg and typical cargo/passenger load factor)

I suppose that level of detail goes to paying subscribers only (sadface)

I second bilbo’s proposal!

While you’re at it, could we have honest & direct politicians too? I gave up going out to dinner with the aircraft salesmen, as we’d just tell each other what we already knew & started to invite them home for takeaways. Much more pleasant all round, especially for people who spent a lot of time in hotels.

All that really matters is the revenue and profit that each business makes; these are the undeniable facts, and what will keep the shareholders happy.

Clearly a large proportion of these kind of events is given over to theatrics; serious investors know this and will look beyond and into the detail for themselves to ascertain the true picture.

In other words, enjoy the show for what it is and don’t try to read too much into these superficial productions.

The A350-900 will be the gold standard of twin aisles from a comfort perspective. Crowd pleasing 2-4-2 configuration and wide seats. For 5-10 hour flights, the A350-900 is the best option for most of the flying public. Glad Airbus, Delta, and Hawaiian forged a better vision for that segment of travel.

L:T *2*****

You mean A330-900?

Ya, that one.

Don’t kid yourself. These birds will be flying in high-density config with 16.5″ seats in no time.

With what operators/airlines apart from LCC and charters?

We shall see. There are only two announced so far, and neither has released seating configurations to my knowledge. Given how quickly majors jumped on 10-abrest 777 I wouldn’t be surprised if 9-abrest economy sections appeared on A330 neo.

“The A350-900 will be the gold standard of twin aisles from a comfort perspective. Crowd pleasing 2-4-2 configuration and wide seats.”

Could be close. An improved cabin experience, double armrest for middle seats maybe slightly better wider seat enhancements, quieter engines. Maybe preferable over many others.

https://leehamnews.com/2014/09/06/final-a330neo-analysis-cabin-improvements-gives-the-a330neo-gains-over-todays-a330/

ISTAD membership is pretty savvy on all things aeronautical, having just returned from Prague the A v’s B road show is these days regarded as exasperating light entertainment.

The venue has an almost club type feel to it and the sharing of common interests and friendly banter that exists between members likely means they walk away with a greater understanding of capabilities and in service performance than either A or B would admit too

To me its just Theatre

What really matters is who delivered how many aircraft this year.

Unlike autos, they have convinced people tghat orders are the benchamakr when they can only produce so many a year and for single aisles its almost exacly 50/50

Wide aisles Boeing has the overall advantage and I don’t see the FedEx 767 or the 767 Tanker (I can never remember what KC number they changed it to)

Airbus can choose to ignore that (put in the MRTs for A330 as well).

But the 767 alone is 269 aircraft on a program that is paid for (tanker travails aside the production part is paid for, established process and kept hot)

Airbus will move up in wide aisle sales and we all get to sit back and see what happens to 747 and A380.

“Wide aisles Boeing has the overall advantage and I don’t see the FedEx 767 or the 767 Tanker (I can never remember what KC number they changed it to)”

Could you finish your thought? Thanx. 🙂

Sorry, thought it was clear but see it was not.

Basically as the 767 is in production in both freighter and early tanker, then those should be part of the overall sales.

Same with A330 MRT, add em in.

Not doing so selectively loads the dice in Airbus favor as they do not make many freighters and the total A330MRT orders don’t come close to the 179 KC46 (for better or worse)

Does Airbus take the 777F off the production same as 767F? 747F?

Thanks Transworld, sorry I was dense!

Pickles: not dense, it could have been worded better, good to clarify.

I think you are right regarding the 767, it just makes no sense to ignore Boeing #1 customer, supporter, R&D partner and tax agency.

http://marketrealist.com/2014/12/investors-introduction-boeing/#image-view

Keejise

I will remind you that the US shares its aeronautical research with the world (NASA) . Does Europe?

The fact that there is spin off from Military to Commercial and visa versa I don’t think has any validity as it occurs in all countries.

Where was the US supposed to get its KC135s from ? Commet?

Do I agree there should not be launch aid? Yes

Do I vehemently disagree with what Washington State did? Yes

Did Airbus refuse those same tax breaks in Alabama? No

On the original WTO assessment Boeing as asses a something like 6 billion against Boeing and 18 billion against Airbus.

Interesting aspect as if you have a successful program like the A320 its taughted as continue to pay back. However the A380 will never pay back so in affect what they are doing is paying back the A380 loans with the A320 program.

A380 being artificially launched killed the 747. That’s not one company entity assisting another, each launch aid should stand on its own.

17 years to be repaid and I don’t see that happening.

Ergo, it distorted the so called free market.

Transworld

I fully concur with your views re deliveries but I would like to suggest an alternate scenario. The world economy takes a major dive, something consistent with almost every measure from political to demographic to economic. I know I sound like the deranged man at the street corner. Look at historical trends and this economy of free money has a limited life unless we call it a new paradigm (ha).

Given that it comes down to the best frame for the job. Airlines do not buy on promise and bull anymore, the products must stack up both in terms of spec and price. Looking back in recent years b777-300er is a one trick pony that is worth the trick, a330-300 something similar, winner takes all within its specific spec and no space for competition.

We move on to find 787-9, 350-9, (350-10 and 787-10 (jury out)) and 777-x to be the go to aircraft, in their niche they look likely to take the winnings. A330neo could mop up some medium haul stuff. VLA dead, I am sorry to say.

The fun is in short haul, a320/b737 has been fun for years, this where the base cash is generated for both OEMs. But in 5 years what will we see? I fear a slow debacle unfolding for the b737 as the production numbers stall in 2020. Hope i am proven wrong by a NSA to be announced shortly.

I do agree that massive long term sales can be an indicator.

However, if Boeing tilts the deck and comes out with an all new 737RS then what happens at that point? Suddenly they have slots available that Airbus does not (and probably not in Washington state for Assembly)

I don’t say sales is not an indictor but if you can’t make the numbers you sold then the only true bench mark is produced (and most sold) vs the pie in the sky never to be achieved.

I don’t disagree on the world situation, its pretty squirrely.

I don’t know about the one trick Pony so much as nothing in that exact segment works.

I do have to wonder when people like Finair buy an A330 improved and then get talked into an A350 that is clearly a category above what they ordered?

So did they order the wrong thing originally or are they enamored with Airbus and as long as its reasonably competitive going with them?

I am not saying Boeing does not have “loyal” types as well but the A330 shift was pretty amazing how many upsized when either they don’t need an A350 or they were wrong that the A330 was the right size and range all along.

“Tinseth said large 737 operators like RyanAir have not ordered their replacement 737NGs yet. The MAX therefore has a large captive market still not harvested:”

I am certain Michael O’Leary will be amused to be learn Ryanair is a captive market. There are a number of airports in Europe that thought like that as well, only to learn the contrary.

Bjorn – just to be clear – I am assuming this is your insertion and not something that Boeing actually stated at ISTAT. Is that right?

Ryanair would have to pay a realistic market price for the A321. That might be an issue.

Keesjie: that is funny though. When you sell more than you deliver and no competition why should Airbus sell Ryan Air an A321 at other than a nice profit!

Maybe he is waiting for the MOM?

The word captive is mine but Tinseth said the same in more words.

I think the facts support Tinseth and Boeing especially in the widebody space. Have to wonder if the A350-1000 is the A340-500/-600 all over again.

Follow the orders . . .

http://www.wsj.com/articles/ethiopian-airlines-to-buy-15-to-20-boeing-777x-jetliners-ceo-says-1444227923

SQ, CX, BA, UA, AA, AF, KL, QR, DL, EY, JAL , loyal Boeing customers and large 777 operators.

They all ordered A350 fleets, including A350-1000 orders and conversion rights.

It took many years; a blow in slow motion. Ferociously denied and overshouted by the Boeing side. Still happening, 777x didn’t sell over the last 15 months. The press / analysts are careful, not asking questions. Ethiopian is a great win.

Yes, I see a similar trajectory of the A332 vs A333. There is a good possibility that eventually more A350-1000 are produced than A350-900. Or, maybe more A321 than A320? Something for Boeing to ponder.

The A350-900 needs to trade range for more space. How about a 4m stretch, the A350-950 at the same -900 weights?

Enzo is right . . . “follow the orders” . . .

http://www.seattletimes.com/business/eva-airways-to-buy-26-widebody-boeing-jets/

Long week in Toulouse or is it “to-lose”. Reduced to roping off some seats and rebranding an airplane.

I thought Bair was arrogant at ISTAT when he said Boeing was going to dominate the widebody sector. Now I am not so sure. Perhaps he was just being matter-of-fact.

What Bair said was Boeing was going to drive Airbus out of the twin aisle business.

ET going for the Airbus was always going to be a longshot. Especially so after Obama’s recent trade mission to Ethiopia.

http://www.travelpulse.com/news/airlines/obama-visits-ethiopia-salutes-its-airline.html

What no one has addressed is the big move up to the A350.

Comment was made how astute the operators are in their selection.

either they were biased to Airbus (I am fine with that I have equipment bias as well sometimes based on support not equipment being better) but then the astute is not correct as they buy closest available not best offering.

I think Hawaiian was the sole holdout because the A330 was what they wanted not the A350 (and got it eventually, probably at a great deal)

So either the A330 was wrong for a lot to start out with or the A350 was right and they ignored Boeing offe4rings.

I don’t call that astute, I call that politics and maybe under the table relationships. Not that its new but…..,.

TransWorld I’m not sure what you exactly mean, but at the time the A330 and A350 were both selling fast and conversions were made (2006-2012) , the 787 world was one of broken dreams and promises where everybody learned to ignore official program updates.