Leeham News and Analysis

There's more to real news than a news release.

Asian airline shift portends big ramifications

Subscription Required

Introduction

April 17, 2017, © Leeham Co.: A shift is underway among Asian airlines that could have ramifications for the airframe and engine manufacturers and, by extension, their suppliers.

It doesn’t appear, however, that aerospace analysts in the US and Europe realize this shift. At least none has written about it that we’ve seen among the research notes we receive.

Summary

- The creation of the Value Alliance of Low Cost Carriers brings together eight LCCs under one alliance.

- AirAsia faces a competitive threat.

- Full service carriers also face a threat, particularly those in Japan, concludes one aerospace analyst team in the region.

- Airbus, Boeing have a backlog of more than 1,000 airplanes with the VALCC group and hundreds more with other airlines.

Read more

Pontifications: Lessor cites cool reception to MAX 10

By Scott Hamilton

April 17, 2017, © Leeham Co.: Buckingham Research Group last week issued back-to-back notes about Boeing. One was a recap of an investors call with Steve Rimmer, CEO of Altavair Airfinance (nee Guggenheim Aviation partners). The other was BRG’s earnings preview, the first off the mark for Boeing’s earnings call on April 26.

I’ll include a summary of BRG’s earnings preview in a subsequent post when other analysts issue their previews.

BRG’s Rimmer note is lengthy and covers industry issues beyond Boeing. Here are a couple of the Boeing-focused points:

Airbus won’t hit 1:1 book:bill this year

![]() April 14, 2017: Airbus won’t hit a 1:1 book:bill (sales:deliveries) this year and maybe not for the next few years, it was revealed at the annual general meeting Wednesday.

April 14, 2017: Airbus won’t hit a 1:1 book:bill (sales:deliveries) this year and maybe not for the next few years, it was revealed at the annual general meeting Wednesday.

Credit Suisse issued a note late yesterday on a variety of topics that included this:

Trump reverses self on ExIm Bank

April 13, 2017, © Leeham Co.: President Donald Trump reversed himself and now supports the US Export-Import Bank, according to news reports. He will appoint

Donald Trump suddenly discovered the US ExIm Bank was a “profit center” for the US Treasury. Photo via Google images.

two people to long-standing vacancies to allow ExIm to approve deals more than $10m.

ExIm, Trump now says, is a profit center for the US Treasurer.

His sudden understanding on this revelation is like his eye-opening realization that dealing with the North Korean situation isn’t easy.

Supporters of ExIm pointed out for years that the Bank returns money to the US Treasury.

Could an NMA be made good enough, Part 4?

By Bjorn Fehrm

Subscription Required

Introduction

April 13, 2017, © Leeham Co.: Last week we finished the sizing of the fuselage for an NMA design. Now we continue with the wing. We go through the key parameters that will decide the performance of the wing and the aircraft.

The NMA is a critical design case. The performance envelope has to be just right. Too high and the economics of the aircraft won’t work, both for purchase price and operational costs.

Figure 1. The NMA takes more and more the shape of a 767 replacement (A United 767-200). Source: United

Summary:

- Wing design is the mixing of conflicting requirements to a successful compromise.

- The NMA wing will use the design principles of the Boeing 787/777X wings but will be different in area, size and plan-form.

- The wing is sizing the engines, something we will look at in the next article.

Delta reviewing Airbus wide-body order, but more is going on

Subscription Required

Introduction

![]() April 12, 2017, © Leeham Co.: Delta Air Lines today said on its earnings call that it is reviewing its wide-body order with Airbus.

April 12, 2017, © Leeham Co.: Delta Air Lines today said on its earnings call that it is reviewing its wide-body order with Airbus.

At face value, the Delta statement might seem alarming. But as so often becomes the case, the “review” may not be what it seems.

Summary

- There is more activity about fleet requirements than simply “reviewing” the wide-body orders.

- Delta’s preparing to issue an RFP for single-aisle Airbus A321neos and/or Boeing 737-9/10s.

- Boeing hopes Delta will be a launch customer for the MAX 10.

- The NMA/MOM aircraft could be involved.

Pontifications: 787 production rate remains a question

By Scott Hamilton

April 10, 2017, © Leeham Co.: Boeing’s first quarter earnings call is scheduled for April 26, two weeks and two days from today. Officials said on the January earnings call, for year-end 2016, that they will decide this year whether to increase the 787 production rate to 14/mo by the end of the decade.

LNC has long believed this won’t happen. In fact, we predicted last September Boeing will have to lower the production rate from 2020.

The question of the rate is sure to come up on the 26th. I doubt CEO Dennis Muilenburg will be prepared to announce a decision one way or the other. It’s Boeing’s pattern to put off announcements like this until the very last minute, so a go-no go on rate 14 probably won’t be announced until toward the end of the year.

Middle Eastern airline turmoil hits Boeing

Subscription Required

Introduction

April 10, 2017, © Leeham Co.: Tim Clark of Emirates Airline said the new breed of long-haul, low cost carriers are hurting EK’s load factors and yields.![]()

Etihad Airlines’ business strategy of taking financial stakes in LCCs hasn’t produced the positive financial results desired.

Three big airlines, EK, EY and Qatar Airways, face over-capacity now compounded by electronic carry-on restrictions by the US and UK.

Figure 1. Click on image for a crisp view.

The thee carriers largely compete for the same connecting traffic through hubs only 72-235 miles apart (Figure 1). This is like having hubs in Milwaukee and Chicago (81 air miles apart) and Chicago-Detroit (237 air miles) with much, much smaller domestic catchment basins.

Summary

- Declining financial results for Emirates, Etihad.

- Deferring airplanes: 787s, 777X

- Long-haul LLC, Trump travel ban, poor investments hurt the airlines.

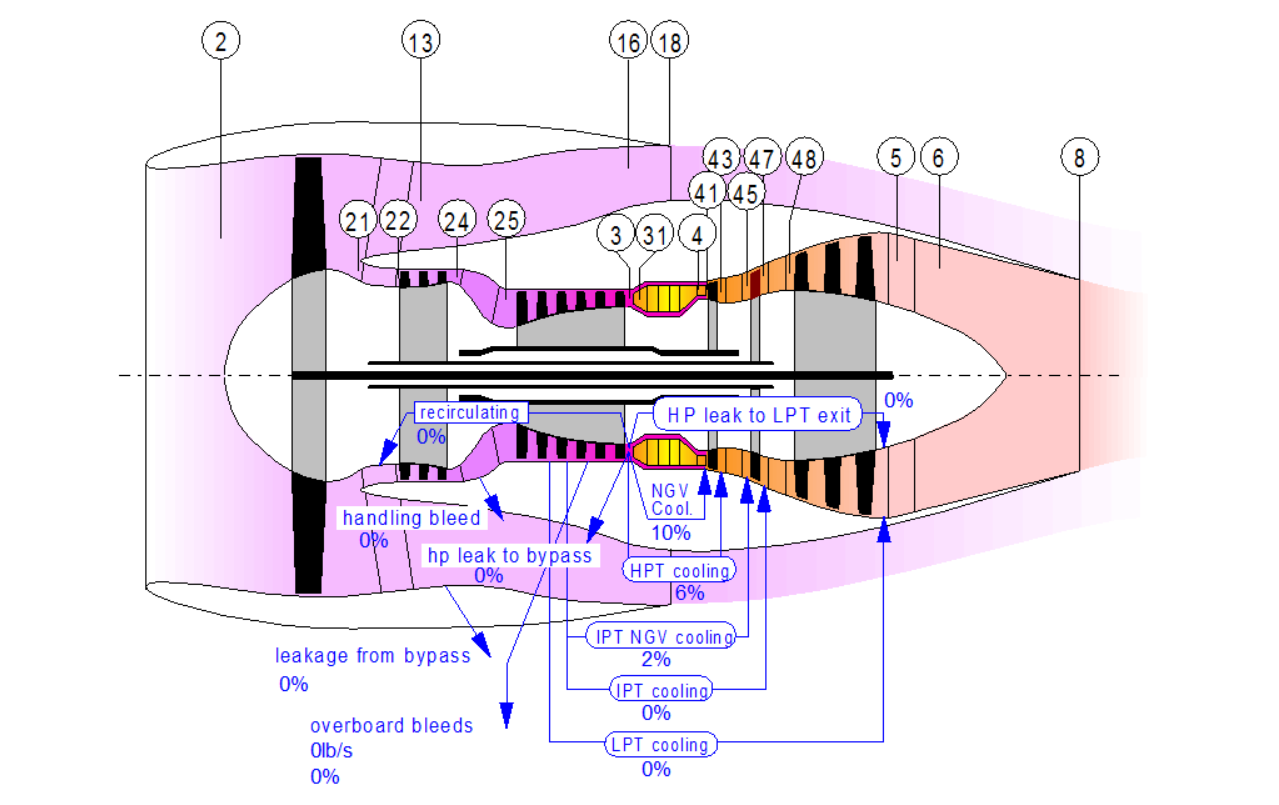

Bjorn’s Corner: Aircraft engine maintenance, Part 6

By Bjorn Fehrm

April 7, 2017, ©. Leeham Co: Last week’s Corner developed the overhaul shop visits per year for wide-body engines. We will now look at how the market develops around these overhaul opportunities.

How does the shop structure develop over a popular engine’s life-cycle? How much choice has an operator and when?

Figure 1. Principal picture of a three-shaft wide-body turbofan with station numbers. Source: GasTurb.

Things get worse before better at Cathay

April 6, 2017, © Leeham Co.: Cathay Pacific Airways faces a loss this year after posting its first loss in eight years last year.

Analysts following the Hong Kong-based airline see another loss, with declining revenues and pricing pressure from competition.