Leeham News and Analysis

There's more to real news than a news release.

Bjorn’s Corner: What did we learn in 2015; engines

By Bjorn Fehrm

15 January 2016, ©. Leeham Co: Last week we looked back on what happened in 2015 on the airframe front. We finish the retrospective by looking at what turbofan engine technology came to market in 2015. New engine technology is vital, as it is on the engine side that the quest for higher fuel efficiency has the largest successes.

While advances on the airframe side might bring an additional 5% per generation, the engines typically increase their efficiency per new generation with up to three times that value. Fuel efficiency per delivered thrust unit was improved with a whopping 15% over the engine it replaces for the Pratt & Whitney Geared Turbofan (PW GTF). It was certified for use on the Airbus A320neo in Q4 2015

The competing CFM LEAP-1A shall deliver the same improvement level to the A320neo once it is certified in the summer of this year. This engine has a smaller sister that started ground tests last year, the LEAP-1B, which is developed for the Boeing 737 MAX series.

The engine that is easily forgotten is the Rolls Royce Trent XWB. It entered service on the Airbus A350-900 during the year. It brings an improvement level of around 10% compared to the engines of the aircraft that the A350 replaces (Airbus A340/A330ceo and Boeing’s 777-200 range).

Dissection of the 2015 Airbus order book

Jan. 13, 2016, © Leeham Co. Airbus yesterday reported 1,139 gross and 1,036 net orders for 2015, dramatically out-performing Boeing’s sales figures.

Jan. 13, 2016, © Leeham Co. Airbus yesterday reported 1,139 gross and 1,036 net orders for 2015, dramatically out-performing Boeing’s sales figures.

Boeing’s 737NG outsold the A320ceo family but the A320neo captured 67% of the sales vs the 737 MAX. The A321neo picked up 98.3% of the market against the 737-9.

Boeing dominates the twin-engine wide-body sector, posting 212 gross orders compared with 170 for Airbus. Airbus recorded a 45% market share.

But Boeing’s clear win was due to the freighter sector, with the tipping order the 49 767-300ERFs from FedEx. Boeing sold 71 freighters last year, compared with just four by Airbus.

Lining up passenger-to-passenger model sales only, Airbus sold 166 twin-engine wide-body airplanes and Boeing sold 141, for a 46% market share.

Exclusive Interview: Airbus COO Tom Williams about changing times for Airbus.

By Bjorn Fehrm

Subscription required

Introduction

13 January 2016, ©. Leeham Co: Airbus COO Tom Williams has a goal of reducing development expenses by 50% and streamlining the production to “best in class.”

Williams is in charge of the areas at Airbus with the greatest headwinds as Airbus goes from a development driven company to a production driven one.

It’s a daunting task to manage development, production and sourcing for a company with a product range where each delivered unit is made up of four million parts. It does not get easier by having to shrink the development activities from 30,000 employees and contractlors to 20,000.

We spoke to Williams about these challenges at the sidelines of Airbus 2016 annual press conference that recapped 2015 orders and deliveries.

Summary:

- Airbus is now changing from a development-driven organisation, constantly creating new products, to a production-oriented organisation.

- The development activities have to be transformed so as to support a company to that does constant improvement and derivatives, not new product lines.

- At the same time, the shareholders are saying it is payoff time. Years of investment shall now be honoured with industry conform return on invested capital. Read more

Airbus annual press conference 2016

By Bjorn Fehrm

Introduction

12 January 2016, ©. Leeham Co: Airbus held its annual press conference in Paris today against a backdrop of record 2015 deliveries. The year that went past was consequently a good one for Airbus. Orders were at a record high for the third year in succession and deliveries exceeded previous years for the 13th year in succession.

But the Airbus sky wasn’t totally cloud free; the large A380 only got sales by having ANA mop up the mess after Japan’s Skymark bankruptcy and production of the new A350 was hindered by a sole source lavatory supplier.

The result was that Airbus missed two 2015 delivery targets, the 15 per year for A350 (delivered 14) and the 2016 delivery of the first A320neo. The latter was because of “paperwork issues” related to certain things being “late to finish” ahead of certification. Read more

Dissection of Boeing’s 2015 order book

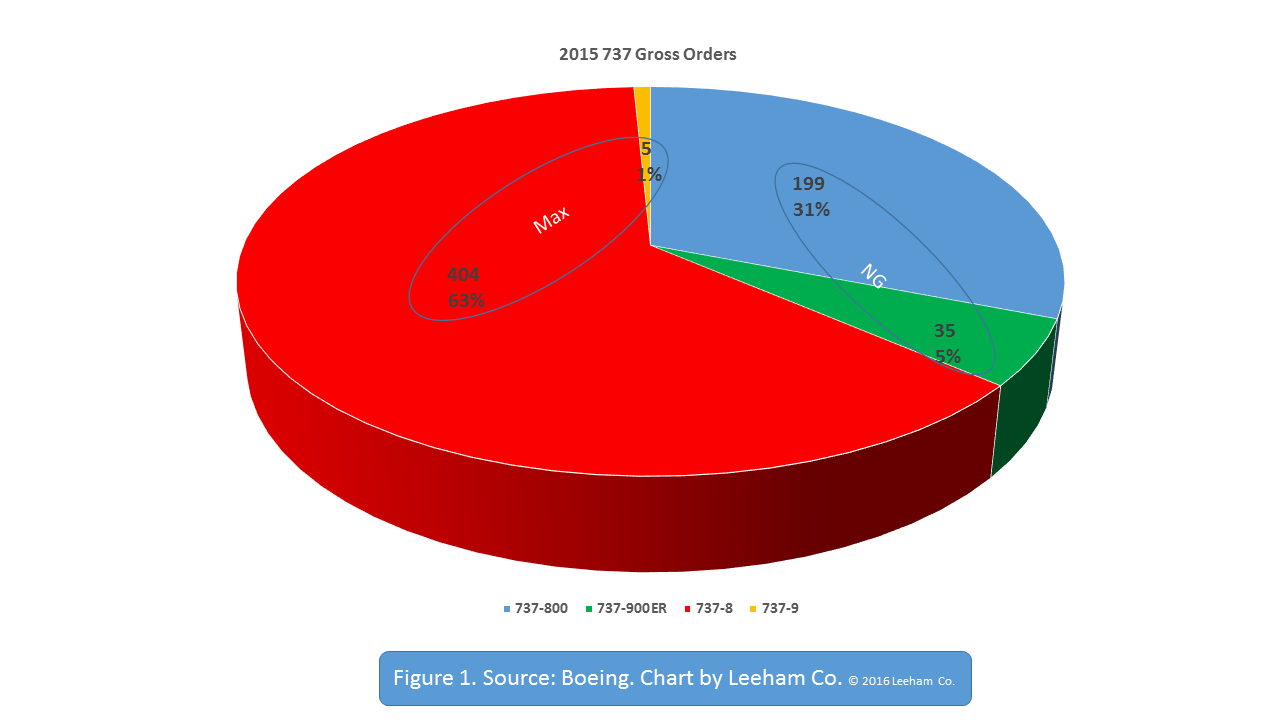

Jan. 12, 2016, © Leeham Co. Boeing announced its year-end 2015 orders tally, with 768 net orders and 878 gross orders. It is becoming increasingly clear the 737 MAX is essentially a one-aircraft family.

Jan. 12, 2016, © Leeham Co. Boeing announced its year-end 2015 orders tally, with 768 net orders and 878 gross orders. It is becoming increasingly clear the 737 MAX is essentially a one-aircraft family.

As expected, 737NG orders are declining, but Boeing won an important order from Delta Air Lines for the 737-900ER. There were no orders for the 737-700 and the 737-800 remains the backbone of the NG family.

There were no orders last year for the 7 MAX. There were four commercial orders for the 9 MAX plus one -9 BBJ. There were 400 orders for the commercial -8 MAX and four -8 BBJs. This means 99% of the MAX sales were for the -8 MAX and just 1% for the -9 MAX (Figure 1).

The -9 MAX nonetheless currently accounts for about 9% of the MAX backlog (Figure 2.)

Pontifications: Deliveries matter, so do orders

By Scott Hamilton

Jan. 11, 2015, © Leeham Co.: Boeing out-delivered Airbus last year by a wide margin. Airbus obtained more orders than Boeing by a wide margin.

Behind our paywall today, we look at some of the reasons for this as we update our annual production forecast. The principal reason Boeing out-delivered Airbus is that production for the 787 is going full blast and production for the A350 is only beginning to ramp up. By 2018, we forecast Airbus will slightly surpass Boeing in production and therefore deliveries.

With Boeing trailing Airbus dramatically for orders this year, an old refrain has resurfaced from years ago when Airbus began outselling Boeing. Phil Condit, then the CEO of Boeing, dismissed the Airbus gains by saying orders don’t matter, only deliveries matter. There have been a few similar statements in recent times.

Bjorn’s Corner: What did we learn in 2015?

By Bjorn Fehrm

08 January 2016, ©. Leeham Co: It’s the first Corner for the year and a look at 2015 as a year of technology advancements is due. 2015 will be remembered as the year when three clean sheet airliners passed important milestones. This will not happen for many years to come, so it will be worth to look at what they brought to world of aviation.

I’m thinking of Bombardier’s (BBD) CSeries getting certification for its first variant; the Mitsubishi MRJ doing its first flight’ and COMAC’s C919 being rolled out. Going forward, we will only have derivatives progressing through such milestones for years except for the roll-out of United Aircraft’s MS-21 single aisle airliner in 2016.

The Airbus A320neo was certified in 2015 and Boeing’s 737 MAX rolled out, but these are derivatives of in-service aircraft.

Embraer’s E-Jet E2 will roll out in February but this is a further development of today’s E-jet and Airbus A350-1000 is a variant of the in-service A350-900.

It will be a long time before we see so much new in a year, so it can be instructive to look at to what extent did these new aircraft bring the state of the art of airliners forward.

Boeing delivers 762 airliners, gets 768 orders in 2015

![]() Jan. 7, 2015: Boeing racked up 762 airliner deliveries last year, a record, while booking 768 orders–a book:bill of fractionally over 1:1.

Jan. 7, 2015: Boeing racked up 762 airliner deliveries last year, a record, while booking 768 orders–a book:bill of fractionally over 1:1.

Boeing throughout the year had largely guided a book:bill of slightly better or slightly lower than one.

The company delivered 495 737s, an equivalent rate of 41.25/mo. There were 18 747-8 deliveries, matching the monthly production rate of 1.5/mo. There were 16 767-300ERs delivered, matching the production rate, and 98 777s, slightly fewer than the equivalent 99.6 annual production rate.

LNC’s annual production forecast for Airbus, Boeing

Subscription Required

Introduction

In our annual production rate forecast for the Big Two OEMs, we combine announced production rate plans, Market Intelligence indicators—largely from the supply chains that serve the Big Two—and our own analysis of where we believe rates should be based on backlog, market conditions and ramp-up of the 777X and A350 production.

conditions and ramp-up of the 777X and A350 production.

Our forecasts may well run contrary to what the Big Two will say publicly, and even privately, but our assessment is what it is.

Summary

Read more

2 Comments

Posted on January 11, 2016 by Scott Hamilton

Airbus, Boeing, Leeham News and Comment, Premium

737 MAX, 747-8, 767, 777, 787, A320, A330, A350, A380, Airbus, Airbus and Boeing production forecast, Boeing, Leeham Co.