Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Bjorn’s Corner: New engine development. Part 5. Turbofan design problems April 26, 2024

- Airbus 1Q2024 results: Airbus CEO: “A350 in-service experience drives positive reputation and orders” April 25, 2024

- A350-1000 or 777-9? Part 3 April 25, 2024

- Boeing CEO promises company is turning around…again April 24, 2024

- Solid start for stand-alone GE Aerospace despite cuts to LEAP output April 23, 2024

Pontifications: Twelve new designs in 10 years spurred orders

By Scott Hamilton

Aug. 8, 2016, © Leeham Co.: The book:bill for Airbus and Boeing this year will be hard-pressed to reach one. Airbus has a better shot, given lower production rates. But the recent years of record-setting orders are over for now.

Unlike some, this doesn’t represent a bursting bubble to LNC. Rather, it’s a natural progression of the cycles that are historically seen.

It’s necessary to put some context into the recent years of these unprecedented number of orders.

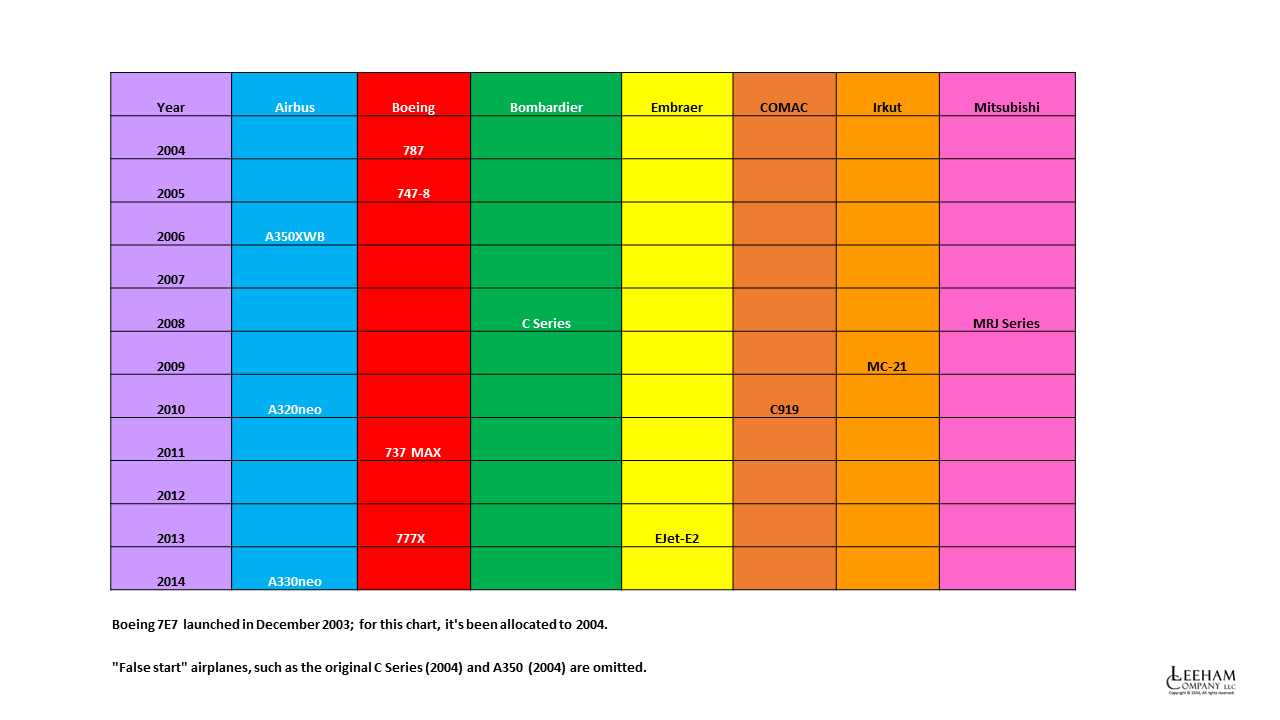

Twelve models in Ten Years

Serving as the backdrop for the pace of orders was the development worldwide of 12 new and significant derivative airplanes in 10 years. There was also launch by Airbus of the A350-ULR and the A321LR, minor derivatives of their respective families.

None of this counts the basic family subtypes of many of these models.

Click to enlarge.

It was the dawn of the jet age in 1954 (after the de Havilland Comet’s unfortunate disasters) with orders from Pan American World Airways that set off a splurge of development. There were 10 mainline aircraft designed, from the Boeing 707 and Douglas DC-8 to the DC-9 in 1963. The Lockheed Electra and Vickers Vanguard prop-jets are included in this accounting (though neither was successful). Small turbo-props like the Fokker F-27 and YS-11 are not. The Soviet bloc aircraft are also excluded.

(The Boeing 737 program was launched in 1965, the start of the next development cycle.)

New technology, better fuel efficiency

With fuel prices spiking to what was then an unprecedented $40/bbl, Boeing launched the 7E7 in December 2003. Airbus responded with the first version of the A350, which was a heavily redesigned A330.

Neither airplane sold well in the first year. The Boeing, eventually named the 787, saw only 54 sales in 2004. The original A350 program launch followed in 2005, but met with tepid market response. A redesigned A350 XWB followed the next year.

Like the 787, the A350 XWB was an all-new design with new technology.

By now, fuel prices were heading up dramatically, eventually reaching about $120/bbl in 2010. Thus it was natural airlines wanted more fuel efficient narrow-bodied aircraft as well.

Bombardier’s 2008-version of the C Series was a game-changing aircraft. An all-new design with a new engine won some key orders that prompted Airbus to offer the re-engined A320neo. Boeing responded with the 737 MAX.

Embraer developed the EJet-E2, which is markets as a new design though its antecedents are clearly from what is now called the E1.

China, Russia and Japan also developed their own new aircraft, using new technology engines and designs.

New airplanes, burst of orders

With the high-fuel price environment, new technology engines and new engines, a burst of orders had to be expected.

Equally, as the backlogs got bigger and delivery dates farther out in the future, it was inevitable that the order cycle would peak. And it has.

The industry is now on the downward side of the bell curve of the cycle.

There currently is the near-term prospect of only one brand-new aircraft development program: the Boeing New Mid-range Aircraft, or NMA, for the Middle of the Market sector. If Boeing launches this program, perhaps next year, Airbus may feel compelled to launch a new-design response. At the moment, the NMA is hardly a given.

Boeing is considering another 737 derivative, the MAX 10. Airbus has a response ready if needed.

But the next five years are not going be as exciting as the last five. So orders aren’t likely to spike sharply any time soon.

What about the 77X in the chart? Seems significant

Yep another nice clean informative graphic but the 777x should be in there at 2013 yes?

@Geo Yes, 777X certainly should. Oversight. That’s the thing about lists: it’s too easy to overlook something.

This is definitely an oversight. But I don’t know if it has any Freudian implications or not. 🙂

A Freudian slip? It’s when you say one thing and mean your mother!

Thank you, thank you, you’ve been a great audience!

Agree, new wing, engines, fuselage frames qualifies for ” new”

“The original A350 program launch followed in 2005, but met with tepid market response”

But once the airlines realised these fine new planes would cost significantly more, many warmed to the A330 NEO, with all new engines, winglets and pylons as well as a more economical cabin layout.

In the meantime, in what is imo not at all good for the industry, there seems to be an alignment of turbon manufacturers with air framers. But there might be more to that than meets the eye.

turbofan*

“But once the airlines realised these fine new planes would cost significantly more, many warmed to the A330 NEO, with all new engines, winglets and pylons as well as a more economical cabin layout.”

They didn’t even wait for the NEO and bought 500 A330 CEO since 787 launch and before 787 troubles began & kept buying.

https://www.flightglobal.com/assets/getasset.aspx?itemid=60566

“Unlike some, this doesn’t represent a bursting bubble to LNC. Rather, it’s a natural progression of the cycles that are historically seen.”

Indeed – reading some press, you’d really think that some “analysts” were stupid enough to believe the airframers would continue to book massively over their build rates year after year and the airlines would be happy waiting decades for their aircraft.

In my opinion, the backlogs are too large – particularly in the narrowbody market. I believe that the airframers could have sold the same slots for more money if they’d held off a bit. Although I suppose counter to that, they were moving to capitalise on the airlines’ feeding frenzy and panic buys.

Somewhat concerning news via BBC…

“The UK’s Serious Fraud Office (SFO) has launched an investigation into allegations of “fraud, bribery and corruption” in the civil aviation business of Airbus.”

http://www.bbc.com/news/business-37005459

Hopefully this will provide some illumination on this dodgy corruption prone business that Scott is so fond of.

Yeah, I wonder why this isn’t a headline. I saw this and thought “this can’t be good. It seems as if it is kinda being buried in the news (I saw it late Saturday night, I believe)

Although, not seeing it on this website is not really surprising. Nor FlightGlobal.

@neutron: The Serious Fraud investigation is not something LNC has any knowledge of nor ability to investigate on our own. Putting it here would only be linking to other news reports. In contrast, the reported SEC probe of the Boeing program accounting is something with which we are familiar (program accounting, that is). Although we don’t like program accounting and believe it hides true profit and loss, it is an accepted method of reporting. We strongly defended Boeing’s right to use it and largely dismissed the validity of the probe as it was described in the press. Also in contrast, back in 2006 when EADS CEO and Airbus co-chair Noel Forgeard professed ignorance of the A380 problems that emerged in May or June that year, we were vociferous in our incredulity that he could make such claims.

That’s what I meant…it was a news dump on Saturday night and I regret not saying you guys wouldn’t pick up, nor FlightGlobal.

“With fuel prices spiking to what was then an unprecedented $40/bbl, Boeing launched the 7E7 in December 2003.”

Five years later the barrel peaked at $150 just when Bombardier was about to launch the CSeries at Farnborough, in July 2008. Shortly afterwards oil prices plummeted as we entered what is now referred to as the Great Recession. This situation may have helped BBD to sign a key customer (Swiss) when oil prices were extremely high. It’s only after the official launch that prices started to drop sharply, and this quickly became an unfavourable environment for the CSeries. However, had BBD decided to launch a bit later, or had the recession hit a little earlier, there might be no C Series today. So in a sense the timing was perfect for Bombardier. But I didn’t see it this way at the time. On the contrary, I thought that the declining fuel price was rather disastrous for the CSeries. On the other hand I did recognize at the time that it was a very good thing that the CSeries was already launched when the recession started.

Today we may, or we may not, be about to enter into a world recession, or perhaps just a simple slowdown, whatever the situation is the C Series order book is almost full for the next few years. On the other hand I believe that A&B should be cautious and postpone their respective intention to increase production rates. For a relatively long period of time we have been accustomed to high B2B ratios, but this situation is obviously changing now. The problem is that we don’t know if it’s only a fluctuation or if it’s part of a longer trend. For sure the potential for sustained demand is still there as many markets are stil developing, but perhaps we are due for a pause.