Leeham News and Analysis

There's more to real news than a news release.

Fundamentals of airliner performance, Part 6; The engine

By Bjorn Fehrm

19 Jan 2015: There is a lot written about the fundamentals of how aircraft fly. It is something that fascinates people and it generates a high level of understanding of these fundamentals. The same is not true for the airline turbofan engines in use today; their detailed function remains a bit of black art.

![]() To some extent this might be because what is exiting in the engines (the thrust) is generated behind closed doors. The only visible part of the process is a rotating fan face and sometimes a slight miss-colored exhaust out the other way. There is also at takeoff a funny buzzing sound interspersed with the general engine noise. Apart from that, the most that one sees is a round nacelle and that is it.

To some extent this might be because what is exiting in the engines (the thrust) is generated behind closed doors. The only visible part of the process is a rotating fan face and sometimes a slight miss-colored exhaust out the other way. There is also at takeoff a funny buzzing sound interspersed with the general engine noise. Apart from that, the most that one sees is a round nacelle and that is it.

Airbus reveals record orders at annual press conference

By Bjorn Fehrm

Toulouse 13 Jan 2015: Airbus today held their annual press conference where they among other things revealed their final numbers for orders and deliveries. The press conference was hosted by Airbus CEO Fabrice Bregier accompanied by COO Customers John Leahy, new COO Tom Williams and new Head of Programs Didier Evrard.

Airbus in 2014

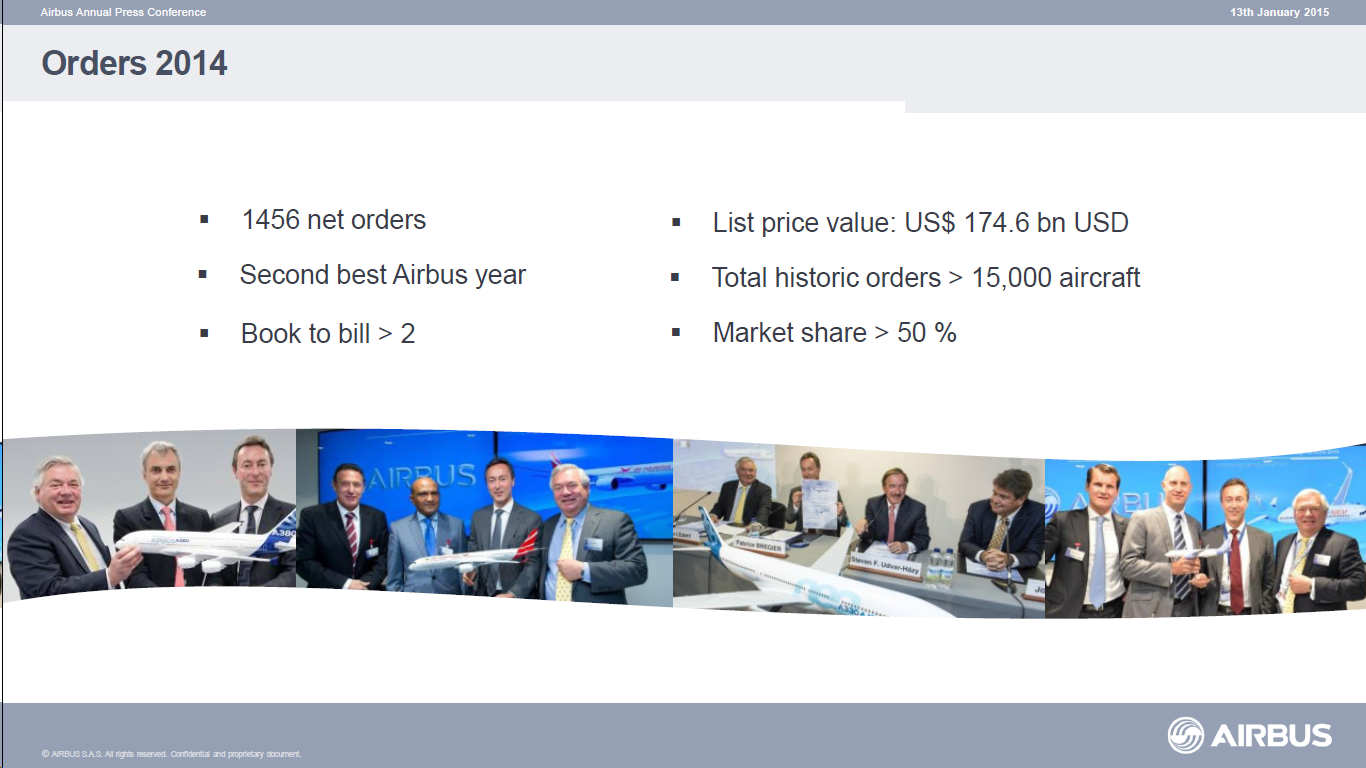

Bregier started with pointing out that 2014 was a very eventful year for Airbus. Airbus did their customary end of year sprint and passed Boeing for net orders with 24 aircraft netting 1456 commands, Figure 1.

Figure 1. Airbus orders for 2014. Source: Airbus.

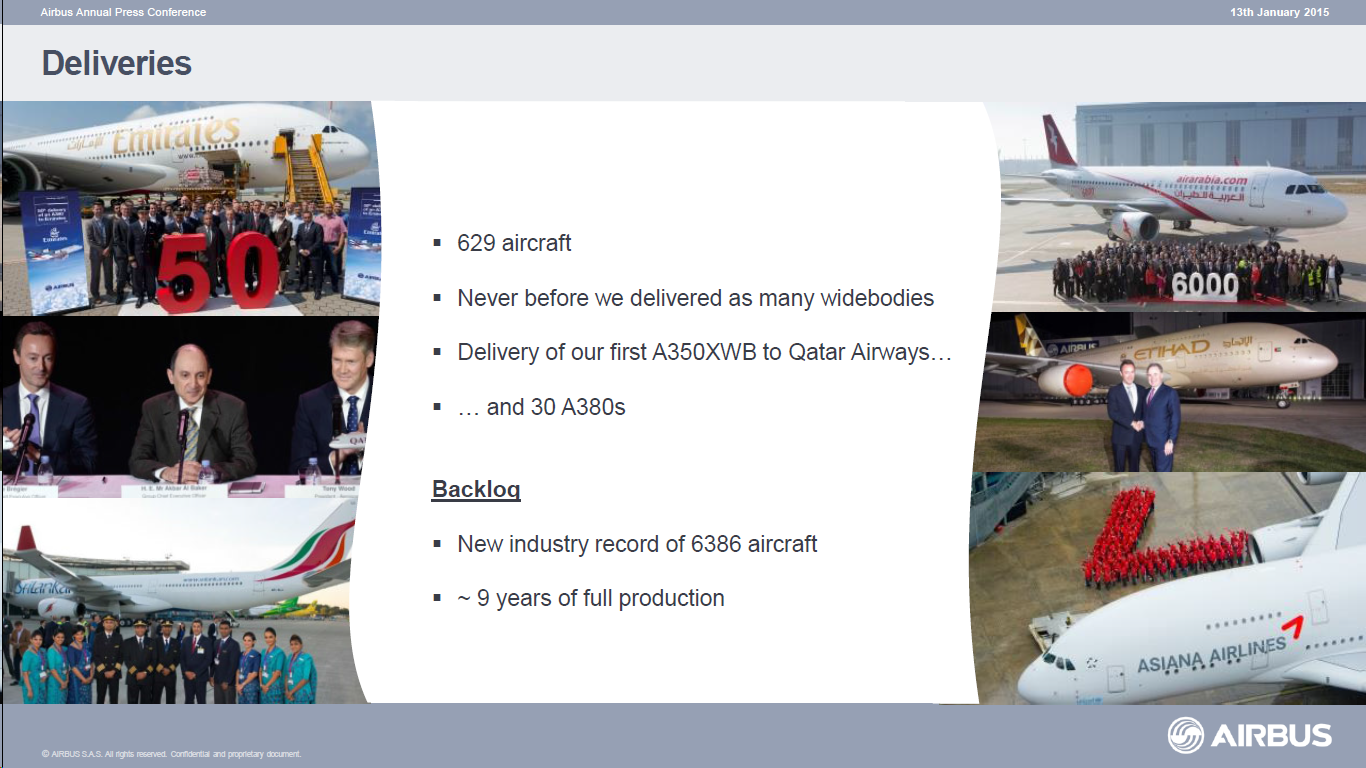

On the delivery side Boeing is ahead with 723 deliveries versus Airbus 629, Figure 2.

Figure 2. Airbus deliveries for 2014. Source: Airbus.

Further Airbus certified the A350 and delivered the first aircraft to its launch customer, Qatar Airways. It also launched the A330neo and got 120 orders during the year. Finally they flew the A320neo first prototype.

A380neo decision likely this year, triggering the next widebody engine project

Subscription required

By Bjorn Fehrm

Introduction

Jan. 12, 2015: One of the subjects which is sure to come up on Airbus annual press conference on Tuesday the 13th in Toulouse will be when and how Airbus will re-engine the A380.

Airbus Commercial CEO Fabrice Bregier vowed during the Airbus Group Global Investors Day last month that an A380neo is coming.

There is much speculation around this subject as the business case of re-engineering an aircraft that is selling at such low numbers is difficult to get to close. The business case is difficult to make work for Airbus ![]() (such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

(such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

Summary

- A380 Classic equals Boeing 777-300ER seat fuel costs.

- Boeing 777-9 beats A380 on CASM, an A380neo regains the advantage.

- Engine makers face hard choices to retain dominance or to broaden market penetration.

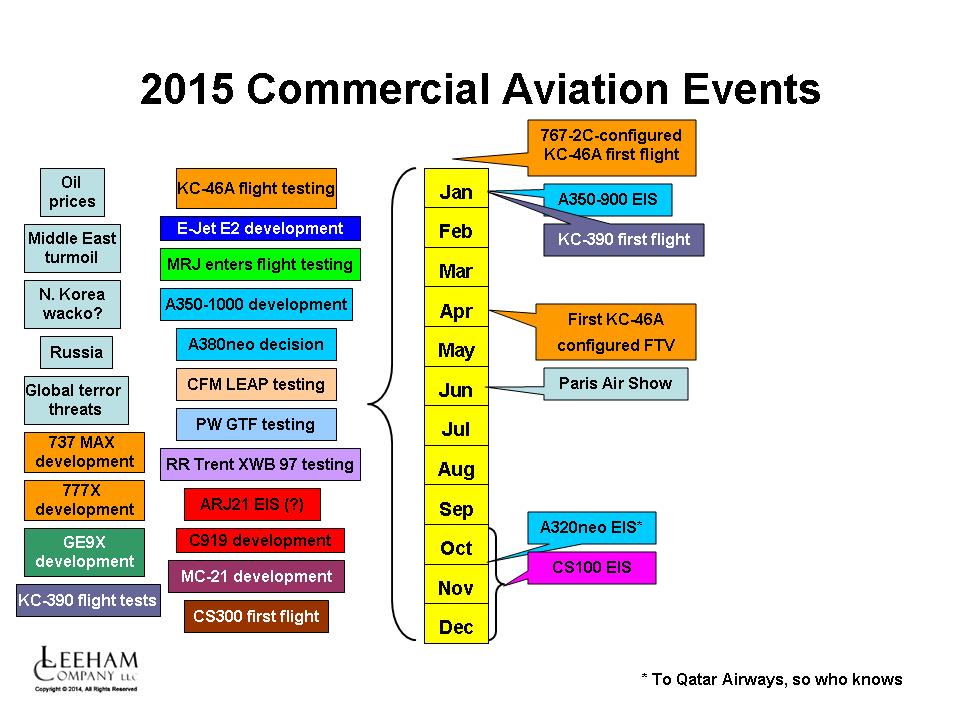

Looking ahead in 2015 in commercial aviation

Here’s a visualization of events to look for in commercial aviation in 2015.

Click to enlarge for crisp view.

Boeing 777-300ER and its replacements; A350-1000 and 777-9X.

By Bjorn Fehrm

Subscription required.

Introduction

Dec. 21, 2014: Last week we did a deep analysis of A380 and its competition. It has been windy weeks for the aircraft since the Airbus Global Investor Forum and it was time to bring some needed facts on the table. These facts showed there is a clear difference between the hype being perpetuated in the media and the reality. As we cleared the situation around the A380, we also touched on the large twins that could fulfill at least parts of its missions.

![]() There has been a lot of discussion around these aircraft as well as they form the battle of titans one level down from A380, the large, long-haul market today dominated by Boeing’s 777-300ER (the A380 does not have a real competitor–the 748i is clearly smaller, in fact so much smaller that it will be engulfed by the 777-9X).

There has been a lot of discussion around these aircraft as well as they form the battle of titans one level down from A380, the large, long-haul market today dominated by Boeing’s 777-300ER (the A380 does not have a real competitor–the 748i is clearly smaller, in fact so much smaller that it will be engulfed by the 777-9X).

Summary

- The 777-300ER had an exclusive run in its size until launch of the A350-1000;

- The A350-1000 doesn’t enter service until 2017;

- 777-9 EIS set for 2020, with hopes to advance by six months;

- We undertake a full economic analysis which gives good cues as to the future dominance of Boeing or Airbus in this highest margin segment of the market.

A380, a deep analysis of its competitiveness

By Bjorn Fehrm

Subscription required.

Introduction

Dec. 18, 2014: In our Monday article we go behind the scenes of the doubts that were spread over the A380 by Airbus last week. To complete the picture we now update our competitive analysis that we did in February this year. We then compared the A380 to Boeing’s 747-8i, the 777-300ER and the forthcoming 777-9X. We also included Airbus closest aircraft, the A350-1000.

![]() A lot has happened since then. Airbus has done a lot of work on the passenger area of the A380 to offer increased passenger densities and the pictures of the emerging Boeing 777-9X and Airbus A350-1000 is now clearer.

A lot has happened since then. Airbus has done a lot of work on the passenger area of the A380 to offer increased passenger densities and the pictures of the emerging Boeing 777-9X and Airbus A350-1000 is now clearer.

Sales efforts of the A380 has also progressed, with meager results despite adding a leasing proposition what should make the hurdles of operating a small sub-fleet of A380s lower. To understand why, we interviewed Mark Lapidus, the CEO of Amedeo, the leasing company which specializes in financing and leasing of A380s. We wanted specifically to talk to Lapidus about the reactions of the airlines to the A380 and what problems he saw in selling an aircraft of this type.

In preparing the article we also gathered additional info from Airbus and Boeing, from the former around their work on the cabin configurations and densities, from the latter the maintenance costs for the up and coming 777-9X.

Summary

- In our February article we established that an A380 is roughly equal on fuel per passenger transported to the benchmark in the present non-VLA long haul market, the Boeing 777-300ER. We also found that this is highly dependent on how many passengers one assumes for both aircraft in the comparison.

- We could also see that come 2020, when the replacement of the 777-300ER would be available, the 777-9X, A380 would trail with up to 20% in fuel efficiency, once again dependent on how many seats were used in the comparison.

- At the time we only looked at a fuel consumption comparison; we did not include crew cost, maintenance costs, landing and en route fees to generate Cash Operating Costs (COC) or capital costs to come to Direct Operating Cost (DOC). In today’s updated analysis we add these costs items.

- Finally we have talked with Amedeos CEO Mark Lapidus, asking about his discussions with the Airline CEOs and their teams, to understand what the reactions are from the airlines and why has he not placed any A380 with customers yet.

As we did this deeper study, a more nuanced and different picture emerged from the one seen in February. The results busts a number of deeply engraved myths, one being that four engines are more expensive to fly and maintain than two.

737 MAX 8 could be enabler for some LCC Long Haul

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Introduction

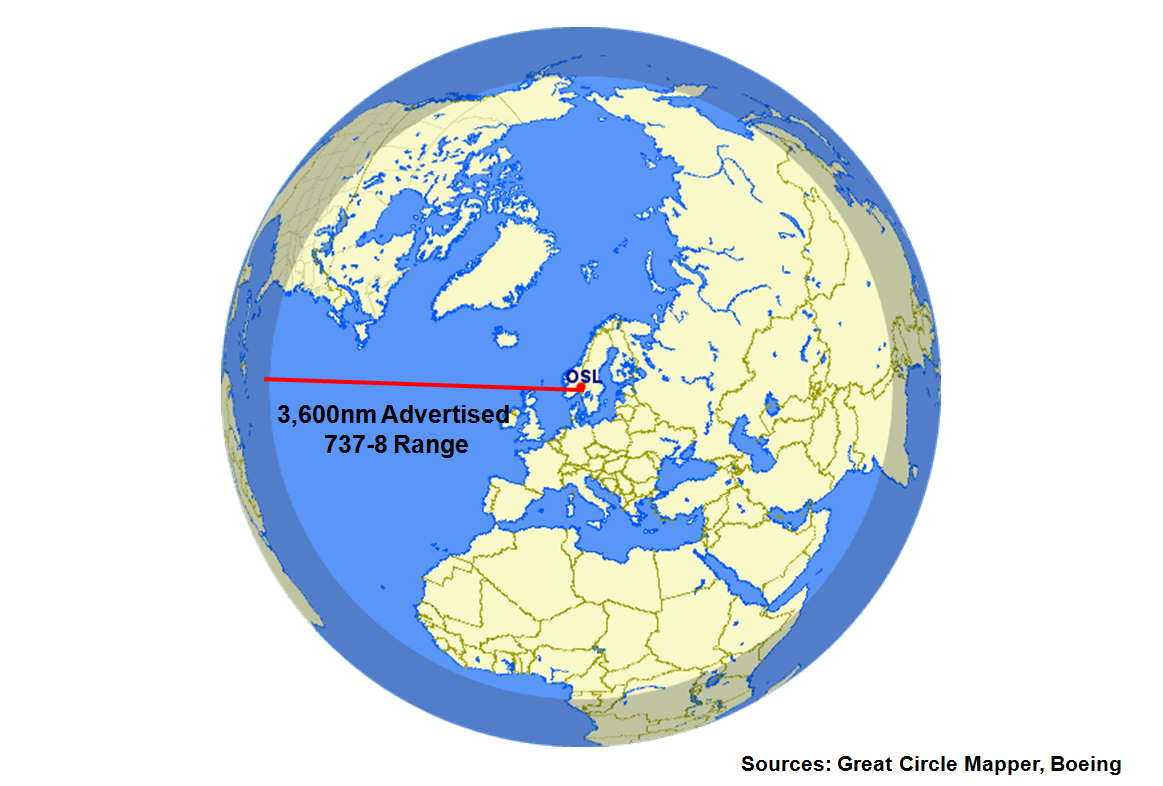

Figure 1. Nominal range of 737 MAX 8 from Oslo Source: Great circle mapper, Boeing. Click on Image to enlarge

Dec, 8, 2014:The Boeing 737-8 MAX is the successor to the 737-800 and has largely been thought of in this context.

Our analysis, prompted by Norwegian Air Shuttle (NAS) plans to use Boeing 737-8 MAXes to begin trans-Atlantic service on long, thin routes, comes up with a conclusion that has gotten little understanding in the marketplace: the 8 MAX has enough range and seating to open a market niche below the larger, longer-legged 757, and the economics to support profitable operations for Low Cost Carriers interested in some trans-Atlantic routes or destinations beyond the range of the -800.

Summary

- We based our analysis on our proprietary, economic modeling, assumed Norwegian cabin configuration standards.

- We compared the operating costs of the 737-8 with Norwegian’s present long haul aircraft 787-8 in a similar cabin configuration.

- The comparison range is the max endurance range for an LCC long haul 737-8, eight hours or 3,400nm air distance (no wind included).

Fundamentals of airliner performance, Part 5; Approach and landing

By Bjorn Fehrm

Dec. 2, 2015: The time has now come to cover descent and landing in our ![]() articles around airliner performance. As many aspects of descent are similar to climb we will repeat a bit what we learned in Part 4:

articles around airliner performance. As many aspects of descent are similar to climb we will repeat a bit what we learned in Part 4:

- For high speed operation the pilots fly on Mach as this gives him maximum information around possible effects on the aircraft when he is close to the high speed limit, the maximum Mach number. Beyond this the aircraft gets into supersonic effects like high speed buffeting or unsteady flight.

- For operations under the cross over altitude for Mach 0.78 to 300 kts IAS the pilot flies on Indicated Air Speed (IAS) which gives him maximum information how the aircraft reacts should he go close to the aircraft’s lower speed limits.

Lets now start to go through the steps that our 737 MAX 8 performs after leaving its cruise altitude.

MTU investors day: views of its engine programs, future airplane timelines; separately, Embraer COO interview

Figure 1. Technical milestones have been passed on PW GTF programs for the applications on Bombardier, Airbus, Mitsubishi and Irkut airplanes and are approaching for Embraer. Source: MTU Investors Day. Click to enlarge.

Nov. 30, 2014: MTU Investors Day: MTU is a major participant in engine development and supplies, participating on the GEnx, GTF and GEnx program. It’s also a member of the joint venture in International Aero Engines and it’s a major player in the aftermarket Maintenance, Repair and Overhaul (MRO) sector, providing a serious competitive alternative to the aftermarket contracts offered by the engine OEMs. Its held an investors day conference Nov. 25. Highlights included:

- Milestones have been passed on the Pratt & Whitney Geared Turbo Fanengine for the Bombardier CSeries, Airbus A320neo family, the Mitsubishi MRJ and Irkut MC-21; and are on schedule for the Embraer E-Jet E2.

- The success of the GTF is requiring huge production commitments.

- The large number of airplane/engine programs require a major ramp-up of production during the next few years.

- The major investment in new engines is largely over for now, leading to the expectation of long-term revenue from MRO.