Leeham News and Analysis

There's more to real news than a news release.

Lufthansa fleet exec praises top-level change at Bombardier

Feb. 13, 2015, c. Leeham Co.: The appointment of Alain Bellemare as president and chief executive officer of Bombardier is viewed positively by the largest and most influential customer for the slow-selling CSeries, Lufthansa Airlines Group.

Nico Buchholz, EVP Fleet Management, Lufthansa Group.

Lufthansa has a firm order for 30 CSeries and options for 30 more. The Group’s subsidiary, Swiss, is to get the firm orders. The market anticipates that the Group could eventually exercise options for its other subsidiaries.

Nico Buchholz, executive vice president for fleet management for the Group, told Leeham News and Comment today that he has worked with Bellemare as a supplier-customer for years in his previous position as an executive of Pratt & Whitney.

Boeing 757 MAX: why its operating economics does not work

By Bjorn Fehrm

Introduction

Feb 12, 2015: In a series of articles during the autumn we covered the replacement scenarios for Boeing’s 757-200 when used for long haul passenger operations. The series also included an interview with Boeing’s head of new airplane studies, Kourosh Hadi, director of product development at Boeing where he outlined what Boeing studied and why.

This week The Wall Street Journal published an article portraying that Boeing seriously considered launching a re-engined 757 as a response to Airbus A321LR. Boeing has since vehemently denied the story and we have given the reasons why it does not make sense for Boeing.

As a complement we show the operational economical analysis that we did at the time of our 757 articles, now updated to the exact modifications suggested by The WSJ, a new engine and new winglets paired with modern avionics.

Regional operations with the Turboprop, prop-jet or Jet

- We examined the future of turboprop airliners Jan. 5, 2015, analyzing the backlogs of Bombardier and ATR–and the ATR overwhelming dominance of the current turboprop sector. This is the second of a series looking at this sector.

By Bjorn Fehrm

Subscription required

Introduction

08 Feb 2015: Passenger traffic is growing the world over on a regional, domestic and international level. For domestic and international airlines the choice of mainline transport aircraft is clear today: there are only two vendors, Boeing and Airbus, and they produce similar products.

For regional transportation there is more choice. First of all, one can chose type![]() of aircraft, turboprop or jet. Within jet, there are several OEMs that are active. The choice in turboprop is more restricted. In practice, the choice stands between the classical turboprop with ATR and a faster type from Bombardier, the Q400 “Prop-Jet” as it is called, as its speed lands between the classical turboprop and regional jet.

of aircraft, turboprop or jet. Within jet, there are several OEMs that are active. The choice in turboprop is more restricted. In practice, the choice stands between the classical turboprop with ATR and a faster type from Bombardier, the Q400 “Prop-Jet” as it is called, as its speed lands between the classical turboprop and regional jet.

The question is, what are the real differences between them in terms of design, passenger comfort and economics and what is the right choice for a market segment? We will take a deeper look into this by analyzing the ATR72 as the classical turboprop, the Bombardier Q400 as the Prop-Jet and CRJ700 as the regional jet.

Summary:

- The ATR72-600, Bombardier Q400 and CRJ700 are all about the same size, around 70-80 seats single class or 60-70 seats dual class.

- They offer different comfort levels, and it is not all about speed.

- In developing the economics in two steps we seek the crossover points between the different types.

Exclusive: Emirates Airlines gets pitch for 100 Boeing 747-8s

- Update, 3:30pm PST: For those who may not be adept at reading literally what was written, we did not say Boeing made the pitch.

Feb. 4, 2015: In a pitch designed to save the Boeing 747-8 and simultaneously kill the prospect of an Airbus A380neo, Emirates Airlines has received a pitch for 100 of the slow-selling Boeing, two sources familiar with the situation tell Leeham News and Comment (LNC). This is isn’t yet a formal proposal, as far as we know.

Tim Clark, president of Emirates, said he would buy 100 A380s if Airbus re-engined and launched the neo. The neo would use the new Rolls-Royce Advance engine, according to two different sources. Neither Pratt & Whitney nor GE Aviation, which dominate the current A380 engine market share with its joint venture Engine Alliance GP7200, are interested in developing a new engine for the prospective A380neo, according to public statements by both companies. PW doesn’t offer an engine alone that could be adapted to the size required for the A380neo. GE’s GEnx engine, used on the Boeing 787, is in the thrust and size bracket but would only improve the efficiency with 4-5%, thus not worth the change effort. The smaller version of the GEnx is on the 747-8. Read more

First analysis of Mitsubishi Regional Jet, MRJ

Subscription required

By Bjorn Fehrm

Introduction

25 Jan 2015: Japan has not produced a commercial aircraft since 1973, when the last YS-11 twin engined turboprop rolled off the assembly line. The YS-11 was developed by a consortium of Japanese “heavies,” where two are also active in the creation of ![]() the MRJ, Mitsubishi Heavy Industries and Fuji Heavy Industries. This time Mitsubishi Heavy Industries is very much in command as they own 64% of the company set up to develop, assemble and market the aircraft, Mitsubishi Aircraft Corporation, Fuji Heavy Industries are working as design consultants this time.

the MRJ, Mitsubishi Heavy Industries and Fuji Heavy Industries. This time Mitsubishi Heavy Industries is very much in command as they own 64% of the company set up to develop, assemble and market the aircraft, Mitsubishi Aircraft Corporation, Fuji Heavy Industries are working as design consultants this time.

Figure 1. Mitsubishi MRJ90 starting its Pratt & Whitney GTF engines for the first time. Source: Mitsubishi.

The first MRJ prototype has run its engines 10 days ago and is preparing for first flight later in the spring. It is therefore time to take a closer look at the first model, MRJ90, and compare it to its direct competitor, Embraer 175 E2.

Summary:

- The MRJ90 and E-Jet 175 E2 are the same size, around 90 seats single class or 80 seats dual class;

- Both aim for scope clause acceptance at 76 seats despite being to heavy; and

- They are different in their fuselage packaging but surprisingly similar in their capabilities.

Fundamentals of airliner performance, Part 6; The engine

By Bjorn Fehrm

19 Jan 2015: There is a lot written about the fundamentals of how aircraft fly. It is something that fascinates people and it generates a high level of understanding of these fundamentals. The same is not true for the airline turbofan engines in use today; their detailed function remains a bit of black art.

![]() To some extent this might be because what is exiting in the engines (the thrust) is generated behind closed doors. The only visible part of the process is a rotating fan face and sometimes a slight miss-colored exhaust out the other way. There is also at takeoff a funny buzzing sound interspersed with the general engine noise. Apart from that, the most that one sees is a round nacelle and that is it.

To some extent this might be because what is exiting in the engines (the thrust) is generated behind closed doors. The only visible part of the process is a rotating fan face and sometimes a slight miss-colored exhaust out the other way. There is also at takeoff a funny buzzing sound interspersed with the general engine noise. Apart from that, the most that one sees is a round nacelle and that is it.

Airbus reveals record orders at annual press conference

By Bjorn Fehrm

Toulouse 13 Jan 2015: Airbus today held their annual press conference where they among other things revealed their final numbers for orders and deliveries. The press conference was hosted by Airbus CEO Fabrice Bregier accompanied by COO Customers John Leahy, new COO Tom Williams and new Head of Programs Didier Evrard.

Airbus in 2014

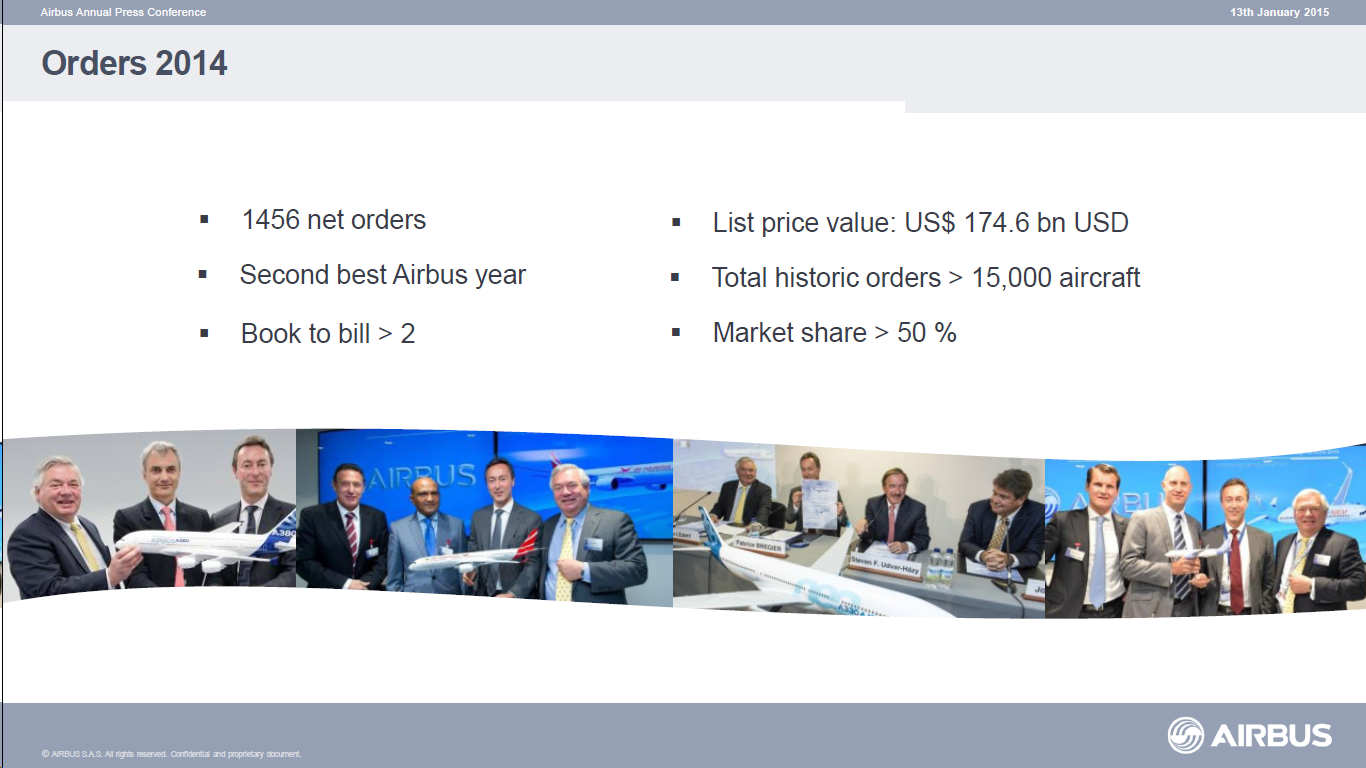

Bregier started with pointing out that 2014 was a very eventful year for Airbus. Airbus did their customary end of year sprint and passed Boeing for net orders with 24 aircraft netting 1456 commands, Figure 1.

Figure 1. Airbus orders for 2014. Source: Airbus.

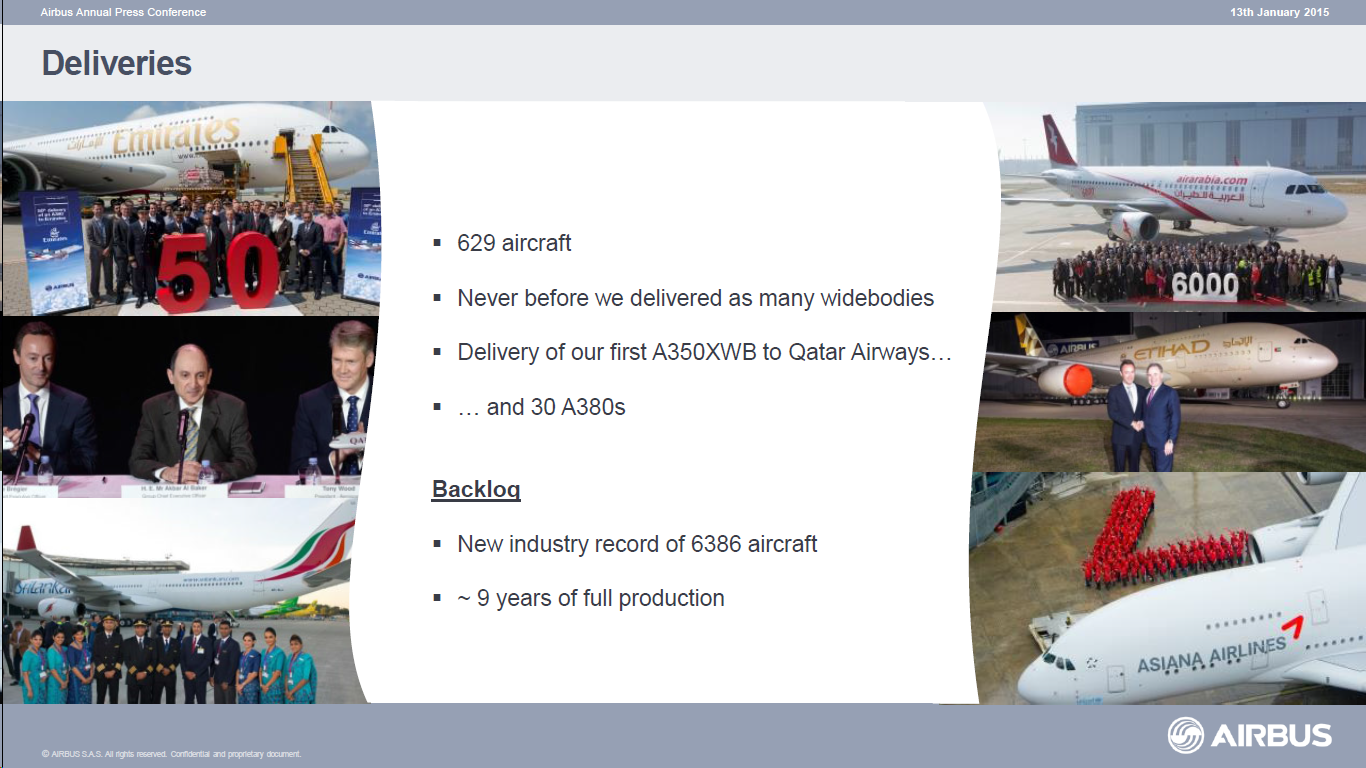

On the delivery side Boeing is ahead with 723 deliveries versus Airbus 629, Figure 2.

Figure 2. Airbus deliveries for 2014. Source: Airbus.

Further Airbus certified the A350 and delivered the first aircraft to its launch customer, Qatar Airways. It also launched the A330neo and got 120 orders during the year. Finally they flew the A320neo first prototype.

A380neo decision likely this year, triggering the next widebody engine project

Subscription required

By Bjorn Fehrm

Introduction

Jan. 12, 2015: One of the subjects which is sure to come up on Airbus annual press conference on Tuesday the 13th in Toulouse will be when and how Airbus will re-engine the A380.

Airbus Commercial CEO Fabrice Bregier vowed during the Airbus Group Global Investors Day last month that an A380neo is coming.

There is much speculation around this subject as the business case of re-engineering an aircraft that is selling at such low numbers is difficult to get to close. The business case is difficult to make work for Airbus ![]() (such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

(such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

Summary

- A380 Classic equals Boeing 777-300ER seat fuel costs.

- Boeing 777-9 beats A380 on CASM, an A380neo regains the advantage.

- Engine makers face hard choices to retain dominance or to broaden market penetration.