Leeham News and Analysis

There's more to real news than a news release.

The ascent of the Big Three Chinese carriers

Subscription Required

By Vincent Valery

Introduction

Jan. 18, 2021, © Leeham News: As the COVID-19 outbreak spread throughout China in January last year, their airlines were the first hit by the sudden collapse in passenger traffic. Most of the world’s carriers would follow the same faith by March.

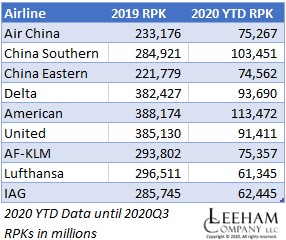

However, as China managed to bring the COVID-19 outbreak under control, domestic traffic progressively picked up. According to IATA statistics, October 2020 Revenue Passenger Kilometers (RPMs) in domestic China were down 1.4% year-over-year, compared with a 60.7% decline in the domestic USA market. However, one should note that travel between China and the rest of the world remains very limited, notably due to the draconian quarantine requirements on arrivals from abroad.

Due to the faster recovery in domestic passenger traffic, China Southern Airlines had more RPKs year-to-date than Delta and United, only trailing American Airlines. Air China and China Eastern Airlines have had comparable year-to-date RPKs with Air France – KLM, and more than Lufthansa and IAG. Below is a summary chart:

The three carriers received significant financial support from the Chinese government to sustain their operations.

The COVID-19 pandemic will likely accelerate the big three Chinese carriers’ global importance compared with their equivalents in the USA and Europe. With that in mind, LNA analyzes their structure and financials in recent years.

Summary

- Three state-owned enterprises;

- The specific structure of each carrier;

- Varying financial performance;

- Ambitious growth plans.

Outlook 2021: Despite vaccines, COVID-19 will continue to dominate aviation in the coming year

Subscription Required

By Judson Rollins

Introduction

Vaccine containers in an air freight container. Source: UPS.

Jan. 4, 2021, © Leeham News: Recent approval of two major vaccine candidates are driving euphoria among aviation investors, employees, and travelers. Many commentators are talking about a “return to normal” later this year.

Alan Greenspan’s famous phrase, “irrational exuberance,” comes to mind. Vaccine approvals provide reason for hope, but not in the near term. Even Singapore’s government, one of the world’s most efficient, says it will need most of 2021 to fully vaccinate its population.

On the other end of the economic spectrum, Duke University’s Global Health Institute says low-income countries may have to wait until 2024 if high-income countries continue to reserve vaccines for their own populations.

Pharmaceutical giants Pfizer, Moderna, and AstraZeneca, which have released efficacy data on their vaccines and are now obtaining approval from various jurisdictions, announced a combined capacity to produce vaccines for up to 3.1bn people by the end of 2021. China’s Sinovac claims it will be able to produce 600m doses, but it is still evaluating the efficacy of its vaccine candidate.

Summary

- Reluctance to take vaccine likely to slow rollout

- Borders re-opening depends on rollout, proof of vaccination

- Pre-travel testing may be a dubious solution

- Business, leisure travel likely to be permanently impacted

- Airline financial woes likely to continue

- New aircraft demand will stay low in 2021

Pontifications: 2020 Retrospective–the worst ever seen

By Scott Hamilton

Dec. 21, 2020, © Leeham News: This is my last Pontification of 2020. I’ll be off between the Christmas and New Year’s holidays.

It’s only fitting to look back at what is the worst year in commercial aviation—ever.

I’ve just completed my 41st year in this industry. I’ve seen two Gulf Wars, SARS, 9/11, the Great Recession and several economic cycles.

Lockheed and McDonnell Douglas exited the commercial airliner business.

I’ve seen three groundings: the McDonnell Douglas DC-10, Boeing 787 and 737 MAX. I’ve been on site of two significant crashes: the American Airlines DC-10 in Chicago and Delta Air Lines’ 727 in Dallas. I flew over a third, a Delta L-1011 in Dallas the day after it happened.

I worked for the first new airline certified by the Civil Aeronautics Board in 40 years, the first Midway. I also went through one bankruptcy and one merger, each part of the deregulation shake-out.

As a reporter, I covered some of the business giants, including Bob Crandall, Herb Kelleher, John Leahy and others.

It’s been a great four decades.

But nothing compares to the global industry disaster of 2020.

A year of reckoning for Low-Cost Long-Haul

Subscription Required

By Vincent Valery

Introduction

Dec. 7, 2020, © Leeham News: Since the beginning of the COVID-19 outbreak, numerous carriers have either ceased operations or gone into court-supervised restructurings. Among those undergoing restructurings are the world’s two largest low-cost long-haul airlines, AirAsia X and Norwegian Air Shuttle.

Both carriers were in a precarious financial condition before the pandemic. Their troubles contrast with the financial solidity of some major low-cost airlines, including Ryanair and Wizz Air.

IAG closed its Level base in Paris Orly, while Lufthansa ceased SunExpress Deutschland’s operations. NokScoot, a joint venture between Singapore Airlines and Nok Air, also ceased operations after years of losses.

Before the COVID-19 outbreak, Primera Air ceased operations in 2018. Wow Air and XL Airways folded in 2019. Along with AirAsia X’s and Norwegian’s financial struggles, this raises questions about the viability of the low-cost long-haul business model.

LNA looks at the sequence of events that led to four major carriers’ failure and the viability of their business models.

Summary

- Low-cost long-haul isn’t new;

- Bringing no-frills to the next level;

- Undercapitalized for the level of risk;

- When going mainstream does not work;

- One certainty and a question mark on viability.

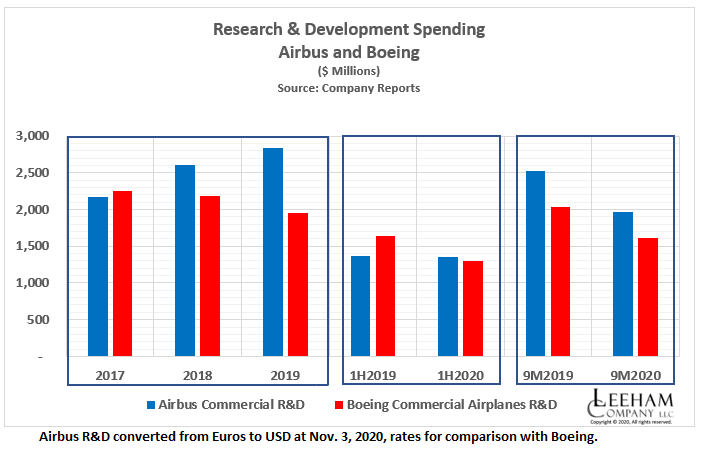

HOTR: Airbus, Boeing R&D spending continues decline

By the Leeham News Team

Nov. 5, 2020, © Leeham News: Research and Development spending by the Airbus and Boeing commercial units declined year-over-year.

The movement is in keeping with cost-cutting by the Big Two OEMs. For Airbus, the reduction is due to the coronavirus pandemic. For Boeing, it’s due  to the 737 MAX grounding and the pandemic.

to the 737 MAX grounding and the pandemic.

Boeing’s spending typically lags Airbus. Richard Aboulafia, a consultant with Teal Group, for years criticized Boeing over its smaller spending, favoring instead shareholder value. Airbus overtook Boeing is innovative single-aisle airplane development years ago. Boeing’s choice of creating a 777 derivative instead of a new design to compete with the A350-1000 proved to be a weak move. There are only a handful of customers and the skyline is weak.

Lessors to Take Growing Share of Fleeting the Future

By Kathryn B. Creedy

Air Lease Executive Chair Steven Udvar Hazy expects lessors to play a larger role in aircraft fleeting in the future, according to comments made during yesterday’s Aviation Week Fireside Chat with the lessor.

“I don’t see lessors going below 40%,” he told Air Transport World Editor Karen Walker. “I see it creeping up to perhaps 50% or 55% and that includes operating leases and various other exotic mechanisms.”

Udvar Hazy pointed to the poor financial shape of the world’s airlines which have used all their current levers to increase liquidity to ride out the Covid 19 crisis.

Pontifications: Winter is coming

By Vincent Valery

Sept. 28, 2020, © Leeham News: The end of September marks the time when airlines in the Northern Hemisphere assess their summer season financial performance. Depending on the outcome, they adjust their capacity and evaluate their cash needs to see through the lower demand winter months.

This summer was significantly different from what airlines envisioned earlier this year. They had to re-arrange schedules on short notice to capitalize on the uptick in passenger demand after the lifting of some travel restrictions put in place during Spring.![]()

With a resurgent COVID-19 spread in some countries and the re-establishment of movement restrictions, airlines need to, once again, adjust their plans for winter months.

The engine manufacturers worst hit by the pandemic

Subscription Required

By Bjorn Fehrm

Introduction

September 28, 2020, © Leeham News: The worldwide COVID-19 pandemic is shaking the air travel and airliner manufacturing industries like no crisis before.

More than 9/11, the oil crisis of 1973 or 2005 or the financial crisis of 2008. The problems for the airlines and the airframe OEMs are on the front pages of the world’s media.

The part of the airliner industry that is not so visible but is perhaps hardest hit, is the engine industry. Its weird business model amplifies the effects of the crisis.

Summary

- Airframe OEMs lose money on the first hundreds of aircraft produced.

- When they announce “black numbers”, it means the per aircraft losses stop. It doesn’t mean the aircraft program is positive.

- For engine OEMs, it’s worse. They never reach ‘black numbers” on engine production. Their only money makers are old engine programs that fly a lot.

HOTR: Boeing bear case: $73bn revenue drop 2020-2025

By the Leeham News Staff

Sept. 9, 2020, © Leeham News: Morgan Stanley has a new aerospace analyst, Kristine Liwag, who initiated coverage on a half dozen companies over two days last week.

Among them, of course, was Boeing.

One of the conclusions in one of her notes:

“Assuming that some orders for growth and those ordered by lessors are cancelled in the 2020-2025 timeframe, we estimate that there is $73bn downside risk to Boeing’s revenue from 2020-2025. We note that our Bull case scenario assumes that the entire current order book converts to revenue.”

Liwag and her team also write, “there is an underappreciated risk that Boeing is particularly vulnerable to cancellations as the 737 MAX grounding (March 2019) opened up cancellation rights (without penalty) for aircraft deliveries that were delayed a year.”

But Morgan Stanley doesn’t let Airbus off the hook

“Boeing and Airbus manufacture aircraft to an order book. White tails, which are aircraft without owners, are uncommon and undesired. When demand is strong and the production skyline is sold out, as we have seen in the past few years, a new aircraft is a scarce commodity that airlines and lessors want. In times of uncertainty, a new aircraft, with a capital cost of $50mn-$200mn per unit, becomes a white elephant.”

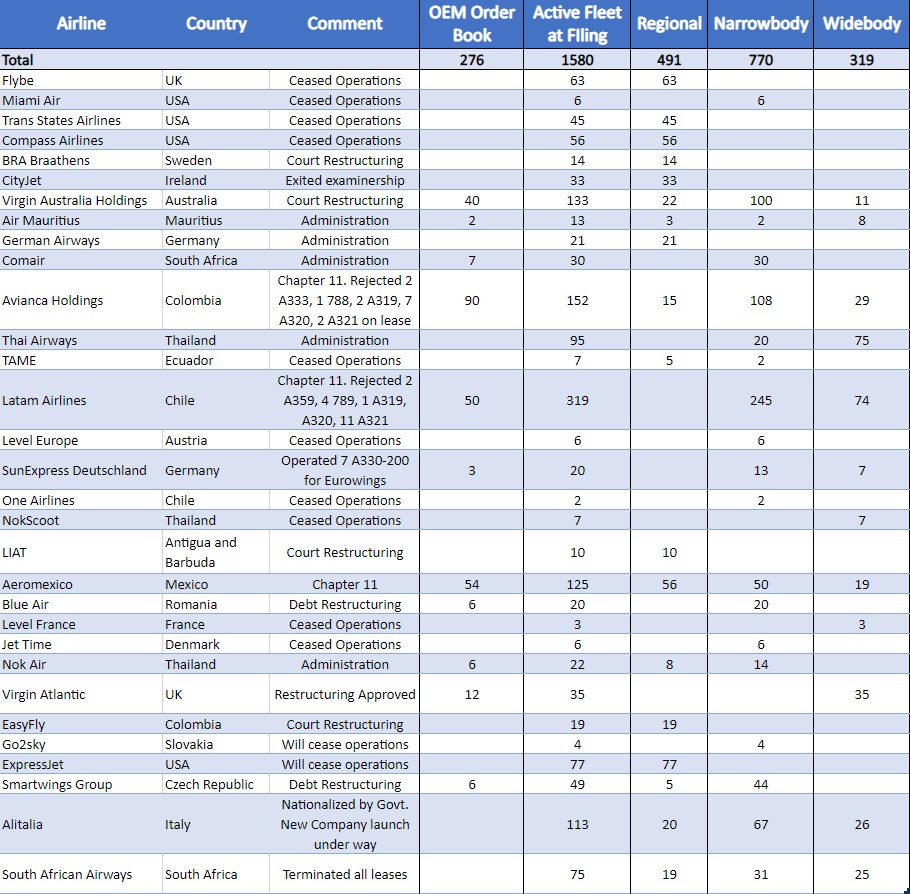

HOTR: Five more airlines under court restructuring or ceasing operations

By the Leeham News Staff

Aug. 31, 2020, © Leeham News: The Smartwings Group is the latest airline to file for a court restructuring.

LNA’s monthly tracking of failed carriers adds Virgin Atlantic, EasyFly, Go2Sky, ExpressJet, and the Smartwings Group to the list of carriers in bankruptcy or court-supervised restructuring since COVID collapsed the global airline industry beginning in mid-March.

Among those five, Go2Sky and ExpressJet announced that they would cease operations. Virgin Atlantic won the support of its creditor for a court-supervised restructuring.