Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Does an A220-500 need a new wing and engines? Part 4. July 3, 2025

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

2015 a year of execution for Embraer commercial

Subscription Required

Introduction

Jan. 7, 2015: Embraer, the world’s #3 commercial airplane manufacturer, ![]() enters 2015 viewing this as a year of execution, says its chief commercial officer, John S. Slattery.

enters 2015 viewing this as a year of execution, says its chief commercial officer, John S. Slattery.

There are three pillars:

- Continuing to fill out the balance of the current generation orders and commitments in advance of the E-Jet E2 re-engined airplane scheduled for entry-into-service in 2018;

- Execution to continue to grow the commitments for the E2—there are already 590; and

- Execution for the next several years for the milestones of the E2 development.

Summary

- Customer base goal by the end of 2017;

- Customer support;

- Barriers to entry for competitors.

New and Derivative airplanes: Some good, some not; Part 1

First of two parts.

Earlier this year, Airbus officials said they will concentrate on improving existing airplanes once the A350 enters service.

Boeing followed by saying it would not take any “moonshots” and develop new airplanes, at least for some indeterminate time.

The sentiment on the part of both companies is understandable if not disappointing for aviation purists who want to see new and innovative airplane models rather than made-over sub-types.

This is one of those cases where both schools of thought are right. (Text continues below photo.)

Later this month, we will unveil a new, updated Leeham News and Comment with a combination of paid and free content. Watch this space for more information.

New airplanes are, to state the obvious, very expensive to develop and in this increasingly technological age and demand for “smarter” airplanes that are more fuel efficient and which try to improve passenger experience while cramming as many revenue-paying passengers into the airplane as possible, becoming more and more challenging. Where it once was possible to bring an airplane to market within four years of launch, today airframers routinely look at seven years and even eight. Even derivative airplanes are now taking six or seven years to enter service from launch.

Bombardier woes go beyond CSeries

The news last week that Bombardier reorganized its business units, laid off another 1,800 employees and saw the retirement of Guy Hachey, president and CEO of the aerospace division, was viewed by some media and observers as an indictment of the CSeries program. While it’s certainly true that delays in the program weigh heavily on BBD, the problems don’t stop with CSeries.

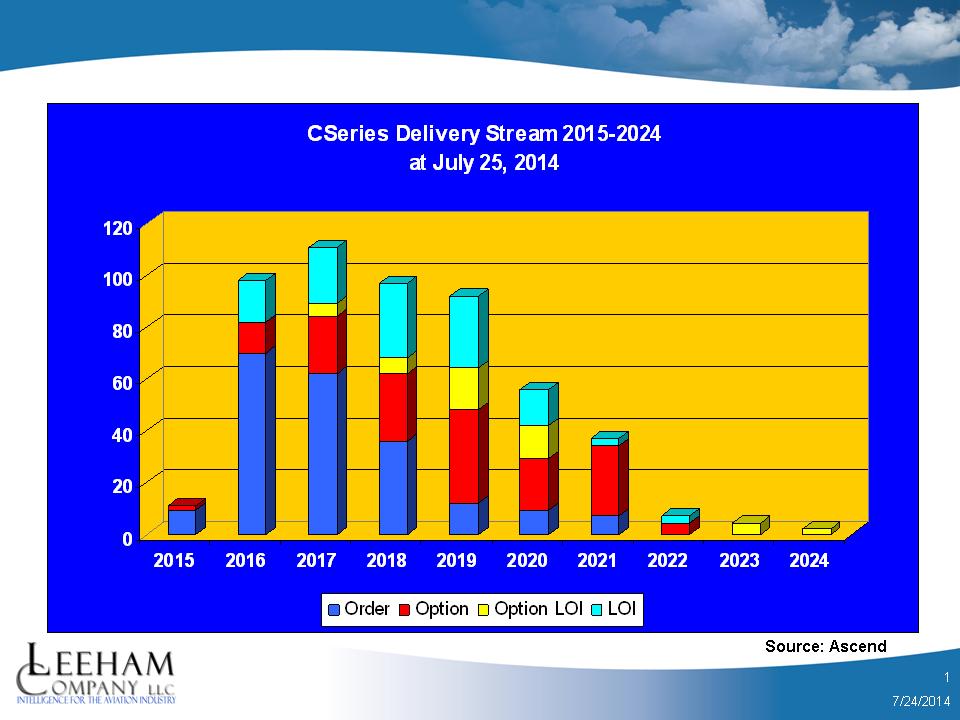

Bombardier has 203 firm orders and 310 commitments for CSeries. This delivery stream doesn’t include any potential rescheduling as a result of the grounding of the Flight Test fleet from May as a result of the engine incident.

Slow sales of the CRJ, Q400 and business jets–as well as program development issues with a new corporate jet–all combined to drag down financial performance and bleed cash. Bombardier doesn’t have the balance sheet strength of Boeing or Airbus, nor strong sales of other airplane family members, to weather the challenges of new airplane development programs.

Leeham News launches Premium plan, companion to free content; engineer joins staff

Free content.

Leeham News and Comment (LNC) today launched a Premium subscription plan as a companion to free content.

LNC has provided news and commentary since February 2008, providing industry-leading information and insightful analysis, principally focuses on Airbus, Boeing, Bombardier and Embraer but also including emerging challengers to the Big Four OEMs, the leading engine manufacturers, suppliers and airline news.

LNC has been a leading resource of news and comment throughout the commercial aviation industry and its professional followers in the aerospace supply chain, investment analysts and the media.

Since the first of this year, LNC increasingly provided more and more technically-based content. This content is valuable and supplements the industry-leading news and reporting that has been provided since 2008. We are pleased to announce the addition to our staff, Bjorn Fehrm, who focuses on technical evaluation and complements the strategic expertise of Scott Hamilton, the founder of LNC and Leeham Co. consultancy.

Read more

16 Comments

Posted on October 14, 2014 by Scott Hamilton

Airbus, Airlines, Boeing, Bombardier, CFM, Comac, Embraer, Irkut, Mitsubishi, Pratt & Whitney, Rolls-Royce, Sukhoi

737-9, 757, 757 replacement, A321NEO, Airbus, Bjorn Fehrm, Boeing, Bombardier, CFM, Comac, Embraer, Irkut, Leeham News and Comment, Mitsubishi, Pratt & Whitney, Rolls-Royce, Sukhoi